August 1, 2026

Asia's Oil Arteries Under Siege: What Happens When the World's Most Critical Chokepoint Closes

Energy security has long been treated as a planning problem rather than a crisis scenario. For decades, Asian economies constructed their industrial foundations on a single, reliable assumption: that Gulf crude would flow continuously through one narrow waterway. That assumption is now being stress-tested in real time. The Strait of Hormuz closure impact on Asia oil supply has moved from theoretical risk to operational emergency, and the arithmetic of the shortfall is stark enough to demand serious attention.

When big ASX news breaks, our subscribers know first

The Waterway That Runs Asia's Industrial Machine

To understand the depth of the current crisis, it helps to think about the Strait of Hormuz not as a geopolitical flashpoint but as a piece of physical infrastructure. It functions, in practical terms, like a single-lane bridge carrying the fuel supply of an entire continent. There is no bypass. There is no redundant route that comes close to matching its capacity.

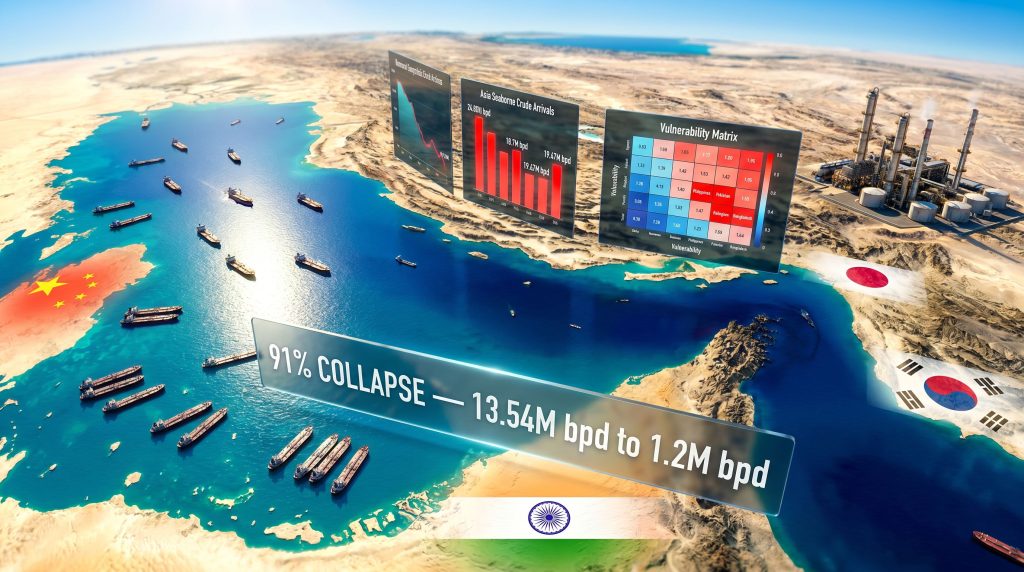

In 2024, roughly 84% of all crude oil and condensate volumes transiting the strait were bound for Asian markets. The receiving nations form the backbone of the global manufacturing economy: China, India, Japan, South Korea, Taiwan, and a string of Southeast Asian states whose refining sectors were deliberately built around the specific grades of crude that Gulf producers supply.

The volume data tells the most important part of the story:

| Metric | Volume / Figure |

|---|---|

| Average monthly crude arrivals in Asia (3 months to Feb 2026) | 24.82 million bpd |

| Asia seaborne crude arrivals in April 2026 | 18.7 million bpd (lowest in 10+ years) |

| Asia seaborne crude arrivals in May 2026 | 19.47 million bpd |

| Decline from pre-disruption baseline | ~22% below three-month average |

| Estimated supply shortfall | >5 million bpd |

| Hormuz transit volumes reaching Asia in May 2026 | ~1.2 million bpd |

| Pre-disruption Hormuz transit average (3 months to Feb 2026) | 13.54 million bpd |

The collapse from 13.54 million bpd to just 1.2 million bpd through the strait represents a reduction of over 91% in Hormuz-routed crude reaching Asia within a matter of months. By any historical standard, this qualifies as one of the most severe acute supply disruptions in modern energy market history.

A critical detail that receives insufficient attention in mainstream commentary is the crude grade compatibility problem. Asia's refining infrastructure was not built for generic oil. It was engineered around specific light-heavy blending ratios derived from Gulf producers. When those grades disappear, refiners cannot simply switch to an alternative crude without adjusting processing configurations, catalyst formulations, and output yield structures. The disruption is therefore not just volumetric. It is also qualitative.

Why US Crude Cannot Fill a 5 Million Barrel Per Day Gap

The instinctive policy response in Western commentary has been to point toward American crude exports as a natural substitute. The United States has, undeniably, expanded its export capacity considerably in recent years. Asian buyers have accelerated procurement from US suppliers. However, the substitution arithmetic simply does not work at the scale required, and crude oil price trends heading into this period already signalled the structural tightness underlying these markets.

| Supply Source | Incremental Capacity Available | Key Constraint |

|---|---|---|

| United States (WTI/shale) | Moderate uplift possible | Port infrastructure, voyage time to Asia |

| West Africa (Nigeria, Angola) | Limited spare capacity | Existing contract commitments |

| Latin America (Brazil, Guyana) | Growing but slow to ramp | Long-haul freight costs |

| North Sea / Norway | Small volumes | Primarily European-oriented |

| Russia (sanctioned routes) | Uncertain and politically complex | Sanctions compliance risk |

Beyond raw volume constraints, there are infrastructure realities that economic commentary tends to gloss over. US export terminals face binding throughput limits. Voyage durations from Gulf Coast loading ports to East Asian refineries are materially longer than Gulf-to-Asia transit times. Longer voyages mean more vessels are required to maintain equivalent delivery frequency, and the global tanker fleet cannot be conjured into existence quickly.

What this means practically is that even maximum utilisation of every available alternative supplier would leave Asia's refineries running well below the feedstock volumes required to sustain normal output. The gap of more than 5 million bpd is not a rounding error. It is a structural shortfall.

How Asian Refiners Are Managing the Crisis: A Three-Stage Progression

The operational response of Asian refineries has followed a recognisable sequence, and understanding where markets currently sit within that sequence matters enormously for anyone trying to anticipate what comes next.

Stage 1: Inventory Drawdown

In the earliest phase, refineries maintained near-normal processing rates by liquidating commercial crude stockpiles held in onshore tanks and floating storage. This approach preserved the appearance of operational continuity while the underlying supply position deteriorated. Commercial inventories, however, are not designed to absorb multi-month supply deficits. They represent a buffer measured in weeks, not a structural solution.

Stage 2: Strategic Reserve Activation

Several Asian governments have moved toward activating or considering strategic petroleum reserves to sustain refinery feedstock supply. Japan and South Korea maintain government-mandated SPR levels that, on paper, represent meaningful cover. The critical limitation is that strategic reserves are calibrated for short-duration disruptions, typically those lasting days to a few weeks. A sustained Hormuz closure measured in months places these systems under a fundamentally different kind of stress than they were designed to withstand.

Stage 3: Forced Throughput Reduction

This is the stage that carries the most consequential downstream effects. Refineries across multiple Asian markets have begun cutting processing rates to extend the useful life of remaining crude inventories. Reduced throughput directly translates to lower output of diesel, gasoline, jet fuel, and petrochemical feedstocks. The downstream cascade from refinery throughput cuts is wide: transport logistics, agricultural operations, manufacturing, and power generation all feel the pressure simultaneously.

The central question confronting energy markets is not whether inventory depletion is occurring. It clearly is. The question is how many weeks of operational buffer remain before refiners face binary choices between shutting processing units or procuring spot crude at crisis-level premiums.

Country-by-Country Exposure: Who Faces the Most Immediate Risk?

The disruption will not be absorbed uniformly across Asian markets. The divergence between well-reserved, credit-worthy importing nations and frontier economies with minimal buffers is where the most severe near-term consequences will emerge. Furthermore, geopolitical trade tensions have complicated the diplomatic pathways that might otherwise accelerate alternative supply arrangements.

| Country | Gulf Import Dependence | SPR Coverage | Vulnerability Rating |

|---|---|---|---|

| Japan | High | ~150-180 days (government + industry) | Moderate-High |

| South Korea | High | ~90-100 days | Moderate-High |

| China | Very High | Significant but opaque | Moderate |

| India | High | Limited (~10-15 days) | High |

| Taiwan | Very High | ~60-90 days | High |

| Philippines | High | Minimal | Very High |

| Pakistan | High | Minimal | Very High |

| Bangladesh | High | Minimal | Very High |

| Vietnam | Moderate-High | Limited | High |

The vulnerability of frontier and developing Asian economies extends beyond simple reserve shortfalls. Nations such as Bangladesh, Pakistan, and the Philippines lack the financial reserves, sovereign credit ratings, and diplomatic leverage required to outbid larger economies for scarce non-Gulf cargoes on spot markets. When China or South Korea enters the spot market, smaller buyers are effectively priced out.

There is a compounding mechanism that deserves emphasis. These countries are typically net refined fuel importers with limited domestic refining capacity. When crude supply tightens, they face a double exposure: shortages of crude feedstock and simultaneous price spikes in imported refined products. Currency depreciation amplifies the problem further, as oil prices rise in US dollar terms, driving inflation through every cost structure in the economy. According to analysis from Zero Carbon Analytics, Asian countries with minimal strategic buffers face disproportionate exposure to precisely this kind of compounding shock.

The LNG Dimension: A Parallel Crisis Running Simultaneously

A dimension of the Hormuz disruption that receives less analytical attention than crude oil is its impact on liquefied natural gas flows. The strait is the primary export corridor for Qatari LNG, one of the world's largest gas supply sources. Qatar's liquefaction capacity represents a significant share of global LNG trade, and a sustained closure disrupts gas flows to China, Japan, South Korea, Taiwan, and a range of South Asian markets simultaneously. The LNG supply outlook for 2025 and beyond had already flagged tightening conditions before this disruption materialised.

The downstream effects of LNG supply disruption cascade through multiple industrial systems:

- Power generation: Countries with high LNG dependency for baseload or peaking electricity face supply constraints when gas import volumes fall, creating potential grid instability during periods of peak demand.

- Industrial processes: Chemical plants, fertiliser producers, steel mills, and cement manufacturers rely on gas as both an energy input and a chemical feedstock. Cost inflation and potential output curtailment affect these sectors concurrently.

- Agricultural supply chains: Fertiliser production, particularly ammonia and urea synthesis which depends on natural gas as a primary input, faces upstream disruption with downstream consequences for food security across Asia's agricultural economies.

The LNG dimension transforms what might appear to be an oil market problem into a multi-vector energy security crisis affecting electricity, industry, agriculture, and transport simultaneously.

The next major ASX story will hit our subscribers first

How Refined Fuel Prices Adjust When Supply Falls Short

When physical crude supply falls materially below refinery demand, markets do not simply freeze. They clear through a price mechanism that forces demand to contract toward available supply. The process is economically painful, and it is not distributionally neutral. In addition, OPEC's market influence over production decisions adds a further layer of uncertainty to how quickly alternative barrels can be mobilised at scale.

The price transmission sequence operates as follows:

- Crude feedstock scarcity drives refinery throughput cuts, reducing refined product output volumes.

- Lower product output creates regional shortages, pushing spot product prices to elevated premiums over normal levels.

- Elevated spot prices translate into retail fuel price increases, rationing consumption through cost.

- Demand rationing propagates through the broader economy, compressing GDP growth, accelerating inflation, and widening current account deficits in oil-importing nations.

The sectors most exposed to this transmission mechanism include:

- Transport logistics, where freight costs rise and feed into the price of all physical goods.

- Agricultural operations, dependent on diesel for irrigation systems, harvesting equipment, and supply chain logistics.

- Energy-intensive manufacturing, facing simultaneous input cost increases and demand softening from their own customers.

- Government fiscal positions, as fuel subsidy obligations rise precisely when fiscal resources are under pressure from currency depreciation and weakening growth.

The US Export Policy Wildcard That Markets Are Not Fully Pricing

There is a secondary risk embedded within the current situation that has not yet fully entered market pricing: the domestic political economy of US crude exports. American politicians across both major parties have a well-documented tendency to frame export volumes as a cause of domestic fuel prices, even when the economic evidence consistently refutes this interpretation.

In a globally integrated oil market, restricting US crude exports would not lower retail prices at American filling stations in any meaningful way. It would reduce producer revenues, distort refinery economics, and remove one of the primary alternative supply sources for Asian buyers at precisely the moment when the need for that supply is greatest. The oil market disruption risks stemming from trade policy decisions compound the physical supply challenge considerably.

The intersection of a Hormuz closure and US export restriction politics represents a tail-risk scenario with asymmetric consequences for Asian energy security. Even the credible threat of export curbs could trigger accelerated spot purchasing by Asian buyers, tightening markets further before any policy is enacted.

Scenario Modelling: Four Pathways Forward

| Scenario | Hormuz Status | Duration | Asia Impact |

|---|---|---|---|

| Rapid Reopening | Fully reopened within 2-4 weeks | Short | Moderate: inventory drawdowns replenished, prices normalise |

| Partial Transit | Intermittent access, vessel-by-vessel approval | 1-3 months | Severe: ongoing uncertainty, elevated prices, selective rationing |

| Prolonged Closure | Sustained blockade beyond 3 months | Extended | Critical: forced refinery shutdowns, GDP contraction, fuel rationing |

| Cape Rerouting at Scale | Alternative routing via Cape of Good Hope | Structural shift | High cost: extended voyage times, persistent freight inflation |

The Cape of Good Hope rerouting scenario warrants specific attention because it represents the only available large-scale alternative to Hormuz transit. Diverting tankers around the Cape adds approximately 10 to 14 days to voyage times from the Gulf to East Asian ports. Longer voyages require a proportionally larger vessel fleet to maintain equivalent delivery frequency. The global tanker fleet is finite and cannot be rapidly expanded. The result is a structural freight cost premium embedded into every barrel delivered via this alternative. As the World Economic Forum has outlined, the range of commodities affected by this rerouting extends well beyond crude oil, creating lasting input cost inflation across multiple supply chains even if physical volumes eventually recover.

Frequently Asked Questions: Strait of Hormuz Closure and Asia Oil Supply

What percentage of Asia's oil supply passes through the Strait of Hormuz?

In 2024, approximately 84% of crude oil and condensate shipments transiting the Strait of Hormuz were bound for Asian markets. This concentration makes Asia by far the most exposed region globally to any sustained disruption of the waterway.

How much has Asia's crude oil supply already fallen due to the Hormuz disruption?

As of May 2026, Asia's total seaborne crude arrivals were approximately 22% below the pre-disruption three-month average of 24.82 million bpd, representing a shortfall exceeding 5 million bpd. April 2026 recorded the lowest seaborne crude arrivals in over a decade at 18.7 million bpd, according to Kpler shipping data.

Which Asian countries are most at risk from a prolonged Hormuz closure?

Countries with minimal strategic reserves and high Gulf import dependence face the greatest near-term exposure. Bangladesh, Pakistan, the Philippines, and Vietnam are considered particularly vulnerable due to limited buffer capacity and constrained access to spot market alternatives. India, despite being a larger economy, also carries significant exposure given its relatively limited strategic reserve coverage of approximately 10 to 15 days.

Can US crude exports replace Gulf oil for Asia?

Not at the required scale. While the United States has increased crude exports to Asian buyers, the volume gap exceeds 5 million bpd. No combination of alternative suppliers can currently fill that shortfall. Logistical constraints, vessel availability, crude grade compatibility, and port throughput limitations further restrict the substitution potential.

What happens to refined fuel prices if the strait remains closed?

If the closure persists beyond current inventory buffer levels, refined fuel prices across Asia are expected to rise materially as price-driven demand destruction becomes the market-clearing mechanism. Less economically resilient nations will experience pronounced price spikes, rationing, and potential fuel shortages before larger economies with deeper reserves reach equivalent stress levels.

How long can Asian refineries operate on existing inventories?

This varies by country and individual refinery, but the trajectory of inventory depletion, combined with already-reduced throughput rates, suggests operational buffers for many refiners are now measured in weeks rather than months under a sustained closure scenario. The answer to this question will likely determine the timeline of the next escalation phase in refined product markets.

Asia's Energy Security Model: Structural Flaws Exposed

What the current crisis has laid bare is not merely a supply disruption. It is a fundamental architectural vulnerability in Asia's energy security design. Decades of rapid economic growth were built on the assumption of reliable Gulf supply through a single strategic chokepoint. That assumption reduced costs and simplified supply chain management. It also concentrated systemic risk in a way that is now proving enormously consequential.

Diversification efforts pursued in recent years, including expanded US crude sourcing, African supply relationships, and multi-origin LNG procurement, provide partial resilience. However, they are structurally insufficient to absorb a shock of this magnitude at speed. The Strait of Hormuz closure impact on Asia oil supply has revealed that the margin of safety built into Asia's energy supply architecture is considerably thinner than policymakers, energy planners, and markets had assumed.

For energy analysts, supply chain strategists, and investors, the coming weeks will be defined by three interconnected variables: the pace of inventory depletion across Asian refining markets, the political durability of the Hormuz disruption, and the rate at which alternative logistics chains can credibly scale. Each of these factors carries significant uncertainty, and the interaction between them creates a range of outcomes with meaningfully different economic consequences.

The Strait of Hormuz closure impact on Asia oil supply is not a contained event with a predictable resolution timeline. It is an active stress test of the infrastructure, institutions, and policy frameworks that underpin the energy security of the world's most economically dynamic region.

Disclaimer: This article contains forward-looking analysis, scenario modelling, and market projections based on data available at the time of writing. Energy market conditions are subject to rapid change. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and consult qualified advisers before making any investment or commercial decisions.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Energy Disruptions?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across the commodities most exposed to energy security shifts — turning complex market signals into actionable investment insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.