July 13, 2026

The Global Race for Battery-Grade Spodumene Is Reshaping Where Lithium Gets Mined

For most of the past decade, the mental map of hard-rock lithium production looked remarkably simple: Australia dominated spodumene output, the Atacama salt flats anchored brine-based supply, and China controlled the conversion capacity sitting between raw ore and battery-ready chemistry. That concentration of supply across so few geographies has become one of the most discussed structural risks in the clean energy transition. Battery manufacturers, automotive groups, and sovereign governments alike are actively searching for credible alternatives, and increasingly, that search is leading to an unexpected destination: the interior highlands of southeastern Brazil.

The Jequitinhonha Valley in Minas Gerais State sits at the centre of what geologists have described as one of the world's most significant untapped lithium-bearing pegmatite corridors. Pegmatite geology is critical here because hard-rock spodumene, unlike its brine-based counterpart, produces a more consistent lithium oxide grade and is generally better suited to the Dense Media Separation (DMS) processing pathway preferred by many chemical converters. The region has attracted growing exploration activity, but one project has moved furthest along the development curve: the Atlas Lithium Neves project, which is now targeting commercial production of battery-grade lithium oxide concentrate by the fourth quarter of 2027.

When big ASX news breaks, our subscribers know first

Understanding Spodumene Concentrate and Its Role in the Battery Chain

Before assessing the Neves project's commercial significance, it helps to understand precisely where spodumene concentrate sits within the broader lithium supply architecture. The distinction between hard-rock vs brine lithium is fundamental here, as lithium does not travel directly from mine to battery. Instead, it moves through a multi-stage processing chain:

- Hard-rock spodumene ore is extracted via open-pit mining methods from pegmatite formations.

- The ore is crushed and processed through Dense Media Separation, a gravity-based beneficiation technique that separates spodumene mineral particles from gangue material using a heavy liquid medium.

- The output is battery-grade spodumene concentrate, typically carrying 5.5% to 6.5% Li₂O content by weight.

- This concentrate is then shipped to lithium chemical converters, primarily located in China and increasingly in South Korea and Japan.

- Converters subject the concentrate to roasting and leaching processes to produce either lithium hydroxide monohydrate or lithium carbonate, the two battery-grade chemicals that ultimately enter cathode active material manufacturing.

"Spodumene concentrate is not the finished product that enters an electric vehicle battery. It is the upstream feedstock upon which the entire lithium chemicals industry depends. A project that can reliably deliver high-grade concentrate at competitive cost occupies a structurally advantaged position in the supply chain."

DMS was selected for the Neves project because it is a proven, modular technology with a well-understood cost profile in spodumene applications. Furthermore, modular DMS plant configurations allow capacity to be expanded in phases without requiring a complete redesign of existing processing infrastructure, a feature that directly supports the project's phased growth ambitions.

The Neves Project: Core Metrics and What They Mean in Practice

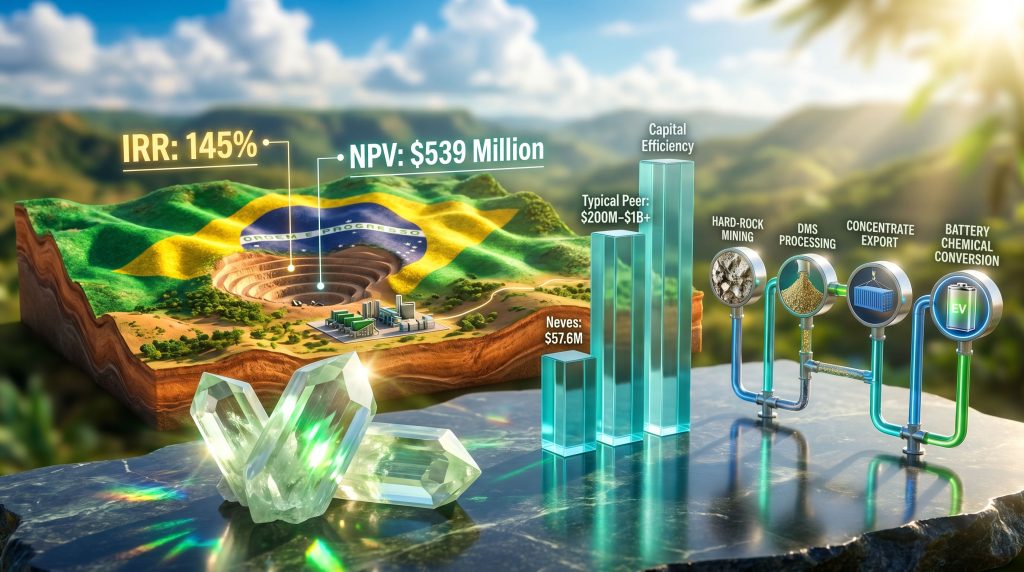

The definitive feasibility study completed for the Neves project establishes a financial and operational profile that stands apart from most hard-rock lithium developments currently in the pipeline globally. The key figures are presented below.

| Financial and Operational Metric | Neves Project DFS Figure |

|---|---|

| Phase 1 Annual Production Capacity | ~150,000 tonnes of spodumene concentrate |

| DFS Steady-State Output | ~146,000 tonnes/year |

| Phase 2 Expansion Target | 300,000 tonnes/year |

| Internal Rate of Return (IRR) | 145% |

| Project Payback Period | 11 months |

| Net Present Value (NPV) | $539 million |

| Direct Capital Cost | $57.6 million |

| Mine Gate Operating Cost | $489 per tonne |

| DFS Benchmark Market Price | ~$2,300 per tonne |

| Metallurgical Recovery Rate | 61.7% |

| Target Commercial Production | Q4 2027 |

The 145% IRR figure is the metric most likely to attract scrutiny from experienced mining investors, and understandably so. IRR figures at this level are almost never associated with conventional mine development. What explains it in this case is the combination of a comparatively modest direct capital cost of $57.6 million against an operating cost of $489 per tonne and a DFS benchmark market price of approximately $2,300 per tonne.

That spread of roughly $1,800 per tonne of operating margin, applied across 146,000 tonnes of annual output, generates cash flows that rapidly recover the initial capital outlay. Atlas Lithium's Neves project produces lithium oxide concentrate with a financial profile that genuinely stands out in the current development landscape.

"An 11-month payback period is genuinely exceptional by the standards of hard-rock lithium development, where recovery periods of three to seven years are considered normal. The combination of low entry capital and wide operating margins is the mathematical driver, but the underlying enabler is the project's geological endowment and its location within a mineralised corridor that reduces both stripping ratios and haul distances."

The metallurgical recovery rate of 61.7% warrants some context. DMS-based spodumene projects typically achieve recoveries in the 60% to 68% range depending on ore hardness, liberation characteristics, and circuit configuration. The Neves figure sits within the established commercial range, suggesting the DFS was prepared using realistic rather than optimistic recovery assumptions, a meaningful indicator of study quality.

Disclaimer: IRR, NPV, payback period, and production figures presented here are drawn from the company's own Definitive Feasibility Study and represent forward-looking projections subject to commodity price movements, permitting outcomes, construction execution, and market conditions. They do not constitute financial advice.

Engineering Execution: Contracts, Costs, and Construction Progress

Is the Project Tracking to Budget?

One of the most telling signals of a mining project's maturity is not the quality of its financial model but the discipline with which it executes against that model during the pre-production phase. On this dimension, the Atlas Lithium Neves project has provided a concrete data point: every major contract awarded to date has been finalised at or below the cost levels assumed in the DFS budget.

| Contract Scope | Appointed Firm |

|---|---|

| Detailed Engineering | Promon Engenharia |

| Project Management, Cost Control and Risk | TSX Engineering |

| Engineering, Procurement and Construction (EPC) | Cerne Construções |

| Earthworks and Civil Construction | RETC Infraestructura |

| Electromechanical Assembly | Alfa Engenharia |

This contract execution discipline matters enormously in a sector where cost overruns routinely erode project economics. When every awarded contract comes in at or under the budgeted figure, it validates the accuracy of the DFS cost modelling and reduces the probability of the budget blowouts that have derailed numerous lithium projects during the 2021 to 2024 development boom.

DMS plant equipment has already been delivered to Brazil and is staged for assembly. The processing plant assembly contract awarded to Alfa Engenharia represents a further milestone in de-risking the project's construction timeline. Operational and environmental licences required for construction and mining have both been secured, removing two of the most commonly cited risk factors for junior lithium developers. Permitting timelines in lithium-producing jurisdictions can extend to five years or more in competitive regulatory environments, making the existing licence position a tangible competitive advantage.

Offtake Demand: Why Buyers Are Competing for Neves Concentrate

Perhaps the most commercially significant aspect of the Neves project's current position is the scale of demonstrated buyer interest relative to planned production. Written product interest received from prospective purchasers already exceeds three times the project's Phase 1 annual capacity of 150,000 tonnes. This is not a situation where the project is searching for customers; the opposite problem exists.

Three formal offtake agreements have been disclosed:

| Offtake Partner | Volume Commitment | Notes |

|---|---|---|

| Chengxin Lithium | 60,000 tonnes/year | Major Chinese lithium chemical processor |

| Yahua Industrial | 60,000 tonnes/year | Leading Chinese battery materials supplier |

| Mitsui and Co. | 15,000 t/y (Phase 1) / 60,000 t/y (Phase 2) | Japanese trading house and strategic investor |

The combined confirmed offtake volume from these three agreements totals 135,000 tonnes per year in Phase 1, representing approximately 90% of planned annual output. The Mitsui arrangement deserves particular attention because it extends beyond a simple commercial supply agreement. Mitsui and Co. has committed a $30 million strategic investment alongside its offtake position, a structure that aligns the Japanese trading house's financial interests directly with the project's successful execution.

The participation of both Chinese lithium chemical processors and a major Japanese trading house in offtake competition for the same project's output reflects a broader geopolitical dynamic. Furthermore, as battery supply chains undergo structural review in the context of trade policy shifts and resource nationalism, buyers are actively seeking non-Australian, non-Chinese spodumene supply. Brazil offers geological quality, operational viability, and a jurisdiction that sits outside the most contested nodes of the current critical minerals trade environment.

How Neves Compares to Global Hard-Rock Lithium Peers

Context is essential when evaluating any single project's metrics. The comparison below situates the Atlas Lithium Neves project against the broader universe of DFS-stage hard-rock lithium developments.

| Comparison Dimension | Neves Project | Typical Hard-Rock Lithium Peer |

|---|---|---|

| IRR | 145% | 20% to 50% for most DFS-stage projects |

| Payback Period | 11 months | 3 to 7 years |

| Direct Capital Cost | $57.6 million | $200 million to $1 billion or more |

| Operating Cost | $489 per tonne | $400 to $700 per tonne (project-dependent) |

| Permitting Status | Fully permitted | Often 2 to 5 or more years to permit |

| Offtake Coverage | More than 3x planned capacity in interest | Typically 50% to 100% of planned output |

The capital cost comparison is particularly instructive. Many of the large-scale hard-rock lithium projects that entered development during the 2020 to 2023 period carried direct capital requirements exceeding $500 million, in some cases exceeding $1 billion. At $57.6 million, the Neves Phase 1 capital requirement is dramatically lower, reflecting the modular DMS approach, the quality of the ore body's near-surface mineralisation, and the relatively straightforward processing circuit required.

It should be noted that the $2,300 per tonne benchmark price used in the DFS represents a significant premium above spot lithium concentrate prices that prevailed through much of 2024 and early 2025. The broader global lithium market experienced a substantial correction during this period, and prospective investors should assess the project's economics across a range of price scenarios rather than relying solely on the DFS benchmark. That said, even at materially lower price assumptions, the project's operating cost of $489 per tonne provides a buffer that many higher-cost spodumene operations lack.

The next major ASX story will hit our subscribers first

The Jequitinhonha Valley's Geological and Socioeconomic Significance

What Makes Brazil's Pegmatite Corridor Compelling?

The Jequitinhonha Valley's lithium endowment is rooted in the same Precambrian geological architecture that hosts pegmatite provinces across eastern Brazil. Lithium-caesium-tantalum (LCT) type pegmatites, the class of rock formation that hosts spodumene mineralisation, formed in this region through the crystallisation of lithium-enriched granitic melts during tectonic events hundreds of millions of years ago. The density of pegmatite occurrences in this corridor is one reason Brazil has emerged as a credible alternative to the established Australian hard-rock lithium provinces.

Beyond geology, the socioeconomic dimension of lithium development in this region carries significant weight. The Jequitinhonha Valley has historically been one of the more economically marginalised areas of Minas Gerais State. The Neves project is projected to sustain approximately 5,000 direct and indirect jobs at full operation, a figure that represents a substantial employment base for a region where large-scale industrial activity has been limited. This social dimension also contributes to the project's community licence to operate, a factor that experienced mining investors increasingly treat as a material risk variable.

In addition, technologies such as direct lithium extraction are reshaping how the broader industry thinks about recovery efficiency, and the learnings from such methods continue to influence processing design decisions across hard-rock projects as well.

Atlas Lithium holds approximately 557 km² of mineral rights across Brazil, representing the largest lithium exploration footprint among publicly listed companies operating in the country. The Neves project constitutes the lead asset within this portfolio, but the company's longer-term strategy involves developing additional processing facilities across its broader landholding as global lithium demand scales. Phase 2 at Neves targets a doubling of output to 300,000 tonnes per year, with Mitsui's offtake commitment structured to scale accordingly.

Key Takeaways for Investors and Industry Observers

The Neves project's current development position can be summarised through several distinct lenses:

- Capital efficiency: A direct capital cost of $57.6 million delivering 150,000 tonnes per year of spodumene concentrate output represents one of the most capital-lean development models in the hard-rock lithium sector globally.

- Demand validation: Offtake interest exceeding three times planned Phase 1 capacity signals genuine commercial pull from sophisticated battery supply chain participants, not speculative buyer enquiries.

- Execution discipline: All major contracts awarded at or below DFS budget levels, combined with equipment already on-site, reduces the probability of the cost overruns that have impaired numerous lithium projects during recent development cycles.

- Permitting certainty: Both operational and environmental licences have been secured, removing a category of development risk that has delayed projects in numerous other jurisdictions by years.

- Strategic investor participation: Mitsui and Co.'s $30 million commitment alongside a scalable offtake structure reflects institutional-grade confidence in the project's technical and commercial fundamentals.

- Supply chain positioning: Brazil's emergence as a hard-rock spodumene producer offers global buyers a credible source of geographic diversification away from the Australian-Chinese supply axis that currently dominates the market.

This article is intended for informational purposes only and does not constitute financial or investment advice. All forward-looking projections, including production targets, financial returns, and timelines, are based on company-disclosed feasibility study data and are subject to material risks and uncertainties. Readers should conduct independent due diligence before making any investment decisions.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and commodity data into clear, actionable insights for investors at every level — begin your 14-day free trial today and position yourself ahead of the broader market, or explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns.