June 23, 2026

The Structural Fragility Hidden Inside Every Tonne of Aluminium You Buy

Global commodity markets have long priced aluminium as though its supply chain were diversified, resilient, and geographically distributed. The reality, as the ongoing Strait of Hormuz aluminium trade disruption is now making unmistakably clear, is far more concentrated and far more fragile than most downstream buyers, fabricators, or even institutional investors have historically accounted for.

The Gulf Cooperation Council region produces roughly 8 to 9 percent of global primary aluminium output each year. That figure alone might not alarm anyone. However, the detail that transforms it from a statistic into a systemic risk is this: virtually all of that production must exit through a single 33-kilometre-wide maritime passage. There is no pipeline alternative, no overland route, and no bypass. The Strait of Hormuz is not merely a trade corridor for Gulf aluminium; it is the only corridor.

Understanding why the current disruption is structurally different from past episodes of geopolitical tension requires examining the mechanics of the supply chain, not just the headlines.

When big ASX news breaks, our subscribers know first

A Chokepoint That Controls Both Inputs and Outputs

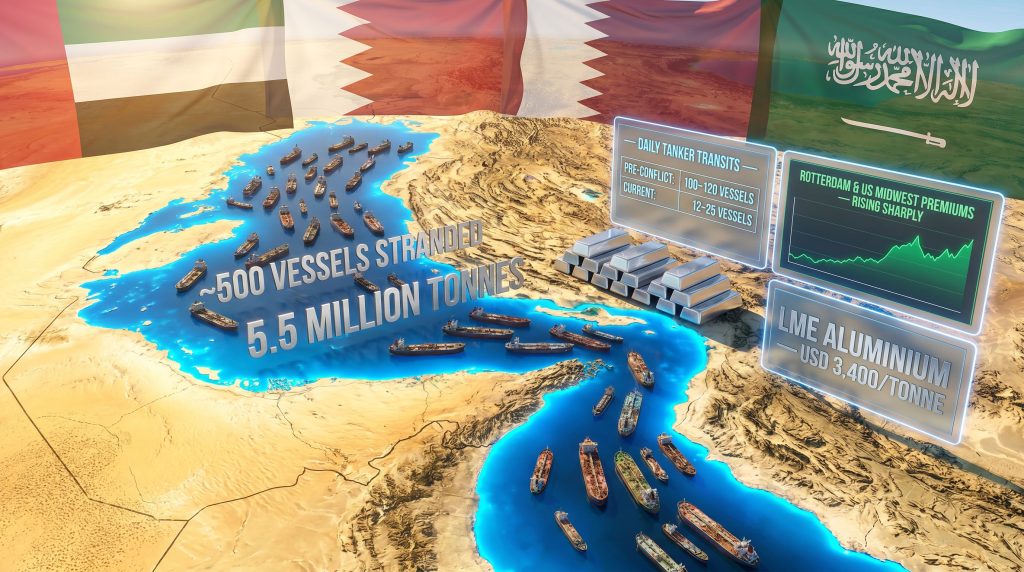

One of the most underappreciated dimensions of the Strait of Hormuz aluminium trade disruption is that it operates in two directions simultaneously. Most market commentary focuses on the export side: approximately 5.5 million tonnes of GCC primary aluminium that transit the strait annually, heading toward European, Asian, and North American buyers. This is the visible part of the problem.

Less discussed, but equally consequential, is the import dependency of Gulf smelters themselves. Operations across the UAE, Bahrain, Qatar, and Saudi Arabia are not vertically integrated from mine to metal. They depend on seaborne deliveries of alumina and bauxite, primarily sourced from Australia, Guinea, and Brazil, to keep their potlines running. Disrupt those inbound flows, and production curtailment becomes a mathematical inevitability regardless of how much finished aluminium is sitting in warehouses.

The critical inventory buffer that stands between disruption and curtailment is measured in weeks, not months. Gulf smelters typically carry only three to four weeks of alumina stockpile at any given time. This is not an oversight; it is a reflection of global just-in-time logistics norms optimised for efficiency rather than resilience. The alumina market pressures already building before this crisis have made that vulnerability significantly more acute. When the Strait becomes unreliable, that efficiency becomes a liability.

"The Hormuz disruption creates a pincer effect on Gulf aluminium producers: metal cannot efficiently leave while the raw materials needed to make it struggle to arrive. This dual-directional pressure is the defining structural risk for the global aluminium supply chain in this scenario."

What Vessel Traffic Data Is Actually Telling Us

The current situation is complicated by a significant divergence between official and independent assessments of shipping activity. According to maritime intelligence data from Windward, daily vessel crossings through the strait fell sharply to just 12 transits on Sunday, June 21, compared to 35 the previous day. Multiple vessels entering the waterway disabled their Automatic Identification System (AIS) transponders, creating tracking blind spots that elevate risk perception across the entire shipowner and insurer ecosystem.

A brief recovery had occurred earlier in the week. Data from Kpler showed 25 vessel transits on Thursday, the highest single-day figure since mid-April, following diplomatic engagement between the United States and Iran. However, Iran's Islamic Revolutionary Guard Corps subsequently announced on Saturday, June 20, that the waterway was again closed, citing issues with ceasefire implementation related to Israel's conduct.

US Central Command contested this assessment, reporting 55 merchant vessel transits on the same Saturday that commercial tracking services recorded far lower figures. This contradiction is not simply a public relations dispute. It creates a genuine pricing problem for commodity markets, one that echoes the uncertainty seen during the oil price shock that rattled energy markets earlier this year.

| Metric | Pre-Conflict Baseline | Current Reported Level |

|---|---|---|

| Daily tanker transits | 100-120 vessels | 12-25 vessels (commercial data) |

| Vessels stranded in Persian Gulf | ~0 | ~500 vessels (including 220 oil tankers) |

| LME aluminium price (June 19) | Stable | ~USD 3,400 per tonne |

| Rotterdam/US Midwest premiums | Baseline | Rising sharply |

When government-reported transit figures diverge sharply from independent maritime intelligence data, commodity markets face a dual-uncertainty problem. Neither the scale of disruption nor the pace of recovery can be reliably priced, which forces traders into defensive positioning rather than directional conviction. For a deeper assessment of how these dynamics are reshaping trade flows, UNCTAD's analysis of Hormuz disruptions provides important context on the broader economic implications.

The Re-Mobilisation Problem: Why Recovery Is Slower Than Markets Expect

Even if diplomatic negotiations produce a formal agreement on safe passage, the operational reality of restoring normal shipping volumes is considerably more complex than a policy announcement can resolve.

Reports indicate that sections of the central Strait have been mined, rendering direct navigation routes temporarily unsuitable for commercial traffic. Vessels are currently confined to limited inshore corridors near the coastlines of Oman and Iran, a constraint that significantly limits both traffic volume and the size of vessels that can safely transit.

The re-mobilisation challenge is compounded by the scale of the backlog. Roughly 500 vessels, including approximately 220 oil tankers, have remained stationary in the Persian Gulf for months. Before these ships can re-enter active service, many will require inspections, maintenance work, and resupply operations. Industry analysts estimate the full normalisation of shipping flows could take several months after security conditions stabilise.

Kpler's lead oil analyst Matt Smith has noted that transit activity is showing a modest pickup following diplomatic engagement, but that no major operator has yet committed to resuming full-scale transits. The absence of a clear "first mover" among major shipowners reflects persistent risk aversion in the face of elevated war risk insurance premiums and unresolved physical security concerns.

BIMCO's Chief Safety and Security Officer Jakob Larsen has confirmed that despite ceasefire discussions, the security environment for commercial shipping remains volatile. Larsen noted that the signing of a ceasefire agreement does not, in itself, resolve the security risks facing vessel operators navigating the strait.

How Aluminium Prices Are Responding: The Premium Signal

Is the LME Price Telling the Full Story?

Financial markets have so far interpreted the disruption as temporary rather than structural. LME aluminium prices remained relatively stable at approximately USD 3,400 per tonne as of June 19, without the sharp spike that a prolonged supply shock would typically generate. Brent crude edged lower during the same period, and major Asian equity markets posted gains, suggesting institutional investors are not yet modelling a sustained disruption scenario into their base cases.

This apparent calm at the benchmark level, however, masks a more telling signal in the physical market. Regional premiums in both Rotterdam and the US Midwest have risen sharply, reflecting real tightness in spot supply that the futures market has not yet fully priced. Furthermore, this divergence between spot physical premiums and LME benchmark pricing is one of the most important early warning indicators for a more significant aluminium pricing event. Analysts tracking aluminum at multi-year highs have flagged precisely this gap as the critical signal to monitor.

The pattern is well established in commodity market history: physical premiums typically lead LME price movements during supply disruptions because spot buyers face actual shortages while futures participants continue to price recovery expectations. If diplomatic progress stalls and shipping volumes do not recover within coming weeks, the conditions for a rapid LME repricing event will be firmly in place.

The alumina market is also experiencing trade flow distortion that will feed back into smelter cost structures. Shipments diverted away from Gulf destinations are reportedly being absorbed at higher rates by China, a rebalancing that creates secondary pricing pressure and eventually flows through to global smelter operating economics.

Geographic Exposure: Who Bears the Greatest Risk?

Not all regions face equal vulnerability to the Strait of Hormuz aluminium trade disruption. The exposure profile varies significantly by geography and by the specific nature of each region's dependency.

Europe carries the highest structural exposure among importing regions. Approximately 20 percent of the continent's primary aluminium supply is sourced from Middle Eastern producers, a dependency that has developed over decades as Gulf smelters expanded production capacity. In addition, Europe has limited short-term alternative sourcing options at comparable cost and volume, making it the most vulnerable major consuming region.

Asian economies including Japan, South Korea, and Taiwan face a compounded exposure profile. They are significant importers of Gulf aluminium but also depend heavily on Gulf LNG for electricity generation. A sustained Hormuz disruption therefore threatens both their metal supply chains and the energy economics of their domestic smelting operations simultaneously.

The United States faces Midwest premium escalation that is already underway, with exposure compounded by the impact of US aluminium tariffs that limit flexibility in redirecting procurement toward alternative origin sources.

The industry segment risk hierarchy, ranked by immediacy of operational impact, breaks down as follows:

- Gulf-based primary aluminium producers face the highest immediate operational risk, caught between export pathway disruption and incoming raw material constraints.

- European aluminium importers and downstream manufacturers face the highest supply security risk among consuming regions.

- Global aluminium traders are exposed to premium volatility and sharply elevated logistics costs.

- Asian smelters dependent on Gulf LNG face indirect but meaningful energy cost transmission risk.

- Downstream fabricators and end-use industries across automotive, aerospace, and packaging face delayed but significant cost pass-through exposure as the supply shock works through the value chain.

The next major ASX story will hit our subscribers first

The Energy Dimension: The Risk Most Buyers Are Not Pricing

Aluminium smelting is one of the most electricity-intensive industrial processes in the global economy, with power costs typically representing the single largest operating expense for a smelter regardless of geography. This creates an indirect exposure mechanism that extends far beyond the Gulf itself.

Smelters across Asia, Europe, and other major producing regions maintain meaningful dependency on oil and LNG originating from the Gulf for electricity generation. Any sustained tightening of energy supply flows through the Strait would elevate electricity generation costs across smelting regions that have no direct physical connection to the conflict zone.

This energy transmission channel is largely invisible in standard supply chain risk analysis, which tends to focus on metal trade flows rather than the energy inputs that make production possible. It represents a second-order vulnerability that becomes a first-order problem if the disruption extends beyond a few weeks. Consequently, the economics of green steel pricing and low-carbon metal production are increasingly being viewed as a hedge against exactly this kind of fossil fuel dependency exposure.

"For aluminium producers, traders and downstream consumers, the concern extends beyond metal shipments to the broader question of whether reliable and affordable energy can be maintained. This dual challenge of raw material supply chain security and energy economics is the defining operational tension of a prolonged Hormuz disruption."

Diplomatic Mechanisms and the Gap Between Agreement and Reality

Swiss-hosted diplomatic talks between the US and Iran have incorporated maritime security as a formal agenda item, with Iranian Foreign Ministry spokesperson Esmaeil Baghaei confirming that a mechanism for safe passage discussions was established through negotiations. This represents meaningful diplomatic progress in acknowledging the shipping crisis as a bilateral priority.

However, the gap between establishing a negotiating mechanism and achieving verifiable, consistent vessel transit restoration is considerable. Ceasefire discussions have not yet translated into the physical mine clearance, operational vessel re-mobilisation, and insurance market recalibration that shipping normalisation actually requires. These are sequential steps, each with its own timeline, and diplomatic progress on one does not automatically accelerate the others.

For commodity markets, this sequential dependency is critical to understand. A ceasefire announcement is a necessary condition for shipping normalisation, but it is far from a sufficient one.

Frequently Asked Questions: Strait of Hormuz and the Aluminium Market

How Much Aluminium Passes Through the Strait of Hormuz Annually?

The GCC region ships approximately 5.5 million tonnes of primary aluminium through the Strait of Hormuz each year, representing a significant share of global seaborne aluminium trade.

What Percentage of Global Aluminium Production Comes From the Gulf?

The Gulf Cooperation Council region accounts for approximately 8 to 9 percent of total global aluminium output. Among the top aluminium producers globally, several Gulf-based operations rank as critical swing suppliers, making any sustained corridor disruption a material supply event for world markets.

How Quickly Could Gulf Smelters Face Production Cuts If Alumina Imports Are Restricted?

Gulf smelters typically maintain alumina inventory buffers of only three to four weeks. If inbound raw material shipments are restricted beyond this window, production curtailments become a realistic near-term operational outcome.

Why Are LME Aluminium Prices Not Rising Sharply Despite the Disruption?

Financial markets appear to be pricing a temporary rather than structural disruption scenario. Physical premiums in Rotterdam and the US Midwest have risen more sharply than LME benchmark prices, reflecting the difference between spot physical market tightness and longer-term futures market sentiment.

Which Countries Are Most Exposed to a Hormuz Aluminium Disruption?

Europe faces the greatest structural exposure, with approximately 20 percent of its primary aluminium supply sourced from the Gulf. Japan, South Korea, and other Asian economies face compounded exposure through both metal imports and LNG energy dependency.

What This Episode Reveals About Long-Term Supply Chain Vulnerability

The concentration of 8 to 9 percent of global aluminium production in a region served by a single maritime chokepoint is not a new vulnerability. It is a structural feature of the industry that has been systematically underpriced by global markets for decades, largely because the Hormuz passage has historically functioned without prolonged interruption.

The current Strait of Hormuz aluminium trade disruption is a stress test of assumptions that were never properly examined. The dual-directional disruption mechanism, blocking metal exports while simultaneously constraining raw material imports, creates a compounding supply shock dynamic that is more severe than any simple trade route closure model would suggest.

Rising physical premiums ahead of LME price movement remain the primary early warning signal to monitor. Diplomatic progress on maritime security mechanisms is necessary but insufficient. Physical mine clearance, vessel re-mobilisation, and insurance market recalibration must all occur in parallel before shipping volumes can return to pre-conflict norms.

The broader lesson for aluminium supply chain strategy is that energy corridor dependency must be evaluated alongside metal trade route exposure as a first-order risk category, not an afterthought. Industries that rely on the most energy-intensive metals in the world cannot afford to treat the energy supply chains underpinning their production as separate considerations.

Disclaimer: This article contains forward-looking analysis, scenario projections, and market commentary intended for informational purposes only. It does not constitute financial or investment advice. Commodity prices, shipping volumes, and geopolitical developments referenced are based on publicly available data and are subject to rapid change. Readers should conduct independent research and seek qualified professional advice before making any investment or procurement decisions.

Want to Capitalise on ASX Mineral Discoveries Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across more than 30 commodities — including those exposed to global supply chain disruptions like the one reshaping aluminium markets today — turning complex data into actionable investment insights. Explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.