July 18, 2026

When a Narrow Waterway Holds the World Hostage

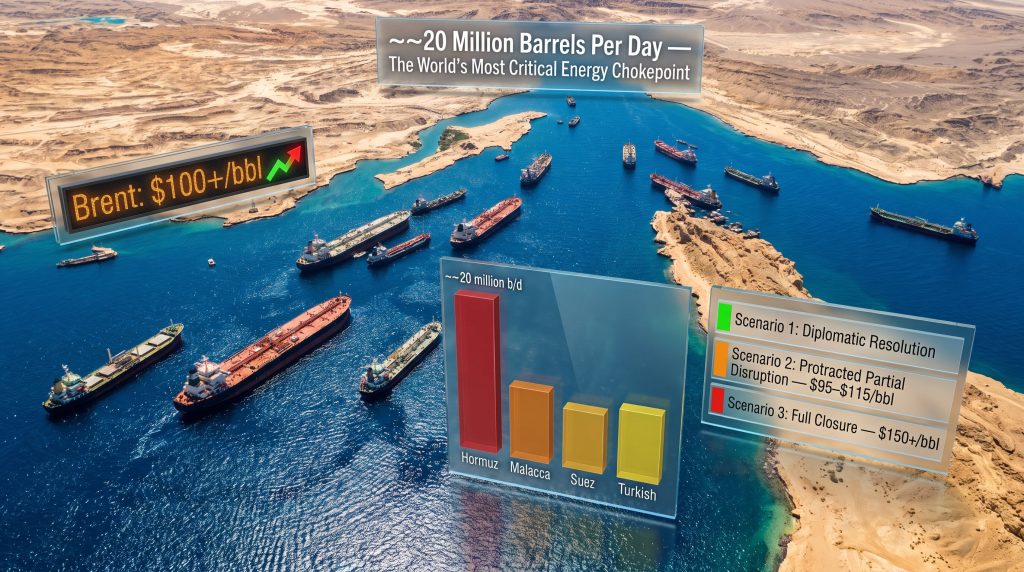

Every few decades, global energy markets are reminded of a fundamental structural weakness: the overwhelming concentration of supply flows through a handful of maritime passages. No chokepoint illustrates this vulnerability more starkly than the Strait of Hormuz oil supply disruption. Stretching just 33 kilometres at its narrowest point between the Iranian coastline and the Omani peninsula, this sliver of water connects the Persian Gulf to the Gulf of Oman and, by extension, to every major energy-consuming economy on earth.

Before hostilities reshaped global shipping in 2026, approximately 20 million barrels of oil per day transited the strait, representing roughly one-fifth of total global oil supply. Qatar, the world's largest LNG exporter, routes every cubic metre of its seaborne gas through this single corridor. The arithmetic of dependency is therefore straightforward, and the strategic question it raises is equally unambiguous: what happens to the global economy when a passage carrying this volume of energy effectively closes?

The answer, now playing out in real time, is more complicated and in some respects more counterintuitive than most analysts anticipated.

When big ASX news breaks, our subscribers know first

The Geometry of Hormuz: Why Is There No Meaningful Bypass?

Understanding why the Strait of Hormuz oil supply disruption carries such systemic weight requires understanding what alternatives do and do not exist. Two partial bypass pipelines serve the region: Saudi Arabia's East-West Pipeline and the Abu Dhabi Crude Oil Pipeline (ADCOP). Both offer relief at the margins, but neither comes close to substituting for full strait throughput, and neither handles LNG.

A comparison of the world's major maritime energy chokepoints illustrates the unique severity of Hormuz's structural position:

| Chokepoint | Daily Oil Flow (Pre-Crisis) | Alternative Route Available? | Strategic Risk Level |

|---|---|---|---|

| Strait of Hormuz | ~20 million b/d | Extremely limited | Critical |

| Strait of Malacca | ~16 million b/d | Partial (longer routes) | High |

| Suez Canal / Bab el-Mandeb | ~9 million b/d | Cape of Good Hope | Elevated |

| Turkish Straits | ~3 million b/d | Partial pipeline options | Moderate |

Even when partial rerouting is theoretically possible, the practical consequences are severe. Alternative routing around the Arabian Peninsula adds two to three weeks of additional transit time and substantially higher freight costs — constraints that compress refinery scheduling windows and push up delivered prices across Asian markets simultaneously. Furthermore, as explored in crude oil geopolitics, these structural chokepoints have long been identified as systemic risk factors embedded in global supply pricing.

How the 2026 Conflict Escalated Into a Maritime Crisis

The sequence of events that produced the current disruption began with coordinated US-Israeli strikes on Iranian territory in late February 2026. Iran's response was not a conventional military counter-strike but an asymmetric maritime campaign, deploying Islamic Revolutionary Guard Corps (IRGC) attack boats, drone strikes, and missile systems against commercial vessels attempting to transit the strait.

Shipping traffic collapsed in stages. Following a brief partial resumption, July 2026 saw hostilities reignite and tanker transits fall to below 10% of pre-war baseline volumes. The IEA has characterised the resulting disruption as the largest oil supply shock in recorded energy market history, exceeding both the 1973 Arab Oil Embargo and the 1990 Gulf War shock in combined volume and duration.

According to analysis from the Brookings Institution, the Hormuz corridor's structural importance to global markets means even partial closures create disproportionate downstream consequences across both physical supply and financial derivatives markets.

"The scale of the current disruption has no modern parallel. Over 1,000 vessels are stranded in the Persian Gulf, and approximately 20,000 seafarers from across the globe remain unable to exit the region through normal channels."

A lesser-known dimension of the crisis is the IRGC's informal toll enforcement mechanism. A small number of vessels have reportedly secured passage through payments made to Iranian naval forces outside formal maritime law, creating a parallel shadow shipping corridor that operates at elevated cost and under extreme legal ambiguity.

The current disruption metrics paint a stark picture:

| Disruption Metric | Status (July 2026) |

|---|---|

| Estimated daily supply loss | 10.1 to 14 million barrels per day |

| Shipping traffic vs. pre-war baseline | Below 10% of normal volume |

| Vessels stranded in the Persian Gulf | Over 1,000 ships |

| Stranded seafarers | Approximately 20,000 personnel |

| Brent crude price | Surged past $100/barrel |

| IEA strategic reserve release | 400 million barrels (largest in history) |

The Demand Destruction Paradox: Why Haven't Prices Spiked Higher?

One of the most analytically striking features of the current crisis is the muted price response relative to the physical supply loss. With Brent trading in the high $80s to low $90s per barrel at the time of writing — rather than at the $130 to $150 range that historical disruption models would project — markets appear to be pricing in a concurrent and equally powerful demand-side shock.

The explanation centres on China. Chinese crude imports collapsed 41% year-on-year in June 2026, falling to just 7.12 million barrels per day, the weakest monthly reading since October 2016. Chinese refinery runs simultaneously dropped toward pandemic-era lows. The world's largest oil importing nation effectively withdrew from the spot market at precisely the moment when Gulf supply became structurally unavailable.

This creates a demand-supply gap dynamic that defies simple modelling. However, the underlying oil market volatility remains significant, as the oil market volatility generated by geopolitical friction continues to suppress long-term investment certainty across the sector:

- A physical supply shortfall of 10 to 14 million barrels per day relative to pre-crisis production capacity

- A simultaneous demand collapse of several million barrels per day from China alone

- A strategic reserve release of 400 million barrels from IEA member states adding approximately 2.5 to 3 million barrels per day of buffer supply

- Demand destruction signals from other Asian economies rationing consumption in response to high spot prices

The net result is a price level that appears paradoxically orderly, but which analysts warn is masking enormous underlying physical stress.

Brent Backwardation and What the Futures Curve Is Telling Us

A critical technical signal that headline prices obscure is the behaviour of the Brent futures curve. Brent futures have flipped into backwardation, meaning near-term contracts trade at a premium to longer-dated ones. In energy markets, this structure indicates that physical barrels are immediately scarce, with buyers willing to pay a significant premium for prompt delivery over future supply.

Backwardation typically precedes sustained price rallies as above-ground inventory buffers are drawn down. The futures market is, in effect, signalling that the physical stress is real and intensifying, even if the headline price has been partially suppressed by demand destruction.

How Long Can Strategic Petroleum Reserves Hold the Line?

The IEA's coordinated release of 400 million barrels — the largest in the organisation's history — has provided a critical buffer. However, at current drawdown rates, analysts project that SPR capacity across member states could reach critical depletion levels by July to August 2026. Beyond that point, no equivalent buffer mechanism exists.

IEA Executive Director Fatih Birol has communicated publicly that the global economy faces serious structural damage unless the Strait of Hormuz reopens within weeks rather than months. The window for preventing a deeper economic shock is narrowing rapidly.

A residual shortfall of approximately 9 million barrels per day relative to pre-crisis demand levels would remain even after accounting for demand destruction, with no SPR capacity left to absorb it. The IEA's detailed assessment of how global supply has attempted to readjust reinforces the scale of the structural gap that remains unbridged.

Which Nations Face the Greatest Exposure?

Asian economies collectively represent the largest block of Hormuz-dependent oil and LNG importers. Their exposure varies by degree, but the overall picture is one of widespread structural vulnerability:

| Country | Gulf Import Dependency | Key Vulnerability |

|---|---|---|

| Pakistan | Very High | LNG supply from Qatar; spot market reliance |

| India | High | Crude oil imports; 15,000+ seafarers stranded |

| Japan | High | LNG supply; Hormuz declared effectively off-limits |

| South Korea | High | Pivoting to Red Sea routing alternatives |

| China | Moderate to High | Collapsed imports; seeking non-Gulf LNG deals |

Pakistan: Emergency Procurement at Historic Premiums

Pakistan's structural exposure to the crisis is among the most acute globally. State-owned Pakistan LNG awarded PetroChina a prompt cargo for July 21 to 22 delivery at $20.7 per MMBtu, the highest spot LNG price paid by Pakistan in four years. This reflects the near-total disruption of Qatari LNG flows, which transit Hormuz without any alternative routing option.

Pakistan's vulnerability is compounded by limited domestic gas production, negligible strategic reserves, and constrained foreign currency reserves that restrict its ability to participate repeatedly in elevated spot markets. Each additional emergency procurement at crisis-level prices tightens fiscal conditions further. In this context, disruptions to global LNG supply are translating directly into sovereign fiscal stress for import-dependent economies.

India: Seafarer Crisis and Domestic Supply Protection

India has issued a formal advisory barring the deployment of Indian maritime workers on vessels transiting the strait, following crew fatalities in regional attacks. More than 15,000 Indian seafarers are estimated to remain stranded west of the strait, creating a significant humanitarian and logistical crisis for the world's largest maritime workforce supplier.

On the domestic supply side, New Delhi moved to protect fuel availability by nearly doubling export taxes on diesel to 15.5 rupees per litre and on jet fuel to 14.5 rupees per litre. The measure reflects an unusual policy tension: India's refining sector is simultaneously experiencing strong export margins that incentivise shipping fuel abroad, while domestic supply security demands those barrels remain available locally.

This dynamic positions India as an emerging swing supplier in global fuel markets, a structural shift with significant long-term implications. With Ukrainian strikes estimated to have knocked out up to 40% of Russian refining capacity through July and August 2026, Russia's major oil companies have approached Indian refiners for gasoline supply, inverting the countries' conventional energy trade relationship.

Japan, South Korea, and China: Structural Rerouting Begins

Japan's trade ministry has taken the position that Hormuz transits are effectively off-limits for the foreseeable future, triggering emergency supply diversification planning across the country's LNG import portfolio. South Korea is actively exploring Red Sea routing as an alternative, accepting meaningfully longer transit times and elevated freight costs.

China's strategic response contains a less widely observed detail: the first US LNG cargo to arrive at a Chinese terminal since February 2025 docked at Hainan in bonded storage status. This classification allows the cargo to be held, traded, or re-exported without clearing Chinese customs, enabling Beijing to sidestep its own 15% tariff on US LNG while maintaining strategic optionality. It is a technically elegant workaround that reveals the sophistication of China's commodity trade infrastructure under geopolitical pressure.

Commodity Contagion: The Nickel and LNG Ripple Effects

The Strait of Hormuz oil supply disruption is not confined to crude oil and LNG. A largely underappreciated secondary impact is cascading through industrial commodity chains.

Nickel: The Sulphur Supply Chain

Indonesia, the world's largest nickel producer, sources approximately 75% of its sulphur inputs from the Gulf region. Sulphur is a critical processing input for nickel hydrometallurgical operations, and its disruption directly threatens Indonesian output capacity. Nickel prices surged to a three-week high above $17,000 per tonne in July 2026, with processing cost increases of approximately $10,000 per tonne reported across affected operations.

The strategic significance extends beyond nickel itself. Indonesian nickel supply underpins global battery supply chains for electric vehicles, meaning a protracted Hormuz disruption could indirectly constrain the energy transition supply chain even as it devastates conventional energy markets.

Asian LNG Spot Market Volatility

Asian LNG spot prices jumped approximately 10% as Hormuz supply fears reignited, reflecting the structural single-point-of-failure created by Qatar's total dependence on strait access. Qatar accounts for roughly 20% of global LNG supply, and every cubic metre of its seaborne exports transits Hormuz without exception. For markets structured around Qatari baseload supply, there is no short-term substitute. In addition, the broader pressure on critical minerals demand from supply chain disruptions is compounding the investment case for non-Gulf sourcing alternatives.

The next major ASX story will hit our subscribers first

Corporate Strategy Under Crisis: Iraq as the Hormuz Exit Play

The crisis is reshaping corporate strategy across the oil sector. US major ConocoPhillips has agreed to acquire a 42% stake in BP's northern Iraq venture, targeting four producing fields with over 3 billion barrels of combined resources. The strategic logic extends beyond resource acquisition: northern Iraqi production, if routed through Turkey rather than the Gulf, represents a genuine Hormuz-bypass production asset.

Simultaneously, discussions around reviving an Iraq-Syria pipeline corridor as an alternative routing mechanism have gained traction, with US diplomatic involvement noted in the conceptual framing. Feasibility constraints remain substantial, including Syrian political instability and infrastructure rehabilitation costs, but the strategic impetus behind such alternatives has never been stronger.

The Basra terminal drone incident, which briefly suspended Iraqi crude loadings before operations resumed without confirmed damage, and the Khor Mor gas field shutdown that cut 2.5 GW of power supply to Kurdistan, illustrate that even Gulf production assets not directly within the strait face escalating security risk.

Three Scenarios for Resolution

Investors and policymakers are increasingly applying scenario frameworks to assess the range of outcomes:

Scenario 1: Rapid Diplomatic Resolution (Low Probability)

- Preconditions: US-Iran ceasefire within 2 to 4 weeks; IRGC withdrawal from maritime enforcement

- Market outcome: Oil prices retreat from $100-plus levels; LNG spot premiums normalise; Asian import markets restabilise

- Assessment: Low probability given the current apparent abandonment of diplomatic channels by both parties

Scenario 2: Protracted Partial Disruption (Moderate Probability)

- Preconditions: Sporadic exchanges continue; limited shipping resumes under high-risk war premiums; IRGC toll system expands

- Market outcome: Oil prices stabilise in the $95 to $115 range; LNG markets remain elevated; SPR reserves reach critical depletion by August

- Assessment: Reflects the current trajectory most closely

Scenario 3: Full Closure Including Bab el-Mandeb (Low Probability, Catastrophic Impact)

- Preconditions: Iran directs Houthi forces to seal the Bab el-Mandeb strait; reports that Iran has instructed Yemeni Houthi forces to prepare for Red Sea shipping attacks add non-trivial weight to this scenario

- Market outcome: Oil prices potentially exceeding $150 per barrel; global recession risk elevated; food and fertiliser supply chains severely disrupted

- Assessment: Low but not negligible probability; piracy incidents in the Gulf of Aden add further instability signals

The Long Arc: Structural Shifts in Global Energy Architecture

Whatever the near-term resolution, the Strait of Hormuz oil supply disruption of 2026 is accelerating structural changes in global energy security architecture that were already underway. Asian import markets are compressing their timelines for supply diversification, moving from aspirational multi-year plans to emergency near-term contracting with non-Gulf producers spanning the United States, Australia, and Africa.

The SPR framework itself faces a credibility test. Designed to manage disruptions measured in weeks, not months, the IEA reserve system is being stress-tested against a shock that may persist well beyond its operational design parameters. The policy debate about whether to expand SPR capacity, diversify reserve locations geographically, or accelerate demand-side resilience through electrification and efficiency investment is no longer academic.

Jeff Currie, a prominent commodities strategist, has articulated the view that the longstanding narrative of oil abundance has definitively broken down — a perspective that the current crisis appears to be validating in real time. The illusion of elastic supply, maintained through a combination of US shale growth and Gulf spare capacity, is being stripped away by a crisis that has simultaneously disrupted the world's most concentrated supply corridor and revealed the limits of strategic reserve buffers.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario projections, and price estimates involve significant uncertainty and should not be relied upon as predictive of future market outcomes. Readers should conduct independent research and consult qualified financial advisers before making investment decisions.

Could the Hormuz Crisis Signal the Next Major Resource Discovery Opportunity?

The structural shifts now reshaping global energy security — from supply chain vulnerabilities to accelerating demand for non-Gulf commodities — are creating a new landscape for mineral discovery investment. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into actionable insights the moment they are announced; explore historic examples of exceptional returns driven by major discoveries, and begin a 14-day free trial to position ahead of the market.