July 28, 2026

When Announcements and Operations Diverge: Reading the Reopening of the Strait of Hormuz Correctly

Energy markets have a well-documented tendency to price political resolutions before the physical infrastructure that underpins them has actually been restored. The dynamic is not new. From the post-Gulf War mine-clearance operations of the early 1990s to the 2019 Abqaiq attack recovery, commodity markets have repeatedly front-run geopolitical announcements, only to reprice when operational reality diverges from diplomatic narrative.

The reopening of the Strait of Hormuz in June 2026 is following this same pattern with striking fidelity. Understanding the gap between what has been announced and what has actually changed is essential for anyone tracking global energy markets, Gulf economic trajectories, or Mexico's fiscal exposure to crude price volatility.

When big ASX news breaks, our subscribers know first

The Structural Weight the Strait Carries in Global Energy Trade

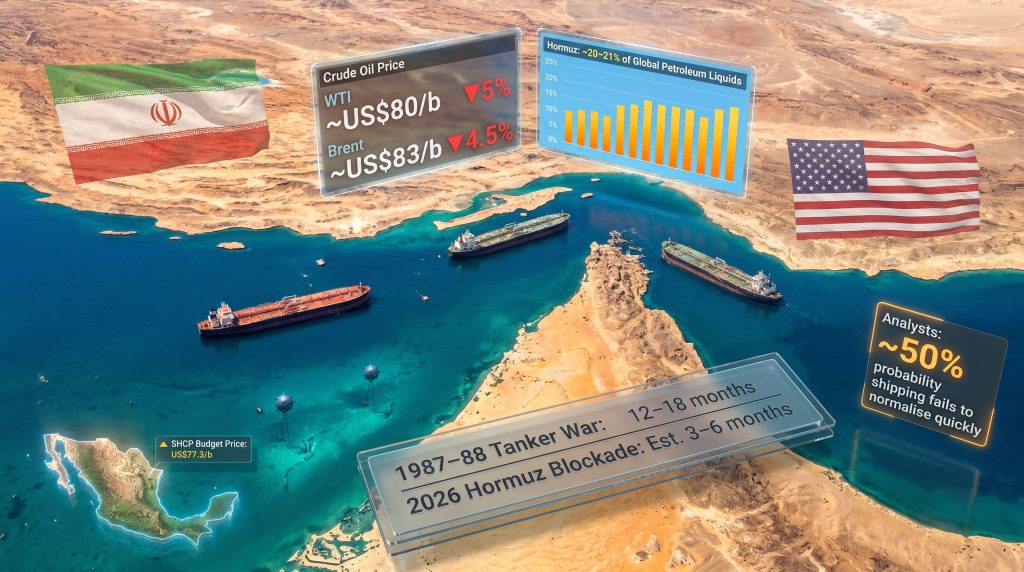

The Strait of Hormuz is approximately 33 kilometres wide at its narrowest navigable point, connecting the Persian Gulf to the Gulf of Oman. That geography, combined with the concentration of producing nations on its shores, means the waterway carries roughly 20 to 21% of global petroleum liquids annually. No pipeline network exists at sufficient scale to substitute for full Strait throughput in any short-to-medium timeframe, making it categorically different from other geopolitical chokepoints where alternative routing is at least partially viable.

The economies carrying the highest structural exposure are concentrated in Asia-Pacific: Japan, South Korea, India, and China all depend on Persian Gulf supplies transiting the Strait as a core component of their refining feedstock. European refiners face secondary exposure through LNG rerouting dynamics and Brent price benchmarking effects. Latin American producers, including Mexico, encounter the disruption primarily through benchmark price volatility and its direct impact on PEMEX export revenue and the domestic IEPS fuel subsidy mechanism.

Furthermore, the trade war impact on oil prices has added an additional layer of complexity to an already fragile supply picture, compressing the margin for error across global benchmarks.

A critical and often overlooked feature of Hormuz risk is that full closure is not required to trigger global price dislocation. Even a 20 to 30% throughput reduction is sufficient to reprice all major crude benchmarks, because the marginal barrel sets the global clearing price regardless of whether the majority of supply is still flowing.

What the US-Iran Agreement Actually Contains

The June 2026 agreement commits the US to lifting the naval blockade and reopening the Strait within 30 days of a signed memorandum of understanding. President Trump confirmed the agreement publicly, characterising the reopening as imminent upon MoU signature. That framing was subsequently contested by Iran, which reversed course after the US characterisation diverged from Tehran's interpretation of the deal's terms — a reversal pattern that mirrors the fragility of prior ceasefire announcements since February.

This is not the first announced breakthrough. The timeline of failed de-escalations since early 2026 establishes an important precedent:

- An initial ceasefire announcement in April that preceded a resumption of strikes.

- A brief de-escalation in late May that also failed to hold.

- The June 2026 formal agreement, which markets treated as materially more credible despite the reversal that followed US framing of the deal's terms.

The agreement's coverage, and its gaps, are best understood through the specific elements it does and does not address:

| Agreement Element | Current Status |

|---|---|

| Naval blockade suspension | Announced, contingent on MoU signing |

| Mine-clearance operations | Not yet commenced |

| Insurance underwriting restoration | Pending independent security confirmation |

| Fleet repositioning timelines | Estimated months, not weeks |

| Iran's interpretation of deal terms | Disputed following US public characterisation |

Commodity analysts at Sparta Commodities, led by Neil Crosby, have assigned approximately 50% probability to a scenario where Hormuz shipping fails to normalise quickly under current conditions. That is not a tail risk characterisation. It is a central scenario probability that warrants systematic positioning, not dismissal.

How Oil Markets Responded and Why the Pricing May Be Premature

WTI and Brent futures both registered sharp declines following the formal announcement, with WTI falling over 5% to approximately US$80 per barrel and Brent declining 4.5% to approximately US$83 per barrel — both reaching their lowest levels since early March. On the surface, this looks like a rational market pricing in restored supply. However, the more nuanced reading is considerably more cautious.

Both benchmarks remain more than 20% above pre-conflict levels, meaning the market has partially unwound the geopolitical risk premium without fully resolving the physical conditions that justified it. Sparta Commodities estimates an additional US$5 to US$10 per barrel downside on formal signing beyond the initial roughly US$5 per barrel knee-jerk drop, but this downside scenario is entirely conditional on physical normalisation proceeding on schedule.

The Sparta Commodities analysis identifies a particularly underappreciated risk: the US administration's persistent signalling of an imminent deal in the weeks preceding the formal announcement effectively suppressed prices below what underlying physical fundamentals justified. If the physical reopening stalls, this verbal suppression effect could unwind sharply, creating a snapback risk that short-positioned traders have not adequately priced into forward curves.

Even a partial recovery scenario — where ship traffic returns to approximately 50% of pre-conflict levels within 30 days — leaves significant supply uncertainty embedded in prices. Full normalisation requires three independent operational milestones, each capable of causing multi-week delays on its own. Monitoring current crude oil prices in the near term will be critical for assessing whether the market's optimism is justified or premature.

The Three Operational Barriers Markets Are Underweighting

Mine-Clearance: The Longest Lead-Time Constraint

Mine-sweeping operations in contested Gulf waters require coordinated naval assets, hydrographic survey vessels, and verified safe-passage corridor declarations. The historical precedent from post-Gulf War mine clearance operations in the early 1990s suggests full operational clearance of a contested waterway takes months, not weeks, even under cooperative conditions. A single uncleared mine incident after commercial traffic resumes would trigger immediate insurance withdrawal and fleet standdown, regardless of the political agreement's status.

Insurance Underwriting: The Commercial Gating Mechanism

War-risk insurance underwriters will not restore standard coverage until independent security assessments confirm mine-free corridors. Protection and Indemnity clubs — the mutual insurers that cover the vast majority of global tanker tonnage — represent the critical commercial gatekeepers. Their reinstatement of coverage is a prerequisite for major tanker operators to resume normal Gulf routing. Premium normalisation is expected to lag any political announcement by weeks to months, creating a practical bottleneck that no diplomatic press release can accelerate.

Fleet Repositioning: The Logistics Lag

Very Large Crude Carriers that repositioned to alternative routing or standby positions during the conflict require 7 to 14 days of transit time to return to operational Gulf loading positions. Port congestion at alternative loading terminals across the UAE and Saudi Arabia may have created scheduling backlogs that extend effective supply restoration timelines further, even after security conditions technically permit routing resumption. As Maersk has noted, reopening the Strait would have a more limited immediate impact on cargo flows than many market participants currently assume.

IMF's Assessment: Infrastructure Damage Is the Binding Constraint

IMF Managing Director Kristalina Georgieva welcomed the ceasefire announcement but explicitly cautioned that physical energy market recovery will require considerably more time than the announcement implies. Her assessment pointed to significant Gulf infrastructure damage as the primary constraint on rapid supply restoration — a characterisation that the IMF had not fully quantified as of mid-June 2026.

Five of the eight Gulf oil-exporting countries are projected to experience outright economic contractions in the current fiscal year, a figure that underscores the scale of structural damage the conflict has inflicted on the region's productive capacity.

| IMF Indicator | Current Assessment |

|---|---|

| Gulf oil exporters in contraction | 5 of 8 countries |

| Revised projections release date | July 8, 2026 |

| Prior scenario basis | April 2026 (pre-full escalation) |

| Infrastructure damage characterisation | Significant, not yet quantified |

The July 8 IMF release will be the first comprehensive post-conflict damage assessment and is expected to serve as the authoritative baseline for institutional investors and sovereign fiscal planners. The April scenarios issued before full conflict escalation are now considered analytically outdated.

The next major ASX story will hit our subscribers first

Mexico's Dual Exposure: Fiscal Headroom and Structural Vulnerability

Mexico's Finance Ministry revised its budget oil price assumption to US$77.3 per barrel, a figure that sits close to post-announcement price levels. At approximately US$80 per barrel, Mexico retains modest fiscal headroom above its budget assumption. A decline of US$5 to US$10 per barrel as physical normalisation proceeds would compress but not eliminate this buffer.

The fiscal exposure operates in both directions simultaneously through the IEPS fuel subsidy mechanism:

- Elevated prices above approximately US$77 per barrel generate roughly MX$2.5 billion per week in IEPS subsidy costs, directly weighing on the federal fiscal balance.

- Simultaneously, PEMEX export volumes are already running approximately 20% below the SHCP's annual target, meaning per-barrel revenue gains from elevated prices are partially offset by the volume shortfall.

The three scenarios Mexico's fiscal planners are navigating:

| Scenario | Oil Price Range | Fiscal Impact |

|---|---|---|

| Physical normalisation proceeds on schedule | US$70-75/b | IEPS relief; export revenue decline |

| Partial normalisation (50% traffic recovery) | US$78-83/b | Near-budget neutral; subsidy pressure continues |

| Normalisation stalls; prices snapback | US$88-95/b | Elevated subsidy burden; PEMEX revenue benefit partially offset by volume gap |

Mexico's fiscal planners have navigated versions of this volatility pattern at least three times since February 2026, giving the SHCP a practised, if uncomfortable, familiarity with the dual-edged nature of crude price movements for the Mexican sovereign balance sheet.

PEMEX's Compounding Structural Weaknesses

The Hormuz situation exposes PEMEX vulnerabilities that predate the current conflict. Active drilling rigs in Mexico fell 58% between January 2024 and January 2025, directly constraining near-term production recovery capacity. PEMEX recorded a MX$46 billion net loss in the first quarter of 2026, with capital expenditure cut by 51% in real terms, limiting the company's operational capacity to respond to any market opportunity the Strait reopening might create.

The oilfield services dynamic compounds this picture. SLB and Carso held close to US$1 billion in overdue PEMEX invoices as of mid-2025. SLB's decision to sign a long-term framework agreement with Venezuela's PDVSA on June 10, 2026 — covering exploration, field development, digital enablement, and workforce training — illustrates the direction in which global oilfield services capital is flowing. In addition, PDVSA policy shifts have made Venezuela an increasingly attractive destination for international capital, contrasting sharply with Mexico's payment-strained mixed contract model.

Against this backdrop, SENER and PEMEX announced a MX$93 billion (approximately US$5 billion) Comprehensive Reactivation Plan for petrochemicals and fertilisers spanning 2026 to 2030. The centrepiece is a MX$25 billion ammonia and urea plant in Poza Rica, Veracruz, targeting annual production of 708,000 tonnes of urea, with the objective of raising PEMEX's domestic urea market share from 19% to 84% by 2029.

Independent analysts note that the plan's execution credibility is materially undermined by PEMEX's Q1 2026 net loss, the 51% real-term capex cut, and the precedent established by the Olmeca refinery, which exceeded its original budget by approximately 100% and was delivered three years behind schedule. Downstream ambition without upstream financial stability has a documented track record of underdelivery in PEMEX's recent history.

Comparing 2026 to Historical Chokepoint Disruptions

| Event | Disruption Type | Physical Recovery Timeline | Price Impact Duration |

|---|---|---|---|

| 1987-1988 Tanker War | Mine and missile attacks | 12-18 months for full normalisation | Elevated risk premium 2+ years |

| 2019 Abqaiq Attack | Infrastructure strike | 6-8 weeks for production restoration | 2-3 week price spike |

| 2021 Suez Canal Blockage | Navigation obstruction | 6 days physical; weeks for backlog clearance | 2-3 week freight premium |

| 2026 Hormuz Blockade | Combined mine and naval blockade | Estimated 3-6 months for full normalisation | Ongoing, 20%+ above pre-conflict |

The 2026 situation is structurally more complex than any of these precedents. Unlike the Suez blockage, which involved a single vessel with no security threat dimension, the current situation involves active mine contamination, insurance market withdrawal, and a diplomatically fragile agreement subject to reversal on interpretation grounds. Unlike the 2019 Abqaiq attack, which had a clear single-infrastructure remediation path, the Hormuz situation requires multilateral security verification across an entire contested waterway before commercial shipping can resume at meaningful scale.

Key Indicators to Monitor for Physical Reopening Progress

For energy market participants tracking the reopening of the Strait of Hormuz, the following operational indicators carry more analytical weight than diplomatic announcements:

- Mine-clearance progress updates from US Navy and coalition naval assets operating in the Gulf, which represent the longest lead-time constraint on physical normalisation.

- War-risk insurance premium movements, which function as a leading indicator of commercial shipping confidence and P&I club underwriting appetite.

- VLCC fixture data, showing whether tanker operators are actually booking Gulf loading slots rather than simply awaiting conditions.

- Iran's public statements on deal interpretation, where any divergence from the US characterisation represents an early warning signal for reversal risk.

- IMF July 8 revised projections, which will provide the first institutionally authoritative assessment of Gulf economic damage and global inflation pass-through.

Furthermore, OPEC's market influence in shaping production responses to any prolonged normalisation delay will be a key variable for traders monitoring medium-term supply trajectories.

The asymmetric risk structure facing energy traders is notable: the downside scenario, where physical normalisation proceeds broadly as announced, is largely already reflected in current prices. The upside risk, where normalisation stalls and prices snapback toward the US$88 to US$95 per barrel range, remains underweighted in current market positioning. This asymmetry argues for caution around aggressive short exposure in crude benchmarks until mine-clearance milestones are independently verified rather than diplomatically declared.

The Broader Lesson: Operational Timelines Do Not Bend to Press Releases

The most important analytical takeaway from the reopening of the Strait of Hormuz announcement is that the gap between a diplomatic agreement and a functioning physical shipping corridor is measured in operational milestones, not press conferences. Mine-clearance, insurance underwriting restoration, and fleet repositioning each operate on timescales governed by maritime engineering, actuarial risk assessment, and logistics — none of which compress in response to political urgency.

The 50% probability that commodity analysts assign to a failed normalisation scenario is not a pessimistic fringe view. It is a central scenario estimate that reflects the documented fragility of prior ceasefire announcements and the operational complexity of restoring a contested waterway to commercial viability.

For Mexico specifically, the episode has simultaneously exposed the fiscal sensitivity embedded in the SHCP's budget oil price assumption and the structural limitations that prevent PEMEX from fully capitalising on elevated prices even when they occur. Volume underperformance, capital constraints, and oilfield services capital flight are not problems that a Strait reopening resolves. They are problems that persist regardless of where the Brent benchmark settles.

This article draws on reporting and analysis published by Mexico Business News, including coverage of Sparta Commodities' market assessments, IMF Managing Director Kristalina Georgieva's post-ceasefire commentary, and PEMEX's operational and financial disclosures. This article contains forward-looking analysis and scenario projections that involve inherent uncertainty. Nothing in this article constitutes financial advice. Readers should conduct independent research before making investment or commercial decisions based on energy market conditions.

Want to Stay Ahead of the Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex market data into actionable investment insights — explore how historic discoveries have generated substantial returns and begin your 14-day free trial to position yourself ahead of the broader market.