July 19, 2026

Understanding the Strait of Hormuz: The World's Most Critical Energy Chokepoint

The global energy landscape trembles when massive infrastructure systems face disruption, creating ripple effects that extend far beyond initial supply constraints. Modern economies have become increasingly dependent on complex networks of energy transportation, storage, and distribution that can amplify localised disruptions into worldwide economic shocks. The current Strait of Hormuz closure demonstrates how quickly critical infrastructure can become compromised, triggering immediate supply chain disruptions across global markets. Furthermore, understanding these cascade mechanisms reveals the fragility underlying seemingly robust global markets.

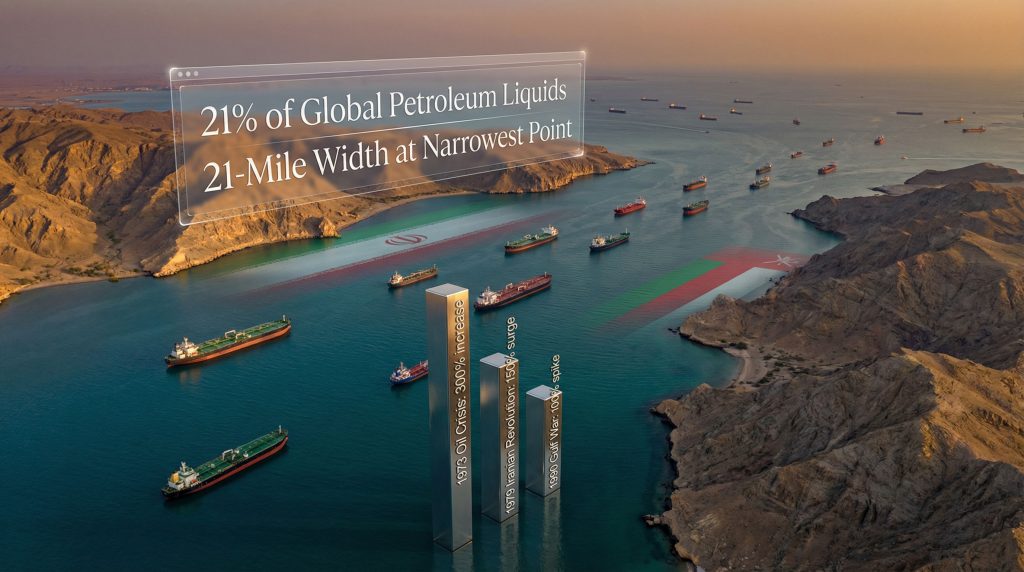

The Strait of Hormuz represents one of the most strategically significant maritime passages in the global energy system. This narrow waterway serves as a critical transit route for approximately 21% of global petroleum liquids, making it an essential artery for international energy flows. At its narrowest point, the strait measures just 21 miles wide, creating a natural bottleneck that concentrates enormous volumes of energy cargo through a relatively confined space.

Recent events have demonstrated the vulnerability of this chokepoint in dramatic fashion. Maritime traffic data shows daily vessel transits plummeting from 138 to just 2 ships, representing a staggering 98.6% reduction in normal shipping activity. This collapse in maritime activity provides concrete evidence of how quickly critical infrastructure can become compromised, triggering immediate supply chain disruptions across global markets.

Geographic and Strategic Importance

The physical characteristics of the Strait of Hormuz create unique operational challenges for maritime traffic. Navigation through this narrow passage requires precise coordination, especially given the high volume of large crude carriers and liquefied natural gas tankers that typically transit these waters. The concentration of such massive energy flows through this geographic pinch point creates inherent systemic risk for global energy security.

Alternative routing options remain severely limited, with most diversionary routes requiring significant additional costs and transit times. The East-West Pipeline system represents one potential bypass mechanism, though capacity constraints limit its ability to fully compensate for lost maritime throughput. Saudi Arabia has been attempting to maximise utilisation of this pipeline infrastructure to redirect flows from the Gulf to Red Sea export terminals, though this represents only partial mitigation of the overall supply disruption.

Historical Precedents and Threat Assessments

Previous closure attempts provide important context for understanding market response patterns and economic consequences. The current situation differs from historical precedents in several key aspects, including the scale of disruption and the technological methods employed to restrict passage.

GPS jamming systems have emerged as a significant technical challenge for maritime navigation, creating chaos that extends beyond simple physical blockade. This technological disruption represents an evolution in chokepoint control methods, adding layers of complexity to traditional maritime security concerns. The consequences of such closures could be catastrophic for global oil markets.

When big ASX news breaks, our subscribers know first

How Does a Hormuz Closure Cascade Through Global Markets?

Energy market disruptions follow predictable patterns of price volatility and supply chain stress, though the magnitude and duration of impacts vary significantly based on the severity and persistence of the disruption. Current price movements demonstrate both the immediate shock effects and the complex market psychology surrounding geopolitical energy crises. However, the oil price rally analysis reveals additional complexities beyond simple supply-demand dynamics.

Recent oil price data reveals dramatic intraday volatility, with Brent crude falling from approximately $120 per barrel to $92, while WTI crude traded at $83.79 with an -$10.98 change (-11.59%). These price swings reflect market uncertainty about both the duration of the disruption and the effectiveness of potential policy responses. In addition, the tariff market impact creates additional layers of price complexity.

Immediate Price Shock Mechanisms

The following table illustrates historical oil price responses to major supply disruptions:

| Crisis Event | Price Impact | Duration | Recovery Timeline |

|---|---|---|---|

| 1973 Oil Crisis | 300% increase | 6 months | 2-3 years |

| 1979 Iranian Revolution | 150% surge | 12 months | 18 months |

| 1990 Gulf War | 100% spike | 3 months | 6 months |

| 2019 Tanker Attacks | 4% jump | 2 days | 1 week |

Current market behaviour suggests traders are weighing multiple scenarios simultaneously. Louisiana Light crude showing +$14.39 (+16.95%) over a 4-day period indicates regional premium development as alternative supply sources become more valuable. Meanwhile, Murban crude at $98.63 with -$11.54 (-10.47%) reflects the complex pricing dynamics affecting Middle Eastern crude grades specifically.

Secondary Market Contagion Effects

Natural gas and LNG markets have experienced severe disruption, with LNG shipping rates soaring 650% to $300,000 per day. This massive increase in transportation costs demonstrates how chokepoint closures create bottlenecks throughout the energy supply chain, affecting not just the restricted commodity but all related transportation and logistics services. Furthermore, the natural gas price trends show additional volatility patterns.

High-sulphur fuel oil (HSFO) prices have jumped 40% as the Singapore bunkering hub faces supply constraints. This secondary effect illustrates how energy supply disruptions cascade through maritime fuel markets, creating additional cost pressures for global shipping operations beyond the directly affected energy exports.

Which Industries Face the Greatest Economic Disruption?

Manufacturing and industrial sectors dependent on petrochemical feedstocks face immediate supply chain stress when major energy chokepoints close. The current crisis has already forced multiple critical facilities offline, demonstrating the interconnected nature of energy infrastructure and downstream industrial production.

Bahrain's Sitra refinery (405,000 barrels per day capacity) has been forced offline and declared force majeure, while the UAE's ADNOC Ruwais facility (922,000 barrels per day capacity) has also halted operations. These facility shutdowns represent approximately 1.3 million barrels per day of combined refining capacity offline, creating immediate shortages of refined products and petrochemical feedstocks.

Transportation and Logistics Sector Impact

The transportation sector faces multiple pressure points during chokepoint closures:

- War risk insurance premiums: Range from 0.5% to 2.5% of cargo value

- Route deviation costs: $500,000 to $2 million per tanker

- Alternative pipeline capacity: Limited throughput compared to maritime routes

- Modal transportation shifts: Increased reliance on overland pipeline systems

Asia's refining margins have soared to 4-year highs as crude supply constraints create profitable arbitrage opportunities for facilities with available feedstock inventory. This margin expansion demonstrates how supply disruptions can create significant economic benefits for certain market participants while imposing costs on others.

Manufacturing and Industrial Consequences

Petrochemical supply chains face immediate stress as feedstock availability becomes constrained. Crack spreads (the differential between crude oil input costs and refined product output prices) have surged, indicating tightening supply conditions for essential industrial inputs including:

- Fertiliser production: Ammonia and urea manufacturing dependent on natural gas feedstocks

- Plastics and synthetic materials: Ethylene and propylene derivatives essential for manufacturing

- Pharmaceutical ingredients: Petroleum-based chemical compounds for medical applications

The closure has created severe shortages in consumer markets, with India facing a severe cooking gas shortage as 90% of its LPG supply typically comes from the Middle East. 14kg LPG cylinders now cost $10 per unit after prices remained unchanged for a full year, demonstrating how supply disruptions translate directly into consumer price inflation.

What Are the Regional Economic Vulnerabilities?

Different regions exhibit varying degrees of exposure to Strait of Hormuz closure impacts based on their import dependency patterns, strategic reserve capacities, and alternative supply arrangements. Asia-Pacific economies show particularly high vulnerability due to their substantial reliance on Middle Eastern energy imports.

Asia-Pacific Exposure Analysis

The following table shows regional oil import dependencies via the Strait of Hormuz:

| Country | Hormuz Dependency | Strategic Reserves | Alternative Sources |

|---|---|---|---|

| Japan | 87% of oil imports | 150+ days consumption | Limited domestic production |

| South Korea | 70% dependency ratio | 96 days consumption | Diversified supplier base |

| China | 43% of crude imports | 90+ days consumption | Russia, domestic production |

| India | 85% of petroleum products | 22 days consumption | Russia, domestic production |

China's crude oil imports jumped 16% year-over-year to average 11.99 million barrels per day in January-February, suggesting strategic stockpiling ahead of the crisis. This pre-positioning demonstrates sophisticated supply chain risk management by major importing economies anticipating potential disruptions.

India's strategic petroleum reserves hold only 30 million barrels across three storage sites, representing minimal buffer capacity compared to consumption needs. This vulnerability has led India to maximise short-haul Russian imports rather than participating in coordinated strategic reserve releases with IEA member countries.

Production Response Mechanisms

Middle Eastern producers have implemented dramatic production cuts in response to export constraints. The OPEC production impact demonstrates coordinated responses to supply disruptions:

- Iraq: 3 million barrels per day production reduction

- Gulf producers collectively: 6.7 million barrels per day output cuts

- Saudi Arabia: Maximising East-West pipeline utilisation for Red Sea exports

These production cuts represent approximately 6-7% of global oil production capacity being temporarily removed from markets, creating immediate supply tightness even as stored crude accumulates in the Persian Gulf region.

European Market Resilience Factors

European economies demonstrate greater resilience due to:

- Diversified supply sources: North Sea production, Norwegian gas, Russian alternatives

- Strategic petroleum reserves: Collective IEA member capacity exceeding 120 million barrels

- Renewable energy infrastructure: Reduced fossil fuel dependency compared to Asia-Pacific

- LNG import infrastructure: Multiple terminal facilities enabling flexible supply sourcing

Europe and Asia are now battling for critical spot LNG supply, with European buyers redirecting cargoes originally destined for Asian markets. This competition illustrates how supply constraints force regional markets to compete directly for limited available resources.

How Do Strategic Petroleum Reserves Function During Crises?

Strategic petroleum reserves represent the primary policy tool for managing short-term supply disruptions, though their effectiveness depends on coordination between major consuming nations and the scale of reserve releases relative to market shortfalls. The current crisis has tested international cooperation mechanisms and revealed limitations in reserve deployment strategies.

G7 finance ministers discussed releasing up to 400 million barrels from strategic reserves but ultimately decided against coordinated action. This decision reflects complex political calculations about reserve depletion, market intervention effectiveness, and the precedent-setting nature of large-scale releases.

Global SPR Capacity and Release Mechanisms

The International Energy Agency coordinates strategic reserve policies among member countries, with total collective reserves of approximately 1.5 billion barrels. Maximum daily release capacity reaches 4.2 million barrels, though sustained releases at this level would rapidly deplete available stocks.

Key strategic reserve holdings include:

- United States Strategic Petroleum Reserve: 714 million barrels

- China's emergency reserves: 550 million barrels (estimated)

- European Union collective capacity: 120 million barrels

- Japan's strategic reserves: 150+ day supply equivalent

Effectiveness in Price Stabilisation

Historical experience suggests strategic reserve releases provide temporary price relief but cannot address sustained supply disruptions. The current crisis demonstrates this limitation, as market concerns about duration and escalation override the short-term supply cushion that reserves might provide.

The Middle East accounts for only 5% of global crude storage capacity (320 million barrels) despite representing one-third of global oil flows. This storage deficit means that even temporary export restrictions quickly create logistical bottlenecks as laden tankers accumulate in the Persian Gulf with no discharge capacity.

What Economic Scenarios Emerge from Extended Closures?

Extended chokepoint closures create cascading economic effects that compound over time, moving from immediate price volatility to structural adjustments in supply chains, investment patterns, and regional economic relationships. Scenario analysis reveals how different closure durations would impact global economic growth and inflation patterns.

Short-Term Impact Modelling (0-30 days)

The following scenario analysis shows potential economic impacts from closure duration:

| Scenario Duration | Oil Price Range | Global GDP Impact | Inflation Acceleration |

|---|---|---|---|

| 0-7 days | $80-100/barrel | -0.1% to -0.3% | +0.5 to +1.0 percentage points |

| 7-30 days | $100-130/barrel | -0.5% to -0.8% | +2.0 to +3.0 percentage points |

| 30-90 days | $130-150/barrel | -0.8% to -1.2% | +3.0 to +4.0 percentage points |

| 90+ days | $150+/barrel | -1.2%+ | +4.0+ percentage points |

Current price movements suggest markets are pricing scenarios in the 7-30 day range, though Qatar has warned oil could hit $150 in weeks if the situation continues to escalate. This price trajectory would place the crisis in the severe long-term impact category with significant GDP consequences.

Medium-Term Structural Adjustments (1-6 months)

Extended closures force permanent changes in global energy infrastructure and trade patterns. This includes addressing the energy exports challenges that affect producer nations:

- Pipeline construction acceleration: 3-7 year development timelines

- LNG terminal expansion: $2-5 billion capital investment per facility

- Alternative route development: Permanent modal shifts from maritime to overland transport

- Regional supply agreement restructuring: Long-term contract renegotiation

Morgan Stanley analysts note that war has flipped the LNG surplus narrative, indicating fundamental reassessment of global gas market balance. This shift from surplus to shortage conditions represents a structural change that will persist beyond the immediate crisis resolution.

The next major ASX story will hit our subscribers first

How Do Financial Markets Price Hormuz Closure Risk?

Financial markets employ multiple mechanisms to price geopolitical energy risks, including futures curve analysis, volatility premiums, and cross-asset correlations. Current market behaviour reveals sophisticated risk assessment processes that extend beyond simple supply-demand calculations to encompass geopolitical probability assessments and policy response expectations.

Oil market psychology during the current crisis reflects optimism that President Trump would call off his war soon, suggesting price movements are heavily influenced by political resolution expectations rather than purely physical supply availability. This psychological component creates additional volatility as markets react to political signals and diplomatic developments.

Derivatives and Risk Premium Calculations

Futures markets provide insight into closure duration expectations through contango and backwardation patterns. When near-term prices exceed distant month prices (backwardation), it typically indicates immediate supply constraints with expectations of eventual normalisation. Current curve structures suggest markets are pricing temporary rather than permanent supply disruption.

Key risk pricing indicators include:

- Volatility index correlations: Energy volatility premiums versus broader market uncertainty

- Credit default swap implications: Sovereign risk assessment for regional economies

- Currency market transmission: Petrodollar recycling disruption impacts

- Cross-commodity spreads: Relative pricing between crude oil, natural gas, and refined products

Market Psychology and Sentiment Drivers

Market behaviour during chokepoint crises reveals the importance of perception management and policy signalling. Brent crude falling back to $92 per barrel after reaching nearly $120 demonstrates how political statements and policy signals can override physical supply constraints in short-term price formation.

The first non-Iranian crude oil carrier (Shenlong tanker operated by Greece's Dynacom shipping company) successfully passing through the Strait since the blockade began provides concrete evidence that absolute closure may not be maintained, influencing market sentiment about supply availability. According to analysis of the strategic importance, no major power can maintain complete control over this vital waterway.

What Are the Long-Term Economic Transformation Effects?

Persistent chokepoint vulnerabilities accelerate structural changes in global energy systems, forcing investments in redundancy, alternative infrastructure, and supply chain resilience that reshape international energy trade patterns. These transformational effects often persist long after immediate crises resolve.

Energy Security Investment Acceleration

Infrastructure development priorities emerging from the crisis include:

- Pipeline construction timelines: 3-7 years for major cross-border systems

- LNG terminal expansion costs: $2-5 billion per facility with 2-4 year construction periods

- Strategic storage expansion: Underground salt cavern development requiring 5-10 year development cycles

- Alternative transportation methods: Rail and truck transport capacity expansion

Korea has implemented price caps on domestic gasoline and diesel at $1.30 per litre, demonstrating how governments intervene to protect consumers from volatile international prices. Such policies create fiscal costs that must be sustained through other revenue sources or deficit spending.

Geopolitical Economic Realignment

The crisis accelerates existing trends toward regional energy security arrangements:

- Trade route diversification: Permanent shift toward overland pipeline systems

- Regional economic bloc strengthening: Enhanced cooperation within geographic regions

- Technology transfer acceleration: Faster deployment of alternative energy systems

- Supply chain regionalisation: Reduced dependence on distant supply sources

Russia's main Black Sea port of Novorossiysk resuming operations after disruptions provides alternative supply routes for consuming nations seeking to reduce Middle Eastern dependency. Such diversification efforts become permanent features of energy security planning.

How Can Economies Build Resilience Against Chokepoint Risks?

Economic resilience against chokepoint disruptions requires comprehensive strategies encompassing supply diversification, strategic inventory management, alternative infrastructure development, and coordinated policy responses. The current crisis provides valuable lessons for designing more robust energy security frameworks.

Diversification Strategy Framework

Effective chokepoint risk management requires multiple parallel approaches:

- Supplier relationship diversification: Multiple source countries and regions

- Transportation route redundancy: Maritime, pipeline, rail, and truck options

- Storage capacity optimisation: Strategic location and capacity sizing

- Contractual flexibility: Spot market access and flexible delivery terms

India's decision to maximise short-haul Russian imports rather than participate in IEA strategic reserve releases demonstrates practical diversification in action. This approach reduces transportation risk while maintaining supply security through alternative supplier relationships.

Policy Response Mechanisms

Coordinated international responses prove most effective during major disruptions:

- Emergency allocation systems: Sharing available supplies among allied nations

- Price stabilisation tools: Strategic reserve releases and consumer protection measures

- International cooperation protocols: Diplomatic engagement to resolve underlying conflicts

- Market intervention coordination: Synchronised policy actions to prevent competitive bidding escalation

South Korea's implementation of transportation fuel price caps illustrates domestic policy responses to international supply shocks. Such measures require fiscal resources but can prevent broader economic disruption from cascading through transportation-dependent sectors.

The current Strait of Hormuz closure demonstrates the critical importance of building resilient energy systems. However, the situation also reveals how geopolitical tensions can quickly transform from localised conflicts into global economic crises affecting every aspect of modern commerce and industry. Consequently, economies must invest in redundant infrastructure, diversified supply chains, and coordinated policy frameworks to maintain stability during future disruptions.

Disclaimer: This analysis is based on current market conditions and publicly available information. Energy market conditions can change rapidly, and past performance does not guarantee future results. Readers should conduct their own research and consult with qualified professionals before making investment decisions related to energy markets or securities.

Looking to Profit from Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including energy and commodity sectors experiencing dramatic market shifts during global supply disruptions. When major chokepoints like the Strait of Hormuz create market volatility, Discovery Alert's immediate notifications help investors identify actionable opportunities ahead of broader market recognition, turning complex mineral data into profitable trading insights.