July 18, 2026

The Anatomy of a Chokepoint: Why Hormuz Closures Keep Reshaping Global Energy

Every few years, the global energy system receives a sharp reminder of how much of its stability rests on a single 33-kilometre corridor of water. The Strait of Hormuz has long occupied a unique position in geopolitical risk theory, not because disruptions are frequent, but because the consequences of a sustained closure are so disproportionately severe. When strategists model worst-case energy supply shocks, the strait appears at the top of virtually every list. What is unfolding in mid-2026 is not a theoretical exercise.

With the Strait of Hormuz shut again as US-Iran fighting restarts, energy markets are being forced to price a scenario that analysts have long warned about but rarely had to confront in sustained form: a formal, declared, and at least partially enforced closure of the world's most consequential maritime energy passage. Furthermore, understanding current crude oil prices in this context requires grasping just how quickly the situation evolved from isolated incidents to a structural supply crisis.

When big ASX news breaks, our subscribers know first

A Pattern, Not an Incident: The Closure Chronology Since February 2026

Understanding the July 2026 situation requires stepping back from the immediate headlines. The current closure is not the first, and the escalation that produced it has been building across several months of fragile ceasefires and renewed hostilities.

| Date | Development | Operational Status |

|---|---|---|

| February 28, 2026 | Iran closes strait after US-Israeli air strikes | Closed |

| April 8, 2026 | Provisional ceasefire produces partial reopening | Partially Open |

| April 18, 2026 | Re-closure following renewed hostilities | Closed |

| June 20, 2026 | Further closure linked to Israeli activity in Lebanon | Closed |

| Early July 2026 | US strikes approximately 140 Iranian military sites | Escalated |

| July 6, 2026 | IRGC strikes three commercial vessels near Oman | Critical Incident |

| July 11, 2026 | Iran formally declares strait closed until further notice | Formally Closed |

The July 11 declaration is best understood as a formal reinstatement of a closure regime that has been intermittently active since late February. Each cycle of opening and re-closure has eroded commercial confidence further, making the cumulative effect on shipping behaviour arguably more damaging than any single closure event. Consequently, the oil market disruption caused by these repeated cycles is compounding in ways that single-event modelling cannot fully capture.

What Ignited the July Escalation

The July 6 maritime incident near Oman served as the immediate flashpoint for the current phase of conflict. Iran's Islamic Revolutionary Guard Corps struck three commercial vessels operating in the area, including a Qatari liquefied natural gas tanker. Iranian authorities stated the ships had disregarded navigational warnings and attempted to transit through a sea-mine-lined corridor without authorisation.

The United States launched retaliatory strikes against Iranian military infrastructure the following day. Iran responded with coordinated missile and drone attacks targeting Gulf military installations where US forces are based. Air raid sirens activated across multiple Gulf states as the exchanges escalated. By July 8, President Trump had publicly declared the existing ceasefire framework finished.

Iran's formal closure announcement on July 11 cited US interference in facilitating alternative transit routes as justification, framing its action as a defensive response to what it characterised as systematic undermining of its strategic position. The IRGC has since been conducting active interdiction operations against vessels attempting unauthorised passage. For a detailed account of the latest US-Iran exchanges, including the formal closure declaration, reporting from the region provides critical ground-level detail.

The Declaration Gap: Iran Says Closed, Washington Says Open

One of the most analytically significant features of the current situation is the direct contradiction between Iranian and American official positions on the strait's operational status.

Iran's position is unambiguous: the waterway is formally closed to commercial traffic, and the IRGC is enforcing that closure through active naval operations. The US government, including statements from President Trump and Vice President JD Vance, maintains that Iran does not hold sovereign authority over the strait and that it remains accessible.

This divergence creates what market analysts are describing as a dual-reality problem. Commodity traders and energy procurement teams cannot rely solely on official government statements when the statements themselves are contradictory. Maritime intelligence data, which tracks actual vessel movements rather than political declarations, shows that commercial traffic has significantly slowed but has not stopped entirely. Some operators are continuing to attempt passage under substantially elevated risk conditions and at dramatically higher insurance costs.

For energy markets, the practical implication is that the strait is operating in a contested zone somewhere between fully open and fully closed, with the precise degree of interdiction fluctuating based on IRGC operational tempo and US military countermeasures.

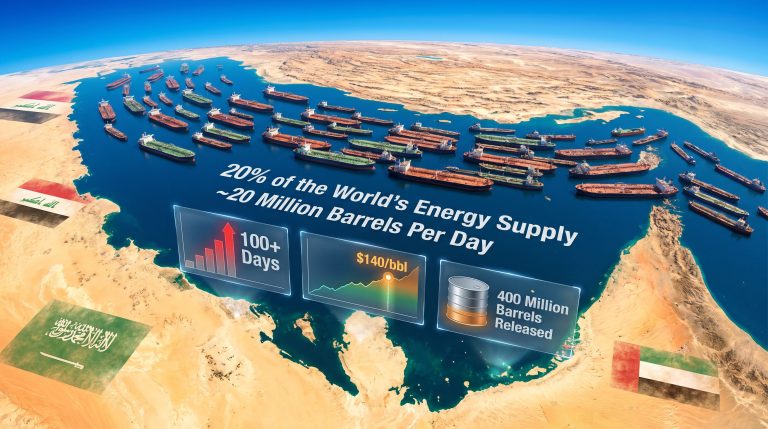

The Scale of What Is at Stake

To understand why the Strait of Hormuz shut again as US-Iran fighting restarts commands such intense institutional attention, it is worth quantifying exactly what passes through this narrow corridor under normal conditions.

- Approximately 20 to 21% of all global seaborne oil trade transits the strait each year

- Roughly 17 million barrels of crude oil per day move through the waterway

- Qatar, the world's largest LNG exporter, routes the substantial majority of its shipments through Hormuz

- The strait also carries significant volumes of refined petroleum products destined for South and Southeast Asian markets

| Commodity | Key Exporters at Risk | Primary Import Markets Affected |

|---|---|---|

| Crude Oil | Saudi Arabia, Iraq, UAE, Kuwait, Iran | Asia-Pacific, Europe, United States |

| Liquefied Natural Gas | Qatar | Japan, South Korea, China, Europe |

| Refined Products | Saudi Arabia, UAE | South Asia, Southeast Asia |

The critical structural vulnerability is that no single bypass route can absorb anything close to full Hormuz volumes. The UAE's Abu Dhabi Crude Oil Pipeline, which routes oil to the Fujairah terminal on the Gulf of Oman, can handle approximately 1.5 million barrels per day. Saudi Arabia's East-West Pipeline, known as Petroline, provides additional capacity. Combined, these alternatives handle a fraction of the 17 million barrels per day that normally transit Hormuz. The arithmetic of the bypass problem is stark.

Oil Price Implications: From Risk Premium to Triple Digits

Australia's Commonwealth Bank has publicly flagged the possibility of oil prices returning above US$100 per barrel if the current closure is enforced effectively over a sustained period. This warning reflects institutional modelling of supply disruption scenarios rather than speculative commentary. In addition, geopolitical oil price analysis consistently highlights how formal closure declarations carry far greater market weight than implied threats alone.

Historical precedent offers some calibration. During the 2011-2012 period of heightened US-Iran tension over Iran's nuclear programme, and again during the 2019 tanker attack incidents in the Gulf of Oman, oil prices experienced spikes of 10 to 25% over relatively short windows. Those episodes involved threats and incidents rather than a formal, declared closure backed by active naval interdiction. The current situation, at least in its declared form, is structurally more severe.

Three broad price scenarios are emerging from institutional analysis:

Scenario 1: Partial Blockade Continues (Assessed as Most Probable)

- Iran maintains selective interdiction targeting vessels using unapproved routes

- Commercial traffic volume falls by 40 to 60% relative to pre-conflict baseline

- Oil prices stabilise at a geopolitical risk premium of approximately US$15 to US$25 per barrel above pre-conflict levels

- Shipping operators continue passage attempts at sharply elevated war risk insurance rates

Scenario 2: Full Enforcement Over Extended Period

- Iran achieves effective interdiction of the majority of commercial traffic

- Global oil supply faces a disruption representing 15 to 20% of normal seaborne volumes

- International Energy Agency coordinates emergency strategic petroleum reserve releases among member nations

- Brent crude breaches US$100 per barrel; LNG spot prices reach multi-year highs across Asian import markets

Scenario 3: Diplomatic De-escalation Within 30 to 60 Days

- Back-channel negotiations produce a revised ceasefire framework

- The strait reopens under internationally monitored conditions

- Oil prices partially retrace the geopolitical premium

- A structural risk discount remains embedded in energy market pricing for six to twelve months thereafter

The next major ASX story will hit our subscribers first

How Energy Markets Are Responding Across Asset Classes

The market response to a formal closure declaration spans well beyond crude oil futures. The cross-asset implications are meaningful for investors tracking energy sector exposure:

- Crude oil futures: Upward pressure on both Brent and WTI benchmarks, with the Brent-WTI spread widening as regional supply constraints bite unevenly

- LNG spot markets: Asian spot LNG prices rising sharply as supply security concerns prompt forward buying. Furthermore, global LNG supply chains are facing compounding pressure as Qatar's export volumes remain constrained

- Integrated energy equities: Major producers with diversified production outside the Gulf corridor seeing share price appreciation as marginal supply value increases

- Tanker stocks: High volatility as operators navigate the tension between elevated freight rates and war risk exposure

- War risk insurance premiums: Surging for vessels operating in or near the Persian Gulf, with some insurers withdrawing coverage for Hormuz transit entirely

- Gulf currency and sovereign credit markets: Under pressure as fiscal stability assumptions for Gulf Cooperation Council members are reassessed

A less commonly discussed dynamic is the differential impact across crude grades. Persian Gulf producers export predominantly medium and heavy sour crude, and Asian refineries that have invested heavily in hydrocracking and desulphurisation capacity to process these grades cannot easily switch to lighter sweet alternatives from Atlantic Basin producers. This refinery configuration mismatch means the price impact of a Hormuz disruption is not uniformly distributed across crude benchmarks.

The Structural Fault Lines Behind the 2026 Conflict

The maritime confrontation is a surface expression of deeper structural tensions that have been building for years. The US-Iran conflict in 2026 is not reducible to a single dispute over shipping lanes. Several underlying drivers are operating simultaneously:

- The status of Iran's nuclear programme and the collapse of multilateral inspection frameworks

- The depth of US-Israeli military coordination in the broader Middle East theatre

- Iran's relationships with proxy networks across the Gulf and Levant regions

- Competition for influence over Gulf maritime corridors as strategic assets

- The role of Israeli military operations in Lebanon in triggering the June 2026 escalation that preceded the July incidents

The July 6 strike on a Qatari LNG tanker is particularly significant from a strategic signalling perspective. Qatar is not a party to the US-Iran conflict, and targeting its commercial shipping communicates Iran's willingness to impose costs on neutral parties as leverage. This raises the geopolitical stakes for Gulf Cooperation Council members who had previously sought to maintain working relationships with both Tehran and Washington. However, oil price movements driven by these geopolitical signals are already filtering through to downstream energy pricing globally.

The Long-Term Energy Security Recalibration

Perhaps the most durable consequence of the recurring Hormuz closures in 2026 will be the acceleration of structural investment in energy supply diversification. For major Asian importing nations, the vulnerability has become impossible to manage through diplomatic hedging alone.

Japan and South Korea, which import the vast majority of their crude oil and LNG from Gulf producers, are accelerating assessments of alternative supply relationships with producers in North America, Australia, and East Africa. India, whose refinery sector is deeply integrated with Gulf crude processing, faces a particularly complex adjustment challenge given both volume and grade dependencies.

European energy planners, already sensitised to supply chain fragility following the 2022 Russian gas crisis, are treating the 2026 Hormuz disruptions as further validation of diversification investment made since that period, while also recognising residual LNG exposure through Qatari supply contracts.

For energy sector strategists, the 2026 Hormuz crisis reinforces a principle that has been gaining institutional momentum: geopolitical risk is not a tail event to be modelled separately from core supply planning, but an embedded structural variable that requires ongoing management. The ongoing coverage of the crisis highlights just how rapidly circumstances can shift when naval interdiction moves from threat to enforcement. The strait being shut again as US-Iran fighting restarts is, in this sense, both an acute crisis and a long-term strategic signal about the fragility of geography-dependent energy systems.

Frequently Asked Questions

What exactly is the Strait of Hormuz and why does it matter?

The Strait of Hormuz is a narrow maritime passage connecting the Persian Gulf to the Gulf of Oman and the wider Arabian Sea. At its narrowest navigable point, it spans approximately 33 kilometres. It functions as the primary export corridor for crude oil produced by Saudi Arabia, Iraq, the UAE, Kuwait, and Iran, and for the bulk of Qatar's LNG exports. Any material disruption to traffic through the strait directly affects global oil and gas supply volumes, with downstream consequences for fuel prices, industrial energy costs, and national energy security planning.

Has the strait been closed before July 2026?

The July 11 closure is the fourth distinct formal or partial closure event since late February 2026. Historically, the waterway has faced threats of closure during previous periods of US-Iran tension, including the 2011-2012 nuclear programme standoff and the 2019 tanker incident period, but sustained enforced closures have been rare in the modern era.

Are there workable bypass routes?

Partial alternatives exist. The UAE's Abu Dhabi Crude Oil Pipeline provides approximately 1.5 million barrels per day of bypass capacity to the Fujairah terminal. Saudi Arabia's East-West Pipeline adds further capacity. However, the combined throughput of available bypass infrastructure represents a small fraction of the 17 million barrels per day that normally transit the strait, meaning no realistic alternative configuration can substitute for Hormuz access at scale.

What does this mean for LNG markets specifically?

Qatar's status as the world's largest LNG exporter means that any sustained Hormuz closure directly constrains global LNG supply. The July 6 strike on a Qatari LNG tanker near Oman underscores the acute exposure of LNG trade. Asian spot LNG prices are already rising in response to supply security concerns, and the markets most exposed are Japan, South Korea, and China, which collectively account for a large share of global LNG imports.

Disclaimer: This article contains forward-looking analysis and scenario modelling based on information available at the time of writing. Energy market conditions, geopolitical developments, and price outcomes remain subject to rapid change. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and consult qualified advisers before making investment decisions.

Want to Track the ASX Opportunities Emerging From Global Energy Disruptions?

When geopolitical shocks like the Strait of Hormuz closure reshape commodity markets, the ripple effects often surface as significant mineral and energy discoveries on the ASX — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment these opportunities are announced, turning complex market signals into actionable insights. Explore how major discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to ensure you're positioned ahead of the market.