May 20, 2026

The Strait That Could Break Global Energy Markets

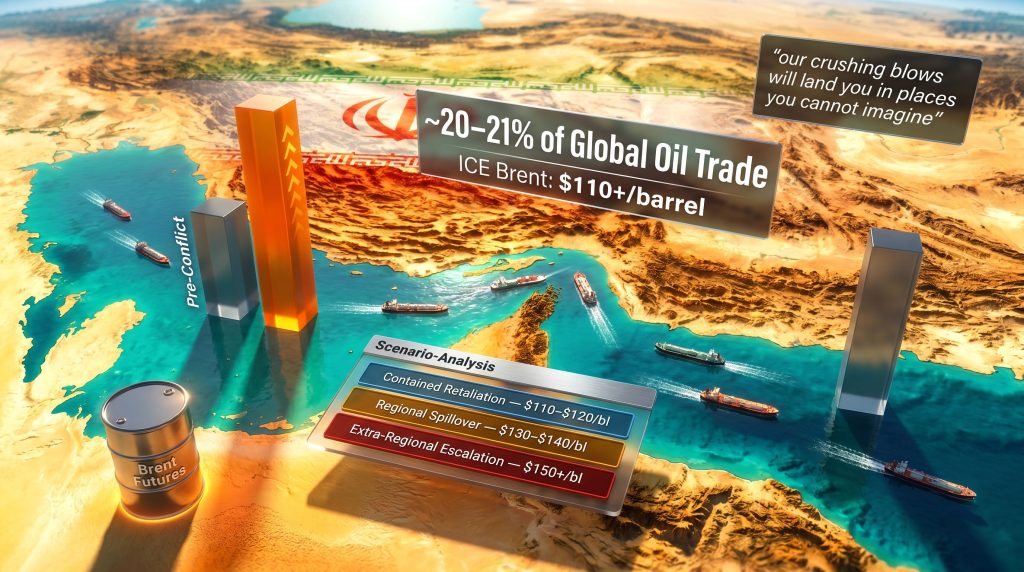

When geopolitical friction reaches the world's most critical energy chokepoint, commodity markets do not simply react — they reprice reality. The Strait of Hormuz has long been described as a shipping lane, but that framing dramatically understates its function. It is, more precisely, a sovereign lever: a 33-kilometre-wide passage through which approximately 20 to 21 percent of all globally traded oil transits every single day. For Iran, this geography is not passive inheritance. It is strategic capital, and Tehran has now moved decisively to formalise that control in ways that extend well beyond military posturing.

Understanding what Iran warns new US-Israeli strikes will broaden war truly means requires stepping back from the immediate headlines and examining the structural architecture Iran has been quietly constructing around the strait — and what the commodity market consequences of each possible escalation pathway could be. The crude oil volatility trends feeding into current pricing reflect a market recalibrating in real time.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz Has Become a Sovereign Instrument

Iran's establishment of the Persian Gulf Strait Authority (PGSA) marks a categorical shift in how Tehran intends to manage the waterway going forward. This is not a symbolic gesture. The PGSA operates as a legal administrative body requiring all vessels transiting the strait to obtain formal permits and comply with a published regulatory framework. Passage without authorisation is now classified as illegal under Iran's unilaterally declared maritime governance structure.

Simultaneously, Iran launched the "Hormuz Safe" digital insurance platform, which provides cover for Iranian ships and cargo transiting the waterway, with payments settled in cryptocurrency. The significance of cryptocurrency settlement should not be overlooked: it is a deliberate architectural choice designed to operate entirely outside Western financial infrastructure, including the SWIFT system and US dollar-denominated insurance markets.

On 4 May, Iran formally claimed administrative authority over a significantly expanded maritime zone, stretching from the western tip of Qeshm Island to Umm al-Quwain on the UAE's western coast, and from Kuh Mobarak in Hormozgan province to southern Fujairah on the UAE's eastern coast. This territorial claim provides Iran with the legal scaffolding to argue that any vessel it intercepts or refuses passage has violated its sovereign jurisdiction.

Strategic Architecture Note: Iran's maritime authority move is not symbolic. It is a legal and operational framework designed to make any future closure of the strait internationally defensible under its own governance structure, while simultaneously building financial infrastructure immune to Western sanctions.

Six Weeks of Strikes, One Underestimated Outcome

Beginning on 28 February, US and Israeli forces launched approximately six weeks of intensive strike operations targeting Iranian military assets, leadership infrastructure, and energy facilities. The physical damage was substantial. The strategic outcome, however, produced a critical miscalculation: the strikes largely failed to destabilise the Iranian government's internal grip on power.

The consequences for global commodity markets were immediate and severe:

- Iranian armed forces effectively restricted passage through the Strait of Hormuz, dramatically curtailing commercial shipping volumes

- Multiple Gulf Cooperation Council (GCC) member states dependent on Hormuz transit were forced to curtail both oil and LNG export volumes

- Front-month ICE Brent crude futures surged above $110 per barrel, representing a price increase of more than 50 percent compared to pre-conflict levels

- War risk insurance premiums for Hormuz-transiting vessels spiked, creating a cost shock for shipping operators globally

- A US naval blockade of Iranian ports compounded the disruption, adding a second vector of supply constraint to an already stressed market

Key Metric: A 50%+ surge in Brent crude pricing within approximately three months represents one of the fastest geopolitical oil price shocks in modern commodity market history — comparable in pace, though not yet in duration, to the 1973 Arab oil embargo.

Escalation Scenarios: Stress-Testing the Next 90 Days

The Islamic Revolutionary Guard Corps (IRGC) issued explicit warnings that any renewed US or Israeli military action against Iran would cause the conflict to expand beyond the Middle East Gulf region entirely. The IRGC specifically stated that Iranian forces did not deploy their full range of capabilities during the initial phase of the conflict — a deliberate deterrence signal framing all prior strikes as a constrained response, not a maximum one. Three forward-looking scenarios now define the market's risk envelope.

Scenario 1: Contained Retaliation

Iran responds to any new strike within the existing theatre, targeting US or Israeli military assets symmetrically. The PGSA permit framework remains operative, keeping the strait partially functional. Brent crude stabilises in the $110 to $120 per barrel range; LNG spot prices remain elevated but manageable.

Probability: Low

Scenario 2: Regional Spillover

Iranian retaliation extends to GCC energy infrastructure across Saudi Arabia, the UAE, and Kuwait — including export terminals, desalination plants, and refinery assets. Simultaneous drone and missile activity across multiple production zones disrupts the GCC's collective export capacity. Brent could breach $130 to $140 per barrel; LNG markets face acute supply shortfalls; natural gas-derived fertiliser feedstock costs spike as upstream gas prices surge.

Probability: Moderate

Scenario 3: Extra-Regional Escalation

Iran activates proxy networks and asymmetric capabilities beyond the Middle East, potentially including cyber and physical action targeting Western energy and financial infrastructure. This scenario corresponds directly to the IRGC's explicit warning that retaliatory strikes would reach places the US and Israel cannot anticipate. Commodity price discovery above $150 per barrel becomes plausible; global LNG supply contracts face force majeure clause activation; petrochemical feedstock markets enter systemic disruption.

Probability: Low to Moderate, but highest potential impact

| Escalation Scenario | Hormuz Status | Brent Price Range | LNG Market Impact | Probability |

|---|---|---|---|---|

| Contained Retaliation | Partially open (PGSA permits) | $110–$120/bl | Elevated, manageable | Low |

| Regional Spillover | Significantly restricted | $130–$140/bl | Acute shortfalls | Moderate |

| Extra-Regional Escalation | Effectively closed | $150+/bl | Force majeure risk | Low-Moderate |

Diplomacy Under Pressure: Pakistan, the Gulf, and the Nuclear Threshold

Pakistan's Role as Primary Mediator

Pakistan has emerged as the most consequential third-party actor in the current diplomatic process. It hosted the first formal round of negotiations between Iranian and US representatives in Islamabad in April, and Pakistan's interior minister subsequently travelled to Tehran for a further round of direct talks with Iranian officials. The choice of Pakistan as mediator reflects a sophisticated diplomatic logic: it is a Muslim-majority nuclear state with longstanding relationships on both sides, offering both parties political cover and credible neutrality.

Gulf Leaders as Conflict Managers

Perhaps the most structurally significant development of this conflict is the emergence of GCC leaders as active managers, not passive observers, of US military decision-making. The leaders of Qatar, Saudi Arabia, and the UAE directly intervened to persuade Washington to postpone a planned strike, effectively exercising a veto over US military timing. This represents a structural shift in regional power dynamics: Gulf states, facing direct economic exposure to any escalation's consequences, have inserted themselves as indispensable intermediaries between Washington and Tehran.

US President Donald Trump stated publicly that he had postponed military action after Gulf leaders indicated they believed a deal with Iran was within reach. Trump's own articulation of the minimum acceptable outcome focused specifically on preventing nuclear weapons capability from reaching Iranian hands — establishing the non-proliferation threshold as the non-negotiable core of any potential agreement. The broader trade war economic impact layered on top of these tensions has further complicated the diplomatic calculus.

Strategic Insight: Iran's ability to absorb six weeks of intensive strike operations without regime collapse has fundamentally altered the negotiating balance. Tehran now enters any diplomatic process having demonstrated extraordinary resilience — transforming durability itself into a bargaining asset.

What This Means for Global Commodity Markets

Crude Oil: The Embedded Risk Premium

ICE Brent futures holding above $110 per barrel no longer represent a temporary shock premium — they represent the market's revised baseline expectation for a world in which Hormuz transit remains constrained and escalation risk remains structurally elevated. Furthermore, OPEC+ production flexibility is significantly compromised by the fact that several key member states — including the UAE, Kuwait, and Iraq — are themselves directly exposed to regional escalation risk, limiting their ability to serve as compensatory supply backstops. The impact on oil markets from this dual pressure is compounding rapidly.

LNG: A Second Consecutive Geopolitical Supply Shock

Qatar, one of the world's largest LNG exporters, depends on Hormuz transit for a substantial share of its export volumes. Any renewed strait restriction would immediately tighten an already stressed global LNG market. The LNG supply outlook has deteriorated sharply as a result of these developments. European buyers, who spent 2022 and 2023 rebuilding supply chains after Russian pipeline gas disruption, now face the prospect of a second consecutive geopolitical supply shock affecting their LNG import economics. Asian LNG importers — particularly Japan, South Korea, and China — face spot price spikes and potential pressure to renegotiate long-term contract structures.

Fertiliser and Agricultural Cascade Effects

The Gulf region is a significant producer of natural gas-derived fertiliser feedstocks, including ammonia and urea. Supply disruption to these inputs propagates through the entire global agricultural cost structure. Egypt's NCIC fertiliser tender activity provides a useful real-time signal of regional pricing conditions: DAP has been tendered at up to $915 to $917 per tonne fob; granular urea at up to $865 per tonne fob. These benchmarks reflect a market already pricing in elevated feedstock costs and supply uncertainty — and they would move materially higher under a Scenario 2 or Scenario 3 escalation.

| Commodity | Pre-Conflict Baseline | Current Level | Key Risk |

|---|---|---|---|

| ICE Brent Crude | ~$72/bl (est.) | $110+/bl | Hormuz closure, escalation |

| LNG Spot (Europe/Asia) | Elevated post-2022 | Further spiking | Qatar export disruption |

| Urea (fob) | Below $700/t (est.) | Up to $865/t | Gas feedstock cost surge |

| DAP (fob) | Below $700/t (est.) | Up to $915–917/t | Ammonia supply chain |

Disclaimer: Pre-conflict baseline estimates are approximate and based on publicly available market data prior to February 2026. Commodity price data sourced from Argus Media market reporting.

The next major ASX story will hit our subscribers first

Strategic Stockpiling: Europe's Policy Response

One of the less widely discussed but highly consequential policy responses to Hormuz disruption risk is occurring in Norway. The Norwegian parliament, the Storting, is actively debating a proposal to increase emergency diesel and jet fuel reserves from the current 20 days of consumption to 90 days — an increase of 350 percent in buffer capacity. The energy and environment committee has already requested urgent government action, with an autumn 2026 deadline for proposals.

This debate was triggered by a Norwegian Defence Research Institute report from March 2026, which flagged Norway's dependence on imported diesel and jet fuel as a critical national security vulnerability. Norway operates only a single domestic refinery — the 203,000 barrel-per-day Mongstad facility run by state-controlled Equinor — creating concentrated infrastructure risk.

The policy significance extends well beyond Norway. As Europe's largest oil exporter and a country with no IEA stockholding obligation (the only such nation outside North America), Norway's pivot toward strategic fuel reserves signals a broader European recognition that Hormuz disruption is no longer a distant risk requiring only diplomatic management. In addition, the broader commodity market volatility stemming from this conflict is accelerating the case for physical domestic hedging across the continent.

Policy Signal: Norway's proposal to move from 20 to 90 days of strategic fuel reserves, if adopted, represents a 350% increase in buffer capacity — reflecting how seriously European governments are now treating the structural risk of Middle East supply disruption.

Sector Exposure Matrix: Who Bears the Most Risk

| Sector | Exposure Level | Key Risk Vector | Hedge Mechanism |

|---|---|---|---|

| Crude oil importers | Very High | Price spike + supply shortfall | Strategic petroleum reserves |

| LNG buyers (Europe, Asia) | Very High | Hormuz transit disruption | Spot market + alternative suppliers |

| Fertiliser-dependent agriculture | High | Gas feedstock price surge | Forward contracts, stockpiling |

| Shipping and marine insurance | High | War risk premium escalation | War risk clauses, route diversification |

| Petrochemicals | Moderate-High | Feedstock cost inflation | Contract renegotiation |

| Renewable energy developers | Low-Moderate | Indirect capital diversion | Long-term policy frameworks |

Ceasefire Fragility and the Triggers That Matter

The ceasefire reached in early April operates without a formal peace framework, without verified disarmament commitments, and without internationally monitored compliance mechanisms. Both sides continue to issue maximalist rhetoric even as diplomatic engagement continues. According to reporting on the ceasefire status, Iran warns new US-Israeli strikes will broaden war beyond the current theatre — a signal that has not been adequately priced into market consensus. Four specific triggers could cause the ceasefire to unravel:

- A new US or Israeli strike on Iranian territory or Iranian-linked assets

- Breakdown of Pakistan-mediated nuclear negotiations without a framework agreement

- Iran perceiving that GCC states have withdrawn diplomatic protection and acquiesced to renewed Western military action

- Domestic political pressures in the US or Israel demanding demonstrable military resolve within short political timeframes

Conversely, three conditions would meaningfully increase the ceasefire's durability:

- A verifiable interim nuclear agreement freezing Iranian enrichment capacity in exchange for partial sanctions relief

- Formal GCC security guarantees backed by explicit US commitments to refrain from unilateral military action

- Gradual reopening of the Strait of Hormuz under a multilateral maritime governance framework that incorporates elements of the PGSA structure as a face-saving mechanism for Tehran

Final Analytical Note: The most underpriced risk in current commodity market positioning is not whether a diplomatic deal ultimately gets done. It is whether the ceasefire can survive the domestic political pressures on both sides long enough for diplomacy to produce an actionable framework. That survival window is measured in weeks, not months.

The Three Outcomes Defining the Next Quarter

Global commodity markets, energy importers, and institutional investors are now navigating a scenario space defined by three distinct resolution pathways:

- Diplomatic breakthrough: A nuclear framework agreement formalises the ceasefire and enables gradual Hormuz reopening. Commodity prices stabilise and begin a controlled retracement from current elevated levels.

- Frozen conflict: Negotiations stall but neither side escalates. Commodity markets remain structurally elevated with persistent geopolitical risk premiums embedded in crude and LNG pricing. Strategic stockpiling accelerates across Europe and Asia.

- Renewed escalation: A new strike triggers Iranian retaliation beyond the Gulf region. Global energy markets enter a supply shock regime with Brent potentially discovering price above $140 to $150 per barrel and LNG force majeure risk becoming a live commercial issue across multiple supply contracts.

The current market consensus appears to assign low probability to Scenario 3 — but that assessment deserves scrutiny. Iran has explicitly stated its forces held capabilities in reserve during the initial conflict phase. Any pricing model that discounts this signal entirely is not adequately reflecting the full escalation distribution.

This article contains forward-looking analysis, scenario projections, and commodity price assessments that involve inherent uncertainty. Nothing in this article should be construed as financial or investment advice. Commodity price ranges cited represent analytical scenarios, not forecasts. Readers are encouraged to consult independent financial and commodity market advisors before making any investment decisions.

Want to Stay Ahead of the Next Major Commodity Discovery?

While geopolitical shocks reprice energy markets in real time, Discovery Alert's proprietary Discovery IQ model continuously scans ASX announcements to deliver instant alerts on significant mineral discoveries — from gold and copper to the critical commodities most exposed to supply chain disruption. Explore historic examples of major discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to ensure you're positioned ahead of the market when the next transformative announcement hits.