June 25, 2026

What Economic Conditions Define Modern Stagflation Risk?

The intersection of geopolitical tensions with critical energy infrastructure creates cascading effects through interconnected financial systems, potentially triggering a prolonged oil crisis Iran war stagflation scenario. Modern economies face unprecedented challenges when energy security meets prolonged uncertainty, particularly when key maritime chokepoints become flashpoints for broader regional conflicts. Understanding these complex dynamics requires examining how contemporary financial systems respond to sustained energy volatility beyond traditional market mechanics.

The Dual Challenge of Rising Prices and Economic Stagnation

Stagflation represents one of the most perplexing challenges facing contemporary economic policy, combining persistent inflation with economic stagnation in ways that traditional monetary tools struggle to address effectively. Unlike demand-driven inflation, which responds to interest rate adjustments, energy-driven price pressures create supply-side constraints that resist conventional intervention methods.

The 1970s oil shocks provide crucial historical context for understanding how energy disruptions propagate through economic systems. During the 1973-1974 Arab oil embargo, crude prices quadrupled from approximately $3 to $12 per barrel, triggering inflation rates exceeding 12% in major developed economies while unemployment simultaneously rose. The 1979 Iranian Revolution sparked another energy crisis, with oil prices surging from $14 to $35 per barrel, creating a second wave of stagflationary pressure that persisted into the early 1980s.

Key indicators that economists monitor for stagflation development include:

- Inflation persistence: Core inflation measures remaining elevated for consecutive quarters

- GDP growth deceleration: Real economic output declining while price levels continue rising

- Employment stagnation: Labour markets showing weakness despite apparent economic activity

- Wage-price spiral indicators: Compensation increases lagging behind cost-of-living adjustments

Contemporary economies demonstrate both greater resilience and new vulnerabilities compared to previous decades. Strategic petroleum reserves now provide temporary buffers against supply disruptions, while renewable energy penetration offers some insulation from fossil fuel volatility. However, increased global economic integration means disruptions propagate more rapidly across borders, potentially amplifying regional energy crises into worldwide economic challenges.

Why Energy Shocks Amplify Stagflationary Pressures

Energy functions as a fundamental input across virtually all economic sectors, creating direct cost pressures that cannot be easily substituted or delayed. Transportation, manufacturing, and service industries all depend on reliable energy access, making widespread price increases inevitable when supply constraints emerge. This differs fundamentally from other commodity price shocks, which typically affect specific sectors rather than the entire economic foundation.

Consumer spending patterns shift dramatically during sustained energy price increases, as households redirect budgets from discretionary purchases toward essential energy costs. This demand destruction in non-energy sectors occurs simultaneously with rising production costs throughout the economy, creating the classic stagflation scenario where economic activity slows while prices continue climbing.

Transportation vulnerability emerges as particularly acute because alternatives to petroleum-based fuels remain limited for freight, aviation, and maritime shipping. Unlike electricity generation, where natural gas, nuclear, or renewable sources can substitute for oil, transportation sectors face immediate cost pass-through with limited options for efficiency improvements in the short term.

Manufacturing dependencies extend beyond direct energy consumption to include petrochemical feedstocks for plastics, chemicals, and synthetic materials. Energy-intensive industries such as steel, aluminium, and cement production face production cost increases that propagate through construction and automotive supply chains.

When big ASX news breaks, our subscribers know first

How Do Middle East Conflicts Disrupt Global Oil Markets?

Critical Chokepoint Analysis: The Strait of Hormuz

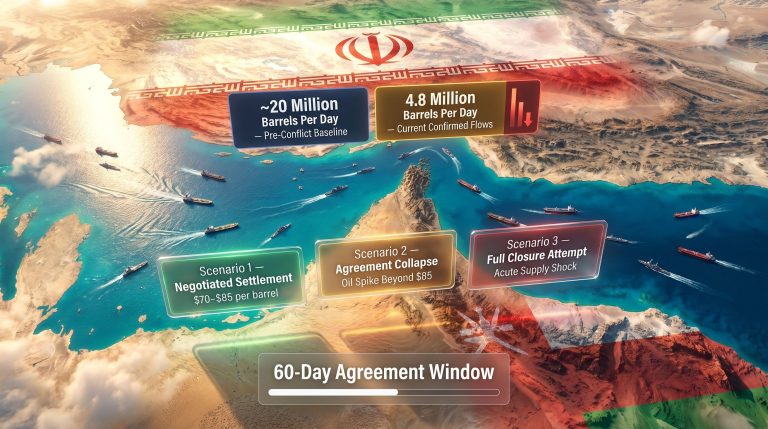

The Strait of Hormuz represents the world's most critical energy transit route, with approximately 21% of global petroleum liquids and 25% of liquefied natural gas passing through this narrow waterway. Analysis from Maybank Group Wealth Management suggests that prolonged closure scenarios could drive oil prices toward $90 per barrel, representing significant economic disruption potential.

| Global Energy Transit Routes | Daily Oil Flows (Million Barrels) | LNG Volumes (Billion Cubic Metres) | Alternative Routing Capacity |

|---|---|---|---|

| Strait of Hormuz | 21.0 | 25.0 | Limited pipeline alternatives |

| Strait of Malacca | 15.6 | 12.8 | No direct substitutes |

| Suez Canal/SUMED | 5.2 | 8.1 | Cape of Good Hope routing |

| Bab el-Mandeb | 4.8 | 6.3 | Cape routing with 2-3 week delays |

Geographic constraints make the Hormuz strait particularly vulnerable to disruption. At its narrowest point, the shipping channel measures only 33 kilometres wide, with two-mile-wide shipping lanes separated by a two-mile buffer zone. This physical limitation means even temporary disruptions create immediate market impact, as tanker traffic cannot be rapidly rerouted through alternative passages.

Alternative routing analysis reveals significant capacity limitations and cost implications. The Trans-Arabian Pipeline (Tapline) and East-West Pipeline provide some Saudi crude export alternatives, but combined capacity remains well below Hormuz transit volumes. Furthermore, prolonged disruptions would exacerbate oil price stagnation that major consumers seek to avoid through diversification strategies.

Insurance Market Responses to Geopolitical Risk

Maritime insurance markets provide early warning indicators for energy supply disruption risks through premium adjustments and coverage availability. During elevated regional tensions, war risk insurance premiums typically increase from standard rates of 0.025% to 0.1% of vessel value, representing millions of dollars in additional costs for large tanker operations.

Coverage withdrawal patterns during previous Middle Eastern conflicts show insurers often suspend new policies rather than adjust pricing, effectively creating shipping embargos through commercial risk management decisions. The prolonged conflict could mean higher prices at gas pumps as shipping costs rise dramatically during extended crisis periods.

Commercial shipping companies face complex decision matrices when evaluating whether to continue operations through elevated-risk regions. Beyond insurance costs, operators must consider crew safety, vessel security, cargo liability, and potential delays from military escort requirements or enhanced security protocols.

Supply Chain Vulnerabilities Beyond Crude Oil

Refined product markets often experience more severe disruption than crude oil markets during Middle Eastern conflicts, as regional refineries concentrate significant processing capacity for petrol, diesel, and jet fuel production. The Gulf region processes approximately 35% of global refining capacity, making refined product supplies particularly vulnerable to regional disruptions.

Liquefied Petroleum Gas (LPG) distribution networks face acute vulnerability, as Qatar and UAE represent major global suppliers with limited alternative sourcing options for Asian markets. Japan, South Korea, and other major LPG importers maintain strategic reserves, but these typically provide only 30-60 days of supply buffer during normal consumption patterns.

Strategic petroleum reserve coordination mechanisms through the International Energy Agency provide some supply disruption mitigation, but effectiveness depends on member country participation and reserve availability. Current global strategic reserves total approximately 4.2 billion barrels, though release coordination requires complex international negotiations that may not align with crisis timeframes.

Which Economic Sectors Face Greatest Stagflation Vulnerability?

Transportation and Logistics Industries

Transportation sectors experience immediate and unavoidable cost pressures during energy price escalations, as fuel represents 20-40% of operating expenses across aviation, trucking, and maritime shipping operations. Unlike manufacturing industries that can adjust production schedules or implement efficiency measures, transportation services must maintain operations to preserve supply chain continuity.

Freight cost escalation creates systematic inflation pressure as transportation charges increase across all goods movement. Container shipping rates, which already demonstrated extreme volatility during recent supply chain disruptions, become additional transmission mechanisms for energy cost inflation into consumer prices.

Aviation sector dynamics prove particularly complex during prolonged energy crises, as jet fuel hedging strategies typically provide only 6-12 months of price protection. Airlines face immediate pressure to implement fuel surcharges on passenger fares and cargo rates, whilst simultaneously managing reduced travel demand as consumers adjust spending patterns.

The logistics industry's cost pass-through mechanisms operate through contractual fuel surcharge formulas tied to benchmark energy prices. These automated adjustments ensure transportation cost increases rapidly propagate to end consumers, creating systematic inflation pressure that persists as long as energy prices remain elevated.

Manufacturing and Industrial Production

Energy-intensive manufacturing industries face immediate production cost pressures that cannot be easily mitigated through operational adjustments. Steel production, aluminium smelting, chemical processing, and cement manufacturing require consistent energy inputs that represent 15-30% of total production costs, making these sectors particularly vulnerable to sustained energy price volatility.

Production capacity utilisation often declines during energy price spikes as manufacturers reduce output to manage cost pressures. This capacity reduction creates supply constraints that amplify price pressures in downstream industries, contributing to broad-based inflation even in sectors not directly energy-dependent.

Regional competitiveness shifts emerge as energy price disparities develop between different geographic markets. Manufacturing operations may relocate production to regions with more stable energy costs, though these adjustments require significant time and capital investment, providing limited short-term relief during acute energy crises.

Industries with limited substitution options for energy inputs face the most severe stagflation pressures. Petrochemical producers, for example, cannot rapidly substitute alternative feedstocks, making them particularly vulnerable to both input cost increases and demand destruction as downstream customers reduce consumption.

Consumer Spending and Retail Dynamics

Consumer spending patterns demonstrate predictable adjustment mechanisms during energy price escalations, with households typically reducing discretionary purchases to accommodate higher transportation and heating costs. This demand destruction occurs simultaneously with retailers facing higher inventory and distribution costs, creating compressed margins throughout the retail sector.

Essential versus discretionary spending trade-offs become pronounced during sustained energy price increases. Food, healthcare, and housing costs consume larger portions of household budgets, whilst spending on dining, entertainment, and non-essential goods contracts. This spending reallocation contributes to economic stagnation in discretionary sectors whilst inflation persists in essential categories.

Regional variations in consumer impact depend heavily on energy dependence patterns and local economic structures. Rural communities with limited public transportation options face disproportionate impact from petrol price increases, whilst urban consumers may experience greater exposure to heating and electricity cost escalations.

What Are the Monetary Policy Implications of Energy-Driven Inflation?

Central Bank Dilemma: Fighting Inflation vs. Supporting Growth

Central banks confront their most challenging policy environment during energy-driven inflation, as traditional interest rate tools prove less effective against supply-side price pressures whilst potentially exacerbating economic stagnation. The Federal Reserve's experience during the 1970s stagflation period demonstrates the difficulty of using monetary policy to combat inflation that originates from external supply shocks rather than domestic demand excess.

Interest rate policy effectiveness diminishes significantly when inflation stems from energy supply constraints rather than economic overheating. Raising rates to combat energy-driven inflation risks deepening recession without addressing the fundamental supply-side causes of price increases. In addition, the prolonged oil crisis Iran war stagflation scenario presents unique challenges that traditional monetary policy frameworks struggle to address effectively.

Historical central bank responses reveal the complexity of communicating policy intentions during stagflation periods. The Volcker Federal Reserve's aggressive rate increases during 1979-1982 successfully reduced inflation expectations but required inducing severe recession with unemployment reaching 10.8%. This approach may not be politically sustainable in contemporary economic and social contexts.

Inflation expectations management becomes critical during prolonged energy crises, as central bank credibility influences whether temporary energy price shocks translate into persistent broad-based inflation. Clear communication that energy-driven inflation represents a transitory phenomenon requires convincing market participants that central banks will act decisively once energy prices stabilise.

Regional Central Bank Coordination Challenges

Different regional economies face varying inflation and growth trade-offs during global energy crises, complicating international monetary policy coordination. The European Central Bank may prioritise inflation control given the eurozone's heavy energy import dependence, whilst emerging market central banks might focus on currency stability and capital flow management.

Federal Reserve policy spillovers create additional complexity for global monetary coordination, as dollar strength during U.S. rate increases amplifies energy import costs for economies with weaker currencies. This dynamic can force other central banks to raise rates defensively to prevent currency depreciation, even when domestic economic conditions favour accommodation.

International monetary cooperation mechanisms through central bank swap lines and coordination agreements provide some stability during crisis periods, but effectiveness depends on shared policy objectives that may not align during stagflation scenarios. Competing priorities between inflation control and growth support can undermine coordinated policy responses.

How Do Different Regions Experience Stagflation Risk?

Energy-Importing Economies: Europe and Asia

Energy-importing regions face the most severe stagflation vulnerability during prolonged Middle Eastern disruptions, as external energy costs create immediate inflation pressure whilst reducing domestic spending power. European Union members collectively import approximately 60% of their energy consumption, with natural gas imports reaching 83% dependence on external suppliers.

| Regional Energy Import Dependencies | Oil Imports (% of Consumption) | Natural Gas Reliance (%) | Alternative Energy Timeline |

|---|---|---|---|

| European Union | 97% | 83% | 2030 targets: 42.5% renewable |

| Japan | 100% | 96% | 2030: 22-24% renewable |

| South Korea | 100% | 98% | 2030: 21% renewable |

| India | 88% | 53% | 2030: 40% renewable |

| China | 70% | 43% | 2025: 20% renewable |

Japan's energy vulnerability reflects decades of nuclear capacity reduction following Fukushima, increasing dependence on LNG imports that transit through potential conflict zones. The country's strategic petroleum reserves provide approximately 200 days of import cover, but LNG storage limitations create more immediate vulnerability during supply disruptions.

South Korea's industrial structure amplifies stagflation risk through heavy dependence on energy-intensive manufacturing exports. Semiconductor, steel, and chemical production require reliable energy access, making the economy particularly vulnerable to both cost increases and supply interruptions that could reduce export competitiveness. Moreover, energy transition challenges across developed economies highlight the complexity of reducing fossil fuel dependence quickly.

India's growing energy import dependence creates fiscal pressures through current account deficit expansion during high energy price periods. Government fuel subsidies, which help moderate domestic inflation pressure, create substantial fiscal costs that limit other government spending options during economic downturns.

Emerging Market Vulnerability Assessment

Emerging market economies face compounded stagflation pressures through multiple transmission channels that amplify both inflation and growth challenges. Currency depreciation during energy price increases magnifies import costs whilst external debt service becomes more burdensome in dollar terms.

Current account balance deterioration occurs rapidly during energy price spikes as import bills expand whilst export demand may weaken due to global economic slowdown. Countries with limited foreign exchange reserves face particular vulnerability, as currency intervention capacity becomes constrained during extended crisis periods.

Fiscal policy constraints limit emerging market governments' ability to provide economic support during stagflation periods. Energy subsidies, which many governments implement to moderate domestic price impacts, create substantial fiscal costs precisely when other revenue sources may be declining due to economic stagnation.

Central bank credibility challenges in emerging markets make inflation expectations harder to anchor during energy crises. Limited track records of successfully managing inflation may cause market participants to anticipate persistent price increases, creating self-fulfilling expectations that require more aggressive policy responses.

Energy-Exporting Nations: Windfall vs. Disruption

Energy-exporting economies experience contradictory pressures during prolonged regional conflicts, benefiting from higher revenues whilst facing increased uncertainty about conflict duration and global economic impacts. Gulf Cooperation Council members must balance windfall revenue management with long-term economic diversification objectives.

Resource curse dynamics suggest that sudden commodity windfalls can create macroeconomic instability without institutional capacity to manage revenue volatility effectively. Saudi Arabia's Vision 2030 diversification programme reflects awareness that oil revenue volatility creates long-term economic vulnerability despite short-term fiscal benefits.

Investment strategy shifts during geopolitical uncertainty often favour liquid asset accumulation over long-term development projects. This preference for financial flexibility may slow economic diversification precisely when windfall revenues could fund structural transformation initiatives.

Regional security costs increase substantially during prolonged conflicts, as energy infrastructure protection and military expenditures consume resources that might otherwise support economic development. These security premiums represent long-term economic costs that persist beyond immediate conflict resolution.

What Historical Precedents Guide Stagflation Risk Assessment?

1973 and 1979 Oil Crisis Comparative Analysis

The 1973-1974 Arab oil embargo provides the foundational case study for understanding how energy supply disruptions translate into stagflation. Oil prices increased from $3.56 per barrel in October 1973 to $11.65 by March 1974, whilst U.S. real GDP declined 3.2% and inflation reached 12.3% by 1974.

Policy response effectiveness during the 1973 crisis revealed the limitations of traditional fiscal and monetary tools. The Nixon administration's wage-price controls proved counterproductive, creating supply shortages whilst failing to address underlying energy cost pressures. Monetary policy accommodation initially aimed at supporting economic growth ultimately contributed to persistent inflation expectations.

The 1979 Iranian Revolution triggered a second oil shock with different characteristics but similar stagflation outcomes. Oil prices doubled from approximately $14 to $35 per barrel between 1978 and 1981, whilst U.S. inflation peaked at 14.8% in March 1980. Unlike the 1973 embargo, which involved coordinated producer action, the 1979 crisis resulted from revolutionary disruption of Iranian production capacity.

Recovery patterns from both crises required multiple years and substantial economic costs. The Volcker Federal Reserve's aggressive monetary tightening during 1979-1982 successfully reduced inflation from double digits to approximately 3%, but required inducing recession with unemployment reaching 10.8% by late 1982.

Modern Economic Resilience Factors

Contemporary energy security mechanisms provide greater resilience against supply disruptions compared to 1970s capabilities. Strategic petroleum reserves now total approximately 4.2 billion barrels globally, compared to minimal reserves during earlier crises. The International Energy Agency coordinates release protocols that can provide temporary supply augmentation during acute shortages.

Renewable energy penetration offers some insulation from fossil fuel price volatility, though integration levels remain insufficient to eliminate energy shock vulnerability. Wind and solar capacity has expanded dramatically since 2010, but backup power requirements and transportation sector dependence on petroleum products maintain significant exposure to oil market disruptions.

Financial market sophistication in energy derivatives trading allows for more efficient risk pricing and hedging compared to previous decades. Oil futures markets, which were nascent during 1970s crises, now provide transparent price discovery and risk management tools for commercial users and financial participants.

However, increased global economic integration may amplify crisis propagation compared to earlier periods. Supply chain interconnectedness means regional disruptions can rapidly affect global production networks, potentially creating broader economic impacts than occurred during more autarkic economic structures of previous decades. Additionally, US‑China trade tensions complicate international coordination during crisis periods.

The next major ASX story will hit our subscribers first

Which Investment Strategies Address Stagflation Scenarios?

Asset Class Performance During Energy-Led Inflation

Asset allocation strategies during stagflation periods require careful analysis of historical performance patterns and correlation structures that differ significantly from normal market conditions. Energy sector equities typically outperform during oil price increases, but broader equity market performance depends heavily on the duration and severity of economic stagnation.

| Historical Asset Returns During Oil Shocks | 1973-1974 Crisis | 1979-1981 Crisis | 2008 Energy Spike |

|---|---|---|---|

| Energy Sector Equities | +37.2% | +42.8% | +28.4% |

| Broad Equity Markets | -37.2% | -17.3% | -26.1% |

| Treasury Bonds (Real Returns) | -8.4% | -11.2% | +3.7% |

| Commodities (Broad Index) | +22.3% | +31.7% | +18.9% |

| Gold | +73.7% | +125.4% | +24.8% |

According to Maybank Group Wealth Management analysis, gold prices could potentially move toward $6,000 per ounce in scenarios involving prolonged geopolitical tensions combined with structural demand shifts. This projection reflects both traditional safe-haven demand and evolving central bank reserve diversification strategies, reinforcing the appeal of gold as an inflation hedge during uncertain economic periods.

Fixed income securities face complex dynamics during stagflation, as nominal yields may increase to reflect inflation expectations whilst real returns remain negative if inflation exceeds yield increases. Inflation-protected securities (TIPS) provide some protection, but availability and liquidity may become constrained during severe stagflation episodes.

Real estate investment considerations depend heavily on financing conditions and regional economic impacts. Property values may benefit from inflation hedging characteristics, but high interest rate environments created by central bank inflation-fighting efforts can substantially reduce valuations and liquidity.

Geographic Diversification Considerations

Geographic asset allocation during stagflation scenarios requires balancing exposure between energy-importing and energy-exporting economies, whilst considering currency dynamics and regional policy responses. Resource-rich economies may provide some portfolio protection through commodity exposure, but political stability and governance quality become critical evaluation factors.

Currency hedging strategies become complex during prolonged energy crises, as exchange rate relationships may deviate from typical correlations. Energy-importing countries may experience currency weakness that creates additional headwinds for international investment returns when measured in domestic currency terms.

Emerging market considerations require careful analysis of energy trade balances and external debt burdens. Energy-exporting emerging markets may benefit from commodity price increases, whilst energy importers face compounded pressures from both higher import costs and potential capital flow reversals.

Portfolio concentration in developed market assets may provide stability during crisis periods but could miss opportunities in resource-rich regions that benefit from higher commodity prices. Balanced exposure across different energy trade relationships may provide more resilient returns across various crisis scenarios.

What Policy Tools Can Mitigate Stagflationary Pressures?

Government Fiscal Response Options

Strategic petroleum reserve releases provide the most direct government tool for addressing energy supply disruptions, though effectiveness depends on coordination among major consuming nations and reserve availability relative to supply shortfalls. The United States maintains approximately 650 million barrels in strategic reserves, whilst other IEA members collectively hold additional reserves totalling over 1.5 billion barrels.

Targeted consumer energy subsidies versus broad-based fiscal support present different trade-offs during stagflation periods. Direct energy cost relief can moderate inflation impact on households but may reduce price signals that encourage conservation and alternative energy adoption. Universal basic income or broad tax relief provides more flexible household support but may contribute to aggregate demand pressure.

Infrastructure investment strategies to reduce long-term energy vulnerability require substantial capital commitments during periods when fiscal resources face competing demands. Renewable energy development, grid modernisation, and energy storage capacity expansion provide long-term security benefits but limited short-term crisis mitigation.

Emergency fuel allocation systems, similar to those implemented during 1970s crises, may become necessary during severe supply disruptions. However, price controls and rationing systems typically create secondary market distortions and supply shortages that can worsen overall economic efficiency.

International Cooperation Mechanisms

International Energy Agency emergency response protocols provide frameworks for coordinated strategic reserve releases and demand reduction measures during supply crises. Member countries commit to maintain 90 days of import cover in strategic reserves and participate in collective response decisions during supply emergencies.

Diplomatic engagement strategies for conflict resolution become critical during prolonged energy crises, as military solutions may worsen supply disruptions whilst economic sanctions can reduce available supply even when physical infrastructure remains intact. Multilateral diplomatic initiatives require careful coordination to avoid working at cross-purposes.

Alternative energy supply route development through pipeline projects and LNG infrastructure expansion provides long-term energy security benefits but requires multi-year construction timelines that offer limited immediate crisis relief. However, accelerated permitting and investment commitments during crisis periods can improve medium-term supply resilience.

Furthermore, tariff impact on markets must be carefully considered when implementing trade-based policy responses to energy crises, as protectionist measures may inadvertently worsen supply chain disruptions.

How Should Businesses Prepare for Prolonged Energy Price Volatility?

Operational Risk Management Strategies

Energy cost hedging instruments provide businesses with tools to manage price volatility, though hedging effectiveness depends on contract duration and basis risk between hedge instruments and actual energy costs. Forward contracts, options strategies, and swap agreements allow companies to lock in energy costs for periods ranging from months to several years.

Supply chain diversification strategies become critical during prolonged uncertainty, as alternative supplier networks and transportation routes provide operational flexibility when primary channels face disruption. Companies may need to accept higher normal-period costs to maintain access to backup suppliers during crisis conditions.

Pricing strategy adjustments for sustained input cost increases require balancing customer retention with margin protection. Automatic fuel surcharge mechanisms, similar to those used in transportation industries, provide one approach for maintaining margins during volatile periods whilst maintaining pricing transparency.

Inventory management strategies may shift toward higher safety stock levels during prolonged uncertainty, though carrying cost increases must be balanced against supply disruption risks. Just-in-time inventory systems that optimise efficiency during stable periods may prove inadequate during extended crisis conditions.

Strategic Planning for Extended Uncertainty

Capital allocation priorities may require adjustment during volatile energy environments, as projects with high energy intensity or long payback periods face increased risk assessment requirements. Investment in energy efficiency improvements and alternative energy sources may provide operational hedge value that justifies accelerated deployment timelines.

Market positioning strategies during potential economic slowdown require careful analysis of demand elasticity and competitive dynamics. Companies serving essential needs may maintain pricing power, whilst discretionary sectors may face margin compression requiring operational efficiency improvements or market share consolidation strategies.

Workforce planning considerations include both direct energy cost impacts on operations and indirect effects through reduced consumer spending in discretionary sectors. Skills development in energy management and efficiency optimisation may become more valuable during extended periods of energy price volatility.

The extended conflict risks sending global economy into stagflation according to recent economic analysis, highlighting the urgency of comprehensive business preparation strategies.

Navigating Economic Uncertainty in Energy Crisis Scenarios

Key Risk Monitoring Indicators

Early warning signals for stagflation development include divergence between core and headline inflation measures, indicating whether energy cost increases are translating into broader price pressures. Central bank communication shifts and market-based inflation expectation measures provide additional indicators of whether temporary energy shocks may become persistent economic phenomena.

Policy response effectiveness metrics include strategic reserve utilisation rates, international cooperation success in supply augmentation, and fiscal support targeting accuracy. Monitoring these indicators helps assess whether policy interventions are successfully mitigating crisis impacts or require adjustment as conditions evolve.

Financial market stress indicators such as credit spreads, equity market volatility, and currency stability provide real-time assessment of crisis severity and market confidence in policy responses. These measures often provide earlier signals than traditional economic statistics, which reflect conditions with substantial lags.

Long-term Economic Structural Implications

Accelerated energy transition investment patterns may emerge from prolonged fossil fuel price volatility, as businesses and governments recognise the economic security benefits of renewable energy diversification. Crisis periods often catalyse infrastructure investments that might otherwise face political or economic obstacles.

Geopolitical risk premium integration in economic planning represents a structural shift toward resilience over efficiency optimisation. This reorientation may reduce global economic integration benefits but improve stability during future crisis periods through reduced interdependence on vulnerable supply chains.

Resilience-building strategies for future energy security require balancing short-term crisis response with long-term structural improvements. Investments in energy storage, grid flexibility, and alternative fuel development provide insurance value that justifies costs beyond normal economic return calculations.

The prolonged oil crisis Iran war stagflation risks associated with extended Middle Eastern conflicts highlight fundamental tensions between energy security and economic efficiency. Understanding these dynamics provides essential context for investment decisions, policy evaluation, and risk management strategies during periods of heightened geopolitical uncertainty.

Disclaimer: This analysis contains forward-looking projections and market predictions that involve substantial uncertainty. Energy markets and geopolitical situations can change rapidly, and actual outcomes may differ significantly from discussed scenarios. Investors should conduct independent research and consider multiple perspectives before making investment decisions. Past performance of assets during previous energy crises may not predict future results.

Ready to Position Yourself Ahead of Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market during periods of economic uncertainty. Begin your 14-day free trial today and secure your market-leading advantage when energy sector dynamics create new investment opportunities.