June 30, 2026

Breaking Down Traditional Energy Market Logic

Global energy markets face an unprecedented crisis as fundamental economic theories that have governed oil trading for decades collapse under geopolitical pressure. The Strait of Hormuz oil market disruption reveals critical vulnerabilities in the global energy architecture that traditional assumption frameworks cannot address. Furthermore, the premise that market forces would ultimately prevail over political interference is being systematically dismantled.

For years, energy economists operated under the premise that price mechanisms could absorb virtually any supply disruption through demand adjustment and alternative sourcing. This theoretical framework assumed that higher prices would naturally incentivise increased production from alternative suppliers while simultaneously reducing consumption through economic substitution effects.

However, the current global energy landscape demonstrates the fatal flaw in this reasoning. When critical infrastructure becomes weaponised by geopolitical actors, traditional market mechanisms cease to function entirely. Price signals become irrelevant when physical chokepoints prevent the actual delivery of commodities, regardless of economic incentives.

When big ASX news breaks, our subscribers know first

Understanding the Scale of Current Market Dysfunction

The magnitude of the current disruption fundamentally differentiates this crisis from previous supply interruptions. Historical oil crises typically affected 2-4% of global supply through production cuts or embargo policies, creating manageable market stress that could be absorbed through strategic reserve releases and alternative sourcing.

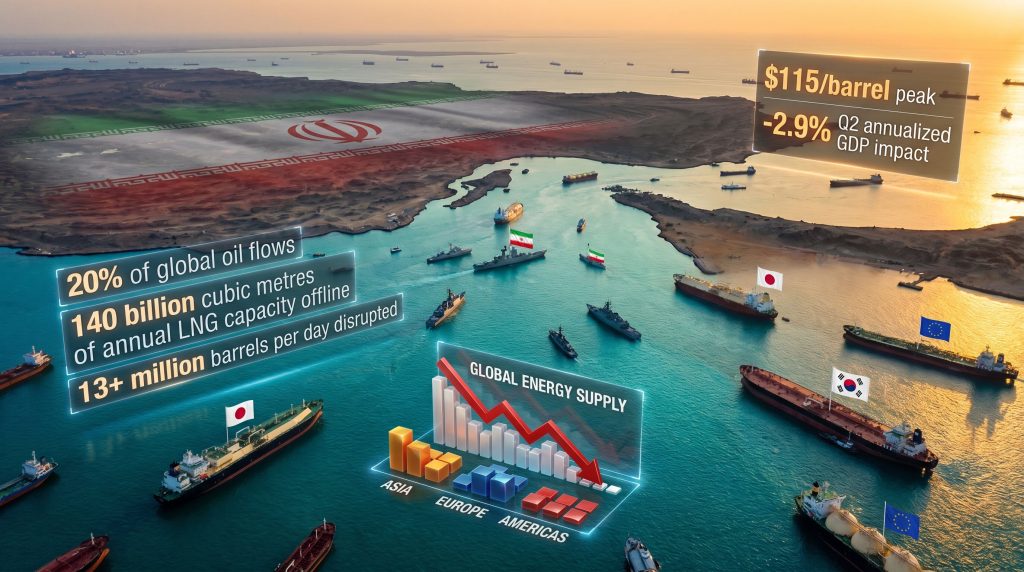

Current verified disruption metrics paint a dramatically different picture. Daily oil throughput loss exceeds 13+ million barrels per day eliminated from global flows, whilst 80% of Asian oil imports are affected simultaneously.

This represents a 5-10x multiplication in disruption magnitude compared to historical precedent, pushing global markets beyond the absorption capacity of traditional stabilisation mechanisms. In addition, the OPEC production impact analysis shows how traditional supply response mechanisms have failed under current geopolitical pressures.

Critical Disruption Metrics

The following data illustrates the unprecedented scale of current market stress:

- Daily oil throughput loss: 13+ million barrels per day eliminated from global flows

- Geographic concentration: 80% of Asian oil imports affected simultaneously

- LNG trade impact: 20% of global liquefied natural gas supplies disrupted

- Critical timeline: 4-6 week supply buffer period before operational crisis

Unlike previous crises that could theoretically be resolved through diplomatic channels or production adjustments, the current situation involves absolute physical constraints that economics cannot overcome. Moreover, this crisis coincides with natural gas trends that compound energy market volatility.

The Technical Failure of Supply Response Mechanisms

Analysis of global supply response capabilities reveals why conventional economic theory proves inadequate in the current environment. The United States faces export constraints with current export infrastructure operating at maximum capacity, whilst domestic political pressure prioritises internal supply security.

Alternative routing limitations present additional challenges. Navigation through contested maritime zones increases operational risks by 14-21 days additional transit time for alternative shipping routes. Consequently, limited port infrastructure capacity cannot handle redirected volumes effectively.

Strategic reserve inadequacy compounds these problems. OECD commercial stocks are approaching minimum operational thresholds, whilst strategic petroleum reserves provide only temporary relief measures. No mechanism exists to replace sustained daily flow requirements through inventory releases.

Regional Market Fragmentation Under Crisis Pressure

The integrated global oil market is rapidly decomposing into three competing regional blocs, each operating under distinct constraints and political priorities. This fragmentation represents a fundamental reversal of decades of globalisation in energy trade, with profound implications for pricing mechanisms and supply security.

European Energy Bloc Vulnerabilities

European markets face acute structural stress following years of energy architecture restructuring. The continent's strategic shift away from Russian hydrocarbons toward seaborne Middle Eastern imports created new dependency vulnerabilities that the current crisis exploits directly.

European refinery infrastructure demonstrates particular vulnerability due to decades of underinvestment and facility closures. The continent's refining capacity was optimised for specific crude grades, creating technical and economic inefficiencies when attempting to substitute Middle Eastern supplies with alternative sources.

| Vulnerability Factor | Impact Level | Timeline |

|---|---|---|

| Middle Eastern import dependency | 60% of seaborne supplies | Immediate |

| Refinery optimisation constraints | Limited crude substitution capability | 2-4 weeks |

| Diesel shortage onset | Structural shortage acceleration | Early May 2026 |

| Commercial inventory levels | Approaching operational minimums | 4-6 weeks |

Asian Market Dependencies and Constraints

Asian economies face the most severe exposure to Strait of Hormuz oil market disruption due to historical dependence on Middle Eastern crude supplies. Regional import patterns reveal systematic vulnerabilities that cannot be rapidly addressed through alternative sourcing.

The cascading failure mechanism is evident as procurement strategies shift from optimisation-based decision making to survival-focused crisis management. Long-term supply contracts face renegotiation under force majeure conditions, while spot markets experience unprecedented tightening pressures.

Furthermore, the Saudi exploration licenses situation demonstrates how regional supply dependencies create additional market vulnerabilities during crisis periods.

Asian Import Dependency Analysis:

- South Korea: 85%+ import reliance with limited domestic resources

- Japan: Similar import dependency with minimal strategic alternatives

- China and India: Pursuing Russian crude substitution but insufficient to offset Gulf supply losses

- Regional average: 60%+ of crude imports historically sourced from Gulf suppliers

North American Strategic Response Limitations

Despite theoretical capacity to serve as a global swing supplier, North American energy markets face their own constraints that limit crisis response capabilities. Political considerations increasingly take precedence over market efficiency as domestic energy security becomes paramount.

Export capacity limitations due to pipeline and port bottlenecks restrict response flexibility. Shale production response is limited by capital allocation cycles, whilst Congressional pressure prioritises domestic supply over global markets. Additionally, transportation infrastructure optimisation for internal distribution rather than export creates further constraints.

Market Signal Breakdown and Storage Crisis Indicators

Traditional market indicators provide misleading information about crisis severity, creating dangerous blind spots for policymakers and market participants. The disconnect between futures pricing and physical market reality indicates fundamental dysfunction in price discovery mechanisms.

Physical Market Reality vs Financial Market Signals

Misleading financial indicators include futures contracts pricing temporary disruption scenarios rather than sustained crisis. Benchmark pricing fails to reflect regional physical market premiums, whilst options markets underestimate long-term supply constraint duration.

However, actual physical market conditions reveal a different reality. European and Asian refinery throughput reductions occur due to feedstock unavailability, not demand weakness. Accelerating inventory drawdowns exceed headline price implications, whilst commercial storage facilities approach minimum operational levels.

"The critical insight is that reduced refinery operations indicate supply chain failure rather than demand destruction, representing a complete inversion of traditional economic interpretation."

Storage Infrastructure Critical Thresholds

Global petroleum storage systems operate with minimum buffer requirements that maintain operational flexibility and emergency response capability. Current inventory trajectories indicate these critical thresholds will be breached within weeks rather than months.

The storage depletion dynamic follows an accelerating curve as remaining inventories become increasingly concentrated in locations with limited distribution capability. This effectively reduces accessible supply faster than headline numbers suggest.

Timeline Analysis:

- Early May 2026: Optimistic scenario for initial critical shortage manifestation

- Mid-May 2026: Widespread acknowledgment of supply crisis severity

- June-July 2026: Potential for rolling blackouts and fuel rationing implementation

Geopolitical Control Mechanisms Replacing Market Forces

The transformation of the Strait of Hormuz from a commercial shipping lane into a militarily controlled chokepoint represents a fundamental shift in global energy governance. Traditional assumptions about diplomatic resolution and market-based solutions prove inadequate when confronting deliberate infrastructure weaponisation.

Iranian Revolutionary Guard Corps Strategic Control

Intelligence analysis reveals that power within Iran has shifted decisively toward the Islamic Revolutionary Guard Corps (IRGC), an entity whose strategic objectives differ fundamentally from civilian government priorities. This internal power realignment eliminates traditional diplomatic channels and negotiation mechanisms.

The IRGC approach represents a calculated strategy of managed chokepoint control rather than complete closure. This allows Iran to retain strategic leverage whilst maximising economic pressure on global markets, representing sophisticated economic warfare that traditional military or diplomatic responses cannot effectively counter.

IRGC Control Mechanisms:

- Ship movement approval: All transit requires explicit military authorisation

- Selective closure strategy: Maintaining leverage whilst avoiding full military confrontation

- Long-war doctrine implementation: Designed to exploit Western dependency on stable energy flows

- Maximum economic pressure tactics: Strategic timing to amplify market disruption

Power-Based Allocation Systems

The current crisis demonstrates how geopolitical control can completely override market-based allocation mechanisms. Ship movements are now determined by military command rather than commercial logic, with cargo priorities established through political rather than economic criteria.

This represents a fundamental inversion of the global energy trade system, where access to supplies depends on political relationships rather than purchasing power. The implications extend far beyond temporary supply adjustments, suggesting a permanent alteration in global energy governance structures.

Moreover, the US‑China trade impact analysis reveals how existing trade tensions compound these geopolitical control mechanisms, creating multiple pressure points in the global energy system.

Economic Impact Assessment and Recovery Scenarios

Macroeconomic modelling of the current crisis reveals impacts that extend far beyond energy sectors, with cascading effects throughout global supply chains, financial markets, and developing economy stability. Traditional monetary and fiscal policy tools prove inadequate when confronting physical supply constraints.

Systemic Economic Risk Factors

Global GDP contraction projections show a 2.9 percentage point annualised decline for Q2 2026, whilst energy-driven broad-based price increases affect multiple sectors. Nine critical commodities face disruption beyond petroleum products, whilst agricultural input costs rise due to fertiliser and transport expense escalation.

Financial market vulnerability spreads energy sector stress to broader equity markets. Developing economy debt service obligations become complicated by higher energy import costs, whilst currency volatility affects energy-importing nations disproportionately.

The Trump tariffs impact analysis provides additional context on how trade policy changes interact with energy market disruptions to amplify economic stress.

Recovery Timeline Analysis

Economic recovery scenarios depend heavily on crisis resolution timing, with each additional month of disruption creating exponentially greater long-term structural damage to global trade relationships and infrastructure systems.

| Disruption Period | Oil Price Peak | GDP Impact | Long-term Market Structure |

|---|---|---|---|

| 2-month resolution | $115/barrel | -2.9% Q2 annualised | Temporary regionalisation |

| 6-month sustained crisis | $150-200/barrel | -4.5% annual | Permanent market fragmentation |

| Partial reopening scenario | $90-110/barrel range | -1.8% annual | Managed chokepoint system |

The modelling indicates that recovery timelines extend far beyond crisis resolution due to structural changes in energy trade relationships. Infrastructure investment patterns and risk management strategies adopted during the crisis period create lasting effects.

The next major ASX story will hit our subscribers first

Long-Term Implications for Global Energy Architecture

The current crisis accelerates fundamental shifts in global energy governance that were already developing due to climate policy, technological change, and geopolitical realignment. These changes represent permanent alterations rather than temporary crisis responses.

Structural Changes in Energy Trade

Regional energy blocs replace global integration as continental supply systems emerge. Security premium pricing values geopolitical stability over cost optimisation, whilst infrastructure redundancy prioritises multiple supply routes despite higher operational costs.

Capital allocation now prioritises supply chain resilience over efficiency. Domestic energy production receives preference despite higher costs, whilst infrastructure projects are evaluated primarily on security rather than economic criteria. Technology development focuses on supply chain independence rather than pure cost reduction.

Policy Tool Limitations

Traditional economic policy instruments prove inadequate when confronting physical supply constraints rather than demand-driven market imbalances. Central bank monetary policy and government fiscal measures cannot create physical energy supplies or overcome infrastructure limitations.

Interest rate mechanisms cannot generate crude oil supplies or overcome transport bottlenecks. Strategic reserve releases provide temporary market relief but cannot substitute for sustained production flows. Demand destruction policies show limited effectiveness due to the essential nature of energy consumption.

International coordination faces obstacles from competing national interests and limited spare capacity. This represents a fundamental limitation of economic policy tools that were designed for demand-side management rather than supply-side physical constraints.

Market Psychology and Investment Strategy Evolution

The Strait of Hormuz oil market disruption demonstrates how geopolitical risk assessment must evolve beyond traditional models that assumed diplomatic resolution and market-based adjustment mechanisms. Investment strategies require fundamental recalibration to account for weaponised infrastructure and power-based resource allocation.

Investment Strategy Implications

Domestic energy production companies gain strategic premium valuations, whilst pipeline and storage infrastructure become critical strategic assets. Renewable energy adoption accelerates due to supply security considerations, and energy efficiency technologies receive increased investment priority.

Supply chain diversification becomes paramount for investment consideration. Regional market exposure requires careful portfolio balance, whilst currency hedging strategies adapt to energy-driven volatility patterns. Commodity exposure management requires sophisticated geopolitical analysis capabilities.

The energy crisis analysis from Bloomberg provides detailed insights into how financial markets are adapting to these new realities.

Sectoral Impact Analysis

Transportation industries face fundamental cost structure changes, whilst manufacturing sectors require energy input substitution strategies. Agricultural operations confront fertiliser and transport cost escalation, and financial services adapt to energy-driven credit risk assessment.

Energy sector positioning shows domestic production gaining strategic advantage. Geographic risk assessment requires comprehensive supply chain analysis, whilst sectoral exposure management becomes increasingly complex.

Technological and Infrastructure Adaptation Requirements

The crisis accelerates technological development and infrastructure investment in areas previously considered secondary priorities. Emergency innovation cycles compress normal development timelines as market forces drive rapid adaptation to supply constraints.

Critical Technology Development Areas

Accelerated renewable energy deployment driven by supply security requirements receives emergency funding priority. Energy storage technology development advances rapidly, whilst grid infrastructure hardening protects against supply disruption scenarios.

Electric vehicle adoption accelerates due to fuel price volatility, whilst alternative fuel development for commercial aviation and shipping gains momentum. Rail and water transport infrastructure receive increased investment, and last-mile delivery optimisation reduces transport energy intensity.

Manufacturing processes undergo redesign for energy efficiency. The chemical industry develops alternative feedstock sources, whilst recycling and circular economy models gain economic viability. Industrial heat pump technology advances rapidly under crisis pressure.

Infrastructure Investment Priorities

Critical infrastructure receives strategic rather than purely economic evaluation. Alternative energy infrastructure development accelerates beyond normal market-driven timelines, whilst energy storage capabilities become national security priorities.

The International Monetary Fund analysis provides official perspective on infrastructure requirements for managing energy security during extended crisis periods.

Financial Market Structural Changes

Energy market dysfunction spreads throughout global financial systems as traditional risk models prove inadequate for assessing physical supply constraints and geopolitical infrastructure control. Market structure evolution reflects adaptation to power-based rather than price-based resource allocation.

Trading and Risk Management Evolution

Commodity trading firms gain advantage over purely financial players, whilst storage and logistics capabilities become strategic competitive advantages. Regional market expertise increases in value over global arbitrage skills, and political risk assessment becomes central to energy trading strategies.

Energy-dependent industries face increased borrowing costs, whilst political risk insurance premiums escalate significantly. Supply chain financing incorporates geopolitical risk factors, and force majeure clauses require comprehensive revision.

Capital markets prioritise energy security over pure efficiency metrics. Infrastructure investment receives strategic premium valuations, whilst technology sectors benefit from energy independence themes. Emerging market exposure requires reassessment based on energy import dependency.

Long-term Financial Architecture Changes

The Strait of Hormuz oil market disruption creates permanent changes in financial market structure that extend beyond crisis resolution. Risk assessment methodologies incorporate geopolitical infrastructure control as a primary factor, whilst traditional arbitrage opportunities diminish under regionalised market conditions.

Investment allocation strategies adapt to prioritise supply chain security over pure efficiency metrics. This represents a fundamental shift in capital market functioning that affects global economic development patterns for years beyond the immediate crisis period.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and geopolitical developments. Energy markets remain highly volatile and subject to rapid changes based on political developments, infrastructure status, and international negotiations. Readers should conduct independent research and consult qualified financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry inherent risks including potential loss of principal.

Ready to Capitalise on Energy Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, enabling subscribers to identify actionable investment opportunities as energy market volatility creates new demand for critical materials and resources. Begin your 14-day free trial today to position yourself ahead of evolving market conditions and secure your competitive advantage in this dynamic investment landscape.