July 28, 2026

Africa's Hidden Energy Fault Line: Why a Persian Gulf Chokepoint Determines the Cost of Living for Hundreds of Millions

Every time geopolitical tension flares in the Persian Gulf, a predictable pattern emerges in financial markets: crude oil futures spike, shipping stocks rally, and energy analysts update their price forecasts. What receives far less attention is the asymmetric damage this pattern inflicts on fuel-import-dependent economies sitting thousands of kilometres from the conflict zone. Nowhere is this asymmetry more pronounced than across the African continent, where the latest disruptions surrounding the Strait of Hormuz crisis and African fuel markets are converging into a serious economic stress event.

Understanding why Africa bears such disproportionate exposure requires looking beyond crude oil prices alone and examining the full architecture of how refined petroleum products move from Middle Eastern export terminals to African fuel pumps. The crude oil geopolitical tensions driving this crisis are reshaping supply routes and cost structures in ways that ripple far beyond the Gulf region.

When big ASX news breaks, our subscribers know first

The Mechanics of the World's Most Consequential Energy Corridor

The Strait of Hormuz is a narrow maritime passage separating Iran from Oman, and its strategic importance to global energy trade is virtually unmatched. Roughly one-fifth of all crude oil and petroleum product exports worldwide transit this corridor on any given day. The concentrated nature of this flow means that even partial disruptions generate outsized consequences for global supply balances.

Energy analysts have modelled scenarios in which a sustained closure could remove between 8 and 10 million barrels per day from global circulation. To contextualise that figure: total global oil consumption sits at approximately 100 million barrels per day, meaning a full closure would eliminate roughly one-tenth of worldwide supply almost immediately. The resulting price shock would be transmitted to every fuel-importing economy on earth, but the severity of that transmission varies enormously depending on a country's structural buffers.

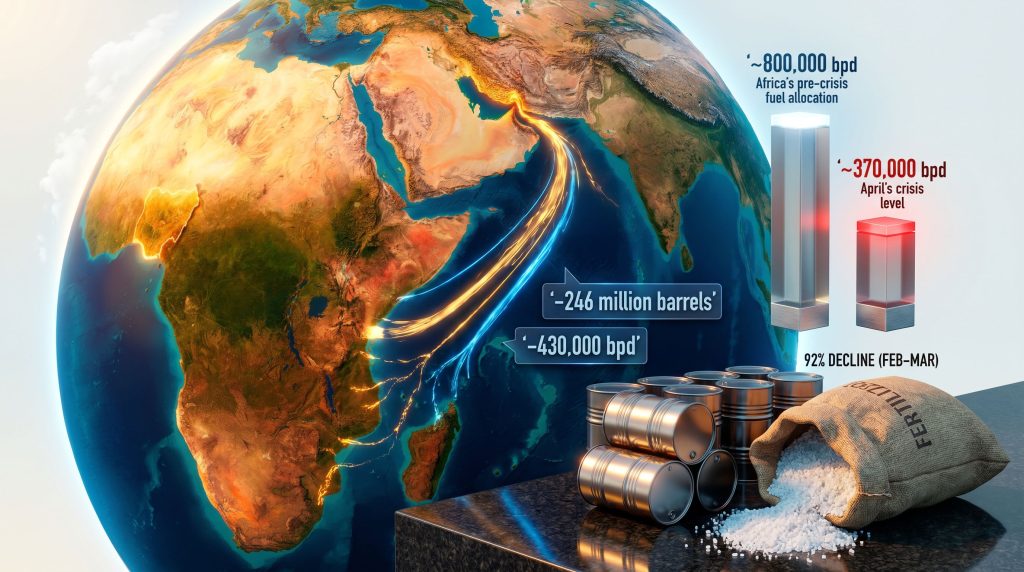

What distinguishes the current episode from previous Hormuz tension cycles is the sustained pace at which global oil inventories have been drawn down. According to the International Energy Agency's latest oil market report, observed global oil stocks have declined by a cumulative 246 million barrels since the conflict began. That volume represents nearly one full week of worldwide oil consumption, and the drawdown shows no sign of stabilising.

The pace of depletion accelerated rather than moderated as the crisis deepened:

- A 129 million-barrel inventory decline was recorded in March

- An even steeper 117 million-barrel fall followed in April

- The IEA has flagged that shrinking global oil buffers materially increase the probability of additional price spikes in coming months

When inventories contract at this velocity, the market loses its shock-absorber capacity. Any further supply disruption, however temporary, risks triggering a price response far larger than the underlying physical shortage would otherwise justify.

How a Persian Gulf Disruption Becomes an African Inflation Problem

The pathway from Hormuz to an African fuel pump involves multiple compounding mechanisms, each of which amplifies the original shock before it reaches the end consumer. Furthermore, the oil market disruption generated by sustained geopolitical instability adds yet another layer of complexity to an already fragile import environment.

The Five-Stage Transmission Chain

-

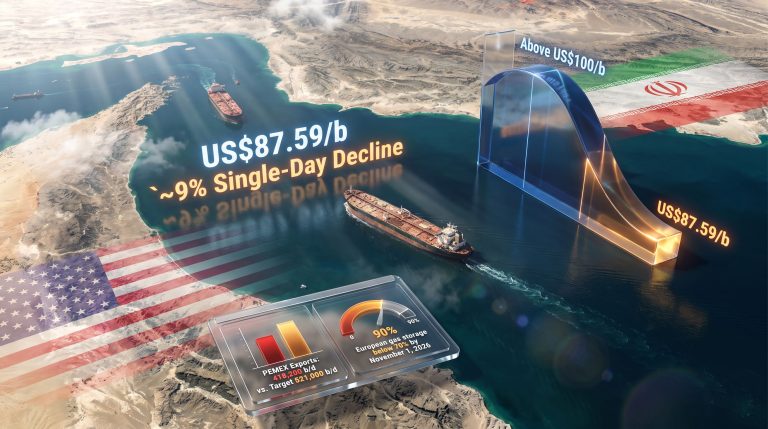

Crude price escalation – Tighter global supply pushes Brent crude toward higher price thresholds, with analysts identifying the $100 per barrel level as a plausible outcome under sustained disruption conditions

-

Freight and insurance cost pass-through – Shipping operators rerouting around the Strait face longer voyage distances, higher fuel burn, and elevated war-risk insurance premiums that are systematically passed to importers through freight surcharges

-

Refined product shortages – Middle Eastern refiners and exporters supply significant volumes of diesel, gasoil, petrol, and jet fuel directly to African markets; when export volumes contract, regional shortages develop independently of crude price movements

-

Currency amplification – Since African fuel imports are denominated in US dollars, any weakening of local currencies inflates import costs even when global crude prices hold steady

-

Broad consumer price inflation – Transport fuel cost increases flow through logistics networks within days, raising prices for food distribution, manufacturing inputs, and essential services across the domestic economy

Africa's Structural Exposure to Refined Product Flows

Africa's specific vulnerability in this crisis is concentrated in refined petroleum products rather than crude oil. The continent does not primarily import crude and refine it domestically; it imports finished fuels directly. This exposes African buyers to disruptions at every point in the Middle Eastern supply chain, from crude extraction through to refining and export.

The scale of Africa's dependence on Middle Eastern refined fuel exports becomes clear when examined against the broader global picture:

| Metric | Pre-Crisis Baseline | April Crisis Level | Change |

|---|---|---|---|

| Total Middle Eastern fuel exports | ~1.4 million bpd | ~700,000 bpd | -50% |

| Africa's fuel import allocation | ~800,000 bpd | ~370,000 bpd (est.) | -430,000 bpd |

| Europe's fuel import allocation | ~440,000 bpd | Reduced but partially buffered | Offset by ~80% domestic production |

| Cumulative global inventory drawdown | Baseline | -246 million barrels | Equivalent to ~1 week of global consumption |

The contrast with Europe is instructive. European economies produce close to 80% of their fuel requirements domestically, meaning external supply disruptions represent a marginal rather than structural problem. Africa imports approximately two-thirds of its total fuel demand, meaning equivalent supply losses translate into far more severe economic consequences. As detailed in this analysis of Hormuz disruptions on African economies, the structural gap between African and European import exposure is widening rather than narrowing.

The Fertilizer Dimension: A Crisis Within the Crisis

One of the most underreported dimensions of the Strait of Hormuz crisis and African fuel markets story involves agricultural inputs rather than transportation fuels. Fertilizer shipments transiting the Hormuz corridor reportedly declined by as much as 92% between February and March, creating a supply shock that threatens to extend the crisis far beyond the energy sector.

For sub-Saharan African economies with large agricultural employment bases, this is potentially more damaging than fuel price increases alone. The compounding effects include:

- Disrupted planting cycles as farmers face sharply higher fertilizer costs or outright unavailability of key inputs

- Reduced crop yields affecting both domestic food security and agricultural export earnings

- Cascading food price inflation that hits lower-income households with particular severity

- Mining and manufacturing exposure to chemical input supply chains sourced from Middle Eastern producers

The fertilizer supply disruption represents a second-order shock that conventional energy market analysis consistently overlooks. For agricultural economies, the inability to source affordable nitrogen and phosphate inputs during planting season can generate food security consequences that persist for a full growing cycle or longer.

Sector-by-Sector Impact: Where the Pain Is Concentrated

Road Transport and Logistics

Diesel-intensive supply chains absorb the immediate impact within days of a price shock. Small and medium-sized enterprises that operate without fuel hedging mechanisms face a direct margin squeeze, with costs either absorbed into business operations or passed to consumers through higher prices for goods and services.

Aviation

African carriers have begun implementing jet fuel surcharges as Jet A1 prices rise alongside broader refined product costs. South African airlines have already adjusted fare structures in response to fuel cost volatility, and similar pricing adjustments are anticipated across East and West African aviation markets as the disruption persists.

Agriculture and Food Systems

The dual pressure of higher diesel costs for irrigation, harvesting, and distribution, combined with restricted fertilizer availability, creates a compounding burden on agricultural productivity. Countries with high food import dependency face the prospect of imported inflation being further amplified by domestic supply constraints. In addition, South Africa green hydrogen initiatives are gaining renewed strategic attention as governments seek to reduce long-term dependence on imported fossil fuel products.

Industrial and Mining Operations

Energy-intensive industries including mining, cement production, and steel manufacturing face higher operational costs as diesel and industrial fuel prices rise. For Africa's commodity exporters, rising production costs erode export competitiveness at precisely the moment when global commodity prices may otherwise be elevated, creating an awkward offset dynamic for resource-sector revenues.

The Dangote Refinery Factor: A Regional Stabiliser Emerges

Amid the disruption, one significant structural development has emerged that carries long-term strategic implications. West African fuel exports surged to approximately 145,000 barrels per day during the crisis period, more than double the preceding three-month average. This increase was driven substantially by expanded output from Nigeria's Dangote Refinery, the largest petroleum refining facility on the African continent.

The significance of this development extends beyond the immediate supply relief it provides. It demonstrates empirically that regional refining capacity can function as a meaningful counterweight to import dependence during global supply disruptions. The Dangote facility's ability to scale output and redirect refined product flows within the continent validates the strategic logic that has underpinned arguments for African refining investment for decades.

Further reinforcing this trend, Africa's richest man has proposed a $17 billion refinery project in Kenya, which, if realised, would represent a further significant expansion of the continent's domestic refining footprint. Whether this proposal advances depends on financing, regulatory frameworks, and the commercial dynamics of the regional fuel market, but the strategic case is strengthened by precisely the kind of supply shock currently unfolding.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways for African Fuel Markets

Scenario 1: Rapid De-escalation

If Hormuz tensions subside within weeks, global inventories could begin recovering within one to two months. African fuel prices would likely remain elevated for a further quarter as supply chains normalise, but the risk of a prolonged inflationary spiral would diminish significantly. This scenario is considered low probability given the structural nature of the underlying geopolitical tensions.

Scenario 2: Prolonged Disruption With Managed Rerouting (Base Case)

A multi-month disruption scenario sees shipping operators permanently reroute significant volumes through alternative corridors including the Cape of Good Hope route, raising freight costs structurally. African fuel import bills remain elevated, consumer price inflation persists, and the economic case for domestic refining investment strengthens materially. West African ports and logistics hubs emerge as ancillary beneficiaries of increased maritime traffic.

Scenario 3: Severe Escalation (Tail Risk)

In an extreme scenario where Hormuz throughput is severely curtailed for an extended period, Brent crude could approach or exceed the $100 per barrel threshold that multiple energy analysts have identified as a realistic ceiling under sustained supply removal of 8 to 10 million barrels per day. Africa would face acute fuel shortages, potential rationing in the most import-dependent nations, and a severe fertilizer crisis threatening the next agricultural season. Analysts tracking OPEC market influence suggest that cartel decisions in this environment could either dampen or dramatically amplify price volatility depending on member-state responses.

Vulnerability Mapping: Which African Economies Face the Greatest Risk?

Not all African economies face identical exposure. Risk profiles vary significantly depending on four key structural variables:

| Risk Category | Key Indicators | Examples |

|---|---|---|

| High vulnerability | High import dependency, weak FX reserves, no domestic refining, agricultural exposure | Many sub-Saharan and East African nations |

| Moderate vulnerability | Hydrocarbon producer but limited refining capacity, must re-import refined products | Several West African oil exporters |

| Lower vulnerability | Regional refining access, diversified import sources, stronger FX buffers | South Africa, Nigeria (with growing Dangote capacity) |

A particularly counterintuitive aspect of this vulnerability mapping is that several African oil-producing nations face significant fuel cost pressures despite sitting atop hydrocarbon resources. The paradox of exporting crude while importing petrol and diesel leaves these economies exposed to the same supply shock dynamics as non-producers, a structural anomaly that domestic refining investment is the only genuine solution to. As reported by African security analysts, this structural fuel vulnerability has been systematically underestimated in continental energy policy planning.

The Strategic Imperative: Building Energy Resilience Beyond the Crisis

The Strait of Hormuz crisis and African fuel markets situation has created a rare and sharply defined policy window. Governments and development finance institutions are confronting, in real time, the economic cost of a supply architecture that routes continental fuel imports through a single geopolitical chokepoint on the other side of the world.

The structural reforms required to meaningfully reduce this exposure are well understood:

- Scaling regional refining capacity across multiple African sub-regions to reduce dependence on Middle Eastern and European refined product imports

- Developing strategic fuel reserve infrastructure to provide inventory buffers against future supply shocks

- Diversifying import source geography to reduce concentration risk in any single supply corridor

- Accelerating the renewable energy transition for electricity generation and certain transport applications, reducing long-term petroleum import dependency

- Building agricultural input supply resilience through domestic fertilizer production capacity and diversified sourcing arrangements

The Dangote Refinery's demonstrated performance during this crisis provides a proof of concept for the regional refining investment thesis. Scaling that model, combined with a deliberate pivot toward energy supply diversification, represents the most durable path toward reducing the continent's vulnerability to future Hormuz-type disruptions.

The Strait of Hormuz crisis is not primarily an energy story for Africa. It is a development story, a food security story, and an economic sovereignty story. The continent's exposure to a distant maritime chokepoint is a direct reflection of structural investment gaps that have accumulated over decades, and the cost of inaction is now being priced in real time at the fuel pump, in supermarkets, and across agricultural fields from Lagos to Nairobi.

Disclaimer: This article contains forward-looking analysis, scenario projections, and commentary on commodity price movements. These represent analytical perspectives and should not be interpreted as financial advice or investment recommendations. Commodity prices, geopolitical developments, and economic outcomes are inherently uncertain and subject to rapid change.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

While geopolitical shocks like the Strait of Hormuz crisis reshape global commodity supply chains and energy costs across Africa, they simultaneously create significant opportunities in resource exploration and mining equities — and Discovery Alert's proprietary Discovery IQ model scans every ASX announcement in real time, instantly identifying significant mineral discoveries and translating complex data into clear, actionable insights for both short-term traders and long-term investors. Explore historic discoveries and the substantial returns they have generated, then begin your 14-day free trial to position yourself ahead of the next major find.