July 15, 2026

The Geography of Energy Vulnerability: Why Every Barrel Passes Through a Needle's Eye

Long before the current confrontation between Washington and Tehran reached its boiling point, energy economists had identified a structural fragility embedded into the global oil and gas system that no amount of diplomatic goodwill could fully resolve. The world's most consequential energy infrastructure is not a pipeline, a refinery, or a storage terminal. It is a narrow strip of water approximately 33 kilometres wide at its tightest point, squeezed between the coastlines of Iran and Oman, through which roughly one-fifth of the entire planet's daily oil and liquefied natural gas supply flows during peacetime conditions.

The Strait of Hormuz is not merely a transit route. It is the economic circulatory system of the Gulf region, without which the export economies of Saudi Arabia, the United Arab Emirates, Iraq, Kuwait, and Qatar effectively cease to function. These nations collectively account for a staggering share of global proven oil reserves, yet their ability to monetise those reserves depends almost entirely on the openness of a single 33-kilometre maritime corridor.

When Iran threatens to halt Middle East energy exports, the world does not simply face a political standoff. It confronts a scenario in which the physical architecture of global energy supply becomes a weapon. Understanding current oil price trends is therefore essential context for any serious assessment of what this confrontation means for global markets.

When big ASX news breaks, our subscribers know first

How the Current Crisis Unfolded: A Conflict Timeline Built on Compounding Triggers

The Opening Strike and the First Market Shock

The sequence of events that produced today's crisis did not begin with a single miscalculation. It began with a military decision. On February 28, 2026, the United States and Israel launched coordinated military operations targeting Iranian territory. Tehran's response was immediate and economically catastrophic: Iran effectively shut down transit through the Strait of Hormuz by attacking and threatening any vessel attempting passage.

The market reaction was swift and severe. Oil prices surged alongside fertiliser costs and broader commodity indices, as traders priced in the possibility that up to 140 million barrels of crude and gas equivalent could be removed from global circulation in a sustained closure scenario. Qatar, home to the Ras Laffan complex widely regarded as the world's largest LNG processing facility, declared force majeure on gas exports following drone strikes on the installation. The declaration triggered contractual disruption clauses across dozens of long-term supply agreements, sending shockwaves through Asian energy markets that depend heavily on Qatari LNG.

The Blockade-Deal-Blockade Cycle

What followed was a pattern that would repeat itself with increasing instability:

- Mid-April 2026: The U.S. military imposed an initial naval blockade on Iranian ports, escalating economic pressure on Tehran.

- Mid-June 2026: The blockade was lifted one day after both parties signed an interim agreement establishing a 60-day negotiation window covering Iran's nuclear programme and the long-term governance of strait access.

- July 14-15, 2026: The blockade was reimposed after talks stalled and Iranian attacks on commercial vessels using a U.S.-supervised alternative route near Oman intensified, triggering the most recent and most dangerous phase of the conflict.

This cycle reveals a critical structural problem with the interim deal: it addressed the immediate symptom of strait closure without resolving the underlying dispute over who has the legal authority to govern passage through the waterway. Iran maintains it retains the sovereign right to regulate traffic and potentially impose fees. The United States formally rejects this position. Furthermore, without resolving this foundational disagreement, each ceasefire carries within it the seeds of its own collapse.

Iran's "All or Nothing" Energy Ultimatum and What It Actually Means

The IRGC Threat: Targeting the Entire Gulf Export System

The most alarming development in the current phase of the conflict is not the scale of the military exchanges. It is the nature of Iran's economic threat. The Islamic Revolutionary Guard Corps issued a declaration in July 2026 stating that energy exports from the entire region would flow for all parties or for none at all. The broader oil market impacts of such a posture are difficult to overstate.

This is not a threat confined to Iran's own oil exports. It explicitly extends to shipments originating from Saudi Arabia, the UAE, Iraq, and Kuwait, nations that are not parties to the direct military confrontation but whose export infrastructure passes through or near Iranian-controlled waters. IRGC spokesperson Ali Mohammad Naini made clear that Iran considers itself the sole arbiter of when and how the conflict ends, and that any modification of blockade conditions is contingent on the complete cessation of foreign military operations against Iranian territory.

This represents a fundamental shift in Iran's strategic posture, from defensive deterrence to offensive economic warfare targeting the Gulf export system as a collective entity.

The Second Front: Bab el-Mandeb and the Dual-Chokepoint Scenario

Intelligence assessments circulating among regional analysts suggest Iran may seek to activate its Houthi allies in Yemen to simultaneously close the Bab el-Mandeb Strait, the narrow maritime gateway connecting the Red Sea to the Gulf of Aden. This secondary chokepoint, already destabilised by years of Houthi attacks on commercial shipping, handles a significant portion of global seaborne trade.

A simultaneous closure of both the Strait of Hormuz and the Bab el-Mandeb would sever two of the world's four major maritime oil corridors at the same time. Analysts have projected Brent crude could spike toward $200 per barrel under this scenario, a level that would trigger demand destruction, emergency strategic reserve releases, and potential recession across import-dependent economies. Qatar has already warned that a full-scale war in the region could halt Gulf energy exports within weeks, further underlining the severity of this dual-chokepoint risk.

The Military Situation: Forces, Strikes, and the Escalation Calculus

U.S. Force Posture in the Arabian Sea

The scale of the American military presence in the region reflects the seriousness with which Washington is treating the threat to free navigation:

| Asset Type | Current Status |

|---|---|

| U.S. Warships in Arabian Sea | At least 19 vessels |

| Aircraft Carriers | 2 operational |

| Amphibious Assault Ships | 1 (carrying 1,000+ Marines) |

| Military Aircraft (Regional) | Hundreds across the Middle East |

| Duration of Reimposition Strike Wave | 7+ hours, dozens of targets struck |

U.S. Central Command confirmed strikes on multiple locations inside Iran on July 15, 2026. Iranian state media reported explosions in Bushehr, Ahvaz, and Bandar Abbas, three strategically significant locations encompassing coastal energy infrastructure and southern port facilities.

The Cascading Regional Impact

The conflict has long since ceased to be a bilateral confrontation. Its effects are now cascading across the broader Gulf region:

- Bahrain and Kuwait issued missile alert warnings as Iranian strikes became a near-daily occurrence throughout mid-July 2026.

- Jordan intercepted and destroyed three Iranian missiles in a single engagement, underscoring the geographic spread of the threat.

- Kuwait reported four naval personnel wounded and a facility set ablaze following a separate Iranian strike on its maritime assets.

- The attacks on Gulf Arab states hosting U.S. forces raise the uncomfortable question of whether those states are beginning to conduct retaliatory operations of their own outside public acknowledgement.

Military analysts note that any attempt to reopen the strait by force would require an operational footprint far larger than what currently exists, potentially encompassing tens of thousands of ground troops alongside the existing naval and air assets.

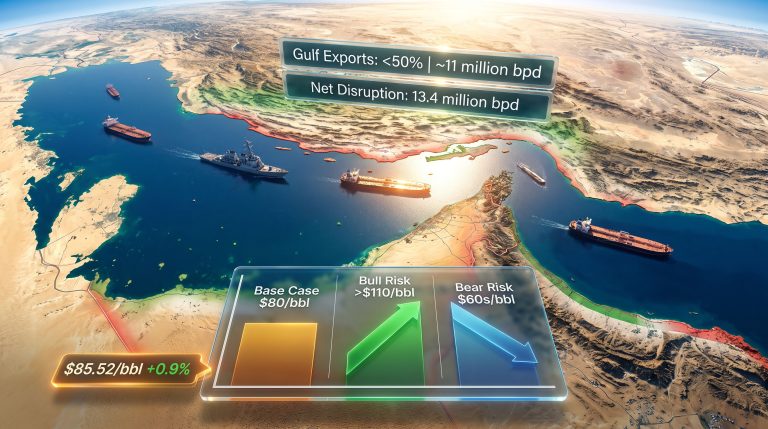

Oil Market Dynamics: What Brent Crude Is Telling Investors

Price Volatility Across the Conflict Cycle

The oil market's response to the crisis has been significant but, crucially, has not yet fully priced in worst-case scenarios. This divergence between market pricing and geopolitical risk represents one of the most important dynamics for energy investors to understand. The intersection of oil and geopolitics has rarely been more consequential than it is at this moment.

| Event | Brent Crude Price |

|---|---|

| Initial strait closure (Feb-Mar 2026) | Surged toward $120/barrel |

| Peak conflict pricing | Nearly $120/barrel |

| July 15, 2026 (brief intraday spike) | Topped $87/barrel |

| Post-Trump fee reversal announcement | Dipped to $78/barrel |

| Analyst projection (prolonged blockade) | $150/barrel |

| Dual-chokepoint scenario projection | $200/barrel |

The gap between the current trading range and analyst projections for sustained disruption scenarios reflects a market pricing in a meaningful probability of de-escalation, rather than treating a full closure as the central case. This is a classic pattern in geopolitical risk pricing: markets consistently underestimate tail risks until they materialise, at which point repricing is sudden and violent.

The 1970s Arab oil embargo provides a sobering historical reference point. A sustained supply shock of similar magnitude triggered demand destruction, structural shifts in industrial supply chains, and inflationary spirals that persisted for years after the physical disruption ended.

Nations Facing the Greatest Exposure

The asymmetry of vulnerability across importing nations is a critical but underappreciated dimension of this crisis:

| Country | Gulf Energy Dependency | Primary Vulnerability |

|---|---|---|

| China | Very High | Manufacturing cost surge, refinery feedstock |

| India | High | Crude import disruption, refinery throughput |

| Japan | High | LNG supply security, limited domestic production |

| South Korea | High | Naphtha and LNG for petrochemical industry |

| Germany and EU | Moderate | LNG price exposure, energy transition cost acceleration |

Asian importers bear the most acute exposure. China alone is the largest buyer of Gulf crude globally, while Japan and South Korea operate petrochemical and industrial systems with limited ability to rapidly substitute supply sources. In addition, the LNG supply outlook for these nations has deteriorated sharply since the Ras Laffan force majeure declaration, creating sustained uncertainty across long-term contract markets.

The Transit Fee Proposal and Its Rapid Reversal

A Policy Departure That Lasted Hours

When President Trump announced the reimposition of the blockade alongside a proposal to levy a 20% fee on all vessels transiting the Strait of Hormuz, he was departing from decades of settled American policy. The U.S. has historically been the most vocal and forceful advocate for the principle that the strait must remain open to all nations without charge or restriction.

The fee proposal was withdrawn within hours. Gulf Arab leaders, described by Trump as the region's kings and emirs, communicated their preference for an alternative arrangement. Rather than transit charges, Gulf monarchs proposed directing large-scale investment commitments into the U.S. economy. Trump publicly endorsed this substitution, noting his own view that no party should be in a position to levy charges on strait passage.

Ambiguity persists over whether the investment pledges represent new financial commitments or a repackaging of announcements made during Trump's earlier visit to the region. The episode nonetheless exposed a genuine tension between Trump's instinct to use economic leverage as a strategic tool and the diplomatic architecture that sustains U.S. basing rights and military cooperation across Bahrain, Kuwait, and the UAE.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways for Global Energy Markets

Scenario 1: Negotiated Re-entry (Base Case)

Regional mediators broker a return to talks within the original 60-day framework. The strait reopens under monitored conditions and Brent crude stabilises in the $85-$95 per barrel range. LNG supply disruptions are partially offset through alternative routing via Australian and U.S. export terminals. However, OPEC's market influence will play a pivotal role in determining how quickly supply-side stabilisation can be achieved.

Scenario 2: Prolonged Strait Closure (Elevated Risk)

Talks collapse entirely. The blockade extends beyond 90 days, contracting global oil supply by up to 20%. Brent crude pushes toward $150 per barrel. The International Energy Agency activates coordinated strategic reserve releases. Asian economies implement emergency energy rationing protocols.

Scenario 3: Dual Chokepoint Activation (Tail Risk)

Iran activates Houthi assets to close the Bab el-Mandeb simultaneously with the Strait of Hormuz. Oil prices spike toward $200 per barrel. Shipping insurance markets freeze. LNG spot prices reach historic highs. Global recession probability increases materially as industrial production costs surge across import-dependent economies.

Frequently Asked Questions

What percentage of global oil supply passes through the Strait of Hormuz?

Under normal peacetime conditions, approximately 20% of the world's combined oil and LNG supply transits the Strait of Hormuz, making it the single most critical maritime energy corridor on Earth.

Has the strait been formally closed before during this conflict?

Iran formally declared the strait closed on March 4, 2026, following the launch of U.S. and Israeli military operations on February 28, 2026. The declaration triggered immediate commodity price surges and forced Qatar to invoke force majeure on LNG export contracts.

What does Iran's IRGC threat actually cover?

The IRGC's declaration extends beyond Iran's own oil exports. It explicitly targets energy shipments from Saudi Arabia, the UAE, Iraq, and Kuwait, framing the disruption as a collective punishment mechanism applied to the entire Gulf export system unless military operations against Iran cease. Iran threatens to halt Middle East energy exports as leverage in what it frames as a defensive response to foreign aggression.

Why was the 20% transit fee proposal abandoned?

The proposal was withdrawn after Gulf Arab leaders offered an alternative involving substantial investment commitments into the U.S. economy. The fee would have represented a fundamental break from longstanding American commitments to toll-free transit of international straits.

What is the Bab el-Mandeb and why does it amplify the risk?

The Bab el-Mandeb is the narrow maritime gateway between Yemen and Djibouti connecting the Red Sea to the Gulf of Aden. A simultaneous closure of this corridor alongside the Strait of Hormuz would sever two of the world's four major maritime oil transit routes. Consequently, analysts project oil prices could reach $200 per barrel under such a scenario.

Disclaimer: This article contains forward-looking scenario analysis and price projections sourced from publicly available analyst assessments. These projections are inherently speculative and subject to rapid change based on diplomatic developments, military actions, and market conditions. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and consult qualified advisors before making any investment decisions.

Want to Capitalise on Energy Market Volatility Before the Broader Market Moves?

When geopolitical shocks like the Strait of Hormuz crisis send commodity prices surging, timing is everything — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral and energy-related discoveries, ensuring subscribers can identify actionable opportunities the moment they emerge. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the next major market move.