May 13, 2026

The Invisible Bottleneck: How One Waterway Controls the World's Energy Pulse

Every major energy crisis in modern history traces back to a single, recurring vulnerability: the assumption that global oil and gas markets can absorb supply shocks without systemic disruption. For decades, that assumption has been quietly underwritten by the uninterrupted flow of hydrocarbons through a narrow corridor of water connecting the Persian Gulf to the open ocean. When Iran expands Strait of Hormuz operational area claims beyond anything previously articulated, the underlying fragility of that assumption becomes impossible to ignore.

The geography has not changed. The vulnerability has always been there. What has changed is the doctrine surrounding it.

When big ASX news breaks, our subscribers know first

Why This Waterway Has No Substitute

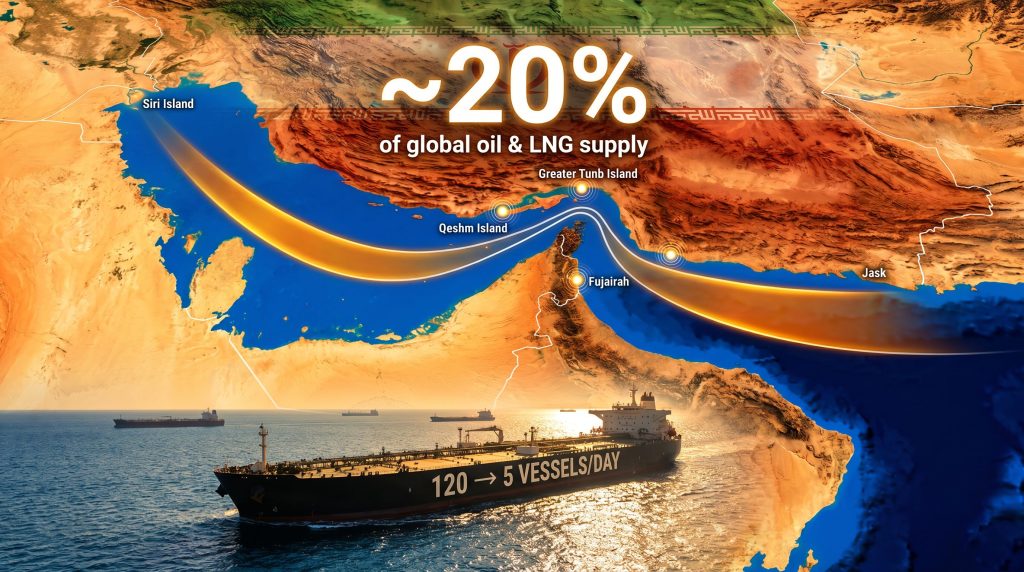

The Strait of Hormuz functions as the circulatory valve of the global energy system. According to the U.S. Energy Information Administration, approximately 20 to 21% of globally traded petroleum transits through this corridor, alongside a substantial proportion of the world's liquefied natural gas exports. No equivalent volume of hydrocarbon supply can be redirected through any alternative route within a commercially meaningful timeframe.

Saudi Arabia operates the East-West Pipeline, which connects its eastern oil fields to Red Sea export terminals, but this pipeline operates near capacity and cannot absorb the full volume currently routed through the strait. The UAE's Abu Dhabi Crude Oil Pipeline (ADCOP), completed in 2012, provides a partial bypass to the Gulf of Oman but handles only a fraction of total UAE export volumes. For Iraq, Kuwait, Qatar, and Bahrain, no viable alternative exists at all.

The physical geography reinforces the problem. The navigable shipping lane through the strait spans approximately 21 miles at its narrowest point, with the International Maritime Organization's Traffic Separation Scheme designating directional lanes of roughly two miles each for inbound and outbound tanker traffic, separated by a buffer zone. This means that millions of barrels of oil daily are funnelled through a passage that, at its most constrained, offers ships roughly the same manoeuvrability as a major urban highway.

The LNG Dimension That Most Analysts Underestimate

Crude oil disruptions attract the most attention in energy markets, but the LNG vulnerability embedded in the strait's geography is arguably more acute in structural terms. Qatar, the world's largest LNG exporter, routes virtually its entire export volume through the Strait of Hormuz. Furthermore, unlike crude oil, LNG cannot be economically rerouted via pipeline to alternative markets. It requires purpose-built liquefaction terminals, specialised tankers, and regasification infrastructure at destination ports. The LNG supply outlook for affected nations makes this vulnerability especially pressing.

Nations that diversified their gas supply away from Russian pipeline flows following the 2022 energy crisis specifically toward Qatari LNG now face a second distinct supply vulnerability concentrated in the same geographic point. European and Asian importers, particularly Japan, South Korea, and economies across South and Southeast Asia, have limited short-term substitution capacity if Qatari LNG shipments are interrupted.

The LNG risk embedded in any Hormuz disruption is structurally different from crude oil risk. Crude oil markets have spare capacity elsewhere; LNG supply chains are geographically locked, and switching between suppliers takes months, not days.

Iran Expands Strait of Hormuz Operational Area: The Doctrine Behind the Declaration

On May 13, 2026, Mohammad Akbarzadeh, deputy political director of the IRGC Navy, made a formal statement through the state-affiliated Fars news agency that redefined the strategic parameters of the strait entirely. As reported by the IRGC, Akbarzadeh indicated that Iran's previous conception of the strait as a limited zone centred on islands such as Hormuz and Hengam had been fundamentally superseded by a new operational framework of substantially greater geographic scope.

The declaration was not a territorial claim in the conventional legal sense. It was an assertion of operational control. Iran defined the strait as a strategic zone stretching from Jask on the eastern coastline to Siri Island in the west, with state-affiliated media outlets Fars and Tasnim reporting that the operational width had expanded from the traditionally accepted 20 to 30 miles to a claimed 200 to 300 miles, or approximately 500 kilometres of maritime space. Tasnim specifically characterised the expanded zone as forming a complete crescent shape across the northern approaches to the Persian Gulf.

This announcement represented the second formal expansion within a nine-day period.

The Two-Stage Escalation: May 4 and May 13, 2026

The sequential nature of these declarations is analytically significant. A single announcement could be interpreted as a reactive posture triggered by specific events. Two announcements within nine days, each progressively larger in geographic scope, suggest a deliberate, staged escalation strategy with each declaration testing international response before the next threshold is crossed.

| Declaration | Date | Geographic Scope | Key Boundary Points |

|---|---|---|---|

| First Expansion | May 4, 2026 | UAE Gulf of Oman coastline | Mount Mobarak and Fujairah (east) to Qeshm Island and Umm al Quwain (west) |

| Second Expansion | May 13, 2026 | 200-300 mile operational corridor | Jask/Sirik (east) to Siri Island (west), crescent formation |

The May 4 declaration was notable in its own right because it incorporated areas internationally recognised as UAE territorial waters. The emirates of Fujairah and Umm al Quwain were both referenced within the declared zone boundary, representing a direct challenge to the territorial sovereignty of a third-party state not directly involved in the underlying conflict. Consequently, this oil market disruption has reverberated well beyond the immediate conflict parties.

The Geographic Anchors and Their Military Significance

Understanding the crescent formation requires understanding the strategic value of each anchor point:

-

Jask and Sirik (eastern anchor): Located approximately 340 kilometres southeast of the strait proper, Jask serves as Iran's primary deepwater crude export terminal on the Gulf of Oman. Establishing it as the eastern boundary of the operational zone extends Iranian military reach far beyond the strait itself into open ocean approaches.

-

Siri Island (western anchor): An Iranian oil export terminal positioned in the central Persian Gulf, approximately 80 kilometres northwest of the strait entrance. Its inclusion as the western boundary draws the operational zone deep into Gulf waters.

-

Qeshm Island (central node): The largest island in the Persian Gulf, Qeshm hosts an established IRGC naval base and sits directly within the narrowest section of the strait's navigable channel.

-

Greater Tunb Island (northern flank): A disputed territory claimed by both Iran and the UAE, Greater Tunb functions as a forward surveillance and positioning point commanding the northern approaches.

-

Fujairah (southern reference): A major UAE bunkering hub and oil export terminal. Its incorporation into the declared zone carries significant implications for shipping operations that currently use Fujairah as a fuel and logistics staging point outside the traditional strait boundary.

The Conflict Timeline That Triggered the Escalation

The zone expansions did not emerge in isolation. They represent the latest phase of a conflict that began reshaping Persian Gulf maritime dynamics from late February 2026 onward.

| Period | Development | Maritime Consequence |

|---|---|---|

| February 28, 2026 | US and Israeli military operations against Iran commence | Immediate collapse in commercial vessel traffic |

| Early March 2026 | Daily transits fall from approximately 120 ships to around 5 | Near-total shutdown of commercial passage |

| March to April 2026 | At least 21 confirmed attacks on commercial vessels reported | 7 seafarers killed, 1 port worker killed |

| April 2026 | Temporary ceasefire-linked passage permitted | Limited civilian vessel movement resumes |

| Post-ceasefire | Continued US naval presence maintained in the region | Iran reverses reopening decision |

| May 4, 2026 | First formal zone expansion declared | UAE coastline incorporated into Iranian control map |

| May 13, 2026 | Second, broader expansion announced | 200-300 mile operational corridor formalised |

The human cost embedded within this timeline deserves more attention than it typically receives in energy market analysis. Over 20,000 seafarers were reported stranded within the Persian Gulf during peak disruption. Commercial shipping insurance premiums for Persian Gulf war-risk coverage surged dramatically as underwriters repriced the risk environment in real time. Port operations across multiple Gulf states experienced severe disruption, creating cascading supply chain effects extending well beyond the energy sector.

The Permission-Based Waterway: How Selective Access Reshapes Geopolitics

One of the most structurally consequential aspects of Iran's new operational doctrine is the introduction of a two-tier maritime access model. IRGC officials stated that sanctioned passage through the redefined zone would be limited to corridors specifically designated by Iranian naval authority, with vessels deviating from mandated routes facing what officials described as decisive responses.

Critically, access has not been denied uniformly. Vessels from non-aligned nations, and those with reported affiliations to China and India, have been permitted transit. Western-affiliated shipping has faced conditions functionally equivalent to a blockade. The broader oil geopolitics analysis surrounding this selective access framework reveals how profoundly it complicates existing alliance structures.

This creates a geopolitical fracture with no clear historical precedent in modern maritime law:

-

Nations that maintain non-aligned or accommodating relations with Iran retain energy supply continuity.

-

Nations aligned with Western-led sanctions regimes or military postures face effective exclusion from the world's most consequential energy corridor.

-

Trading nations positioned between these poles, particularly India, face complex choices between energy security and geopolitical alignment.

The selective access framework is not a military posture in the conventional sense. It is an instrument of economic coercion dressed in the language of maritime security, and its long-term implications for the architecture of global trade may outlast the immediate conflict.

How This Compares to Historical Hormuz Disruptions

Iran has threatened to close the strait on numerous occasions since the 1979 Islamic Revolution, but enforcement has historically been episodic rather than systematic. The current escalation differs from prior episodes in structural ways that matter for assessing its durability.

| Period | Nature of Threat | Enforcement Level | Resolution Mechanism |

|---|---|---|---|

| 1980-1988 Tanker War | Iraqi and Iranian tanker attacks | Significant but partial | US convoy operations, eventual ceasefire |

| 1987-1988 Operation Earnest Will | Direct attacks on convoys | Partially deterred by US presence | Diplomatic resolution post-ceasefire |

| 2019 Tanker Seizures | Iranian seizure of UK-flagged vessel | Isolated incidents | Diplomatic negotiations, gradual de-escalation |

| 2026 Current Escalation | Formal zone redefinition, active interdiction | Near-total traffic collapse at peak | Unresolved; ongoing as of May 2026 |

What distinguishes the 2026 escalation from the Tanker War era is the formalisation of the control claim. During the 1980s, attacks were tactical and attributable to wartime conditions. The current framework involves the formal, publicly announced redefinition of geographic boundaries, the sequential publication of control maps, and the explicit creation of a permission-based access system. This moves the dispute from the domain of active conflict into the domain of asserted territorial doctrine, which is considerably more difficult to reverse through short-term diplomatic intervention. As detailed by The War Zone, the IRGC's claims represent an unprecedented assertion of maritime control.

The next major ASX story will hit our subscribers first

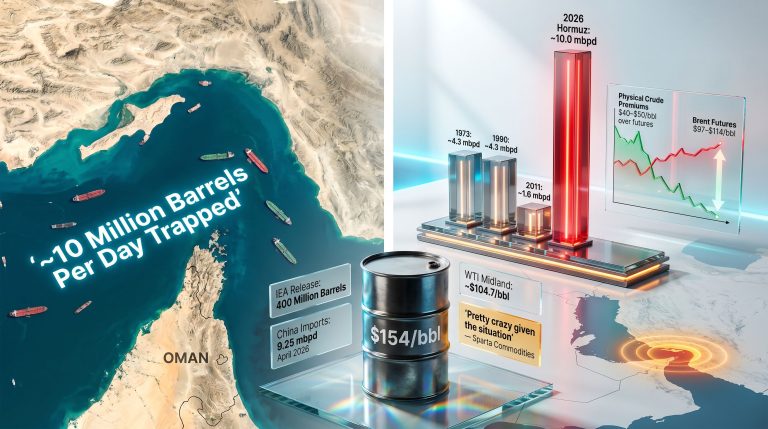

Energy Market Scenarios: What Disruption Levels Mean for Oil Prices

The range of potential outcomes carries materially different implications for global energy prices. An oil price shock of this magnitude has few modern precedents, and the following scenarios are analytical frameworks based on historical disruption precedents and should be treated as indicative ranges rather than forecasts.

| Scenario | Probability Assessment | Estimated Price Impact |

|---|---|---|

| Partial enforcement, selective interdiction | Moderate | Short-term spike of approximately $15-25 per barrel |

| Full closure to Western-affiliated shipping | Lower but non-trivial | Sustained increase of approximately $40-60 per barrel |

| Negotiated corridor reopening | Contingent on diplomatic progress | Price normalisation over 4-8 weeks |

| Direct naval confrontation between major powers | Low probability, high consequence | Extreme volatility, potential supply shock exceeding prior estimates |

These figures are analytical scenarios only. Actual price movements depend on the duration of disruption, spare capacity responses from producers outside the Gulf, and strategic petroleum reserve release decisions by major consuming nations.

The Ripple Effects: GCC States, Asian Importers, and Western Naval Powers

Gulf Cooperation Council States

The GCC members including Saudi Arabia, the UAE, Qatar, Kuwait, and Bahrain collectively depend on the strait as their primary hydrocarbon export corridor. The incorporation of UAE coastline territory into Iran's declared operational zone introduces a direct sovereignty dimension that places GCC governments in an acutely difficult strategic position. Escalation risks supply continuity; accommodation risks normalising Iranian territorial assertions over internationally recognised waters. In addition, OPEC's market influence becomes increasingly constrained when the export infrastructure of multiple member states is subject to external interdiction.

Asian Energy Importers

Japan and South Korea face the most acute near-term LNG exposure among major Asian importers, given their heavy dependency on Qatari supplies and limited short-term alternative supply options. India's reported inclusion among nations granted selective transit access positions it in a complex dual role: a beneficiary of the current enforcement framework, but simultaneously a participant in a system that fractures the international maritime order.

China's position as another selective access beneficiary reinforces its energy security calculus around strategic reserve management and long-term supply diversification, but it also implicates Beijing in a framework that subordinates international maritime law to bilateral geopolitical relationships.

The Insurance Market as a Real-Time Risk Barometer

War-risk insurance premiums for Persian Gulf transits function as one of the most sensitive real-time indicators of geopolitical stress in the energy complex. During the 1980s Tanker War, war-risk premiums surged from historical norms of approximately 0.1 to 0.3% of cargo value to levels exceeding 1% per voyage. The current disruption has similarly triggered significant premium escalation, effectively embedding a geopolitical risk premium into the cost of every barrel that originates from Gulf producers, irrespective of whether specific vessels are interdicted.

This premium increase functions as a de facto tax on global energy consumption, distributed unevenly across importing nations according to their shipping cost exposure and contractual structures.

What Resolution Actually Requires

The diplomatic pathway back to normalised transit faces constraints that did not apply during prior Hormuz crises. Historical de-escalations were achieved when the underlying conflict driving Iranian assertiveness reached a negotiated pause. The 2026 escalation, however, involves the formal declaration of expanded Iranian control doctrine, not merely tactical military actions. Reversing a formally declared operational zone requires either a comprehensive diplomatic settlement or a credible military deterrent sufficient to make enforcement costs prohibitive.

Neither condition appears imminent based on the trajectory documented through May 2026. The sequential zone expansions, the formality of the declarations, and the explicit incorporation of UAE territorial waters into the control framework all suggest a strategic entrenchment rather than a posture designed for rapid reversal.

For global energy markets, supply chains, and maritime insurers, the baseline scenario is sustained disruption until a fundamental change in the US-Iran-Israel strategic equation produces conditions that make a comprehensive diplomatic resolution achievable. The arithmetic of global energy dependency on a single waterway has not changed. What has changed is the confidence with which that waterway can be assumed to remain open. Iran expands Strait of Hormuz operational area claims in ways that challenge every prior assumption about how this critical corridor has functioned within the international order.

Disclaimer: Price impact estimates and scenario analyses presented in this article are indicative frameworks based on historical energy market precedents and publicly available geopolitical reporting. They do not constitute financial advice or investment recommendations. Readers should consult qualified financial and geopolitical risk advisers before making decisions based on the evolving situation in the Strait of Hormuz.

Want to Stay Ahead of the Next Major Energy-Driven Market Shift?

When geopolitical disruptions reshape global commodity markets, the investors who act first on significant ASX mineral discoveries gain the greatest advantage — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those discoveries are announced, turning complex market signals into clear, actionable opportunities. Explore how historic mineral discoveries have generated substantial returns, and start your 14-day free trial today to position yourself ahead of the broader market.