August 5, 2026

The Architecture of Fragility: Why Hormuz Remains the World's Most Consequential Maritime Pressure Point

Every major global supply chain carries within it a single point of catastrophic failure. For the world's energy system, that point is a narrow corridor of water connecting the Persian Gulf to the Gulf of Oman. Strait of Hormuz shipping disruptions have long been recognised by energy economists, naval strategists, and logistics planners as the most consequential maritime risk on earth, not because of what flows through it on any given day, but because of what cannot be rerouted if that flow is interrupted.

Understanding the mechanics of this vulnerability requires looking beyond headline oil prices and tanker counts. The structural dependency runs deep across commodity categories, national economies, and industrial supply chains that most consumers never consider when filling a fuel tank or purchasing a manufactured good.

The Chokepoint That Moves the World: A Structural Overview

At its narrowest navigable point, the Strait of Hormuz measures approximately 34 kilometres across, though the actual shipping lanes are far narrower. Vessels transit through a 3-kilometre-wide inbound lane and a matching outbound lane, separated by a 3-kilometre buffer zone, all overseen by an IMO-designated traffic separation scheme. This geographic reality means that even minor military or naval interference can effectively collapse commercial transit without a full physical blockade.

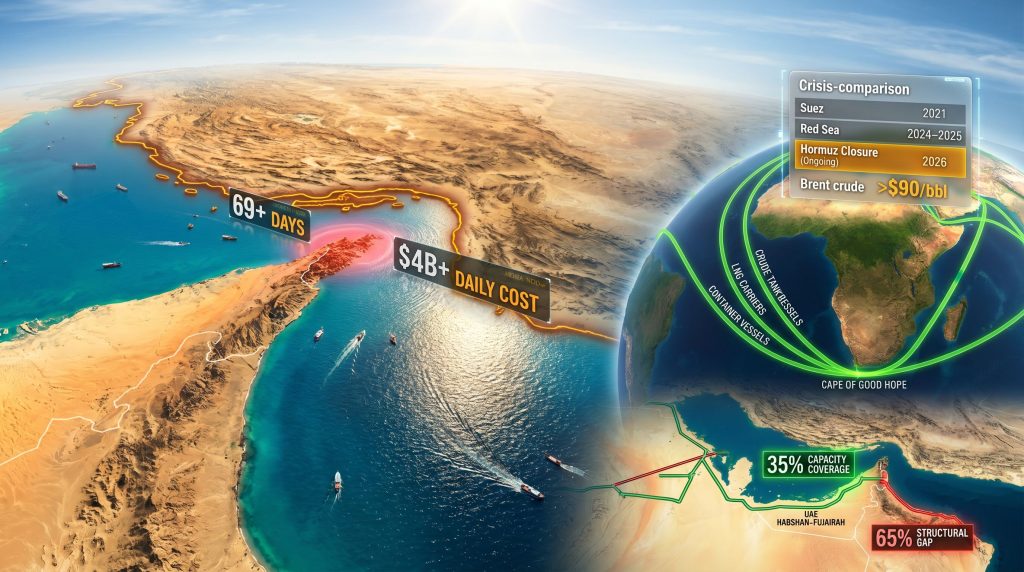

The throughput figures are staggering in their global significance. Under normal operating conditions, approximately 21 to 25% of all globally traded oil passes through the strait, alongside roughly 25% of global LNG exports. No other maritime corridor comes close to concentrating this volume of energy trade in such a narrow geographic passage.

The following comparison illustrates how the Strait of Hormuz stands apart from other critical maritime chokepoints:

| Chokepoint | Daily Oil Volume | Primary Rerouting Option | Strategic Risk Level |

|---|---|---|---|

| Strait of Hormuz | ~21-25% of global supply | Partial pipeline bypass (~35% coverage) | Critical |

| Suez Canal | ~12% of global trade | Cape of Good Hope | High |

| Strait of Malacca | ~25% of global seaborne trade | Lombok/Sunda Straits | High |

| Bab-el-Mandeb | ~10% of global oil | Cape of Good Hope | Elevated |

What separates Hormuz from every other chokepoint is not simply its volume, but the absence of a credible bypass. The Suez Canal, while critical, can be circumvented via Africa's Cape of Good Hope at considerable cost but with functional outcomes. The Strait of Malacca offers alternative Indonesian passages. Hormuz has no maritime equivalent. Furthermore, the LNG supply outlook for Asia-Pacific markets is directly tied to unimpeded passage through this corridor.

How Dependent Is the Global Economy on Persian Gulf Throughput?

The commodity dependency extends well beyond crude oil. The Persian Gulf corridor is also the primary export route for:

- Crude oil from Saudi Arabia, UAE, Kuwait, Iraq, and Iran

- Liquefied natural gas from Qatar, the world's largest LNG exporter

- Petrochemical feedstocks destined for Asian manufacturing hubs

- Fertilizer inputs including urea and ammonia critical to global food production

The national economies most exposed to disruption include Japan, South Korea, India, China, and multiple EU member states, all of which import substantial volumes of Persian Gulf crude and LNG. Japan and South Korea in particular source the majority of their crude oil from Gulf producers, with limited domestic production to buffer supply shocks.

The pipeline bypass infrastructure that exists offers only partial relief. The UAE's Habshan-Fujairah pipeline, with a capacity of approximately 1.5 million barrels per day, and Saudi Arabia's East-West pipeline connecting Eastern Province fields to Red Sea terminals together represent the primary overland alternatives. However, their combined throughput capacity covers only approximately 35% of normal Hormuz flow, leaving a structural gap that cannot be bridged by existing infrastructure alone.

Structural Reality: Even maximum utilisation of all pipeline bypass capacity leaves approximately 65% of normal Hormuz throughput with no viable alternative route. This is not a temporary operational shortfall. It reflects decades of underinvestment in bypass infrastructure during periods when Hormuz transit was assumed to remain stable.

When big ASX news breaks, our subscribers know first

What Is Actually Happening in the Strait of Hormuz Right Now? (2026 Disruption Status)

The 2026 Hormuz closure marks a qualitative shift from previous maritime disruptions. Prior events, including the 2021 Suez Canal blockage and the 2024–2025 Red Sea crisis, were disruptive but geographically contained. This disruption strikes at the single node that those alternative routes were intended to serve. The broader context of oil market disruption stemming from concurrent geopolitical pressures has amplified the severity of market responses.

Timeline of the 2026 Hormuz Closure: From Escalation to Prolonged Blockade

The effective closure of the strait to commercial shipping commenced in March 2026, driven by military escalation involving Iran, the United States, and regional actors. A brief window of potential relief emerged on April 21, 2026, when a fragile reopening appeared possible, but was followed within 24 hours by re-closure on April 22, 2026. As of early May 2026, the disruption has extended beyond 69 consecutive days of effective commercial shutdown.

The collapse in vessel traffic has been near-total. From a baseline of approximately 138 commercial vessels transiting daily under normal conditions, traffic has fallen to near-zero. AIS signal blackouts, sea mine deployment concerns, and wholesale insurance withdrawal have rendered selective passage commercially non-viable even for operators willing to accept elevated risk premiums.

The Scale of Disruption: Key Metrics at a Glance

Snapshot: Hormuz Closure Impact (May 2026)

- 69+ days of sustained effective closure

- ~90–93% reduction in normal commercial vessel traffic

- 150+ ships stranded, including approximately 470,000 TEU in containerised cargo

- All 9 major global container carriers suspended transits, including Maersk, CMA CGM, Hapag-Lloyd, ONE, HMM, Evergreen, and PIL

- Emergency surcharges of $1,500–$4,000 per TEU applied across Gulf-origin cargo

- Tanker rates peaked at $800,000/day (March 7, 2026)

- More than 34,000 ships diverted in the first four weeks of closure

- Estimated daily trade cost: in excess of $4 billion

How Does the 2026 Hormuz Disruption Compare to Previous Maritime Crises?

Historical maritime disruptions provide important context for understanding the severity of the current closure. The 2021 Suez Canal blockage, caused by the grounding of the Ever Given container vessel, lasted six days and delayed approximately 400 vessels while generating an estimated $9–10 billion in trade disruption. The Red Sea crisis beginning in late 2023, driven by Houthi attacks on commercial shipping, rerouted approximately 15% of global shipping over a 14-month period.

| Disruption Event | Year | Duration | Peak Oil Price Impact | Global Trade Disruption |

|---|---|---|---|---|

| Suez Canal Blockage | 2021 | 6 days | ~+4% | ~12% of global trade delayed |

| Red Sea / Houthi Crisis | 2024–2025 | ~14 months | +5–8% | ~15% of global shipping rerouted |

| Hormuz Closure (Ongoing) | 2026 | 69+ days | Brent crude above $90/bbl | 21% of global oil, 25% of LNG at risk; $4B+ daily cost |

The 2026 Hormuz closure represents a structurally different risk category from both predecessors. The Red Sea crisis, for all its duration and disruption, affected a reroutable corridor. Consequently, the Hormuz closure affects the primary source corridor itself, leaving global shipping with diminished buffer capacity precisely when a larger shock arrived.

What Are the Cascading Economic Consequences of Prolonged Hormuz Closure?

Energy Price Transmission: From Tanker Rates to Consumer Fuel Costs

The price transmission mechanism from maritime disruption to consumer fuel costs operates through a chain of market signals that moves faster than physical supply can be rerouted. Spot market volatility in crude oil immediately raises refinery input costs, which translate into higher wholesale fuel prices within weeks and retail price increases within a month or two of sustained supply disruption.

Brent crude trading above $90 per barrel as a direct consequence of constrained Gulf supply reflects this mechanism in real time. Historical precedent supports the magnitude of this response: during the 2022 energy crisis, Brent crude exceeded $130/bbl following Russian supply disruptions affecting a smaller percentage of global supply than Hormuz represents.

The LNG spot market faces a separate but parallel dynamic. Asia-Pacific buyers in Japan, South Korea, and China, who collectively account for the majority of global LNG demand, face supply shortfalls and elevated spot premiums when Qatari LNG cannot transit the strait. During the 2022 European energy crisis, Asian LNG spot prices reached $40–60 per MMBtu above historical contract pricing norms, demonstrating the premium markets will pay when supply security is threatened.

The US Strategic Petroleum Reserve (SPR), which held approximately 700 million barrels at full capacity, can provide a short-term demand buffer during disruptions of 30 to 90 days. However, a closure extending beyond that window exhausts the utility of coordinated IEA member drawdowns and forces structural supply adjustment. The IEA provides detailed guidance on oil security and emergency response frameworks specifically related to Hormuz risk scenarios.

Beyond Oil: Fertilizer, Food, and Industrial Supply Chain Stress

One of the least-discussed dimensions of Hormuz disruption is its impact on agricultural supply chains. The Persian Gulf region is a major global exporter of urea and ammonia, the primary nitrogen-based fertilizer inputs that underpin crop yields across South Asia, Sub-Saharan Africa, and Southeast Asia. Disruption to these export flows compounds food security pressures in import-dependent nations already managing elevated food price inflation.

Petrochemical feedstock shortages represent a secondary industrial consequence. Asian and European manufacturers dependent on Gulf-origin naphtha, ethylene, and propylene face upstream input disruptions that ripple through plastics production, packaging, pharmaceutical manufacturing, and automotive component supply chains.

Scenario modelling suggests that if the closure extends beyond 90 days, projected impacts on agricultural input costs could translate into measurable increases in global food price indices, particularly for nations in South Asia and Sub-Saharan Africa where food expenditure represents a higher proportion of household income. In addition, critical minerals demand for clean energy manufacturing is also affected by broader commodity supply chain disruptions flowing from this crisis.

Regional Manufacturing and Logistics Disruption

Asia-Pacific manufacturing economies face input delays of 2 to 14 additional transit days as vessels circumnavigate Africa via the Cape of Good Hope rather than transiting the Gulf. This is not merely an inconvenience. Just-in-time manufacturing systems, particularly prevalent in South Korean electronics, Japanese automotive production, and Chinese industrial manufacturing, carry minimal inventory buffers and begin experiencing production disruptions within days of sustained input delays.

Freight costs on Gulf-to-Asia routes have effectively tripled as vessels absorb additional fuel, crew time, and port fees associated with the longer routing. Kuwait and UAE production curtailments have added upstream supply pressure, compounding the physical supply constraint with reduced available volumes even for vessels willing to attempt passage.

The Debt-Stressed Developing Economy Risk

The distribution of economic harm from Strait of Hormuz shipping disruptions is deeply asymmetric. Advanced economies with diversified energy mixes, strategic reserves, and currency reserves to absorb import cost increases face elevated inflation and reduced growth. Debt-stressed developing economies, however, face an existential fiscal pressure.

The mechanism works as follows:

- Higher import bills for oil and LNG widen current account deficits

- Widening deficits drive currency depreciation in nations with limited reserve buffers

- Currency depreciation amplifies domestic inflation through higher import costs across all commodity categories

- Elevated inflation forces central banks to raise interest rates, suppressing domestic investment

- Higher sovereign borrowing costs worsen debt sustainability for nations already carrying elevated debt loads

The regions most exposed to this compounding dynamic include South Asia, Sub-Saharan Africa, and parts of Southeast Asia, where energy import dependency, limited foreign exchange reserves, and high sovereign debt levels combine to create systemic vulnerability. UNCTAD's analysis of Hormuz disruptions provides further detail on the implications for global trade and development in these vulnerable regions.

How Is the Global Shipping Industry Responding to Hormuz Closure?

The Cape of Good Hope Rerouting Strategy: Costs, Timelines, and Capacity Limits

The maritime industry's primary response to Hormuz closure is the same route that served European trade before the Suez Canal opened in 1869: circumnavigating Africa via the Cape of Good Hope. This rerouting adds approximately 2 to 14 days of additional transit time depending on origin-destination port pairs, with the greatest time impact felt on Persian Gulf to Northeast Asia routes.

The fuel cost implications are material. Vessels circumnavigating Africa consume 20 to 35% more fuel per voyage than on the direct Gulf route, and the longer voyage also absorbs vessel capacity that would otherwise be available for additional voyages. This capacity absorption effect creates a secondary tightening in global vessel availability, raising freight rates even on routes unaffected by the closure itself.

| Vessel Class | Normal Gulf-to-Asia Transit | Cape Rerouting Transit | Estimated Additional Cost |

|---|---|---|---|

| VLCC (crude tanker) | ~20 days | ~30–34 days | +30–40% voyage cost |

| Suezmax tanker | ~18 days | ~28–32 days | +25–35% voyage cost |

| LNG carrier | ~22 days | ~35–40 days | +30–45% voyage cost |

| Container ship | ~25 days | ~38–45 days | Freight rates tripled |

Carrier Responses and Emergency Surcharge Structures

All nine major container carriers have suspended Hormuz transits. Emergency surcharge frameworks of $1,500 to $4,000 per TEU have been applied across Gulf-origin cargo, reflecting both the additional voyage costs and the scarcity premium associated with limited available capacity on alternative routes.

Force majeure declarations have created complex cargo liability situations. Shippers face contractual uncertainty about delivery timelines, insurance coverage, and their ability to pass elevated freight costs through to end customers. For manufactured goods with thin margins and fixed-price contracts, the financial impact of emergency surcharges can represent the difference between profitable and loss-making shipments.

The insurance market response has further constrained options. War risk premium escalation and policy withdrawal for Gulf-transiting vessels has effectively priced out the marginal operator willing to attempt transit. During the 2024–2025 Red Sea crisis, war risk insurance premiums escalated sharply and became a significant determinant of carrier routing decisions, a dynamic now replicated at greater scale in the Gulf.

Pipeline Bypass Utilisation: Capacity Ceiling and Strategic Gaps

Key Insight: Land-based pipeline infrastructure, including the UAE's Habshan-Fujairah pipeline and Saudi Arabia's East-West pipeline, can collectively handle only approximately 35% of the Strait's normal throughput. This structural ceiling means no combination of pipeline alternatives can substitute for full maritime access, leaving a persistent 65% supply gap that cannot be bridged by existing overland infrastructure alone.

The constraints on pipeline bypass utilisation are multiple and compounding:

- Pipeline throughput limits: physical capacity cannot be expanded quickly regardless of price incentives

- Terminal export capacity: loading facilities at Fujairah and Red Sea endpoints have finite berth and storage capacity

- Crude grade compatibility: not all pipeline-accessible crudes match the quality specifications required by destination refineries

- Maintenance windows: pipelines require periodic maintenance that prevents sustained maximum-rate operation

The decades of underinvestment in bypass infrastructure reflects a rational calculation during periods of Hormuz stability, but one that has amplified strategic leverage for any actor willing to threaten or implement closure.

What Is the Geopolitical and Diplomatic Response to the Hormuz Crisis?

The UN Security Council Dimension: Sanctions, Vetoes, and Fragile Ceasefires

US and Gulf allies pursued a UN Security Council resolution demanding humanitarian shipping corridors and warning Iran of expanded sanctions. The resolution was vetoed by China and Russia, illustrating the structural limits of multilateral enforcement mechanisms when permanent member interests diverge from the majority position.

The IMO Director-General has taken a clear institutional position, rejecting Iranian demands for commercial vessels to pay transit fees as a condition of passage through the strait, citing the absence of safe transit conditions for commercial shipping. This position reflects established international maritime law under UNCLOS, which guarantees the right of transit passage through international straits, but legal frameworks have limited operational force when backed by insufficient enforcement capacity.

A fragile ceasefire reached in April 2026 has remained unstable. The brief reopening window of April 21–22, 2026 demonstrated both that partial resolutions are achievable and that they can collapse within 24 hours without structural diplomatic progress.

US Enforcement Operations: Blockade, Tanker Seizures, and Escalation Risk

US naval enforcement operations, including tanker seizures and interdiction activities, have created an additional layer of operational uncertainty in the strait. The strategic tension between constraining Iranian energy revenue, which provides funding for military operations, and the collateral cost of broader supply disruption creates a difficult calculus for policymakers.

Enforcement actions carry inherent escalation risk. Each tanker interdiction raises the probability of retaliatory mine deployment or missile strikes on commercial vessels, which would further deter already-hesitant commercial operators from attempting transit. The geopolitical trade tensions reshaping broader global commerce in 2025–2026 have made these enforcement calculations considerably more complex for all parties involved.

Iran's Strategic Leverage: The Asymmetric Power of Chokepoint Control

Iran's Hormuz strategy exemplifies asymmetric warfare applied to economic infrastructure. Iran's conventional military capacity relative to its adversaries is limited, but its ability to impose costs on global energy markets through chokepoint disruption vastly exceeds what conventional military metrics would suggest.

Historical precedent for this strategy is well-documented. During the 2011–2012 sanctions escalation, Iranian officials publicly threatened to close the Strait of Hormuz if sanctions were tightened, driving significant oil price volatility without a single ship being stopped. The 2019 attacks on the Kokuka Courageous and Front Altair tankers in the Gulf of Oman demonstrated Iran's operational capability and willingness to act on these threats at reduced diplomatic cost to itself.

Furthermore, Iran recently created a new agency to control shipping in the strait, underscoring the institutionalisation of this leverage. The strategic logic is straightforward: the cost of disruption to Iran is bounded by the existing sanctions it faces, while the cost imposed on global markets is effectively unbounded during a prolonged closure.

Canada's Emerging Role: Energy Diplomacy in a Supply-Constrained World

Against the backdrop of ongoing Strait of Hormuz shipping disruptions, the IEA's diplomatic engagement with Canadian leadership in early May 2026 carries significant strategic weight. IEA Executive Director Fatih Birol travelled to Ottawa and Toronto for a series of high-level meetings with Prime Minister Mark Carney, Energy and Natural Resources Minister Tim Hodgson, and Finance Minister François-Philippe Champagne.

The discussions centred on the implications of shipping disruptions through the Strait of Hormuz for global supplies of oil, natural gas, and other important commodities. The Canadian energy response to the unfolding crisis has positioned the country as a key partner in IEA-led diversification planning. The engagement was notable for its breadth, extending beyond immediate crisis response to address Canada's domestic energy infrastructure development and export expansion capacity.

Canada's position as a potential supply diversification option is grounded in real resource capacity. Canadian oil sands production, offshore Atlantic resources, and the country's underdeveloped LNG export infrastructure represent a combination of near-term and medium-term supply expansion potential that is directly relevant to markets disrupted by Persian Gulf supply constraints.

The China-Russia Factor: Divergent Interests and Strategic Ambiguity

China faces genuine dual exposure to the Hormuz crisis. As a major importer of Persian Gulf crude, China experiences direct economic harm from every day the strait remains closed. Yet China's UNSC veto blocks the enforcement mechanisms that might resolve the disruption more quickly. This reflects a broader pattern of strategic ambiguity in which China's short-term energy security interests conflict with its longer-term interest in maintaining relationships with Iran and limiting Western military enforcement precedents in the Gulf.

Russia's calculation is more straightforwardly beneficial. Elevated oil prices resulting from supply disruption partially offset the impact of Western sanctions on Russian energy revenue. A prolonged Hormuz closure that keeps Brent crude above $90/bbl represents a meaningful financial benefit to Russian export economics, reducing the incentive to support enforcement mechanisms that would end the disruption.

This divergence of great-power interests creates a structural paralysis in multilateral resolution pathways that cannot be resolved through diplomacy alone.

What Are the Long-Term Strategic Implications for Global Energy Security?

Accelerating the Structural Case for Supply Diversification

The 2026 Hormuz crisis is functioning as a catalytic event for energy importer diversification strategies that have been discussed for decades but implemented only partially. Three distinct scenarios are plausible from this point:

Scenario A: Short-Term Resolution (within 30–60 days) — Markets stabilise as shipping resumes. Price spikes reverse. Emergency surcharges are withdrawn. However, the structural vulnerability that enabled the disruption remains entirely unaddressed, and the 65% pipeline bypass gap persists unchanged.

Scenario B: Extended Closure (90–180 days) — Permanent rerouting infrastructure investment accelerates. LNG terminal buildout in alternative supply regions gains commercial momentum. Energy importers accelerate supply diversification agreements with non-Gulf producers, creating durable demand shifts.

Scenario C: Prolonged Multi-Year Disruption — Fundamental restructuring of global energy trade architecture. Non-Gulf producers including Canada, Australia, the United States, and Qatar (via alternative routes) capture long-term market share that may not fully reverse even after strait access is restored.

The Critical Minerals Dimension: A Secondary but Growing Vulnerability

Persian Gulf transit routes carry not only energy commodities but also critical mineral shipments relevant to battery supply chains and clean energy manufacturing. The IEA's inclusion of critical minerals in its May 2026 discussions with Canadian officials reflects growing recognition that the same chokepoint vulnerability affecting oil and gas also affects the mineral inputs required for the clean energy transition.

This creates a compound strategic interest for non-Gulf critical mineral producers. Nations like Canada, Australia, and several African producers that can offer both conventional energy and critical mineral supply chains represent a new category of strategic partnership for energy-importing nations seeking to reduce their vulnerability to single-corridor disruptions.

Piracy Resurgence as a Secondary Consequence

Fuel shortages linked to Hormuz disruption are driving piracy resurgence off the Somali coast, as East African coastal communities face acute supply constraints that historically correlate with increased maritime predatory activity. Small tanker operators, who lack the fleet size to absorb rerouting costs and have been disproportionately excluded from major carrier convoy arrangements, face elevated risk on the Cape of Good Hope routing.

The 2008–2012 Somali piracy surge, which peaked with over 200 attacks in 2011 before coordinated international naval escort programmes drove incident rates sharply lower, provides both a cautionary precedent and a policy template. Naval escort programmes were effective but resource-intensive, and their implementation required exactly the kind of multilateral cooperation that current UNSC dynamics make more difficult.

Infrastructure Investment Priorities Emerging from the Crisis

The crisis is generating visible investment prioritisation in several infrastructure categories:

- Pipeline bypass expansion: UAE and Saudi Arabia face renewed urgency to expand bypass pipeline capacity beyond the current 35% coverage ceiling

- LNG terminal diversification: Atlantic Basin and Pacific Basin LNG receiving infrastructure investment rationale has strengthened materially

- Strategic petroleum reserve reform: Debate over SPR scale, release trigger mechanisms, and coordinated IEA drawdown protocols has intensified

- Alternative port capacity: Waypoint ports including Singapore, Colombo, and Durban face capacity investment requirements as rerouted traffic increases

The next major ASX story will hit our subscribers first

FAQ: Strait of Hormuz Shipping Disruptions Explained

What percentage of global oil passes through the Strait of Hormuz?

Approximately 21 to 25% of all globally traded oil and around 25% of global LNG flows through the Strait of Hormuz under normal operating conditions, making it the single most consequential maritime chokepoint for energy markets worldwide.

How long has the Strait of Hormuz been closed in 2026?

As of early May 2026, the Strait has been effectively closed to commercial shipping for 69 or more days, following an initial closure in March 2026 and a failed brief reopening on April 21–22, 2026 that collapsed within 24 hours.

What happens to oil prices when the Strait of Hormuz is disrupted?

Sustained disruption drives Brent crude prices significantly higher. During the 2026 closure, Brent crude has exceeded $90 per barrel as markets price in supply scarcity. Tanker freight rates also spike dramatically, with VLCC rates reaching $800,000 per day at peak disruption.

Can pipeline infrastructure replace Strait of Hormuz shipping capacity?

No. Existing pipeline bypass routes, including the UAE Habshan-Fujairah pipeline and Saudi Arabia's East-West pipeline, can collectively handle only approximately 35% of normal Hormuz throughput, leaving a structural 65% gap that cannot be covered by any combination of existing overland alternatives.

Which countries are most affected by Strait of Hormuz disruptions?

Japan, South Korea, India, China, and EU member states face the greatest direct exposure due to their high dependence on Persian Gulf crude and LNG imports. Energy-importing developing economies in South Asia, Sub-Saharan Africa, and Southeast Asia face compounding debt and inflation pressures due to widening current account deficits and currency depreciation dynamics.

What is the Cape of Good Hope rerouting cost?

Rerouting via the Cape of Good Hope adds approximately 2 to 14 days of additional transit time and 20 to 35% more fuel cost per voyage, with freight costs on Gulf-to-Asia routes effectively tripling. Emergency surcharges of $1,500 to $4,000 per TEU have been applied by major container carriers.

Why can't the UN resolve the Strait of Hormuz crisis?

UNSC enforcement resolutions have been blocked by Chinese and Russian vetoes, reflecting divergent great-power interests. China's dual role as a Persian Gulf oil importer harmed by the closure and as a veto-wielding power blocking enforcement creates structural paralysis, while Russia's interest in elevated oil prices reduces its incentive to support resolution.

Key Takeaways: What the Hormuz Crisis Reveals About the Fragility of Global Energy Trade

The 2026 Hormuz closure has exposed five structural vulnerabilities in the global energy system that policy discussions have acknowledged but market incentives have failed to address:

-

The bypass gap is structural, not temporary. Existing pipeline infrastructure covers only 35% of normal Hormuz throughput, a gap that cannot be closed without multi-year infrastructure investment.

-

The compounding effect of sequential disruptions is underpriced. The Hormuz crisis arrived before the Red Sea crisis fully resolved, demonstrating that markets and shipping systems have insufficient buffer capacity when multiple chokepoints are simultaneously under stress.

-

Great-power divergence neutralises multilateral enforcement. The UNSC veto dynamics that blocked enforcement resolutions are not an anomaly but a reflection of structurally divergent interests among permanent members.

-

Energy-importing developing economies bear disproportionate risk. The debt-currency-inflation spiral triggered by sustained supply disruptions falls most heavily on nations least equipped to absorb it.

-

Non-Gulf supply nations are structurally underweighted in diversification portfolios. The diplomatic engagement between the IEA and Canadian leadership in May 2026 signals that this underweighting is being actively reassessed at the highest levels of energy policy.

The forward-looking implications point toward accelerated investment in pipeline bypass capacity, LNG terminal diversification, strategic reserve reform, and bilateral energy security agreements between major importers and non-Gulf producers. Canada's combination of conventional hydrocarbon resources, LNG export development potential, and critical minerals endowment positions it as a prominent candidate in these diversification discussions.

The Hormuz crisis functions as the most significant stress test the global energy system has faced since the 1970s oil shocks. Unlike those shocks, which were driven by producer cartel decisions, the 2026 disruption is driven by geopolitical conflict at a physical chokepoint with no full bypass alternative. The resilience reforms that emerge from this stress test will define the architecture of global energy security for the decades that follow.

This article draws on information reported by World Oil (May 7, 2026) regarding IEA Executive Director Fatih Birol's meetings with Canadian Prime Minister Mark Carney, Energy Minister Tim Hodgson, and Finance Minister François-Philippe Champagne, as well as historical data on maritime chokepoints, shipping economics, and energy infrastructure from the U.S. Energy Information Administration, International Maritime Organization, and UNCTAD maritime trade reports. Forward-looking scenario analysis and projections represent analytical modelling and should not be construed as investment advice. Readers seeking additional real-time vessel traffic data may find value in exploring resources such as MarineTraffic AIS tracking services and the UNCTAD maritime disruption monitoring framework.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Energy Disruptions?

The Hormuz crisis is reshaping commodity supply chains and accelerating demand for non-Gulf energy and critical mineral producers — and Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries the moment they're announced, turning complex commodity data into actionable investment insights. Explore how historic mineral discoveries have generated substantial returns for early-positioned investors, and begin your 14-day free trial at Discovery Alert to ensure you're positioned ahead of the market when the next major discovery is made.