June 11, 2026

Understanding the Current Steel Market Downturn

Industrial commodity cycles follow predictable patterns of expansion, peak production, and inevitable contraction phases that reveal underlying economic fundamentals. The world steel production decline has emerged as one of the most significant contractionary periods since the pandemic-driven disruptions of 2020, affecting manufacturing infrastructure worldwide.

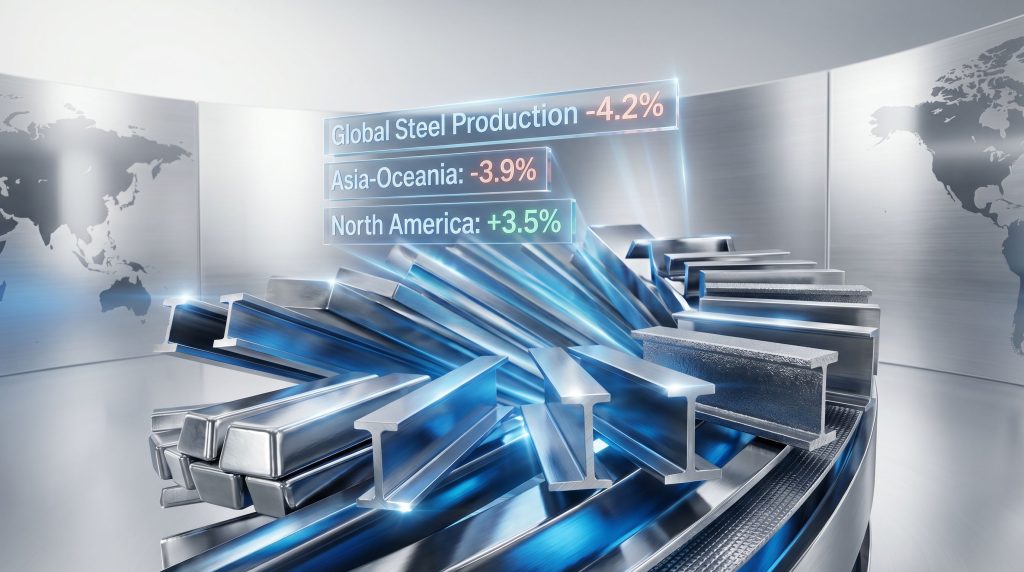

Global crude steel production reached 159.9 million tonnes in March 2026, marking a substantial 4.2% decline compared to the same period in 2025, according to data from the World Steel Association. This monthly contraction extends into broader quarterly trends, with first-quarter 2026 production totaling 459.2 million tonnes, representing a 2.3% year-over-year decrease.

| Region | March 2026 Output (MT) | YoY Change | Q1 2026 Total (MT) | Q1 YoY Change |

|---|---|---|---|---|

| Asia-Oceania | 119.3 | -3.9% | 341.7 | -2.2% |

| Europe (EU) | 11.4 | -4.6% | 34.2 | -4.6% |

| North America | 9.5 | +3.5% | 27.5 | +2.3% |

| CIS Countries | 6.6 | -7.9% | 18.9 | -9.8% |

| South America | 3.6 | -0.5% | 10.2 | -1.9% |

| Middle East | 3.5 | -33.5% | – | – |

| Africa | 2.2 | +11.6% | – | – |

The severity of regional variations within this global downturn reveals complex market dynamics affecting different geographic zones through distinct mechanisms. However, commodity market volatility continues to influence production decisions across all regions.

When big ASX news breaks, our subscribers know first

What Economic Forces Are Driving the World Steel Production Decline?

Steel production patterns typically reflect broader economic momentum across construction, manufacturing, infrastructure development, and energy sectors. The current 4.2% monthly decline signals coordinated demand adjustments across multiple industrial applications simultaneously.

Demand-Side Pressures Across Key Markets

Construction sector activity traditionally accounts for approximately 50% of global steel consumption, making residential and commercial building trends primary indicators of steel demand trajectory. Furthermore, current production patterns suggest:

- Reduced structural steel specifications in new construction projects

- Commercial building delay patterns affecting long-term steel procurement

- Infrastructure project timeline adjustments creating demand timing shifts

- Quality-over-quantity preferences in construction material selection

Automotive manufacturing represents another significant steel consumption category, with traditional vehicle production requiring 900-1,200 kilograms of steel per unit. In addition, industry transitions toward electric vehicle platforms, which typically utilise 200-300 kilograms less steel per vehicle, contribute to evolving demand patterns.

Supply Chain Optimisation Strategies

Manufacturing organisations across multiple industries have implemented inventory management approaches that reduce steel buffer stocks:

- Just-in-time procurement scheduling minimising warehouse requirements

- Demand forecasting integration with production planning systems

- Regional sourcing diversification reducing single-supplier dependencies

- Quality specification upgrades prioritising performance over volume

Energy price volatility throughout 2025 and early 2026 has influenced steel production scheduling decisions. Consequently, natural gas trends directly impact steel manufacturing, which requires substantial electricity and natural gas inputs.

How Are Regional Steel Markets Responding to Global Headwinds?

Geographic production patterns reveal how local demand drivers, policy environments, and industrial structures create differentiated market responses to global economic conditions.

Asia-Pacific: The China Factor and Regional Dynamics

China's Strategic Production Adjustment

China produced 87 million tonnes in March 2026, representing a 6.3% year-over-year decline and accounting for approximately 54% of total Asia-Oceania regional output. This contraction exceeds the global average decline, indicating specific domestic factors influencing Chinese production decisions.

The Chinese steel industry faces multiple simultaneous pressures:

- Domestic consumption optimisation as infrastructure investment patterns mature

- Export market recalibration responding to international trade policy changes

- Production efficiency improvements reducing total volume requirements

- Raw material cost management affecting operational scheduling

India's Counter-Cyclical Growth Pattern

India achieved 15.3 million tonnes of production in March 2026, demonstrating remarkable 9.4% expansion while most major producers contracted. This growth pattern suggests robust domestic demand drivers supporting continued steel consumption:

- Infrastructure development programmes creating steel-intensive project pipelines

- Manufacturing sector expansion increasing industrial steel requirements

- Construction market resilience maintaining structural steel demand

- Import substitution strategies supporting domestic production capacity

Japan and South Korea: Mature Market Adjustments

Japan recorded 6.9 million tonnes with a 4.1% year-over-year decline, while South Korea produced 5.4 million tonnes with modest 1.5% growth. These mature steel markets demonstrate:

- Technology sector demand for specialised steel applications

- Shipbuilding industry cycles affecting regional production patterns

- Export-oriented manufacturing creating variable steel requirements

- Energy efficiency priorities influencing production scheduling

Vietnam emerged as another regional growth market, producing 2.2 million tonnes with 5.7% expansion, indicating continued industrialisation momentum supporting steel consumption growth.

European Union: Navigating Energy Transition Challenges

Germany's Production Recovery Signals

Germany achieved 3.3 million tonnes representing 7.5% year-over-year growth, making it the only major European producer demonstrating significant expansion during the regional downturn. This performance contrasts sharply with the broader EU's 4.6% decline, suggesting specific German market advantages:

- Industrial base resilience maintaining manufacturing steel requirements

- Renewable energy infrastructure development creating specialised steel demand

- Automotive sector recovery supporting high-grade steel consumption

- Technology manufacturing growth requiring precision steel applications

Other European countries (Bosnia-Herzegovina, Macedonia, Norway, Serbia, Turkey, and the United Kingdom) collectively produced 3.8 million tonnes with 4.9% growth, indicating pockets of regional strength despite broader European market challenges. However, tariff market impacts continue to influence trade patterns across the region.

African Market Momentum

African producers (Egypt, Libya, and South Africa) achieved 2.2 million tonnes with impressive 11.6% growth, representing the strongest regional performance globally. This expansion reflects:

- Infrastructure development acceleration across multiple African nations

- Mining sector expansion creating steel-intensive equipment requirements

- Urban development projects supporting construction steel demand

- Industrial capacity building increasing manufacturing steel consumption

What Does the Middle East Production Collapse Reveal About Market Dynamics?

The Middle East experienced the most dramatic regional contraction, with production from Iran, Qatar, Saudi Arabia, and the UAE totalling 3.5 million tonnes, down 33.5% year-over-year. This decline represents eight times the severity of the global average, indicating region-specific disruptions affecting steel production capacity.

Geopolitical Risk Factors

Middle Eastern steel production operates within complex geopolitical environments that can rapidly affect operational continuity:

- Trade route uncertainties affecting raw material supply chains

- Investment climate volatility influencing long-term capacity planning

- Regional security considerations affecting industrial facility operations

- Energy resource allocation between domestic consumption and export priorities

Market Structure Implications

The 33.5% regional decline suggests structural adjustments beyond normal demand cycles:

- Domestic market prioritisation over export-oriented production

- Energy sector competition for natural gas and electricity resources

- Infrastructure project delays reducing regional steel consumption

- Economic diversification strategies affecting industrial investment patterns

This production pattern indicates how geopolitical factors can create market disconnection from global economic fundamentals. Consequently, regional producers experience demand destruction significantly exceeding international trends.

How Are North and South American Markets Bucking Global Trends?

United States: Industrial Resilience Indicators

The United States achieved 7.2 million tonnes with 5.2% year-over-year growth in March 2026, contributing to North America's overall 3.5% regional expansion. This performance demonstrates:

- Infrastructure investment momentum supporting domestic steel demand

- Manufacturing reshoring initiatives increasing regional steel consumption

- Energy sector development creating pipeline and equipment steel requirements

- Construction market stability maintaining structural steel demand levels

North American regional production totalled 27.5 million tonnes in Q1 2026 with 2.3% quarterly growth, indicating sustained demand resilience throughout the first quarter period.

Brazil's Production Adjustment Strategy

Brazil produced 2.8 million tonnes with a modest 2.5% decline, contributing to South America's overall 0.5% monthly contraction. Brazilian steel production reflects:

- Mining sector demand fluctuations affecting steel equipment requirements

- Construction market optimisation influencing regional steel consumption

- Export competitiveness considerations in global market positioning

- Domestic infrastructure project timing creating variable steel demand patterns

The relatively modest South American decline (-0.5%) compared to other major regions suggests regional demand stability and effective production adjustment strategies. Furthermore, iron ore trends continue to influence regional production decisions.

What Do These Production Patterns Signal for 2026-2027 Market Outlook?

Structural Demand Shift Analysis

Current production patterns indicate fundamental changes in global steel consumption rather than temporary cyclical adjustments. However, several emerging trends suggest long-term market evolution, particularly within the world steel production decline framework.

Quality-Focused Consumption Patterns

- High-strength steel specifications replacing traditional grades in automotive applications

- Corrosion-resistant alloys gaining market share in infrastructure projects

- Precision steel products supporting technology manufacturing expansion

- Sustainable steel alternatives meeting environmental performance requirements

Geographic Demand Redistribution

- Emerging market growth (India +9.4%, Africa +11.6%, Vietnam +5.7%) offsetting developed market contractions

- Regional supply chain optimisation reducing long-distance steel transportation

- Domestic market prioritisation over export-oriented production strategies

- Infrastructure investment timing creating variable geographic demand patterns

Investment and Capacity Planning Implications

Strategic Considerations for Steel Producers

Current market conditions suggest several strategic priorities for global steel producers:

- Capacity utilisation optimisation rather than volume expansion focus

- Product mix diversification towards specialised applications and higher margins

- Regional market positioning to capture growing demand centres

- Technology integration for production efficiency and quality improvements

Supply Chain Risk Management

The 33.5% Middle East decline and 9.8% CIS contraction demonstrate how geopolitical factors can rapidly disrupt regional steel supply chains. According to the OECD Steel Outlook 2025, this volatility encourages:

- Multi-regional sourcing strategies to reduce concentration risk

- Inventory management flexibility during supply disruption periods

- Quality specification standardisation across multiple supplier regions

- Contract diversification to manage price and availability risks

The next major ASX story will hit our subscribers first

Strategic Implications for Industry Stakeholders

For Steel Producers

The current world steel production decline creates both challenges and opportunities for global producers. Production scheduling flexibility becomes essential during demand volatility periods, requiring operational systems capable of rapid capacity adjustments.

Product portfolio optimisation toward high-value applications offers margin protection during volume contraction periods. Specialty steel grades for automotive, aerospace, and technology applications typically maintain stronger pricing power than commodity steel products.

Regional market positioning strategies should prioritise growing demand centres. India's 9.4% growth and Africa's 11.6% expansion indicate emerging opportunities requiring investment in regional production capacity or supply chain partnerships.

For Steel Consumers

Supply chain diversification across multiple geographic sources provides protection against regional production disruptions. The 33.5% Middle East decline demonstrates how quickly regional capacity can become unavailable.

Inventory management strategies during volatile periods require balancing cost reduction with supply security. For instance, just-in-time systems offer cost advantages but create vulnerability during supply chain disruptions.

Contract timing optimisation becomes critical during price volatility periods. In addition, current production patterns suggest potential price pressures in regions with declining capacity, while growing production regions may offer more competitive pricing.

For Investors and Analysts

Regional performance divergence creates selective investment opportunities. Producers with strong positions in growing markets (India, Africa, North America) may outperform those concentrated in declining regions.

Technology adoption rates influence competitive positioning during market transitions. Furthermore, companies investing in production efficiency, quality improvements, and sustainable steel production may capture market share during industry evolution trends.

Market consolidation potential increases during prolonged adjustment periods. Smaller producers in declining regions may become acquisition targets for companies seeking capacity at attractive valuations.

Current production patterns suggest successful industry adaptation to evolving market requirements rather than fundamental structural weakness. Understanding these regional variations and demand drivers provides essential intelligence for strategic planning across the entire steel value chain.

The steel industry's response to current challenges demonstrates resilience and adaptability, with successful producers focusing on operational efficiency, market positioning, and customer-specific solutions rather than volume maximisation strategies. This evolution toward sustainable, technology-enhanced production methods positions the industry for long-term competitiveness in changing global markets.

Want to Capitalise on Shifting Commodity Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including iron ore and steel-related opportunities that could benefit from current market dynamics. Subscribers gain immediate access to actionable trading insights, positioning themselves ahead of market movements during periods of commodity volatility and production adjustments. Begin your 14-day free trial today to secure your market-leading advantage.