May 21, 2026

The Strait of Hormuz: When a 33-Kilometre Passage Holds the World's Energy System Hostage

Imagine an energy system so centralised, so structurally dependent on a single geographic point, that the decisions of two governments can simultaneously destabilise fuel supply chains across four continents. That is the precise reality confronting global energy markets as Iran threatens wider retaliation over new US strikes and the Strait of Hormuz remains one of the most volatile flashpoints in modern geopolitical history.

The crisis unfolding in 2026 is not simply a bilateral confrontation. It is a live stress test of the assumptions underpinning global energy security architecture, and the results are deeply uncomfortable.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Cannot Be Replaced or Bypassed

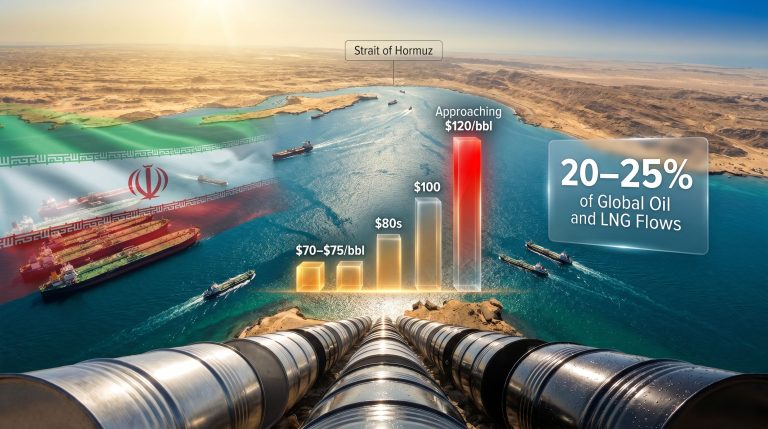

The Strait of Hormuz is a narrow maritime corridor measuring approximately 33 kilometres at its most constrained navigable width, connecting the Persian Gulf to the Gulf of Oman. Under normal operating conditions, roughly one-fifth of all globally traded oil and liquefied natural gas passes through this passage, according to U.S. Energy Information Administration data. No other maritime chokepoint carries a comparable share of global energy trade in such a geographically concentrated form.

The countries most directly exposed to disruptions in this corridor include:

- Japan and South Korea, which source the overwhelming majority of their crude oil imports from Persian Gulf producers

- India, which has significantly expanded its dependence on Gulf crude as domestic refining capacity has grown

- China, the world's largest crude oil importer, with substantial volumes transiting Hormuz monthly

- Parts of Southern Europe and Sub-Saharan Africa, which rely on Gulf LNG and crude shipments as key supply inputs

While alternative routing is theoretically possible, the practical economics are punishing. Redirecting tanker traffic around the Cape of Good Hope adds approximately 10 to 15 days to voyage times for Asian-bound cargoes. That extension compounds freight costs, strains vessel availability, and tightens effective supply even when the physical oil has not been destroyed. The Suez Canal offers partial relief for some routes but cannot absorb a wholesale rerouting of Persian Gulf export volumes. Furthermore, the global LNG supply outlook makes alternative sourcing increasingly complex for the most exposed economies.

The 2026 Crisis Is Structurally Different From Every Previous Hormuz Standoff

Historical episodes of Hormuz tension, including the 1980s Tanker War and the 2019 Gulf of Oman vessel incidents, were characterised by isolated provocations followed by relatively rapid de-escalation. Markets repriced briefly, diplomatic channels absorbed the pressure, and commercial transit largely continued.

The current confrontation does not follow that pattern. Several structural features distinguish this crisis from its predecessors:

- A functioning U.S. naval blockade of Iranian ports is actively limiting Iran's export capacity and economic lifeline

- The IRGC Navy is directly coordinating commercial vessel transit, with only 26 ships transiting the strait in a single 24-hour period, well below pre-conflict throughput norms

- Three commercial vessels sustained confirmed attacks within days, verified by both UK military monitoring and IRGC statements

- Diplomatic channels have effectively collapsed, with Pakistan-mediated back-channel talks described by both sides as producing no substantive progress

- Iran's parliament has publicly signalled that the ceasefire window has been used to rebuild military capacity rather than pursue compromise

Critical Insight: The combination of an active blockade, live vessel attacks, and publicly confirmed military rebuilding during a nominal ceasefire represents a qualitative shift from speculative Hormuz risk to operationally active supply disruption. Markets that continue treating this as a temporary disruption may be systematically mispricing sustained structural risk.

Decoding Iran's Escalation Signals: What the IRGC Warning Actually Means

The IRGC issued a formal warning stating that any renewed military aggression would produce retaliation extending beyond the Middle East, with specific language indicating strikes in locations that adversaries would not anticipate. This language is analytically significant for several reasons.

First, it represents a deliberate departure from Iran's previous doctrine of geographically contained response. Tehran has historically framed its retaliatory posture around proportional in-region responses: missile strikes on U.S. military facilities in Iraq, harassment of Gulf shipping, or proxy activation in Yemen and Lebanon. The explicit reference to extra-regional retaliation introduces a new threat vector. Iran's threats of retaliation against the US have been widely reported, underscoring the seriousness with which analysts are treating the current escalation.

Second, Iran has demonstrated operational capacity for geographically distributed attacks. Its documented history includes precision missile and drone strikes on Saudi oil infrastructure, coordinated proxy warfare through aligned groups across Iraq, Syria, Lebanon, and Yemen, and cyber operations targeting energy sector control systems.

Third, the nuclear enrichment dimension remains the structural core of the impasse. Washington has insisted on a permanent halt to enrichment activities and the surrender of Iran's highly enriched uranium stockpile. Tehran has publicly rejected both conditions as existential concessions incompatible with national sovereignty. This is not a negotiating gap that intermediary diplomacy can easily bridge.

Escalation Mechanism Assessment

| Escalation Mechanism | Current Status | Global Risk Level |

|---|---|---|

| Commercial shipping interdiction (Hormuz) | Active, 3 vessels confirmed attacked | Critical |

| Uranium enrichment continuation | Ongoing, no concessions offered | High |

| Proxy network activation across Gulf region | Elevated readiness confirmed publicly | High |

| Cyber operations targeting energy infrastructure | Elevated risk, no confirmed active campaigns | Medium to High |

| Missile and drone strikes on U.S. facilities | Prior incidents confirmed, ceasefire nominally active | Medium |

| Extra-regional retaliation execution | Declared intent, not yet executed | Elevated |

How Global Oil Markets Are Processing the Threat Environment

Brent crude was trading near $107 per barrel at the time of the latest IRGC warning, having fallen approximately 3.5% in a single session despite the renewed escalation rhetoric. To a casual observer, a price decline during a period of intensified military threats appears counterintuitive. Understanding why this occurred reveals important dynamics about how energy markets are currently processing geopolitical risk.

The session decline reflects a combination of short-term profit-taking by traders who had accumulated long positions ahead of anticipated escalation, and genuine uncertainty about whether the IRGC warning would translate into immediate physical supply disruption. Markets have learned, through repeated Hormuz episodes, to discount statements that are not immediately backed by verifiable operational action.

However, the year-to-date price trajectory tells a fundamentally different story. Brent crude remains substantially elevated on an annual basis, reflecting the cumulative supply pressure generated by sustained Hormuz restriction, reduced Iranian export volumes, and the compounding effect of elevated war-risk insurance premiums on tanker operations. The broader context of oil market geopolitics in 2025 and 2026 has consistently pointed toward structural upward pressure on energy prices.

The shipping insurance dimension is often underappreciated in mainstream energy market analysis. War-risk insurance premiums for vessels transiting the Persian Gulf corridor can increase by multiples during active conflict episodes. This cost escalation is passed through the supply chain as higher delivered energy prices, affecting end consumers in Asia and Europe even when the nominal crude price appears stable. Fuel shortages have already been reported across parts of Asia as a downstream consequence of reduced strait throughput.

Three Market Scenarios and Their Implications

Scenario 1: Diplomatic Breakthrough (Low probability, near-term)

The U.S. modifies its naval blockade conditions, Iran permits full commercial transit resumption, and back-channel talks produce a framework agreement. Under this pathway, Brent crude would likely retrace toward the $85 to $90 per barrel range as the geopolitical risk premium deflates. War-risk insurance would normalise over approximately four to six weeks.

Scenario 2: Sustained Stalemate (Base case)

The ceasefire holds nominally while Hormuz remains partially restricted. Intermittent vessel incidents continue, neither side makes substantive concessions, and Asian importers accelerate strategic reserve drawdowns and alternative supplier diversification. Oil prices remain elevated in the $100 to $115 per barrel band, with global refinery margins staying compressed.

Scenario 3: Full Re-Escalation (Tail risk, elevated probability)

Additional U.S. military strikes are authorised, Iran executes extra-regional retaliation and expands the Hormuz blockade. Under this scenario, analyst scenario frameworks indicate Brent crude could spike toward $130 to $150 per barrel in an acute shock event. Global shipping rerouting becomes operationally mandatory, and LNG spot markets face acute tightening as Asian importers compete for alternative supply.

Investor Warning: The tail-risk scenario carries meaningfully higher probability than historical Hormuz episodes would suggest. U.S. officials have publicly indicated additional military action could occur within days absent diplomatic progress, and Iran has explicitly confirmed active military preparedness for renewed conflict. Positioning that treats scenario three as a remote outcome may be inadequately hedged.

The Gulf State Dilemma: Exposed Partners Caught Between Two Powers

Saudi Arabia, Qatar, and the United Arab Emirates occupy a structurally precarious position in this conflict. They are simultaneously U.S. security partners benefiting from American military presence in the region, major hydrocarbon exporters dependent on Hormuz transit for their own revenue streams, and geographically proximate to any conflict expansion involving Iranian targeting doctrine.

All three states have communicated to the U.S. administration a preference for extending the diplomatic window before authorising further military action. This advocacy reflects rational self-interest: a broadening of the conflict that damages Gulf energy infrastructure or disrupts loading operations at major LNG and crude export terminals would impose direct economic costs on Riyadh, Doha, and Abu Dhabi. Consequently, OPEC's market influence over price stabilisation becomes increasingly constrained when the strait itself is under threat.

The secondary vulnerability of Gulf state energy infrastructure is a dimension often absent from market commentary. Major LNG export terminals, crude oil loading facilities, and pipeline corridors serving these producers represent high-value targets if Iran expands its operational doctrine beyond direct bilateral engagement with U.S. forces.

Pakistan's role as the primary intermediary in back-channel communications reflects both its historical relationships with both parties and the absence of any other willing mediator with simultaneous access to Tehran and Washington. U.S. officials have described reaching a diplomatic deal as the preferred outcome while characterising renewed military action as the secondary option, language that implicitly confirms the military pathway remains operationally ready regardless of diplomatic preferences.

The next major ASX story will hit our subscribers first

Proxy Networks, Cyber Risk, and the Distributed Threat Architecture

One of the analytically underappreciated dimensions of the current crisis is Iran's distributed deterrence architecture. Tehran has invested decades in cultivating aligned groups across Iraq, Syria, Lebanon, and Yemen, specifically to provide retaliatory capacity that does not require direct Iranian military action. These networks retain operational capacity during ceasefire periods and can be activated in response to renewed strikes with limited warning.

The Council on Foreign Relations has identified energy infrastructure targeting, including Gulf state oil facilities and undersea pipeline corridors, as a high-probability escalation pathway if direct military engagement resumes. This assessment reflects both the historical targeting patterns of Iran-aligned groups and the strategic logic of imposing maximum economic cost on U.S. regional partners.

The cyber dimension adds a further layer of complexity. Iran has a documented history of sophisticated cyber operations against energy sector targets, including the 2012 Shamoon attack on Saudi Aramco that destroyed data on approximately 30,000 workstations. The IRGC's explicit warning about retaliation in unexpected locations is entirely consistent with a cyber escalation strategy targeting critical energy infrastructure beyond the immediate Gulf theatre.

Israel's potential role as a co-belligerent further complicates the risk calculus. Iran has explicitly warned that any Israeli participation in renewed strikes would trigger a proportional response, adding a third-party escalation vector that could rapidly expand the geographic scope of conflict beyond what either Washington or Tehran intends. In addition, the compounding effects of trade war oil impacts on an already stressed energy system amplify the downstream risks for global importers.

Key Signals That Will Define the Trajectory of This Crisis

For investors, analysts, and energy security practitioners monitoring the Iran-US confrontation, the following indicators carry the highest forward-looking diagnostic value:

- Hormuz daily transit volume: Any further decline from the already-suppressed 26-vessel figure would indicate active operational escalation rather than managed restriction

- War-risk insurance premium movements: A sharp spike in specialist marine war-risk rates from Lloyd's of London syndicates would precede formal market acknowledgement of escalation and represents an early-warning signal

- U.S. carrier strike group positioning: Changes in the deployment posture of naval assets in the Persian Gulf and Gulf of Oman indicate shifts in operational readiness that typically precede military action

- Iranian uranium enrichment announcements: Any declared acceleration in enrichment activity, particularly toward weapons-grade thresholds, would collapse the remaining diplomatic space entirely

- Gulf state emergency diplomacy signals: Public statements from Riyadh, Doha, or Abu Dhabi calling for urgent mediation would indicate regional powers perceive imminent escalation risk beyond what is publicly acknowledged

- Proxy group operational activity: Drone or missile activity from Iran-aligned groups in Iraq, Yemen, or Lebanon would signal Tehran is activating its distributed deterrence architecture in anticipation of renewed direct conflict

Frequently Asked Questions

What percentage of global oil trade passes through the Strait of Hormuz?

According to EIA data, approximately 20% of all globally traded oil and LNG transits the Strait of Hormuz under normal conditions. No alternative maritime corridor carries a comparable share of global energy trade, making it the single most consequential energy chokepoint on Earth.

Why can't tankers simply reroute around the strait?

While Cape of Good Hope rerouting is physically possible, it adds 10 to 15 days to voyage times for Asian-bound cargoes, significantly inflates freight and fuel costs, and does nothing to address the supply-side reduction caused by lower Iranian and Gulf state export volumes. The economics of rerouting compound supply tightness rather than resolving it.

What does Iran's extra-regional retaliation threat mean in operational terms?

Analysts interpret the IRGC warning as signalling potential activation of proxy networks, cyber operations against energy infrastructure in geographically dispersed locations, or targeting of assets in European or Central Asian corridors, rather than limiting responses to the immediate Gulf theatre.

How high could oil prices go under a full Hormuz closure?

Current analyst scenario frameworks place Brent crude in the $130 to $150 per barrel range under an acute full-closure shock scenario, contingent on closure duration and the speed of strategic petroleum reserve releases by major consuming nations.

Is a diplomatic resolution realistic?

Back-channel talks through Pakistani intermediaries remain nominally active, but the structural impasse over uranium enrichment and the U.S. naval blockade of Iranian ports represents a gap that intermediary diplomacy alone is unlikely to bridge without significant concessions from at least one party. Both sides have publicly acknowledged the talks are stalled.

Which economies face the greatest exposure to prolonged disruption?

Japan, South Korea, India, and China carry the highest direct economic exposure given their dependence on Persian Gulf crude and LNG imports. Parts of South and Southeast Asia are already experiencing downstream fuel supply shortfalls as a consequence of reduced strait throughput under current conditions. The oil prices and trade tensions affecting China in particular add a further dimension of vulnerability for the world's largest crude importer.

The Structural Shift That Markets Are Only Beginning to Price

The 2026 Iran-US confrontation has done something that no previous Hormuz episode achieved: it has converted a theoretical chokepoint vulnerability into an actively weaponised supply constraint operating in real time. The combination of a functioning naval blockade, confirmed commercial vessel attacks, explicitly declared extra-regional retaliation doctrine, and a structurally deadlocked nuclear negotiation creates a risk environment with no meaningful historical parallel for energy markets to calibrate against. Consequently, as Iran threatens wider retaliation over new US strikes, the pressure on policymakers and market participants to reassess long-held assumptions is mounting.

The long-term structural implications extend well beyond current price levels. Major Asian importers that have already begun accelerating strategic petroleum reserve investments and alternative supplier diversification are unlikely to reverse those strategies even if this specific crisis de-escalates. The demonstrated vulnerability of Hormuz-dependent supply chains will drive durable investment in LNG infrastructure diversification, alternative corridor development, and strategic reserve capacity across the Indo-Pacific region.

Gulf state producers face a compounding challenge: they are simultaneously exposed to conflict spillover risk and entirely dependent on Hormuz transit for the export revenues that fund their own economic diversification programmes. Any scenario involving sustained strait disruption imposes direct costs on the very states most vocally advocating for restraint.

The energy security assumption that has underpinned global commodity markets for four decades — that Hormuz disruption is a tail risk rather than a baseline operating condition — may be in the process of being permanently revised. That revision, if it proves durable, carries implications for energy pricing, infrastructure investment, and geopolitical risk premiums that extend far beyond the immediate trajectory of the Iran-US confrontation.

This article contains forward-looking analysis and scenario projections based on publicly available information as of the date of publication. Energy price forecasts and geopolitical scenario assessments involve significant uncertainty. Nothing in this article constitutes financial or investment advice. Readers should conduct independent analysis before making any investment decisions.

Want to Capitalise on the Resource Opportunities Emerging From Global Energy Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex market data to surface actionable opportunities as geopolitical shocks reshape commodity demand and energy security investment flows. Explore how historic mineral discoveries have generated substantial returns for early investors, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major market-moving announcement.