May 21, 2026

Why Mid-Tier Miners Are Rethinking Direct Asset Ownership in High-Risk Jurisdictions

The gold mining industry has undergone a quiet but consequential philosophical shift over the past decade. Where mid-tier producers once competed aggressively to accumulate development-stage assets across diverse international jurisdictions, a growing cohort of operators now views the traditional equity-and-operate model as carrying an increasingly unfavourable risk-to-reward ratio. Construction cost overruns, geopolitical instability, currency volatility, and regulatory unpredictability have collectively reframed the calculus around direct asset ownership in emerging market settings. The result is a strategic migration toward financial instruments that preserve production upside while transferring operational and development risk to parties with deeper local expertise and appetite for capital deployment.

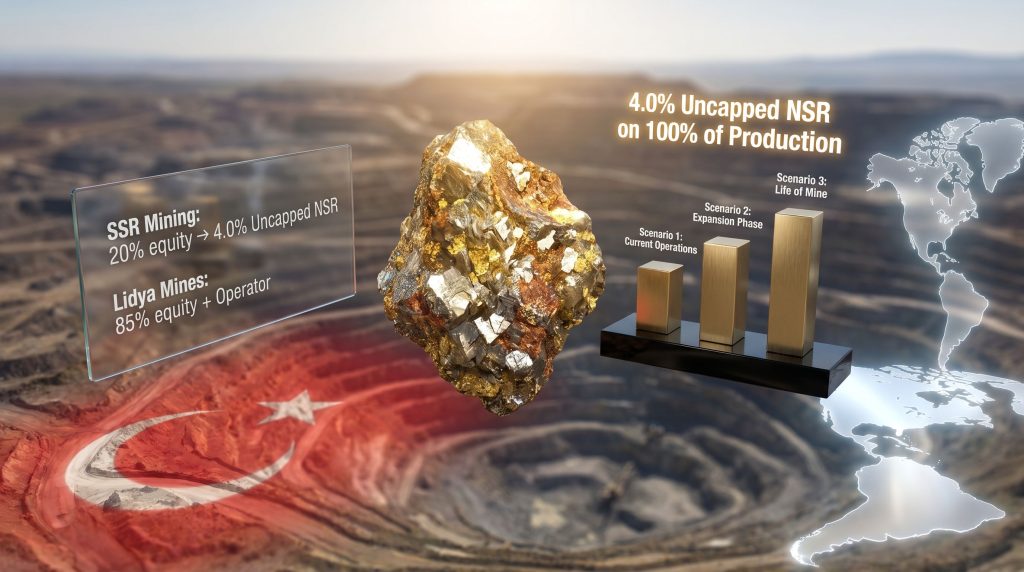

The decision by SSR Mining to sell its stake in Hod Maden exemplifies this broader industry transition. By converting its 20% equity stake and operatorship position in the Hod Maden gold-copper development project in Türkiye into an uncapped 4.0% net smelter return (NSR) royalty on 100% of the project's production, SSR Mining has effectively stepped out of the high-risk operator role and into the position of a passive, production-linked beneficiary. This is not a distressed exit but a deliberate capital allocation decision with significant long-term implications for how investors should evaluate the company.

The Shift From Operator to Royalty Holder: A New Capital Allocation Paradigm

Operating a mine in a politically complex jurisdiction requires constant capital reinvestment, regulatory navigation, and operational management that can consume executive bandwidth disproportionate to the returns generated. Mid-tier producers are increasingly recognising that converting development-stage equity into royalty instruments allows them to reallocate managerial and financial resources toward jurisdictions where they hold stronger competitive advantages, while still maintaining a financial link to the assets they helped advance.

The fundamental logic of a royalty conversion rests on an asymmetric risk-reward proposition. In exchange for relinquishing operational control, the royalty holder surrenders the obligation to fund construction, absorb cost overruns, manage workforce risks, and navigate local regulatory environments. What remains is a perpetual entitlement to a percentage of production revenue, requiring zero additional capital contribution. For a company that has already deployed significant capital into a development-stage project, this structure transforms a sunk-cost equity position into a long-duration, low-maintenance revenue stream. Furthermore, the geopolitical landscape for metals and mining in 2025 has made such conversions increasingly attractive for companies reassessing their emerging market exposure.

What Is a Net Smelter Return Royalty and Why Does Uncapped Matter?

A net smelter return (NSR) royalty is a contractual entitlement to a defined percentage of the gross revenue generated from the sale of mined materials, calculated after deducting processing, smelting, and refining costs. Unlike a net profit interest, which only pays out after all operating costs are recovered, an NSR generates payments as long as the mine is producing and selling ore, making it a significantly more reliable and predictable revenue instrument.

The distinction between capped and uncapped NSR structures is critical for investors evaluating long-duration mining royalties. A capped royalty carries a ceiling on total cumulative payments, after which the royalty obligation extinguishes entirely. An uncapped royalty, by contrast, remains in force for the productive life of the mine, regardless of how much total revenue the project ultimately generates. For high-grade, long-life assets like Hod Maden, the difference between a capped and uncapped structure could represent hundreds of millions of dollars in cumulative receipts over the project's lifetime.

Key structural features of NSR royalties relevant to this transaction include:

- Revenue base: Calculated on gross sales proceeds minus allowable deductions for transport, smelting, and refining, not on net profit after operating costs

- Payment trigger: Activated by production and sale of ore, independent of the operator's overall profitability

- Capital obligation: None for the royalty holder after the initial conversion; all future development and operating capital responsibilities rest with the operator

- Duration: Perpetual for an uncapped royalty, persisting across ownership changes and project restructurings

- Transferability: Royalty instruments can typically be sold, assigned, or used as collateral, providing the holder with additional financial flexibility

When big ASX news breaks, our subscribers know first

What Exactly Did SSR Mining Agree To and What Does It Give Up?

Breaking Down the Transaction Structure

The Hod Maden ownership restructuring involves three parties executing coordinated transactions that fundamentally reshape who bears operational responsibility and who retains production-linked economic participation.

| Party | Pre-Transaction Position | Post-Transaction Position |

|---|---|---|

| SSR Mining | 20% equity + Operator | 0% equity, 4.0% uncapped NSR on 100% of production |

| Royal Gold | ~25% equity partner | 15% equity, 2.5% uncapped NSR on 100% of production |

| Lidya Mines | ~55% equity | 85% equity + full Operator |

The transaction was formally announced on May 18, 2026, with closing targeted for Q3 2026, pending Turkish regulatory approvals and other customary conditions. Upon signing of the definitive agreements, SSR Mining formally resigned as project operator, and all future capital funding obligations transferred entirely to Lidya Mines.

What makes this structure notable from a corporate finance perspective is that SSR Mining received no upfront cash consideration as part of the arrangement. The entirety of the compensation mechanism is the royalty instrument itself. This design reflects a deliberate prioritisation of long-term, production-linked participation over immediate liquidity, and signals that SSR Mining's leadership assessed the future production value of a perpetual uncapped NSR as more valuable than any realistic cash payment that could have been negotiated for a minority development-stage equity stake in an emerging market jurisdiction.

The $243 Million Question: Capital Deployed Versus Value Received

SSR Mining's cumulative capital investment in Hod Maden stands at approximately $243 million. Against this backdrop, the royalty conversion raises a natural question for investors: has SSR Mining effectively written off this investment, or has it converted it into something potentially more valuable?

The answer depends heavily on Hod Maden's eventual production profile. The core scenario analysis breaks down as follows:

Scenario A: Hod Maden advances on schedule

- The 4.0% uncapped NSR generates material long-term cash flows with zero incremental capital requirement from SSR Mining

- Royalty income provides a steady supplement to Americas operating cash flows without equity dilution or increased debt

- The $243 million in prior investment effectively becomes the acquisition cost of a perpetual production-linked asset

Scenario B: Hod Maden faces development delays

- SSR Mining carries no funding obligation and is fully insulated from cost overruns or extended construction timelines

- Royalty payments are deferred but not extinguished; the uncapped structure preserves full upside whenever production ultimately commences

- No additional capital at risk beyond the original $243 million already deployed

Scenario C: Project underperforms or requires restructuring

- SSR Mining's exposure is limited strictly to the royalty instrument; no further equity dilution, no operational liability, no reputational risk from operational failures

- The prior $243 million is effectively reclassified from an active equity position into a contingent long-term asset rather than a stranded cost

- Downside is structurally capped; upside remains unlimited

The risk transfer embedded in this structure is significant. By removing all funding obligations, SSR Mining has eliminated what could have been a substantial future capital call in a jurisdiction where construction timelines and regulatory environments carry meaningful uncertainty.

How SSR Mining Sells Its Stake in Hod Maden as Part of a Broader Americas Pivot

Three Transactions, One Strategic Thesis

The Hod Maden royalty conversion is not an isolated decision. It is the third and final component of a deliberate multi-transaction portfolio restructuring that SSR Mining has executed in rapid succession. Understanding the transaction individually without this strategic context misses the more significant story of what SSR Mining is becoming as a company. In addition, this repositioning aligns with broader mining industry consolidation trends observed across joint ventures and asset sales in 2025.

The three-part repositioning unfolds as follows:

-

Sale of the Çöpler mine in Türkiye: This transaction removed SSR Mining's single largest source of operational and geopolitical exposure in the region. The Çöpler mine had previously experienced significant operational disruption, making its continued ownership a persistent source of investor concern and corporate management distraction.

-

Acquisition of Cripple Creek and Victor (CC&V) in Colorado, USA: The CC&V mine is an established producing asset located within a well-developed mining district in a politically stable, infrastructure-rich jurisdiction. This acquisition established SSR Mining's beachhead for its Americas-focused operating platform.

-

Hod Maden royalty conversion: This final move completes SSR Mining's full exit from Türkiye while preserving economic participation in a high-grade gold-copper development project that may generate substantial production value over its operational life.

Together, these three transactions accomplish a clean and complete geographic pivot. SSR Mining has transitioned from a globally distributed operator with meaningful Turkish exposure into a focused Americas mining company that also holds a valuable royalty instrument linked to a Turkish development project.

What the Hod Maden Project Brings to the Royalty Book

Hod Maden is a high-grade gold-copper development project located in Türkiye, with Lidya Mines now holding 85% ownership and full operational responsibility. The project's development trajectory has involved multiple ownership restructurings, which is not unusual for large-scale mining assets in emerging market jurisdictions where financing complexity, permitting timelines, and operational expertise requirements frequently necessitate partner changes before construction commences.

Lidya Mines brings deep in-country operational familiarity to the Hod Maden project, which is a key reason the ownership transfer made structural sense for all parties. A domestically experienced operator with full funding responsibility and majority ownership has stronger incentives and capabilities to advance the project to production than a minority foreign partner juggling operational roles across multiple continents. Detailed feasibility work on such projects typically underpins these ownership transitions, ensuring the incoming operator has a clear path to production.

Why Two Partners Converted to Royalties Simultaneously

One of the most analytically interesting aspects of the Hod Maden transaction is that both SSR Mining and Royal Gold executed royalty conversions in the same transaction. Royal Gold sold its 15% equity interest to Lidya Mines in exchange for an uncapped 2.5% NSR on 100% of the project's production, while simultaneously retaining a 15% equity stake in the project.

Dual royalty conversions occurring within a single transaction are uncommon in the mining industry. Their simultaneous occurrence here points to a carefully negotiated outcome that aligned the distinct but compatible interests of three parties:

- Lidya Mines sought full operational autonomy and consolidated ownership to efficiently advance the project toward production without minority partner constraints on decision-making

- SSR Mining sought complete operational and jurisdictional exit while preserving perpetual production participation through its royalty instrument

- Royal Gold, as a dedicated royalty and streaming company, likely viewed the hybrid structure of retained equity plus a royalty as consistent with its own portfolio management strategy, allowing it to maintain exposure through both mechanisms

The coordinated nature of the dual royalty conversion is important context for investors. This was not a distressed asset sale where a financially pressured partner was forced to accept unfavourable terms. It was a structured, negotiated arrangement in which all parties obtained their primary strategic objective.

Geopolitical and Jurisdictional Dimensions of the Turkish Exit

Türkiye as a Mining Jurisdiction: The Risk Calculus

SSR Mining's complete exit from Türkiye, spanning both the Çöpler divestiture and the Hod Maden royalty conversion, eliminates the company's exposure to a range of jurisdiction-specific risks that have weighed on investor sentiment. These include:

- Regulatory and permitting risk: Turkish mining regulations have evolved in ways that increased compliance complexity for foreign operators in recent years

- Currency risk: Lira volatility creates unpredictable cost structures for operations denominated partially in local currency while revenues are typically priced in US dollars

- Political risk: The broader geopolitical environment in the region introduces uncertainties around asset security, repatriation of capital, and long-term regulatory stability

- Operational disruption risk: The Çöpler mine's prior operational interruptions demonstrated concretely how Turkish jurisdiction-specific factors could materially impact production continuity

By converting equity to an NSR royalty rather than pursuing an outright sale with full exit, SSR Mining has engineered an elegant solution: it retains economic upside in Hod Maden without bearing any of the operational, regulatory, or capital risk associated with developing a major mining project in this jurisdiction. Royalty payments, when they begin, will be straightforward financial transfers requiring none of the active management attention that direct ownership demands.

The Americas as a Strategic Safe Harbour

North American jurisdictions have consistently ranked among the most preferred operating environments for mid-tier gold producers based on criteria including permitting predictability, infrastructure quality, labour market depth, and legal framework stability. Colorado, where the CC&V mine is located, sits within a region with multi-generational mining history, established regulatory processes, and the infrastructure advantages of a mature mining district.

This jurisdictional preference reflects a broader industry pattern of portfolio rationalisation toward what the sector classifies as tier-one and tier-two jurisdictions. For SSR Mining specifically, the Americas pivot reduces the headline risk premium that capital markets were likely applying to its equity valuation given the Turkish operational complexity. A cleaner geographic footprint in lower-risk jurisdictions typically supports higher earnings multiples and reduced cost of capital, both of which benefit long-term shareholder value.

What the Transaction Means for Investors Evaluating SSR Mining

From Construction-Stage Exposure to a Hybrid Portfolio Model

The Hod Maden royalty conversion formally adds a royalty asset to SSR Mining's portfolio classification. The company now operates across two distinct value drivers:

- Americas operating assets: Active producing mines generating current cash flow, capital expenditure obligations, and direct operational exposure to gold and copper price movements

- Royalty instruments: A long-duration, capital-light production participation right that generates income without operational cost exposure

This hybrid structure is increasingly recognised by capital allocators as an effective model for mid-tier miners seeking to balance near-term cash generation with long-duration upside. While SSR Mining is not positioning itself as a pure royalty company, the addition of the Hod Maden NSR to its portfolio introduces a different risk and return profile than traditional mine ownership — one that sophisticated investors should incorporate into their valuation framework. Furthermore, resource capital funds and private equity participants are increasingly attentive to these hybrid structures when assessing mid-tier mining investment opportunities.

Comparing SSR Mining's Royalty Position to Dedicated Royalty Companies

| Metric | SSR Mining (Post-Transaction) | Typical Royalty/Streaming Company |

|---|---|---|

| Primary business model | Gold mining operator | Royalty/streaming only |

| Royalty type held | 4.0% uncapped NSR (Hod Maden) | Portfolio of NSRs, streams, and royalties |

| Capital obligation on royalty | None | None |

| Upside mechanism | Production-linked royalty payments | Production-linked royalty/stream payments |

| Operational risk exposure | Present in Americas assets | Absent by design |

While SSR Mining is not repositioning as a royalty company, the accumulation of royalty instruments alongside operating mines is a strategy increasingly used by mid-tier producers to balance capital efficiency with long-duration upside exposure. Investors evaluating SSR Mining must now apply a dual analytical lens that accounts for both its operating mine performance and the contingent but potentially significant value embedded in its growing royalty book.

Consequently, gold M&A activity in the Australian and broader global market continues to reflect this same structural logic, with producers increasingly using royalty instruments and strategic divestments to simplify their portfolios. Additionally, analysts tracking the full details of the Hod Maden stake sale have noted the significance of the dual royalty conversion as a defining feature of this particular transaction.

Disclaimer: This article contains forward-looking analysis and scenario projections based on publicly available transaction announcements. It does not constitute financial advice. Investors should conduct independent due diligence and consult a licensed financial adviser before making investment decisions related to any securities mentioned.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: SSR Mining and the Hod Maden Sale

What did SSR Mining receive in exchange for its Hod Maden stake?

SSR Mining exchanged its 20% equity interest and operatorship position for an uncapped 4.0% net smelter return royalty on 100% of Hod Maden's production. No upfront cash consideration was disclosed as part of the transaction terms.

Who is Lidya Mines?

Lidya Mines is the incoming majority owner and operator of the Hod Maden project, holding 85% of the project following the completion of both the SSR Mining and Royal Gold transactions. The company is assuming full operational control and all future capital funding responsibilities for the project's development.

What happens to Royal Gold's position in Hod Maden?

Royal Gold retained a 15% equity interest in the project while simultaneously converting a portion of its prior ownership into an uncapped 2.5% NSR royalty on 100% of the project's production.

When is the transaction expected to close?

The deal is targeted for completion in Q3 2026, subject to Turkish regulatory approvals and standard closing conditions.

How much has SSR Mining invested in Hod Maden?

SSR Mining deployed approximately $243 million into the Hod Maden project over the course of its involvement as equity holder and operator.

Does SSR Mining retain any future funding obligations for Hod Maden?

No. Upon execution of the transaction agreements, all future capital and operational funding obligations transferred entirely to Lidya Mines. SSR Mining carries no further development, construction, or operational financial responsibilities for the project.

Key Takeaways: The Strategic Logic of SSR Mining's Royalty Conversion

-

Capital liberation: Converting approximately $243 million in prior investment from an active equity position into a royalty instrument removes it from the active capital deployment cycle while preserving its productive potential

-

Risk elimination: Zero ongoing exposure to Hod Maden's construction timeline, permitting processes, cost overruns, or operational execution challenges

-

Uncapped upside preservation: The 4.0% NSR ensures SSR Mining participates in all future Hod Maden production value without contributing a single additional dollar of capital

-

Geographic clarity: The transaction finalises a three-part strategic pivot to a purely Americas-focused operating base, simplifying the investment thesis and potentially reducing the geopolitical risk discount applied to SSR Mining's valuation

-

Portfolio evolution: SSR Mining now holds both producing operating assets and royalty instruments, a hybrid model that balances near-term cash flow generation with long-duration production participation

-

Dual royalty signal: The simultaneous conversion of both SSR Mining and Royal Gold equity positions into royalty instruments within a single transaction represents an unusually coordinated risk reallocation, reflecting the aligned interests of all three parties rather than any single distressed seller circumstance

Want to Identify the Next Major Mining Restructuring Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries and strategic mining developments, transforming complex data across more than 30 commodities into clear, actionable insights for investors at every experience level. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated exceptional returns, and begin your 14-day free trial today to gain a market-leading edge.