June 21, 2026

Why the World's Most Consequential Waterway Is Now Effectively Closed

Every major energy disruption in modern history has shared a common thread: the vulnerability of geography. No matter how advanced extraction technology becomes, no matter how sophisticated trading infrastructure grows, physical chokepoints remain the single greatest source of systemic risk in global energy supply chains. The Strait of Hormuz has always represented the apex of that risk. The U.S.-Iran talks and Strait of Hormuz closure unfolding now is not merely a geopolitical flare-up — it is a live stress test of a global energy architecture that was never designed to function without this corridor.

When big ASX news breaks, our subscribers know first

The World's Most Critical Oil Chokepoint: What Makes Hormuz Irreplaceable?

Understanding the Strait's Role in Global Energy Architecture

The Strait of Hormuz is a narrow body of water connecting the Persian Gulf to the Gulf of Oman and, beyond it, the Arabian Sea. At its narrowest point, the navigable channel measures approximately 3 miles (5 km) across, though the wider strait spans roughly 21 miles (34 km). This geographic constriction forces an extraordinary concentration of maritime traffic through a space that, on any world map, appears almost insignificant.

Under normal operating conditions, the U.S. Energy Information Administration (EIA) estimates that approximately 20 to 21 million barrels per day of crude oil, condensates, and petroleum products transit Hormuz — representing roughly one-fifth of all petroleum traded globally. No other maritime chokepoint on Earth handles remotely comparable volumes. The Suez Canal, the Strait of Malacca, and the Panama Canal each carry significant energy cargo, but none approach the sheer throughput concentration found at Hormuz.

The nations most dependent on Hormuz for export access include:

- Saudi Arabia — the world's largest crude oil exporter, with the vast majority of its export infrastructure oriented toward the Persian Gulf

- Iraq — heavily dependent on Gulf terminals for crude exports from its southern fields

- Kuwait — almost entirely reliant on Hormuz passage for oil export revenues

- The United Arab Emirates — a major oil and LNG exporter with Gulf-facing export terminals

- Iran — whose entire petroleum export capacity routes through the strait it now helps to restrict

A substantial share of global liquefied natural gas (LNG) exports bound for Asia — including cargoes destined for Japan, South Korea, China, and India — transit Hormuz. The LNG supply outlook for Persian Gulf producers, particularly Qatar, confirms that tanker routing through Hormuz forms the backbone of East Asian supply chains.

What makes Hormuz truly irreplaceable is not simply its volume but the absence of any credible substitute. The Persian Gulf basin holds approximately 48% of the world's proven oil reserves, according to EIA data. The concentration of reserves in a single geographic basin, combined with export infrastructure oriented entirely toward a single exit point, creates a structural vulnerability with no engineering solution at scale.

A Dual Blockade: How Both Sides Are Enforcing Maritime Restrictions

What distinguishes the current Hormuz situation from prior escalation cycles is the simultaneous enforcement of maritime restrictions from both sides of the geopolitical divide. U.S. Central Command initiated a naval blockade targeting Iranian ports and oil export shipping beginning in mid-April 2026. In the first week of enforcement alone, 33 vessels were ordered back to port under U.S. authority, with American forces authorised to use force against mine-laying operations and tankers transporting Iranian crude.

Iran's Islamic Revolutionary Guard Corps Navy (IRGCN) responded by seizing commercial vessels and firing on others, including an Indian-flagged tanker — asserting that the strait would remain effectively closed until Washington lifted its restrictions. The net result is a strategically engineered standstill: neither side alone possesses the capability to fully close Hormuz, but together, their combined enforcement actions have achieved near-total closure.

The IRGCN operates primarily through asymmetric maritime assets — fast attack craft, mine-laying vessels, and small boat swarms — designed for area denial rather than fleet confrontation. Under normal circumstances, these assets cannot close Hormuz unilaterally. Combined with U.S. naval enforcement, however, the effect is structurally equivalent to a full closure, regardless of formal declarations.

Tanker traffic, which under normal conditions makes Hormuz one of the busiest maritime corridors on the planet, has consequently dropped to near zero. This is not a partial disruption or a temporary spike in risk premiums. It represents an unprecedented operational shutdown of the world's single most important energy transit corridor.

How Did U.S.-Iran Tensions Escalate to This Point?

The Strategic Escalation Timeline

A ceasefire took hold in early April 2026, temporarily reducing the probability of full-scale conventional hostilities. Despite the ceasefire, both sides maintained and actively intensified maritime enforcement operations throughout the month. The conflict entered its second month with no functioning diplomatic pathway and an increasingly hardened set of preconditions on both sides.

The U.S. military posture in the region has reached a scale not seen in over two decades. Three carrier strike groups are now deployed near the Persian Gulf — the largest American naval concentration in the region since the 2003 Iraq invasion. This deployment signals both deterrence capability and escalatory readiness, functioning simultaneously as a negotiating instrument and a military threat. Furthermore, the broader geopolitical risk landscape across the Middle East continues to amplify the consequences of this standoff.

The Collapse of Islamabad Mediation Talks

Pakistan was selected as a neutral host for mediated negotiations between Washington and Tehran. A planned diplomatic visit by senior U.S. envoys was cancelled after Iran's submitted proposal was assessed as insufficient by U.S. officials. President Trump publicly characterised the cancelled trip as a waste of time, stating that if Iran wanted to talk, making contact required nothing more than a phone call.

Iran's response was to harden its position further. President Masoud Pezeshkian articulated that his government would not participate in negotiations conducted under duress or while a naval blockade remained in place. Following the U.S. seizure of an Iranian-flagged vessel, Tehran's foreign ministry declined to participate in a second round of talks, accusing Washington of operating without genuine diplomatic intent.

Iran's Conditions for Returning to the Negotiating Table

Iran has articulated a structured three-part framework for resuming dialogue. As of late April 2026, U.S. officials have not publicly responded to any of these conditions.

| Condition | Iran's Stated Requirement |

|---|---|

| Blockade Removal | Full lifting of U.S. naval restrictions on Iranian ports and shipping lanes |

| Compensation | Financial reparations for damages sustained during the conflict period |

| Security Guarantees | Binding commitments against future military action targeting Iranian territory or infrastructure |

The gap between these preconditions and Washington's current posture is substantial. The U.S. has framed the naval blockade as a primary pressure instrument rather than a negotiable concession, making the first of Iran's three conditions structurally incompatible with Washington's stated strategic logic.

What Are the Global Energy Market Consequences?

Oil Supply Disruption: Quantifying the Market Shock

The arithmetic of the Hormuz closure is straightforward and alarming. Under normal conditions, the strait handles 17 to 21 million barrels per day of petroleum flows. With tanker traffic reduced to near zero, the effective supply removed from global markets represents a shock with no modern precedent in terms of volume or duration.

Prior disruptions — the 1973 Arab oil embargo, the Iranian Revolution of 1979, the 1990–1991 Gulf War — all impacted portions of global supply. None produced a simultaneous closure of the world's largest chokepoint combined with active military enforcement on both sides. The scale differential is not incremental. It is categorical. Understanding the broader crude oil volatility trends provides important context for how markets are likely to respond over the coming months.

Buyers across Asia, Europe, and beyond are scrambling to secure alternative cargo sources. The challenge is not simply price — it is physical availability. Spot market activity can redirect existing cargoes, but it cannot manufacture new volumes where none are flowing.

LNG Market Tightening: A Secondary but Significant Disruption

The disruption to LNG flows compounds the crude oil supply shock. Global LNG trade was approximately 360 to 380 million metric tons per year as of 2023, according to International Gas Union data. Persian Gulf LNG exports — primarily from Qatar, the world's largest LNG exporter — represent a critical supply source for Asian energy markets.

With Hormuz effectively closed, LNG carriers bound for Japan, South Korea, China, and India face operational constraints that extend well beyond price. Long-term contract holders are confronting force majeure scenarios. Spot market prices are rising in response to the supply squeeze. For energy-dependent Asian economies, the secondary LNG disruption is in some respects more immediately consequential than the crude oil shock, given their limited ability to switch fuels at short notice.

Freight, Insurance, and Logistics Cascades

The market consequences of a Hormuz closure cascade through maritime logistics in ways that extend far beyond the immediate supply disruption:

- Voyage rerouting around the Arabian Peninsula adds an estimated 10 to 14 days to transit times versus direct Hormuz passage, according to Clarkson Research shipping analytics

- War risk insurance premiums for vessels operating in the Arabian Sea and Persian Gulf have surged, consistent with historical patterns seen during the 1980–1988 Iran-Iraq War Tanker War period

- Port congestion at alternative terminals in East Africa, Oman's Duqm facility, and southern India is compounding logistical bottlenecks as operators seek alternative routing

- Freight cost escalation reflects both the longer voyage distances and the premium commanded for vessels willing to operate in elevated-risk zones

The current disruption is best understood not as a price spike but as a structural supply availability crisis. When physical volumes cannot reach buyers regardless of the price they are willing to pay, spot market mechanisms lose their ability to clear the market efficiently. This is the defining characteristic of a chokepoint closure versus a standard commodity price shock.

How Is the U.S. Framing Its Military and Diplomatic Strategy?

The Strategic Logic Behind Washington's Posture

The Trump administration has maintained the naval blockade as its primary instrument of coercive pressure, treating it not as an act of war but as a leverage tool in an ongoing negotiation. The public framing from Washington is one of strategic patience combined with escalatory credibility — the message being that talks are available on demand, but only on terms Washington deems acceptable.

Privately, U.S. officials have indicated that infrastructure-level consequences for Iran remain on the table if no agreement is reached. The three-carrier-strike-group deployment serves as the physical embodiment of that threat, providing escalatory options ranging from sustained maritime enforcement to precision strikes against Iranian energy or military infrastructure.

Enforcement Operations: The Operational Record

U.S. Central Command's enforcement record since the blockade commenced includes:

- Dozens of vessel redirections and turn-backs in the first weeks of operations

- Seizure of Iranian-flagged vessels transporting crude oil in violation of the blockade

- Authorisation to use force against mine-laying operations in the strait

- Interception of an additional vessel in the Arabian Sea during the final weekend of April 2026

The cumulative operational tempo signals that enforcement is not symbolic. It is sustained, systematic, and designed to impose material costs on Iran's ability to monetise its petroleum exports.

The next major ASX story will hit our subscribers first

What Role Are Regional Powers Playing in the Standoff?

Oman's Quiet Diplomacy and Gulf State Positioning

Oman has historically served as a discreet backchannel between Washington and Tehran, a role it played during the early stages of JCPOA negotiations in 2013 and 2014. Its continued engagement with both sides during the current crisis suggests it remains active in behind-the-scenes mediation, even as formal diplomatic channels remain closed.

Iran and Oman have engaged in bilateral discussions covering regional security and maritime stability in the strait. While no formal mediation framework has emerged, Oman's geographic position — with coastline on both the Gulf of Oman and the Arabian Sea — gives it both strategic relevance and credibility as a neutral interlocutor.

Gulf Cooperation Council (GCC) states face a structural dilemma that deserves closer examination. Their own oil export revenues are entirely dependent on Hormuz remaining navigable, yet their security relationships with Washington constrain their ability to publicly oppose the blockade. Saudi Arabia's East-West Pipeline and the UAE's Fujairah bypass route provide partial relief, but these alternatives cannot compensate for full Hormuz closure at anything approaching the required scale.

Israel, Hezbollah, and the Multi-Front Risk Environment

Continued military activity involving Israel and Hezbollah adds a compounding risk layer to an already complex regional dynamic. Even if U.S.-Iran talks on Hormuz were to produce a partial agreement, the broader regional instability created by interconnected flashpoints means that risk premiums on Middle Eastern energy infrastructure are unlikely to normalise rapidly.

The oil price shock risks associated with multi-front regional instability are increasingly difficult to model with precision. Energy analysts have consequently described the current environment as a compounding risk architecture — where individual flashpoints reinforce each other's market impact rather than operating as discrete, containable events.

Could the Strait of Hormuz Be Bypassed? Alternative Routes and Their Limitations

Existing Pipeline and Overland Bypass Infrastructure

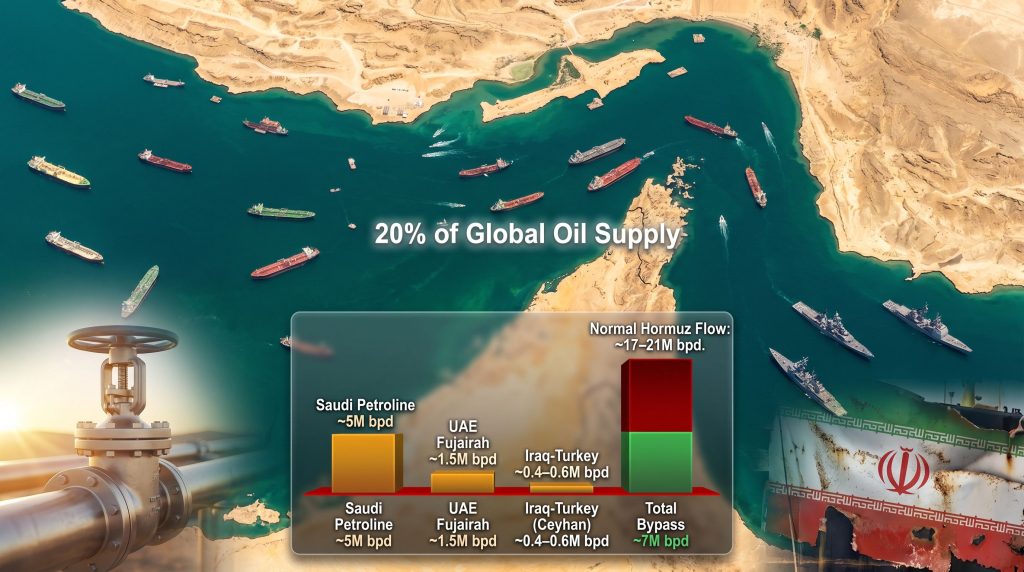

Three primary bypass routes exist that can theoretically divert some Persian Gulf oil flows away from Hormuz:

- Saudi Arabia's East-West Pipeline (Petroline): With a capacity of approximately 5 million barrels per day, this pipeline connects Saudi Arabia's Eastern Province oil fields to the Red Sea terminal at Yanbu. It is the largest bypass route available and has been operational since the 1980s.

- UAE's Habshan-Fujairah Pipeline: Operational since 2012, this pipeline has a capacity of approximately 1.5 million barrels per day and routes UAE crude to the port of Fujairah on the Gulf of Oman, bypassing Hormuz entirely.

- Iraq's Kirkuk-Ceyhan Pipeline: Connects northern Iraqi fields to Turkey's Mediterranean coast, with an operational capacity of approximately 0.4 to 0.6 million barrels per day, though it has operated well below nameplate capacity due to infrastructure maintenance and geopolitical complications.

Why Bypasses Cannot Replace Hormuz at Scale

The arithmetic of bypass capacity versus Hormuz throughput reveals the structural inadequacy of existing alternatives:

| Bypass Route | Approximate Capacity | Coverage of Normal Hormuz Flows |

|---|---|---|

| Saudi Petroline | ~5.0 million bpd | Partial |

| UAE Fujairah Pipeline | ~1.5 million bpd | Limited |

| Iraq-Turkey (Ceyhan) | ~0.4–0.6 million bpd | Minimal |

| Total Combined Bypass | ~7 million bpd | ~35–40% |

Against a normal Hormuz throughput of 17 to 21 million barrels per day, even maximum utilisation of all existing bypass infrastructure leaves a structural supply deficit exceeding 10 million barrels per day. No combination of alternative routing, strategic petroleum reserve (SPR) drawdowns, and demand destruction can bridge a gap of this magnitude over an extended period without significant economic consequences.

A critical and often overlooked constraint is that not all bypass capacity is freely available. Saudi Petroline is optimised for Saudi crude specifically. The UAE's Fujairah terminal handles Emirati production. Neither route can substitute for Iraqi, Kuwaiti, or Iranian volumes, which have no viable overland bypass at scale.

What Are the Near-Term Scenarios for Resolution or Continued Disruption?

Scenario Modelling: Three Possible Pathways Forward

Scenario 1: Negotiated De-escalation (Lower Probability)

Both sides agree to a phased and reciprocal withdrawal of maritime enforcement. Hormuz traffic resumes under a monitored ceasefire framework, and energy markets begin a partial normalisation process. Risk premiums remain elevated as long-term uncertainty persists, but the acute supply disruption is resolved. Given the current gap between stated preconditions on both sides, this pathway carries a low probability in the near term.

Scenario 2: Prolonged Standoff with Managed Escalation (Base Case)

The dual blockade continues for weeks to months. Neither side escalates to full-scale military engagement, but neither concedes the preconditions needed for talks. Energy markets adapt through alternative sourcing, demand adjustments, and SPR releases, while operating under sustained supply stress. Diplomatic back-channels — particularly through Oman — remain active but produce no binding agreement. This scenario is consistent with the current trajectory and carries the highest probability assessment.

Scenario 3: Escalation to Direct Military Confrontation (Tail Risk)

A maritime miscalculation, a significant infrastructure strike, or an uncontrolled escalation spiral triggers broader military engagement. Hormuz closure becomes indefinite or long-term, driving an acute global energy crisis. Major consuming nations draw down strategic petroleum reserves while scrambling to arrange emergency alternative supply arrangements. This scenario carries a low but non-negligible probability given the density of naval assets operating in close proximity.

Frequently Asked Questions: U.S.-Iran Talks and Strait of Hormuz Closure

What percentage of global oil supply passes through the Strait of Hormuz?

Under normal operating conditions, approximately 20% of globally traded petroleum transits through the Strait of Hormuz daily, according to U.S. EIA data. This figure includes crude oil, condensates, and refined petroleum products, and makes Hormuz the single most strategically significant energy chokepoint on Earth.

Why did U.S.-Iran talks collapse in April 2026?

Negotiations broke down after Washington cancelled a planned diplomatic mission to Pakistan, where mediated talks had been scheduled, after assessing Iran's submitted proposal as inadequate. Iran subsequently refused a second round of talks following the U.S. seizure of an Iranian-flagged vessel, with Tehran concluding that Washington was not engaging in good faith diplomacy. The OPEC market influence dynamic has also added complexity to the broader diplomatic calculus.

What are Iran's conditions for reopening the Strait of Hormuz?

Iran has publicly stated three requirements for returning to negotiations: the complete removal of the U.S. naval blockade on Iranian shipping, financial compensation for damages sustained during the conflict, and binding security guarantees against future military action targeting Iranian territory or infrastructure.

Can alternative pipeline routes replace Hormuz oil flows?

No. Existing bypass infrastructure — including Saudi Arabia's Petroline and the UAE's Fujairah pipeline — can collectively handle an estimated 7 million barrels per day at maximum capacity. This covers approximately 35 to 40% of normal Hormuz throughput and leaves a structural supply deficit exceeding 10 million barrels per day that cannot be addressed through alternative routing alone.

How many U.S. carrier strike groups are currently deployed near Iran?

As of late April 2026, three carrier strike groups have been deployed to the region — the largest American naval concentration in the area since the 2003 Iraq invasion.

What is a dual blockade in the context of the Strait of Hormuz?

A dual blockade refers to the simultaneous enforcement of maritime restrictions by both the United States, which is targeting Iranian ports and oil exports, and Iran, which is targeting commercial shipping through the strait. Together, these actions have produced a near-total closure of the waterway that neither side could achieve through unilateral enforcement alone. The 2026 Strait of Hormuz crisis has consequently become one of the most consequential geopolitical events in modern energy history.

Key Takeaways: What the Hormuz Standoff Means for Energy Markets and Geopolitics

The unfolding U.S.-Iran talks and Strait of Hormuz closure represent a convergence of geopolitical, military, and logistical pressures that global energy markets have never faced simultaneously at this scale. Several core conclusions emerge from the current situation:

- The Strait of Hormuz handles approximately one-fifth of the world's total petroleum trade, and no combination of pipeline bypasses, alternative routes, or reserve releases can compensate for its extended closure at current throughput levels

- The dual enforcement architecture, where both Washington and Tehran are simultaneously restricting maritime passage, has produced a chokepoint closure that exceeds what either party could achieve through unilateral action

- Iran's three-part precondition framework for returning to negotiations is structurally incompatible with Washington's current strategic posture, making near-term diplomatic resolution unlikely

- Existing bypass infrastructure covers an estimated 35 to 40% of normal Hormuz flows at maximum utilisation, leaving a supply gap of more than 10 million barrels per day that markets cannot bridge through routing alternatives alone

- LNG disruptions represent a secondary but compounding shock for energy-dependent Asian economies with limited fuel-switching capacity

- Regional actors including Oman and selected GCC states remain engaged in quiet diplomacy, representing the most viable pathway toward de-escalation given the current state of formal diplomatic channels

- The three-carrier-strike-group U.S. deployment signals escalatory readiness beyond maritime enforcement, maintaining the risk of broader military confrontation as a non-trivial tail outcome

This article contains forward-looking analysis, scenario modelling, and geopolitical assessments that involve inherent uncertainty. Readers should not treat scenario probability assessments or market impact projections as investment advice. Geopolitical situations evolve rapidly, and outcomes may differ materially from scenarios described. Energy market participants and investors should consult qualified financial and geopolitical risk advisors before making decisions based on any information contained herein.

For ongoing coverage of upstream energy developments and Middle East regional dynamics, World Oil provides detailed reporting at worldoil.com.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Energy Disruptions?

When geopolitical shocks reshape commodity markets at this scale, the ability to identify significant mineral discoveries the moment they are announced can be the difference between opportunity and missed advantage. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex market signals into actionable insights for investors at every level — and a 14-day free trial lets you experience firsthand why historic discoveries have generated extraordinary returns.