August 1, 2026

When Reliability Dies, Reopening Changes Nothing

Global maritime trade has always carried an invisible assumption baked into its architecture: that the world's great chokepoints are inconveniences to be managed, not weapons to be wielded. For decades, energy planners, shipping executives, and financial risk teams treated the Strait of Hormuz as a geographic constant. That assumption collapsed in 2026, not because the Strait closed permanently, but because it became unreliable. In the economics of global trade, the Strait of Hormuz shipping disruption demonstrated that unreliability is indistinguishable from closure.

Understanding the full weight of the ongoing Strait of Hormuz shipping disruption requires moving beyond the question of whether vessels can physically pass. The more consequential question is whether they will, and the answer, supported by hard maritime traffic data, is increasingly no.

When big ASX news breaks, our subscribers know first

Why This Strait Carries More Than Oil

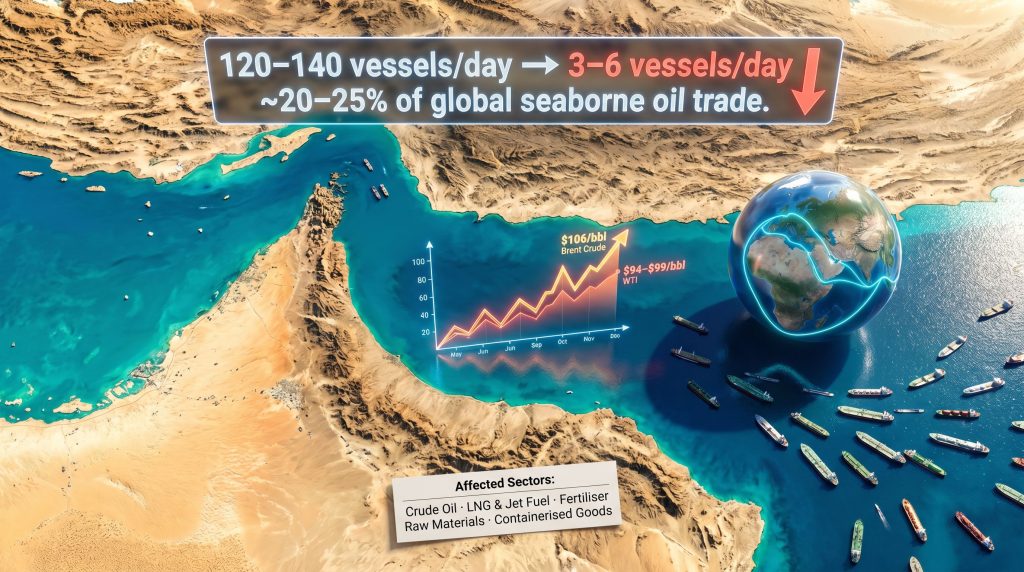

Framing this as an oil market story dramatically understates the systemic exposure. The Strait of Hormuz is the singular exit point for an extraordinary concentration of global commodity flows. Under normal operating conditions, the passage handles approximately 20 to 25 percent of global seaborne oil trade, roughly 20 percent of worldwide LNG and jet fuel shipments, and up to one-third of internationally traded fertiliser raw materials, according to maritime trade data sources including the International Energy Agency and UNCTAD.

The table below illustrates the full commodity profile of normal Strait traffic:

| Commodity | Estimated Share of Global Seaborne Trade | Primary Dependent Regions |

|---|---|---|

| Crude Oil | 20–25% | Asia-Pacific, South Asia, Europe |

| LNG and Jet Fuel | ~20% | Japan, South Korea, India |

| Fertiliser Materials (incl. ammonia) | Up to 33% | South and Southeast Asia, Sub-Saharan Africa |

| Containerised Manufactured Goods | High volume, hundreds of vessels weekly | Global |

This commodity diversity is precisely what makes the current disruption a multi-sector systemic crisis rather than a contained energy market event. When fertiliser shipments seize up, rice production timelines in Bangladesh and Southeast Asia face direct input cost pressures. When jet fuel transits halt, aviation supply chains respond. Furthermore, when LNG flows compress, the LNG supply outlook for European and Asian gas markets tightens simultaneously.

Why Rerouting Is Structurally Harder Here Than in the Red Sea

A critical and widely underappreciated distinction separates the Hormuz disruption from the Red Sea Houthi crisis that began in 2023. In the Red Sea scenario, containerised cargo could, at significant cost, divert around the Cape of Good Hope. That bypass route, while expensive and time-consuming, was physically and commercially executable for most cargo types.

The Strait of Hormuz presents a structurally different problem:

- Very Large Crude Carriers (VLCCs) and LNG tankers face profound logistical barriers to alternative routing, including vessel size constraints and terminal access requirements

- Gulf export infrastructure, including Saudi Arabia's Ras Tanura terminal, Qatar's Ras Laffan LNG facilities, and Kuwait's Mina Al Ahmadi complex, is geographically locked to Hormuz transit with no equivalent alternative deep-water export access

- Saudi Arabia's Petroline east-west pipeline can redirect some crude to Red Sea terminals, but its throughput capacity is substantially below total Gulf production volumes, meaning it absorbs only a fraction of displaced flows

- Airspace complications arising from escalating military activity have compounded the logistical bottleneck, creating a multi-dimensional access problem rather than a single maritime constraint

The 2026 Disruption: How a System Fails in Stages

The Strait of Hormuz shipping disruption of 2026 did not announce itself with a single dramatic event. It unfolded as a cascading systems failure, with each layer of disruption compounding the next in ways that proved far harder to reverse than to trigger.

Phase 1: Insurance Withdrawal (Late February 2026)

Escalating US-Iran tensions triggered the withdrawal of war-risk insurance coverage by major maritime insurers. This is the mechanism most observers missed. Physical access to the Strait remained theoretically intact, but without war-risk insurance, commercial operators faced total uninsured liability for any vessel loss, cargo loss, or crew casualty. Major shipping lines began refusing Hormuz cargo bookings irrespective of whether the Strait was technically navigable. US naval forces diverted approximately 33 commercial vessels during enforcement operations in this period.

Phase 2: Active Interdiction (March 2026)

Iranian authorities seized two container vessels, detaining approximately 40 crew members. Operators responded by disabling AIS (Automatic Identification System) transponders, a practice that violates International Maritime Organization SOLAS regulations but signals extreme operator risk perception. Vessel traffic collapsed from a normal daily baseline of 120 to 140 transits to as few as 3 to 6 vessels per 24-hour period, a decline of approximately 97 percent at peak disruption.

Phase 3: Structural Lock-In (April 2026)

Even during announced ceasefire extensions and partial reopening declarations, the world's largest shipping operators continued to decline Hormuz bookings. Hundreds of vessels accumulated in holding patterns across the Gulf of Oman. Approximately 500,000 containers were stranded, with roughly 20,000 seafarers unable to complete their voyages. As Cyril Widdershoven, Senior Advisor at Blue Water Strategy, observed in analysis published by OilPrice.com on April 25, 2026, none of the world's top shipping companies were willing to take cargo through the Strait even during announced reopening windows.

The Strait of Hormuz was not permanently closed in the traditional sense. It became economically closed: physically accessible in theory, but commercially non-functional due to collapsed insurance markets and entrenched operator risk aversion.

This distinction is foundational to understanding why reopening announcements have failed to restore traffic.

Oil Prices, Supply Shocks, and the Mirage of Normalisation

The price response to the disruption has been severe. Real-time data from OilPrice.com as of April 25, 2026 shows Brent Crude at $105.30 per barrel, the OPEC Basket at $106.30, and WTI at $94.40. At peak escalation, Brent surpassed $106 per barrel amid Gulf producer export constraints. The IEA has characterised the 2026 disruption as the largest supply shock in modern oil market history, with Gulf oil exports collapsing by over 60 percent from normal volumes. These trade war oil prices dynamics reflect how geopolitical confrontation translates directly into energy market volatility.

The conventional market assumption holds that prices retrace when a chokepoint reopens. However, the structural evidence challenges this assumption across several dimensions:

- Insurance repricing operates on its own timeline, not on diplomatic timelines. War-risk premiums embed disruption probability into their models for extended periods following any incident of this severity

- Operator network redesign creates lock-in effects. Shipping lines that have restructured routing contracts, fleet positioning, and scheduling around Cape of Good Hope alternatives do not revert to prior configurations on short notice

- Floating storage overhangs create a supply dynamic that does not respond linearly to chokepoint status changes

- Buyer diversification compounds the effect. Energy importers across Asia and Europe have already accelerated alternative sourcing arrangements, structurally reducing their dependency on Gulf flows regardless of Hormuz status

JPMorgan has publicly stated that oil prices still have further room to rise from current levels, reflecting market assessment that the supply shock has not been fully priced.

The Hidden Price Floor: Why $90+ May Be Structural

A less widely discussed dynamic involves the paradoxical position of Gulf producers themselves. Higher prices partially offset the volume losses caused by the disruption, creating a complex incentive structure. Meanwhile, Norway is reportedly pumping near capacity with its spare output buffer essentially depleted, and global oil inventories are drifting toward record lows. These converging supply-side pressures suggest that even a full Hormuz reopening would encounter a structurally tighter global supply environment than existed before February 2026.

How Global Shipping Routes Are Being Permanently Rewired

The Cape of Good Hope has now become the default routing assumption for Asia-Europe commodity flows. This represents a fundamental rewriting of global logistics network architecture, not a temporary workaround. The commodity price impacts of this rerouting are cascading through manufacturing, agriculture, and energy sectors simultaneously.

The practical implications are significant:

- 10 to 14 additional transit days per voyage on Asia-Europe routes

- Thousands of additional nautical miles, compounding fuel consumption and vessel operating costs per voyage

- Fleet redeployment lock-in, as shipping lines embed Cape routing into long-term contracts and scheduling frameworks

| Dimension | Red Sea Crisis (2023–2025) | Strait of Hormuz Disruption (2026) |

|---|---|---|

| Primary Threat | Houthi militants | US-Iran military confrontation |

| Traffic Decline at Peak | Significant, partial | Approximately 90%+ |

| Rerouting Flexibility | Moderate via Cape bypass | Low due to specialised cargo constraints |

| Insurance Market Impact | Elevated war-risk premiums | Near-total coverage withdrawal |

| Suez/Alternative Recovery | Traffic structurally depressed | Trajectory mirrors Red Sea |

| Assessed Global Scale | Major | IEA: largest supply shock in modern oil market history |

The Red Sea precedent is critical here. Despite years passing since Houthi attacks began, Suez Canal throughput remains structurally below pre-crisis levels. Transit fee discounts offered by the Suez Canal Authority have failed to reverse the traffic migration. That revenue collapse is not cyclical; it reflects permanent behavioural adaptation by shipping operators who have redesigned their networks and have no commercial incentive to revert.

Widdershoven's analysis makes the point directly: the Houthis did not need to close the corridor permanently. They needed only to make it unreliable. Hormuz is now following an identical trajectory at significantly greater scale.

Regional Exposure: Who Bears the Highest Risk

The disruption's consequences are distributed unevenly across the global economy, with certain regions carrying disproportionate exposure.

Asia-Pacific (Highest Hydrocarbon Dependency)

Japan, South Korea, and India collectively depend on Gulf hydrocarbons for a substantial share of their energy import requirements. Japan has approached Saudi Arabia to negotiate emergency supply increases. India's top refining operators are absorbing significant margin compression as crude acquisition costs surge, prompting HSBC to downgrade Indian equities in response. India's manufacturing sector faces sustained input cost pressure that narrows its resilience window considerably.

South and Southeast Asia (Food Security Dimension)

This is perhaps the least-reported consequence of the Strait of Hormuz shipping disruption. Fertiliser supply disruptions linked to ammonia and potash transit constraints are already forcing factory shutdowns in Bangladesh. Rice production timelines across the region face direct input cost pressure. Furthermore, UNCTAD has flagged heightened trade vulnerability for heavily indebted developing economies, a category that includes several South Asian nations already managing elevated debt-servicing costs.

Europe (Energy Security and Industrial Exposure)

Already restructured around post-Russian pipeline gas alternatives following the 2022 Ukraine crisis, Europe's reliance on seaborne LNG imports creates direct Hormuz exposure. European rooftop solar orders have tripled as households and businesses respond to gas price surges. Lufthansa has consequently cancelled unprofitable European summer routes to reduce jet fuel consumption, illustrating how the disruption cascades into aviation economics.

Pakistan (Compounding Shock)

Qatar's LNG supply disruption has forced Pakistan back to spot market purchasing at elevated prices. Pakistan is simultaneously pivoting toward Russian and Venezuelan crude as Middle Eastern supply contracts tighten, a supply chain reconfiguration that carries its own logistical and political complexity.

The next major ASX story will hit our subscribers first

The Four Structural Shifts Already Underway

Regardless of how the immediate US-China trade war and US-Iran diplomatic situation resolves, four structural shifts are already sufficiently embedded to be considered irreversible on any commercially relevant timeframe.

1. Insurance Market Repricing Becomes a Permanent Cost Layer

War-risk premiums for Gulf transit have reached levels that fundamentally alter voyage economics. Even under meaningful de-escalation, insurers will incorporate disruption probability into their models for years. This creates a lasting cost uplift embedded in Gulf export economics that functions as a structural price floor, not a cyclically reversible premium.

2. Energy Buyer Diversification Locks In

Europe is accelerating Atlantic basin and African LNG sourcing, reducing structural dependency on Gulf flows. Japan's Japex has announced plans to quadruple oil and gas production with eyes on US expansion. Asian buyers are expanding US LNG import infrastructure and regional supply redundancy. Gulf producers retain market share but face structural dilution of their pricing leverage as diversification matures across multiple buyer markets.

3. Alternative Export Infrastructure Investment Accelerates

Crisis-driven capital is now moving toward overland pipeline corridors connecting Gulf production to Red Sea export terminals, expanded storage hub development outside chokepoint-exposed zones, and new transshipment architectures designed to reduce single-corridor dependency. Chevron's restart of Wheatstone LNG capacity amid the global gas shortage reflects how non-Gulf producers are responding to the demand signal created by the disruption.

4. Chokepoints as Strategic Weapons Become the Established Norm

The 2026 events have demonstrated that maritime chokepoints are active instruments of geopolitical coercion rather than passive geographic features. The ability to disrupt Hormuz temporarily, without permanent closure, confers leverage far exceeding traditional military capability thresholds. The geopolitical risk landscape across all chokepoint-dependent trade flows has been permanently reset upward, and the baseline risk pricing reflects this new reality.

The Military Response and Its Limits

A 30-nation coalition led by the United Kingdom and France has mobilised a military response aimed at restoring freedom of navigation through the Strait. The coalition's capacity to physically escort vessels is real. Its capacity to restore commercial normalcy is, however, structurally constrained.

Physical reopening and commercial restoration are different problems. Naval escorts address the first; they cannot solve the second. Insurance markets, operator risk perception, and network redesign operate on their own logic, independent of military presence. Even during announced ceasefire extensions, major commercial operators have declined to resume transit. Signals from Israel regarding potential independent military action introduce an additional uncertainty layer that insurance models cannot price out of their risk assessments.

The diplomatic path to durable resolution requires a political settlement between the United States and Iran that extends well beyond maritime security arrangements, and markets are currently pricing in significant uncertainty about whether such a settlement is achievable within any near-term timeframe.

A chokepoint can reopen physically while remaining closed economically. The Strait of Hormuz has already demonstrated this principle in real time, and the data confirms that reopening announcements have not restored commercial traffic volumes.

What the New Architecture of Global Energy Trade Looks Like

The global maritime and energy system is entering a phase of structural fragmentation that will define trade economics across the coming decade. Its core characteristics are already visible in April 2026 data:

- Regionalisation of energy flows, with trade patterns becoming more geographically contained and less dependent on long-haul single-corridor routing

- Redundancy prioritised over optimisation, reversing the cost-efficiency logic that defined the globalisation era

- Permanently higher cost structures embedded across energy, shipping, and manufactured goods pricing

- Chokepoint risk as a standard investment variable across infrastructure decisions, energy contracting, and fleet strategy

Brazil's trade surplus has surged to a record $14.2 billion amid high oil prices, illustrating how the disruption creates winners as well as losers at the national level. Non-Gulf oil producers with export infrastructure independent of Hormuz are experiencing demand and price tailwinds that may permanently alter global production investment flows.

The private sector has already internalised this paradigm shift. Shipping lines, energy traders, and financial institutions are no longer pricing risk based on stability assumptions. They are pricing volatility as the baseline condition. That shift has profound and durable economic consequences for every participant in global trade.

The globalisation model was built on the assumption of frictionless maritime transit through stable chokepoints. Since February 2026, that assumption has been empirically invalidated. What replaces it is a system designed for managed instability, where resilience replaces optimisation, redundancy replaces efficiency, and higher cost structures are the permanent price of operating in a world where geography has become a weapon.

This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Energy market forecasts and scenario projections involve inherent uncertainty. Past market dynamics may not be indicative of future outcomes. Readers should conduct their own due diligence before making any investment or commercial decisions based on the information contained herein.

Want to Position Ahead of the Next Major Commodity Discovery?

As global energy and commodity supply chains undergo permanent structural rewiring, the investment implications extend well beyond oil markets — significant mineral discoveries on the ASX can generate exceptional returns, and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment they are announced, turning complex data into actionable insights. Explore historic examples of major discovery outcomes and begin your 14-day free trial today to ensure you are positioned ahead of the broader market.