May 12, 2026

When a Chokepoint Becomes a Continent: The Strategic Logic Behind Iran's Maritime Expansion

The global energy system was not designed with resilience in mind. It was built around efficiency, and efficiency in maritime trade means concentration. Nowhere is that concentration more dangerous than in the network of narrow passages through which the world's oil flows, and no passage carries more systemic weight than the Strait of Hormuz. For decades, energy security analysts warned that a sustained disruption at Hormuz would be without historical precedent in its economic consequences. In May 2026, that warning stopped being theoretical.

When the Islamic Revolutionary Guard Corps formally announced it had widened its definition of the strait into what it described as a vast operational area, stretching from the port of Jask on Iran's southeastern coast to Siri Island deep in the Mideast Gulf, the IRGC widens Strait of Hormuz operational area in ways that have shifted the architecture of global energy security far beyond any single military confrontation.

When big ASX news breaks, our subscribers know first

Why the IRGC's Redefinition of the Strait of Hormuz Is a Watershed Moment in Maritime Law

From Narrow Chokepoint to Strategic Crescent: Understanding the Jurisdictional Shift

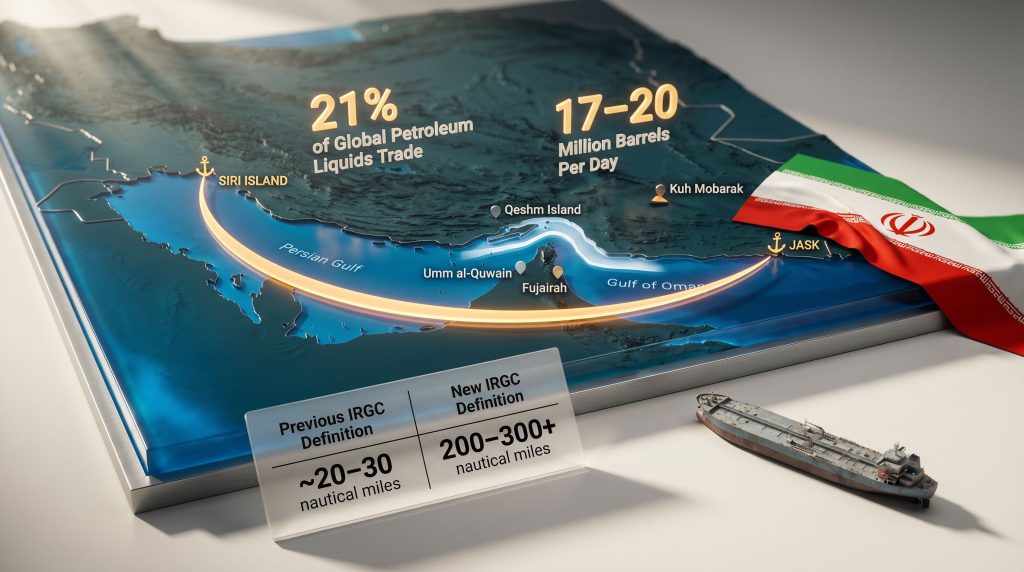

For the better part of modern maritime history, the Strait of Hormuz has been understood as a geographically constrained transit corridor, roughly 20 to 30 nautical miles wide at its most pinched point, governed by well-established international norms that prohibit coastal states from suspending the right of passage even during periods of armed conflict. What the IRGC has now done is functionally dissolve that definition.

According to statements carried by Iranian state media on 12 May 2026, IRGC Navy Deputy Political Director Mohammad Akbarzadeh confirmed that the operational zone had expanded from what was previously described as a limited area around the Hormuz and Hengam islands to a footprint spanning 200 to 300 nautical miles or more. The new area takes the form of what Iranian officials describe as a complete crescent, arcing from Jask in the east to Siri Island in the west.

This is not a symbolic gesture. It is, furthermore, a structural recalibration of where Iranian enforcement authority begins and ends in one of the world's most critical waterways.

What Has Actually Changed: A Comparative Boundary Analysis

| Parameter | Previous IRGC Definition | New IRGC Definition |

|---|---|---|

| Operational Width | ~20-30 nautical miles | 200-300+ nautical miles |

| Western Boundary | Hormuz and Hengam Islands | Siri Island (~70km from UAE's Umm al-Quwain) |

| Eastern Boundary | Narrow strait corridor | Port of Jask, southeastern Iran |

| Shape Descriptor | Linear transit corridor | Complete crescent arc |

| Declared Status | Patrol zone | Full operational control area |

Key Insight: This is the second boundary expansion since the current conflict began. The first, announced on 4 May 2026, extended the zone from the western tip of Qeshm Island to Umm al-Quwain and from Kuh Mobarak to Fujairah. The 12 May declaration explicitly goes beyond those boundaries, suggesting an ongoing and deliberate pattern of incremental expansion.

How Did the 2026 Strait of Hormuz Crisis Reach This Point?

A Timeline of Escalating Jurisdictional Claims

Understanding the current state of the strait requires mapping the sequence of decisions that produced it. The crisis did not emerge fully formed. However, it developed through a series of escalatory steps, each building on the last.

- 28 February 2026: US and Israeli air strikes on Iran trigger the opening phase of the conflict

- 27 March 2026: Iran formally closes the strait to vessels affiliated with the US, Israel, and allied nations

- 6 April 2026: Iran begins permitting selective passage for vessels from nations it considers friendly, creating a de facto corridor system administered by the IRGC

- 8 April 2026: A ceasefire takes effect, though disruption to commercial shipping continues

- 4 May 2026: The IRGC releases two maps delineating an expanded control zone, extending from Qeshm Island to Umm al-Quwain in the west and from Kuh Mobarak to Fujairah in the east

- 12 May 2026: The IRGC announces a further expansion beyond the 4 May maps, formalising the vast operational area doctrine extending from Jask to Siri Island

The Strategic Logic Behind Sequential Expansion

The pattern of incremental boundary announcements is not accidental. Each declaration individually falls short of triggering a decisive military response, yet collectively the steps have achieved a dramatic and potentially irreversible shift in the operational risk environment across the entire Gulf region.

This approach mirrors what international relations scholars sometimes call salami tactics in territorial disputes: a series of small, individually deniable actions that cumulatively produce a new strategic reality. The timing of each expansion correlates with periods of diplomatic stagnation, suggesting the announcements serve as leverage instruments in the broader US-Iran negotiating context rather than purely military operational decisions. Consequently, this oil market disruption has compounded pre-existing pressures on global energy supply chains.

What Does International Maritime Law Actually Say About the Strait of Hormuz?

UNCLOS and the Right of Transit Passage

The legal framework governing international straits is set out primarily in Part III of the United Nations Convention on the Law of the Sea. Under UNCLOS, straits used for international navigation are subject to the right of transit passage, a regime that cannot be suspended by coastal states under any circumstances, including armed conflict. Iran is a signatory to UNCLOS, making its unilateral redefinition of the strait's operational boundaries directly inconsistent with the treaty's provisions.

The IRGC's designation of a specific approved corridor as the only safe route for commercial vessels functions, in legal terms, as a blockade. Blockades of this kind are typically associated with formally declared states of war under the law of armed conflict, a status that creates its own set of international legal obligations and risks.

Where the IRGC's Claims Conflict with Established Norms

Three specific conflicts with international maritime law deserve particular attention:

- Territorial sea limits: Iran's lawful territorial waters extend 12 nautical miles from its coastline. The new operational zone extends well beyond this boundary into the Exclusive Economic Zones of the UAE and Oman

- High seas freedoms: Portions of the expanded zone fall within international waters where no single state holds enforcement jurisdiction under customary international law

- UAE sovereignty implications: Siri Island lies approximately 70 kilometres from the UAE emirate of Umm al-Quwain. The IRGC's westward boundary claim encroaches directly on waters the UAE considers within its own maritime jurisdiction

Legal Warning: The IRGC's operational zone declaration carries no enforceable legal basis under international maritime law. However, the practical enforcement capacity of the IRGC, including mine-laying, vessel boarding, and armed patrol operations, means the de facto risk environment for commercial shipping has materially deteriorated regardless of legal standing. The gap between legal right and operational reality is where the real danger lies.

What Is the Real Strategic Geography of the Expanded Zone?

Mapping the Complete Crescent: Key Locations and Their Significance

The geography of the expanded zone is not arbitrary. Each anchor point was chosen for specific strategic reasons that reveal the scope of Iranian ambitions in the region.

- Jask (Eastern Anchor): Located on Iran's southern coast east of the strait, Jask has been progressively developed as a naval base and alternative oil export terminal. Its inclusion in the eastern boundary of the new zone signals Iran's intent to assert control over the Gulf of Oman approaches, not merely the strait itself

- Siri Island (Western Anchor): An Iranian-administered island in the Mideast Gulf with established oil infrastructure, Siri's designation as the western boundary extends IRGC claims to within striking distance of UAE territorial waters

- Qeshm Island: Iran's largest island, positioned at the mouth of the strait, previously served as the western boundary marker in the 4 May maps. The subsequent expansion beyond Qeshm demonstrates the deliberate, progressive nature of the boundary-widening strategy

- Fujairah (UAE): The UAE's critical non-Hormuz export hub, through which the Abu Dhabi Crude Oil Pipeline terminus operates, now falls within the implied surveillance footprint of the expanded eastern arc

- Umm al-Quwain (UAE): The UAE emirate geographically closest to Siri Island, now within the proximity of declared IRGC operational assertions

Why Blocking Fujairah Matters for Global Oil Markets

Fujairah represents the single most important physical infrastructure for bypassing the Strait of Hormuz. The Abu Dhabi Crude Oil Pipeline, which carries approximately 1.5 million barrels per day, was constructed precisely to route UAE crude exports to the Fujairah coast without requiring any transit through the strait. If the IRGC's expanded zone creates material operational risk for vessels approaching Fujairah through the Gulf of Oman, this bypass mechanism is effectively neutralised.

The strategic significance of this cannot be overstated. Fujairah was designed as the solution to a Hormuz closure scenario. Its inclusion within the IRGC's implied operational reach eliminates the insurance policy the Gulf's oil exporters spent billions of dollars constructing. In addition, current crude oil prices have already reflected elevated risk premiums in response to these developments.

How Much Global Energy Supply Is Now at Risk?

The Chokepoint's Systemic Importance to World Oil Markets

The numbers that define the Strait of Hormuz's role in global energy supply are not new, but they bear repeating in full:

- Approximately 21% of global petroleum liquids trade transited the Strait of Hormuz prior to the current conflict

- The strait handled an estimated 17 to 20 million barrels per day of crude oil, condensate, and refined products under normal operating conditions

- Qatar, the world's largest LNG exporter by volume, routes its LNG shipments through the strait, placing a substantial share of global gas supply within the IRGC's declared operational zone

- The expanded definition now places not just the strait corridor but the broader Gulf of Oman approach lanes under IRGC operational assertion

Energy Price Transmission: From Geopolitical Risk to Consumer Markets

| Supply Disruption Scenario | Estimated Price Impact | Affected Commodity |

|---|---|---|

| Partial strait closure (current baseline) | Significant upward pressure above $100/bl | Crude oil (Brent, WTI) |

| Fujairah bypass route disrupted | Additional premium on Middle East grades | UAE Murban, Saudi Arab Light |

| Qatar LNG flows interrupted | Spot LNG price spike in Asia and Europe | LNG (JKM, TTF) |

| Full operational zone enforcement | Extreme volatility across all energy benchmarks | All petroleum liquids, LNG |

Market Context: US consumers were paying an average of $4.45 per US gallon for regular grade gasoline as of the week ending 4 May 2026, according to the US Energy Information Administration. This figure approaches a four-year high and has created significant domestic political pressure for the Trump administration, which campaigned on pledges to cut fuel prices substantially. The administration has been actively exploring a suspension of the federal gasoline excise tax of 18.4 cents per US gallon, a measure that would cost approximately $39 billion per year according to the nonprofit Committee for a Responsible Federal Budget, and would exhaust the US Highway Trust Fund roughly 14 months ahead of schedule.

Furthermore, crude oil price volatility of this magnitude has historically transmitted into broader inflationary pressures well beyond the energy sector itself.

The next major ASX story will hit our subscribers first

How Are Global Powers Responding to the IRGC's Jurisdictional Expansion?

The US Strategic Posture: Counter-Blockade, Negotiation, and Domestic Pressure

The United States has responded to Iran's closure of the strait with a counter-blockade of its own on vessels travelling to and from Iranian ports, creating a dual-blockade dynamic in the world's most consequential waterway. The Trump administration has repeatedly asserted progress in ceasefire negotiations, while simultaneously describing the ceasefire in place since 8 April as being under significant strain.

Domestically, the political arithmetic has grown increasingly uncomfortable. President Trump, who built a substantial part of his electoral campaign on promises to reduce fuel prices, now presides over gasoline costs approaching four-year highs. The administration's response has included invoking a Korean War-era defence law in an attempt to boost domestic oil production and refining, extending waivers of domestic shipping requirements under the Jones Act, and publicly backing a congressional suspension of the federal gasoline tax. Bipartisan support for the tax holiday has emerged in both chambers, though critics note the fiscal consequences would be substantial.

The US Shale Sector's Cautious Response

The US oil industry's reaction to prices surging above $100 per barrel has been notably restrained compared to previous price cycles. While independent producer Diamondback Energy announced it was accelerating activity in the Permian Basin, citing the supply disruption environment as justification for growth, the US majors have largely held to plans established before the conflict began.

ExxonMobil confirmed it would continue on its previously established production trajectory in the Permian, targeting roughly 1.8 million barrels of oil equivalent per day. Chevron, which had already moderated Permian growth in favour of cash generation, indicated no immediate plans to accelerate. This collective caution reflects hard lessons absorbed during the 2022 price rally triggered by Russia's invasion of Ukraine. The US shale slowdown dynamic is further reinforced by industry consolidation and a diminished pool of private operators who historically led rapid response drilling.

Gulf State Reactions and Diplomatic Exposure

UAE and other Gulf Cooperation Council member states have characterised the IRGC's expanded zone as a violation of established maritime norms. The proximity of the new western boundary to UAE territorial waters creates a direct sovereignty dispute that places Gulf states in a structurally difficult diplomatic position, caught between the competing gravitational fields of Washington and Tehran. OPEC's market influence over production policy has consequently become an even more closely watched variable for energy traders globally.

What Are the Alternative Supply Routes and How Viable Are They?

Existing Bypass Infrastructure: Capacity vs. Demand Gap

The global energy system's backup architecture for a Hormuz disruption is substantial in absolute terms but wholly inadequate relative to the volume that normally transits the strait:

- Abu Dhabi Crude Oil Pipeline (ADCOP): Approximately 1.5 million b/d capacity to Fujairah, now at elevated risk from the expanded IRGC zone's coverage of Gulf of Oman approaches

- Saudi East-West Pipeline (Petroline): Approximately 5 million b/d capacity to Red Sea terminals at Yanbu, viable but already operating at elevated utilisation rates

- Iraq-Turkey Kirkuk-Ceyhan Pipeline: Reduced capacity due to ongoing maintenance and political complications, with limited near-term surge potential

- Combined bypass capacity: Estimated at roughly 6 to 7 million b/d at maximum throughput

Supply Gap Reality: Even with all available bypass infrastructure operating at absolute maximum capacity, the global market faces a structural shortfall of 10 to 14 million barrels per day if the Hormuz route remains effectively closed. No combination of alternative pipelines, strategic petroleum reserve releases, or production acceleration from non-Gulf producers can bridge that gap in any timeframe that avoids severe economic disruption.

The Latin American Opportunity: Real but Insufficient

Brazil, Guyana, and Argentina have collectively moved to position themselves as strategic beneficiaries of the Hormuz disruption, and their pitch is genuinely compelling. Together, the three nations produce approximately 6 million barrels per day, including a record 4.2 million b/d from Brazil in March 2026, more than 900,000 b/d from Guyana, and close to 900,000 b/d from Argentina.

A key selling point that Brazilian oil regulator officials have emphasised publicly is that Brazilian crude exports do not transit any strait, eliminating the chokepoint risk that now defines Middle Eastern supply. However, the investment environment constrains how rapidly this alternative supply can scale. Two thirds of global energy investment in 2026 is forecast by the International Energy Agency to flow toward renewable energy, leaving upstream oil investment in a structurally competitive position for shrinking capital.

Oil services provider Baker Hughes has projected a low single-digit percentage decline in global upstream investment for the year. Latin American producers, despite high-quality acreage, are competing for a contracting share of available capital. Brazil's offshore pre-salt formations remain technically demanding and capital-intensive; Guyana remains dependent on a single ExxonMobil-led consortium at its producing Stabroek block; and Argentina's Vaca Muerta formation, while vast, requires significant infrastructure to unlock at scale.

What Does the IRGC's Designated Corridor Doctrine Mean for Shipping Operators?

Practical Implications for Commercial Vessel Operators

The IRGC's creation of a formally approved transit corridor, outside of which vessels are considered to be operating at their own risk, has fundamentally restructured the commercial calculus for every operator moving cargo through the Gulf region. Marine war risk insurance premiums have risen substantially. The practical effect of the corridor system is to create a two-tier shipping market: vessels from nations the IRGC considers friendly can operate within approved lanes, while Western-affiliated vessels face ongoing exclusion or interdiction risk.

Step-by-Step Risk Assessment Framework for Shipping Operators

-

Identify vessel flag state and ownership chain. Vessels with US, Israeli, or allied-nation connections face the highest interdiction risk under current IRGC policy. Flag state alone is insufficient; ultimate beneficial ownership and charterer relationships are equally scrutinised.

-

Map the new operational zone boundaries. The expanded crescent from Jask to Siri Island must be treated as a potential enforcement zone. Detailed analysis of the redefined boundaries confirms that the 12 May declaration extends well beyond the 4 May maps, and further expansions cannot be ruled out.

-

Assess Fujairah routing viability. Gulf of Oman transits bound for Fujairah now fall within the IRGC's declared operational area. The bypass route previously considered safe from Hormuz risk now carries its own elevated risk profile.

-

Evaluate alternative routing costs. Cape of Good Hope diversions add approximately 10 to 15 transit days and materially increase fuel and charter costs. These economics are now a standard component of Middle East routing decisions.

-

Review war risk insurance coverage thoroughly. Standard Protection and Indemnity club coverage may not extend to incidents within declared conflict zones. War risk endorsements and additional hull cover are essential, not optional.

-

Monitor IRGC communications in real time. The sequential nature of boundary expansions from 4 May to 12 May indicates the operational zone definition remains dynamic. Static routing decisions made on the basis of earlier announcements may be outdated within days.

What Comes Next: Scenario Analysis for the Strait of Hormuz Crisis

Scenario 1: Negotiated De-escalation

A breakthrough in US-Iran talks produces a ceasefire extension and partial reopening of the strait to commercial traffic. The IRGC's expanded zone declaration is quietly walked back or applied with minimal enforcement. Energy markets partially recover, though a persistent risk premium remains embedded in forward prices. This outcome is assessed as low probability in the near term, given the Trump administration's public characterisation of Iran's most recent negotiating offer as a piece of garbage and the stated view that the ceasefire is on massive life support.

Scenario 2: Frozen Conflict with Selective Enforcement (Base Case)

The IRGC maintains its expanded operational zone declaration but applies enforcement selectively based on vessel nationality and cargo destination. A two-tier shipping market solidifies, with friendly-nation vessels operating within IRGC-approved corridors while Western-affiliated traffic remains excluded. Energy prices stay elevated, bypass infrastructure operates near capacity, and non-Gulf producers accelerate investment pitches. This represents the most probable near-term path based on current trajectory.

Scenario 3: Full Operational Zone Enforcement

The IRGC begins actively enforcing its expanded zone across the Gulf of Oman approaches and Fujairah-bound traffic. The UAE bypass route is effectively neutralised. Global oil prices spike sharply beyond current elevated levels, LNG markets in Asia and Europe face acute supply stress, and the probability of direct coalition military responses increases substantially. This is a tail risk scenario, but the sequential nature of IRGC boundary expansions means it cannot be dismissed as implausible.

Strategic Assessment: The most consequential feature of the current situation is not any single military action or diplomatic statement. It is the systematic expansion of the zone within which uncertainty operates. Every extension of the IRGC's declared operational area increases the geographic footprint of risk, reduces the effectiveness of bypass alternatives, and compresses the decision space available to both commercial operators and policymakers. The crescent, as Iranian officials have described it, is still being drawn. The reality that the IRGC widens Strait of Hormuz operational area in deliberate, sequential increments is itself the defining strategic signal of this crisis.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Forward-looking scenarios and price impact assessments involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Energy market conditions and geopolitical developments are subject to rapid change. Readers should consult qualified professional advisers before making decisions based on the information contained herein.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Energy Disruptions?

When geopolitical crises reshape commodity markets at speed, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries — instantly translating complex market shifts into actionable investment opportunities for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the market.