June 4, 2026

The Architecture of Global LNG Vulnerability

Energy security planners have long understood that the global liquefied natural gas trade is not a distributed, resilient network. It is a system with a single catastrophic failure point, and that point is a narrow corridor of water connecting the Persian Gulf to the world.

The Strait of Hormuz, at its narrowest just 21 miles wide, functions as a pressure valve for the entire global energy economy. When it operates freely, few outside the industry pay attention. When it closes, the consequences of a Strait of Hormuz closure LNG supply disruption reach every import terminal on Earth, every industrial gas consumer in Asia, and every household heating bill in northwest Europe.

Understanding how that cascade actually unfolds requires moving past the headline numbers and examining the structural mechanics of why this particular waterway cannot be worked around, substituted, or insured against in any conventional sense.

When big ASX news breaks, our subscribers know first

The Strategic Chokepoint That Controls One-Fifth of World LNG Trade

Geographic and Physical Constraints That Make Hormuz Irreplaceable

The strait sits between the Omani coastline to the south and the Iranian shoreline to the north. Its navigable shipping lanes are narrower still, constrained by shallow water, territorial boundaries, and the physical dimensions of modern LNG tankers, which require deep-draft channels to transit safely.

There is no pipeline network capable of moving LNG-equivalent volumes from the Persian Gulf to export terminals on alternative coastlines. LNG, unlike crude oil, cannot be redirected through overland infrastructure at scale. It must be liquefied at purpose-built coastal facilities, loaded onto specialist tankers, and shipped to regasification terminals. Every one of those coastal liquefaction facilities for Qatar, the UAE, and Iran sits inside the Persian Gulf, behind the strait.

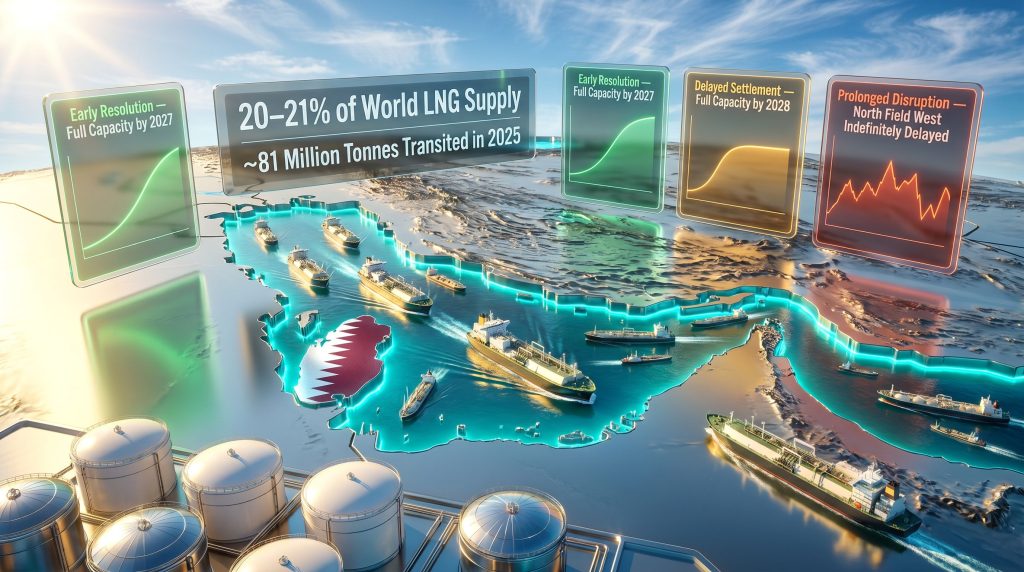

Approximately 81 million tonnes of LNG transited the Strait of Hormuz in 2025 alone, according to analysis from Wood Mackenzie. That volume represents 20 to 21 percent of total global LNG supply, making the strait the single largest concentration of LNG supply risk anywhere in the world. Furthermore, the global LNG supply outlook for 2025 reinforces just how structurally dependent international markets have become on this single corridor.

Qatar's Structural Dependency and the North Field West Question

Qatar's exposure to Hormuz risk is not incidental. It is total. More than 90 percent of Qatari LNG exports must transit the strait to reach global markets, and Qatar is the world's largest or second-largest LNG exporter depending on the year. There is no alternative routing for Qatari cargoes at meaningful scale.

This dependency extends directly to Qatar's long-term expansion ambitions. The North Field West development, one of the most significant LNG capacity additions currently in planning, is structurally contingent on strait stability. A prolonged closure does not merely disrupt existing export volumes. It defers the capital investment decisions and infrastructure timelines for the next generation of Qatari supply, reshaping the global LNG balance well into the 2030s.

The UAE and Iran round out the upstream exposure map. Iran presents a particular geopolitical paradox in any conflict scenario: as both a potential belligerent and an LNG-adjacent gas producer, Iran's position simultaneously creates the closure risk and suffers commercially from it.

What Happens to Global LNG Markets When the Strait Closes?

The Immediate Arithmetic of Supply Removal

The scale of displacement triggered by a Hormuz closure is, by energy market standards, almost without precedent in speed. According to Lloyd's List, LNG supply disruption would be immediate and immense — a characterisation grounded in the structural absence of any buffer capacity in today's LNG market.

Unlike crude oil, where strategic petroleum reserves in major consuming nations provide a partial short-term cushion, LNG has no equivalent emergency release mechanism. Floating storage volumes are limited. Spare liquefaction capacity outside the Persian Gulf is minimal. The removal of more than 70 million tonnes per annum (Mtpa) of supply from global balances creates a shock with no obvious absorber.

For context, the 2022 disruption to Russian pipeline gas flows into Europe, which drove European gas prices to historic highs and triggered an emergency global rerouting of LNG cargoes, involved roughly comparable volumes. That disruption unfolded over months and was partially anticipated by markets. A Hormuz closure operates instantaneously, across all geographies simultaneously, and without the lead time that allows procurement teams to partially hedge.

The absence of any LNG strategic reserve mechanism, equivalent to the oil sector's strategic petroleum reserve system, means that supply shocks translate directly and immediately into price discovery on spot markets. There is no government-held LNG stockpile that can be released to stabilise benchmarks.

Three Recovery Scenarios Modelled Through to 2045

Wood Mackenzie has constructed three distinct scenario frameworks that trace the trajectory of global LNG markets from the point of closure through to 2045, each defined by the reopening timeline and the pace of Middle Eastern infrastructure recovery.

| Scenario | Reopening Timeline | Middle East Capacity Recovery | Key Market Implication |

|---|---|---|---|

| Early Resolution | June 2026 | Full capacity by 2027 | Price spike contained; markets rebalance relatively quickly |

| Delayed Settlement | September 2026 | Full capacity by 2028 | Extended tightness; Asian spot premiums persist through 2027 |

| Prolonged Disruption | Indefinite / sporadic flare-ups | Major projects including North Field West indefinitely delayed | Structural supply deficit; accelerated non-Middle East FID activity |

Each scenario produces a materially different trajectory for European gas prices and Asian LNG benchmarks. Under early resolution, price normalisation is possible within twelve to eighteen months. Under delayed settlement, Asian spot premiums persist through 2027, creating sustained pressure on price-sensitive importers. Under extended disruption, the market undergoes structural repricing, with new price floors emerging that reshape both demand behaviour and long-term contract economics.

One less widely discussed dynamic within the extended disruption scenario involves US Henry Hub pricing. Lower oil prices associated with prolonged Persian Gulf conflict reduce the commercial incentive to produce associated gas from tight oil formations. This constrains the availability of low-cost US gas that would otherwise flow into export facilities, adding an indirect upward pressure to US domestic gas prices. Consequently, the US natural gas price forecast becomes considerably more complex under any sustained Hormuz disruption scenario.

Which Regions Face the Greatest LNG Supply Disruption Risk?

Asia: The Most Structurally Exposed Import Region

Asia's exposure to a Strait of Hormuz closure LNG supply disruption is the highest of any import region, measured both by volume dependency and by the limited flexibility available to procurement teams operating on short notice.

Approximately 25 percent of total Asian LNG deliveries transit the strait, but within that aggregate figure the distribution is uneven. China carries a particularly concentrated exposure, with roughly 30 percent of Chinese LNG deliveries passing through Hormuz. Japan and South Korea, as long-term buyers of contracted Qatari volumes, face not only supply disruption but the complex legal and commercial question of force majeure invocation under their long-term supply agreements.

The force majeure dimension is worth examining carefully. Most long-term LNG supply contracts contain provisions for events beyond a seller's control, including war and physical infrastructure destruction. A confirmed Hormuz closure would likely trigger these provisions, meaning buyers cannot compel delivery and must simultaneously source replacement volumes in an already depleted spot market. The combination of contracted volume loss and spot market competition creates a procurement crisis with no clean resolution.

India occupies a distinct dual position. As both a significant LNG importer and a nation geographically proximate to the disruption zone, India faces simultaneous supply and cost pressures while also absorbing secondary economic effects from elevated energy prices across its industrial base.

Europe: The Secondary Shock and the Price-Setting Role

Europe's vulnerability to a Hormuz closure is structurally different from Asia's but not smaller. Since the 2022 Russian pipeline gas disruption, European buyers have systematically rebuilt their LNG import dependency on Qatari volumes as a replacement supply source. A Hormuz closure effectively reverses that diversification gain.

More critically, Europe's position as the market of last resort for global LNG cargoes means that European gas benchmarks become the global price-setter during supply stress. When Asian buyers compete for Atlantic Basin and US cargoes to replace lost Qatari supply, European buyers must either outbid them or draw down storage at an accelerated rate. Both pathways drive European prices higher, an outcome well reflected in broader natural gas price trends already emerging across 2025.

Storage drawdown dynamics add a further complication. European gas storage levels, rebuilt carefully since 2022 through deliberate procurement and LNG import growth, would face accelerated depletion under a sustained Hormuz closure scenario. The buffer that European energy policymakers have worked to establish since the Russian pipeline crisis would erode, potentially returning the continent to the acute storage anxiety seen in late 2022.

Emerging Market Importers: The Disproportionate Price Burden

South and Southeast Asian importers including Bangladesh, Pakistan, and Thailand represent perhaps the most vulnerable category of LNG buyer under a Hormuz closure scenario, yet they receive the least attention in mainstream energy security discussions.

These nations typically lack the long-term contract portfolio depth that Japanese, Korean, or European buyers maintain. A higher proportion of their supply is sourced on the spot market or through shorter-duration agreements, meaning spot price escalation translates directly into landed fuel costs with limited hedging protection.

At elevated spot LNG prices, demand destruction becomes a rational commercial response. Industrial facilities reduce operating rates. Power sector operators switch to alternative fuels where available, including coal, heavy fuel oil, or diesel. Where switching options are limited, mandatory rationing and load shedding follow. The economic consequences of Hormuz-driven LNG price spikes therefore fall disproportionately on nations least equipped to absorb them.

How Does Non-Middle East LNG Supply Respond to a Hormuz Closure?

The US LNG Pipeline: What It Can and Cannot Do

The scale of LNG capacity currently under construction outside the Persian Gulf is genuinely substantial. More than 150 Mtpa of LNG capacity is currently being built, with the United States representing the largest single contributor to that pipeline. An additional 30 Mtpa is expected to reach Final Investment Decision by late 2027, potentially triggering a further wave of project commitments if geopolitical risk in the Persian Gulf improves project economics for non-Middle East developers.

The critical constraint, however, is timing. LNG liquefaction facility construction requires between four and six years from final investment decision to first cargo. No capacity currently at FID stage, and no capacity that reaches FID in the next twelve months, can contribute meaningfully to a supply balance crisis unfolding over a twelve to twenty-four month horizon. The infrastructure simply cannot be built fast enough.

What a prolonged Hormuz disruption does achieve on the supply side is a structural improvement in the economics of non-Middle East project development. Projects that were marginal at pre-disruption LNG prices become commercially viable at the elevated price levels sustained by a closure. This dynamic could accelerate FID timelines for US Gulf Coast projects, Australian expansions, and emerging suppliers across Africa and South America.

Alternative Corridors and Their Practical Ceiling

Australia's existing LNG export capacity positions it as a natural swing supplier to Pacific Basin buyers seeking replacement cargoes, but Australia's spare capacity is limited and its production is already committed through long-term contract books. Incremental Australian volumes are unlikely to meaningfully offset Persian Gulf losses at volume.

African LNG development ambitions, particularly in Mozambique, Tanzania, and Senegal, remain constrained by infrastructure readiness. Mozambique's offshore LNG development has faced prolonged delays due to security challenges. Tanzania's LNG export ambitions remain in early development. These projects add future supply optionality but cannot respond to an immediate disruption.

Argentina's emerging LNG export potential through partnerships involving Eni, YPF, and XRG represents a medium-term supply addition, with project timelines extending into the late 2020s and early 2030s. Canada's LNG Canada project, nearing initial production, offers a Pacific Basin-oriented supply source that could partially serve Asian buyers displaced from Qatari supply over a multi-year disruption horizon.

The structural gap between what non-Middle East supply can theoretically provide and what is physically available within the critical twelve to twenty-four month window is the defining feature of a Hormuz closure supply crisis. The supply pipeline exists. The construction timeline does not compress.

What Happens to LNG Prices During and After a Hormuz Closure?

Spot Market Mechanics Under Acute Scarcity

LNG spot price escalation under a Hormuz closure follows a compounding mechanism. The initial removal of supply volume triggers direct cargo scarcity. Buyer competition for available spot cargoes then drives benchmark prices higher. Vessel rerouting increases sailing distances and reduces the effective tanker fleet capacity available to the market, pushing charter rates and freight costs higher. Those freight costs pass through into landed cargo prices at regasification terminals, amplifying delivered cost escalation beyond what spot benchmark movements alone would suggest.

The Japan-Korea Marker (JKM), the primary Asian LNG spot benchmark, would likely experience the sharpest initial price movements given Asia's concentrated exposure and competitive buyer base. European benchmarks, particularly the Title Transfer Facility (TTF) in the Netherlands, would follow as European buyers competed for the same Atlantic Basin and US cargoes. In addition, analysis from Timera Energy identifies five key market impacts that compound across both benchmarks simultaneously.

The 2022 European energy crisis provides the closest historical reference point for this dynamic. European gas benchmarks reached levels multiple times their historic averages as Europe and Asia competed simultaneously for global LNG cargoes. A Strait of Hormuz closure LNG supply disruption would replicate that competitive dynamic but with a larger volume displacement and a more sudden onset.

The Post-Reopening Price Paradox

One of the less intuitive features of LNG market recoveries after acute supply disruptions is that prices do not normalise as quickly as physical supply resumption might suggest. Even after the strait reopens, several dynamics sustain elevated price conditions.

Storage restocking demand creates a persistent additional layer of buying. Buyers who drew down storage during the closure period compete to rebuild inventory levels simultaneously, maintaining demand above normal operating levels precisely when supply is in the early stages of recovery.

Deferred cargo delivery backlogs create scheduling congestion at regasification terminals. Infrastructure restart timelines for any facilities that sustained damage during a conflict add further delays to supply recovery. Shipping constraints, including vessel positioning and cargo scheduling disruptions accumulated during the closure, take weeks or months to fully unwind.

Perhaps most durably, a geopolitical risk premium becomes embedded in forward curves and long-term contract pricing. Markets reprice the probability of future Hormuz disruptions upward following any confirmed closure, and that repricing does not fully reverse when the physical disruption ends. Energy markets, particularly gas markets, carry geopolitical risk premiums for extended periods after traumatic supply events.

The next major ASX story will hit our subscribers first

How Are Governments and Energy Buyers Responding to Hormuz Supply Risk?

Structural Diversification Already Underway

Import nations with the most concentrated Hormuz exposure have been accelerating long-term supply agreements with non-Middle East producers since well before the current disruption. The pattern reflects a strategic reassessment of lowest-cost sourcing in favour of risk-adjusted sourcing, a shift that prioritises supply reliability and geographic diversification over price minimisation.

Investment in floating storage and regasification units (FSRUs) represents a parallel strand of this diversification strategy. FSRUs offer import nations flexibility that fixed onshore terminals cannot provide, including the ability to reposition receiving capacity, contract with multiple suppliers on shorter timelines, and respond more dynamically to market conditions. Nations with limited long-term contract coverage and high price sensitivity have been among the most active FSRU adopters.

The Demand Destruction Threshold and Long-Term Gas Dependency

Sustained LNG price spikes above specific thresholds trigger permanent demand responses in some market segments. Industrial gas consumers facing extended periods of uncompetitive energy costs accelerate fuel switching to electrification, process redesign, or facility relocation. These demand losses do not fully return when gas prices eventually normalise, creating a lasting reduction in the addressable market for LNG.

At the macro level, prolonged LNG price volatility attributable to Hormuz risk creates a powerful commercial argument for accelerating electrification and renewable energy deployment in heavily exposed import nations. Nations that have experienced acute energy insecurity driven by LNG supply disruptions invest more aggressively in domestic energy resources, including solar, wind, and storage, specifically to reduce their future exposure.

The long-term demand uncertainty created by this dynamic adds a counterbalancing risk to the FID acceleration thesis for non-Middle East LNG developers. Projects financed on assumptions about Asian or European LNG demand levels through the 2030s and 2040s face genuine uncertainty about whether demand destruction effects from current price volatility will reshape those assumptions downward.

Investment Implications for Non-Middle East LNG Development

From an investment perspective, the commercial landscape for non-Middle East LNG developers has materially improved under a sustained Hormuz disruption. Project economics that appeared marginal at pre-disruption LNG prices become viable at elevated price levels. Buyers that were unwilling to commit to long-term supply agreements at previously requested prices become motivated counterparties when the alternative is exposure to extreme spot market volatility.

This commercial tailwind benefits developers across the US, Australia, Canada, and Africa. However, the trade war impact on oil and associated geopolitical pressures have already elevated risk premiums across the energy complex, meaning Middle East project financing faces compounding headwinds. Wood Mackenzie's analysis confirms that heavily exposed import nations are already exploring structural changes to actively diversify away from gas dependency. That shift, if sustained, represents the most significant long-term demand risk facing any LNG developer, whether in the Middle East or elsewhere.

Frequently Asked Questions: Strait of Hormuz LNG Supply Disruption

How Much LNG Passes Through the Strait of Hormuz Each Year?

Approximately 81 million tonnes of LNG transited the Strait of Hormuz in 2025, representing around 20 to 21 percent of total global LNG supply, according to Wood Mackenzie analysis.

Which Country Is Most Exposed to a Hormuz LNG Disruption?

Qatar faces the greatest single-country exposure, with more than 90 percent of its LNG exports routed through the strait. Among import nations, China (approximately 30 percent of deliveries) and broader Asia (approximately 25 percent of regional deliveries) carry the highest demand-side risk.

Could the US Replace Lost Qatari LNG Volumes?

Not in the short term. While more than 150 Mtpa of US LNG capacity is under construction, construction lead times of four to six years mean new supply cannot reach markets within the twelve to twenty-four month window most critical to managing an acute disruption.

How Long Would It Take for LNG Markets to Recover After the Strait Reopens?

Recovery timelines depend on infrastructure damage, storage drawdown levels, and cargo backlog volumes. Even under optimistic scenarios, full price normalisation would lag physical reopening by several months as restocking demand keeps balances tight.

What Happened to European Gas Prices During Previous LNG Supply Shocks?

The 2022 Russian pipeline gas disruption provides the closest precedent. European gas benchmarks surged to historic highs as the continent competed with Asian buyers for flexible LNG cargoes, a dynamic that would likely repeat under a Hormuz closure scenario.

Would a Hormuz Closure Affect Oil Prices as Well as LNG?

Yes. The strait is also a critical corridor for crude oil exports. A closure would simultaneously tighten oil markets, with cascading effects on energy-intensive industries, transportation costs, and associated gas production economics in the United States. Indeed, oil price movements in recent months have already demonstrated how sensitive energy benchmarks are to Persian Gulf geopolitical developments.

The Long-Term Structural Implications for Global LNG Trade Architecture

Accelerated Diversification of LNG Supply Chains

A Hormuz closure of sufficient duration would permanently alter the way LNG buyers construct their supply portfolios. The shift from lowest-cost sourcing to risk-adjusted sourcing, already underway among more strategically sophisticated buyers, would accelerate across the full spectrum of the import community.

Australia, the United States, and Canada emerge as the primary beneficiaries of this structural reorientation. Their geographic positioning outside the Persian Gulf, combined with established or developing liquefaction infrastructure, makes them natural anchors for buyers seeking to reduce Hormuz concentration risk in their supply books.

The Redefinition of Energy Security in LNG-Dependent Economies

Japan, South Korea, and China are likely to reassess their strategic LNG reserve policies in any post-disruption environment. The structural absence of an emergency LNG release mechanism, which the current crisis exposes so starkly, creates a strong policy rationale for developing floating storage buffers, diversified FSRU infrastructure, and strategic supply agreements with geographically distributed counterparties.

Whether a prolonged disruption accelerates the energy transition timeline in heavily exposed import nations depends on the duration and severity of price impacts. Nations that experience sustained periods of unaffordable LNG prices have demonstrated historically that they invest more heavily in alternatives. The current disruption, if extended, could consequently function as the commercial catalyst that demand-side energy transition programmes in Asia have lacked.

Investment Implications for Non-Middle East LNG Development

The FID acceleration thesis for non-Middle East LNG developers is real but not unconditional. Improved project economics driven by elevated LNG prices create a genuine commercial tailwind. But the long-term demand uncertainty generated by the same price volatility that makes projects attractive today represents the counterbalancing risk that developers and their financiers must model carefully.

Projects structured with sufficient flexibility to manage downside demand scenarios, including tolling agreements, portfolio diversification, and shorter initial contract terms, are better positioned to attract financing in this environment than those predicated on single-scenario demand assumptions extending to 2045.

The geopolitical risk premium applied to Middle East LNG projects would reprice upward permanently following a confirmed Strait of Hormuz closure LNG supply disruption, even after physical supply resumes. This repricing benefits non-Middle East developers not merely through improved near-term price levels but through the structural shift in how institutional investors and project financiers assess the relative risk profiles of competing LNG supply sources globally.

Readers seeking additional context on global LNG market dynamics and geopolitical supply risk can explore related industry analysis published by Petroleum Australia at petroleumaustralia.com.au, which covers ongoing developments across the global gas sector.

This article contains forward-looking analysis and scenario modelling based on third-party research. It does not constitute financial or investment advice. Readers should conduct their own independent analysis before making any investment or procurement decisions.

Want To Position Ahead Of The Next Major Energy-Driven ASX Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across more than 30 commodities — including those tied to the energy transition materials being reshaped by global LNG supply dynamics. Explore historic discoveries and their market returns, then begin your 14-day free trial to ensure you're positioned before the broader market catches on.