July 18, 2026

When Geography Becomes a Liability: The Hidden Architecture of Global Energy Risk

For decades, the global energy system has operated with a structural vulnerability hiding in plain sight. Unlike supply disruptions caused by policy shifts, technological failures, or economic downturns, the concentration of roughly one-fifth of the world's entire oil and liquefied natural gas trade through a single 33-kilometre waterway represents a category of risk that no hedging strategy, reserve mechanism, or diplomatic framework has ever been designed to fully absorb. The Strait of Hormuz global energy security risk is not a theoretical concern discussed in academic papers. As of mid-2026, it is the defining crisis of the modern energy era.

When big ASX news breaks, our subscribers know first

Understanding the Geography: Why 33 Kilometres Can Destabilise the World

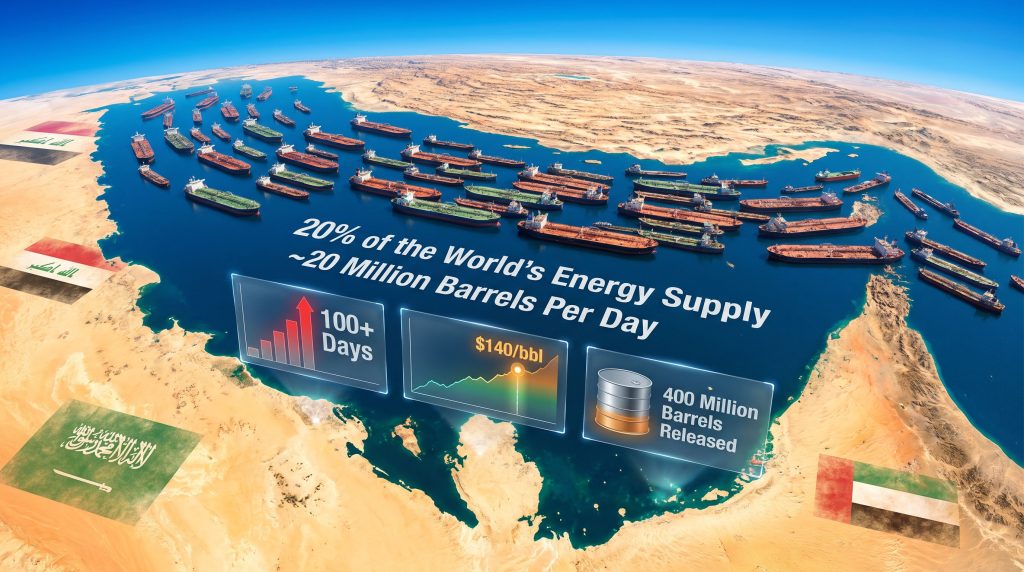

The Strait of Hormuz sits between Iran to the north and Oman to the south, functioning as the sole maritime exit point for crude oil and liquefied natural gas produced by some of the planet's most prolific hydrocarbon exporters, including Saudi Arabia, Iraq, Kuwait, and the United Arab Emirates. Under normal operating conditions, approximately 20% of all global oil and LNG shipments transit this corridor daily.

What makes the Strait categorically irreplaceable is not merely volume but the complete absence of viable alternatives. Overland pipeline infrastructure in the region is limited in throughput capacity and cannot logistically substitute for seaborne transport at scale. No other maritime route exists that could absorb equivalent cargo volumes within any operationally meaningful timeframe. The navigable channel itself, while only 33 kilometres at its narrowest, processes a flow of energy commodities that sustains economies across three continents simultaneously.

This is geography as geopolitical destiny. When the waterway functions normally, its importance remains largely invisible to markets. When it does not, the consequences cascade through every interconnected system in the global economy. Furthermore, the oil and geopolitics dimension of this corridor has long been underestimated by Western policymakers focused primarily on supply-side economics.

The February 2026 Escalation: How the Crisis Was Triggered

The current disruption began on February 28, 2026, when US and Israeli military strikes on Iran triggered a conflict that has progressively strangled transit through the Strait. By mid-July 2026, the blockage had persisted for more than 100 days, making it, by the assessment of senior energy officials including IEA Executive Director Fatih Birol, the most severe oil supply disruption ever recorded in the history of global energy markets. That designation surpasses even the 1973 Arab oil embargo in both scale and systemic reach.

How Severe Is the Disruption? By the Numbers

Raw statistics provide the clearest measure of what is at stake:

| Metric | Current Reality |

|---|---|

| Share of global energy shipments affected | ~20% of all global oil and LNG flows |

| Estimated daily volume halted | ~20 million barrels per day |

| Estimated net crude and products loss | 11–14 million barrels per day |

| Duration of disruption (as of mid-July 2026) | 100+ days |

| Oil price spike scenario (severe disruption) | Up to $140 per barrel |

| Gas price spike scenario | Above $40/MMBtu |

| IEA coordinated emergency reserve release | Up to 400 million barrels |

| Remaining IEA member strategic reserves | ~80% of total holdings still available |

The arithmetic of these figures underscores why no combination of emergency measures can fully replace the corridor's function. Daily flows through the Strait under normal conditions reach approximately 20 million barrels. Even optimistic estimates of what incremental production increases and strategic reserve releases can deliver fall dramatically short of that volume.

Why This Crisis Differs Structurally From Every Previous Energy Shock

The 1973 embargo was politically negotiated and relatively short in duration. The 1990 Gulf War supply shock, while severe, involved a partial disruption rather than a near-complete halt, and the global system at that time carried considerably more shock-absorption capacity. Critically, the Russian sanctions imposed following the 2022 invasion of Ukraine had already consumed a meaningful portion of the global energy system's flexibility before the Hormuz crisis began, leaving the current environment with materially less resilience than any prior comparable episode.

The duration factor also separates this crisis from historical precedents. A disruption exceeding 100 days, with no confirmed diplomatic resolution timeline, moves well beyond the design parameters of existing emergency frameworks, which were engineered for acute, short-duration supply interruptions rather than sustained strategic blockades. Consequently, this oil market disruption has exposed fundamental weaknesses in how the world prices and manages chokepoint risk.

Which Economies Face the Sharpest Exposure?

The geographic distribution of pain has been profoundly unequal. IEA Executive Director Fatih Birol has stated clearly that the disruption has hit Asia with particular severity, given that the region historically sourced 80% to 90% of its energy imports through the Strait of Hormuz. (Reuters, July 17, 2026)

Advanced Asian Economies Under Acute Pressure

Japan and South Korea, both highly industrialised nations with minimal domestic hydrocarbon production, face structural exposure that no amount of energy efficiency improvement can offset in the short term. These economies import the overwhelming majority of the oil they consume, and both have historically relied on Gulf producers routing supply through the Strait.

Developing Nations Bearing the Heaviest Burden

-

Pakistan, Bangladesh, and India have experienced the most acute hardship, with petroleum product prices rising to levels that have effectively removed them from reach for large portions of the population.

-

In lower-income communities across South and Southeast Asia, unaffordability of conventional fuels has pushed households toward biomass-based alternatives including wood and animal dung for cooking, introducing serious respiratory hazards and public health consequences, particularly for women and children.

-

Industrial sectors in import-dependent developing economies face compounding damage through energy-driven inflation across food, transport, and manufacturing supply chains.

The asymmetric nature of this crisis reveals a structural inequity in global energy security architecture. Wealthier nations can absorb price shocks through fiscal buffers and demand substitution. Poorer nations cannot.

Emergency Response Mechanisms: What Has Been Deployed and What Remains

The IEA's Coordinated Strategic Reserve Release

The most significant institutional response came in March 2026, when the IEA coordinated a release of up to 400 million barrels of oil from member nation strategic reserves. The market response was notable: oil prices declined approximately $20 per barrel following the announcement. The IEA's Middle East energy analysis provides additional context on how the agency is framing the long-term structural dimensions of this crisis.

Importantly, this release represented only 20% of total IEA member strategic stockpiles, meaning roughly 80% of collective reserve capacity remained intact. This retained buffer continues to serve as both a practical backstop and a market signal, communicating to traders that further coordinated action remains available if conditions deteriorate.

However, Birol has acknowledged that emergency buffer mechanisms have a finite operational lifespan and cannot sustain indefinite deployment without progressively eroding the strategic safety margin. (Reuters, July 17, 2026)

China's Demand-Side Buffer

China entered the crisis with a strategic oil stockpile exceeding one billion barrels, accumulated prior to the conflict. Additionally, China's rapid domestic deployment of electric vehicles and expansion of public transport infrastructure has reduced the country's per-unit petroleum demand relative to historical growth trajectories. These factors combined have meaningfully moderated what would otherwise have been a more severe demand-driven price spiral.

US Production Increases: Significant but Bounded

The United States, as the world's largest oil and gas producer, has increased output during the crisis. However, the incremental gains achievable, estimated at one to two million additional barrels per day, are structurally incapable of substituting for a 20-million-barrel-per-day maritime corridor. The arithmetic of replacement simply does not function at this scale. Indeed, the oil price shock experienced in prior years provided a warning that many producers and governments chose not to heed.

The next major ASX story will hit our subscribers first

Scenario Modelling: What Happens If the Strait Stays Closed?

| Scenario | Duration | Estimated Oil Price | Key Economic Consequence |

|---|---|---|---|

| Near-term resolution | 0–4 weeks | $90–$100/barrel | Gradual price normalisation |

| Prolonged disruption | 3–6 months | $110–$130/barrel | Sustained inflation, import crises in Asia |

| Severe escalation | 6+ months | $140+/barrel | Global recession risk, energy rationing |

These projections carry significant uncertainty and should be treated as directional scenarios rather than forecasts. Commodity price modelling in active geopolitical conflict conditions involves variables that cannot be reliably quantified. The $140 per barrel upper scenario would represent a price level not witnessed since the most extreme oil market episodes in recorded history, and the associated economic consequences, including global recessionary pressure, food price inflation, and widespread energy rationing, would be severe.

Is the Global Energy System Built to Handle a Crisis of This Duration?

The honest answer is no, and the architecture of existing emergency frameworks makes this apparent. The IEA's coordinated reserve release mechanism was designed with short-duration shocks in mind, calibrated for weeks rather than months. A disruption exceeding 100 consecutive days, involving the world's most critical energy corridor, tests the outer boundary of what these systems were ever intended to manage.

Policy frameworks that appeared adequate in design reveal their limitations when subjected to conditions that were theoretically possible but operationally unprecedented.

The Russian sanctions overhang compounds this structural vulnerability. The global energy system entered the Hormuz crisis with less available shock-absorption capacity than it carried in any of the previous episodes it is now being compared against. Emergency reserves exist and remain substantial, but their efficacy degrades with every additional week of sustained deployment. Furthermore, OPEC market influence over production decisions has added an additional layer of complexity to an already strained supply picture.

Long-Term Implications: Does This Crisis Reshape the Energy Transition?

The Strait of Hormuz global energy security risk has introduced a new dimension into the energy transition debate. On one hand, the acute vulnerability exposed by dependence on fossil fuel flows through a single chokepoint strengthens the strategic case for accelerating renewables deployment and electrification. On the other, the immediate capital demands of navigating the supply crisis have diverted government and corporate attention away from long-term decarbonisation planning.

For Asian governments in particular, the dual pressure is acute. They face urgent need to secure hydrocarbon alternatives in the near term while simultaneously managing international commitments to emissions reduction pathways. China's EV expansion, which has incidentally served as a demand-side buffer during this crisis, illustrates how strategic technology investment can create unexpected resilience.

The lesson for other nations is that energy security and climate strategy are not competing objectives but deeply complementary ones. In addition, insights published by the Energy Transitions Institute on post-crisis energy lessons suggest that nations which invested early in renewables and electrification have shown materially greater resilience during the current disruption. The broader energy transition agenda, consequently, is likely to accelerate as a matter of strategic necessity rather than voluntary commitment.

Frequently Asked Questions: Strait of Hormuz and Global Energy Security

What percentage of global oil passes through the Strait of Hormuz?

Approximately 20% of the world's total oil and liquefied natural gas shipments transit the Strait of Hormuz under normal conditions, making it the single most consequential maritime energy corridor on Earth.

Why can't tankers use an alternative route?

No alternative maritime route exists with the capacity to absorb equivalent volumes. Overland pipeline alternatives serving the region are limited in throughput and cannot replace seaborne transport at scale.

How long can IEA strategic reserves sustain the market?

The IEA's coordinated release of up to 400 million barrels represented approximately 20% of total member strategic holdings. The remaining 80% provides additional buffer capacity, but sustained deployment over many months would progressively erode this safety margin.

Which countries are most affected by the Hormuz blockage?

Asian import-dependent economies face the most severe exposure. Japan, South Korea, India, Pakistan, and Bangladesh are among the most significantly impacted, given that between 80% and 90% of their energy imports historically transited the Strait.

What would oil prices reach in a worst-case scenario?

In a severe escalation scenario involving a prolonged or complete halt to transit, scenario modelling suggests oil prices could reach $140 per barrel, with natural gas prices exceeding $40 per MMBtu. These figures represent directional projections, not confirmed forecasts.

Has this ever happened before?

While the Strait has faced periodic threats and temporary disruptions, the current blockage, persisting for over 100 days and cutting off an estimated 11 to 14 million barrels per day of supply, is assessed by senior energy officials as representing the Strait of Hormuz global energy security risk at its most extreme in recorded history.

Key Takeaways: What the Crisis Reveals About Global Energy Architecture

-

The concentration of global energy flows through a single 33-kilometre waterway represents a systemic architectural risk that markets and policymakers have consistently underpriced across decades of relative stability.

-

Emergency mechanisms including strategic reserves, demand substitution, and production increases provide time-limited relief, not structural solutions capable of replacing the corridor's function indefinitely.

-

The asymmetric burden falling on developing economies in South and Southeast Asia exposes deep inequities in how global energy security is designed and distributed.

-

China's pre-built stockpile and EV adoption illustrate that proactive structural preparation can meaningfully reduce a nation's exposure to chokepoint-driven supply shocks.

-

Diplomatic resolution remains the only pathway to restoring supply at the volume and speed the global economy requires. All other mechanisms are holding actions.

-

The crisis has intensified debate around energy diversification, strategic infrastructure investment, and whether the pace of transition away from fossil fuel dependency needs to accelerate as a matter of national security rather than climate policy alone.

Readers seeking additional context on global energy security frameworks and oil market dynamics can explore related reporting and analysis published by Mining Weekly at miningweekly.com, which covers ongoing developments across the oil, gas, and energy security sectors.

This article contains forward-looking scenarios and price projections that are inherently uncertain. Nothing contained herein constitutes financial or investment advice. Readers should conduct independent research before making any investment or policy-related decisions.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

The energy security vulnerabilities exposed by the Strait of Hormuz crisis underline why investors are increasingly seeking alternative commodity opportunities — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex data across 30+ commodities into actionable insights the moment they hit the exchange. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial to position yourself ahead of the market.