July 15, 2026

The World's Most Dangerous Energy Chokepoint Is in Crisis Again

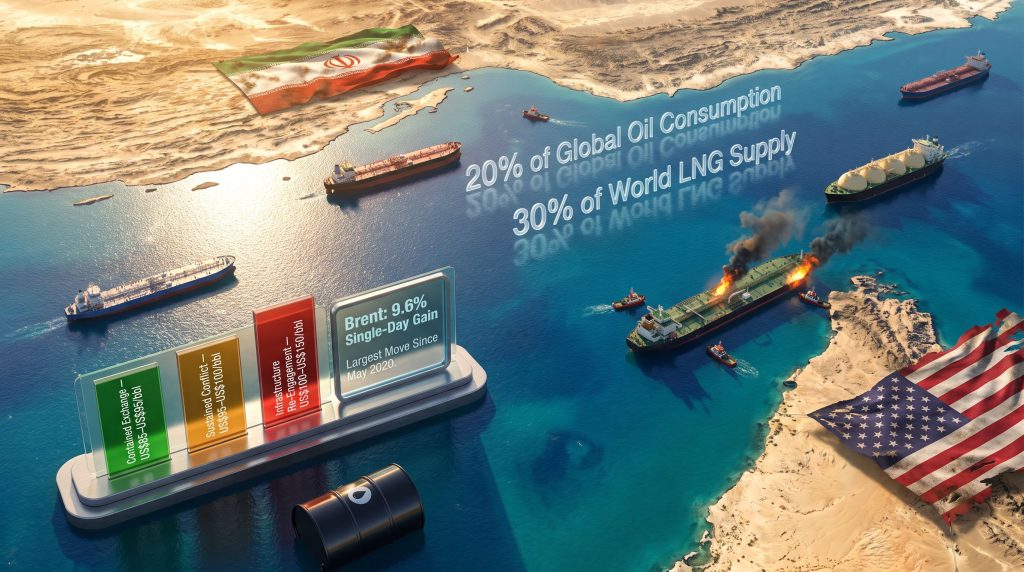

Few geographic features carry as much weight in global energy security as a 33-kilometre stretch of water between the Omani coast and Iran. The Strait of Hormuz is not merely a shipping lane. It is the arterial passage through which roughly 20% of global oil consumption and approximately 30% of the world's liquefied natural gas supply flows every single day. No pipeline network, no alternative maritime corridor, and no combination of overland routes can absorb those volumes if the strait becomes inaccessible at scale. That structural reality is what makes the phrase Strait of Hormuz shut again as US-Iran fighting restarts so consequential for energy markets, supply chains, and geopolitical risk pricing worldwide.

Understanding why this corridor holds the global energy system hostage requires looking beyond the current conflict. The strait has functioned as a pressure point in regional tensions for decades. Every prior threat of closure, from the tanker wars of the 1980s to the IRGC mine-laying incidents of 2019, has incrementally recalibrated how energy markets price Gulf risk. What is unfolding in July 2026 represents the most serious materialisation of that risk since the modern LNG trade took shape.

When big ASX news breaks, our subscribers know first

Contested Waters: What Closure Actually Means in Practice

The current situation is defined by a fundamental and operationally dangerous contradiction. Iran's Islamic Revolutionary Guard Corps has formally declared the strait closed to vessel traffic. The United States Central Command has maintained that the waterway remains accessible, asserting that Iran does not exercise sovereign authority over an international strait governed by established maritime law.

Navigational Limbo: The Strait of Hormuz currently exists in a state of contested access, formally declared closed by one party and formally declared open by another. For shipping operators, the legal distinction is secondary to the physical risk.

The gap between those two positions is not merely diplomatic. On the water, the consequences are immediate. Approximately 20 vessels reversed course toward Oman following Iran's announcement. Two merchant ships came under gunfire while attempting transit. War-risk insurance underwriters have responded by pushing premiums to levels that render some voyages economically marginal without corresponding adjustments to cargo pricing. The practical effect is a strait that functions as neither clearly open nor clearly closed, but as something far more dangerous: a zone of unpredictable physical risk where the rules of passage are genuinely contested. For a broader crude oil market overview, the implications of contested Hormuz access are already being felt in pricing benchmarks globally.

How the Ceasefire Collapsed: A Timeline of Escalation

The breakdown of what had appeared to be a stabilising diplomatic framework unfolded with striking speed. A 60-day ceasefire agreed in mid-June 2026 created a window of relative calm, but accusations of violations began surfacing almost immediately from both sides.

Iran pointed to what it characterised as a US naval blockade of Iranian ports and continued Israeli military operations in Lebanon as justification for re-escalation. Washington's position was that hostilities had formally restarted, with President Trump notifying Congress that military action against Iran had resumed. According to AP News, the sequence of events leading to this renewed conflict had been building for several months across multiple flashpoints.

| Date | Event |

|---|---|

| Mid-June 2026 | 60-day ceasefire formally agreed between US and Iran |

| 20 June 2026 | IRGC announces re-closure of Strait of Hormuz |

| 6 July 2026 | IRGC strikes three commercial vessels near Oman, including a Qatari LNG tanker |

| 7 July 2026 | US launches retaliatory strikes on Iranian military targets |

| 8 July 2026 | Iran responds with missile and drone attacks on Gulf military bases |

| 8 July 2026 | President Trump formally declares the ceasefire ended |

| 14 July 2026 | Strait remains in contested status; vessel avoidance continues |

The trigger event on 6 July was the IRGC striking three commercial vessels near Oman, including a Qatari LNG tanker, after those vessels reportedly attempted to navigate a route reportedly seeded with sea mines while disregarding warnings. Washington responded with retaliatory strikes the following day, and Tehran answered with missile and drone attacks on Gulf military installations hosting US forces.

Phase One vs. Phase Two: A Shift in Targeting Logic

What makes the current phase of fighting analytically distinct from the conflict's opening weeks is the nature of what is being targeted. The February and March 2026 phase was defined by direct strikes on energy infrastructure: Iranian energy facilities were hit, Gulf oil and gas installations were struck, and several regional airports suspended operations under threat.

The July 2026 phase has concentrated on military assets, coastal defence systems, and vessels connected to shipping disruption. Energy facilities have, so far, been largely spared. This narrowing of targeting suggests both parties are calibrating escalation thresholds rather than pursuing maximalist objectives.

Paul Musgrave, Associate Professor of Government at Georgetown University in Qatar, has observed that Washington's stated objectives have contracted considerably since the conflict's opening phase, with regime change rhetoric receding from American discourse even as some voices in Tehran have begun articulating ambitions for expanded influence across the Gulf region.

Three Scenarios for Energy Markets: A Risk Framework

Mapping the possible trajectories of this conflict requires moving beyond simple bullish or bearish oil price calls. The structural risks facing energy markets fall into three distinct scenarios, each carrying different implications for commodity pricing, LNG availability, and supply chain resilience.

| Scenario | Probability | Brent Price Range | Strait Status | LNG Impact |

|---|---|---|---|---|

| Contained Exchange | Moderate | US$85-US$95/bbl | Partially functional | Elevated war-risk premiums |

| Sustained Conflict, No Infrastructure Targeting | Elevated | US$95-US$100/bbl | Functionally restricted | Significant market tightening |

| Full Infrastructure Re-Engagement | Low-to-moderate tail risk | US$100-US$150/bbl | Effectively closed | Acute shortage conditions |

Scenario 1: Contained Exchange assumes both sides maintain targeted military exchanges without crossing into energy infrastructure warfare. Diplomatic back-channels through Qatari and Pakistani mediation remain active and eventually produce a durable framework. Under this scenario, Brent likely stabilises in the US$85-US$95 per barrel range, with shipping adapting through elevated insurance costs and selective route avoidance.

Scenario 2: Sustained Conflict Without Infrastructure Targeting envisions hostilities continuing without diplomatic resolution but with energy facilities remaining largely off-limits. This produces what amounts to a functional closure of the strait without the formal designation: transit becomes unreliable rather than physically blocked. Commonwealth Bank's commodity research team has modelled Brent reaching US$100 per barrel within 10 days under sustained conflict conditions. Furthermore, the oil market impact of this scenario extends well beyond the Gulf, touching import-dependent economies across Asia and Europe. LNG spot markets would tighten meaningfully as Qatari and UAE export volumes face routing uncertainty.

Scenario 3: Full Infrastructure Re-Engagement represents the tail risk scenario in which a return to Phase One conditions sees energy facilities become active targets again on both sides. Commonwealth Bank researchers have projected Brent could reach US$150 per barrel within ten weeks under an unchecked escalation scenario. This would replicate and potentially exceed the price shock recorded when conflict first erupted in February 2026, when Brent previously surpassed US$100 per barrel. European and Asian import-dependent economies would face emergency procurement conditions, and global LNG markets would enter acute shortage territory.

The Oil Price Surge: Reading the Market Signal Correctly

Brent crude climbed to approximately US$85 per barrel during the week of peak escalation in early July 2026, having traded near US$70 per barrel in the immediate aftermath of the June ceasefire agreement. West Texas Intermediate crossed US$80 per barrel over the same period. The oil price rally observed during this period reflects how quickly geopolitical risk can translate into commodity price movements when supply-access fundamentals are genuinely threatened.

The most striking data point was the 9.6% single-day gain in Brent crude recorded at peak escalation, the largest one-day increase since May 2020.

Market Signal: A 9.6% single-day move in Brent crude is not routine volatility. It reflects a market repricing fundamental supply-access risk rather than speculative positioning. The last comparable move occurred during the COVID-19 demand collapse of May 2020, under entirely different structural conditions.

The mechanism driving this repricing goes beyond the immediate price spike. Vivek Dhar, Head of Commodities and Sustainability Research at Commonwealth Bank, has identified the deeper dynamic at work: sustained conflict restarts the clock on global oil inventory depletion. Reduced transit capacity through the Hormuz corridor compresses supply availability to importing nations, drawing down strategic and commercial reserves faster than alternative routes can replenish them. That inventory depletion dynamic, rather than the headline price number itself, is the structural concern for long-term energy planners and procurement strategists.

LNG: The Underappreciated Exposure

The Qatari LNG tanker struck near Oman on 6 July carries implications that extend well beyond a single incident. It signals that LNG export infrastructure and associated vessel traffic are now within the active operational risk perimeter of the conflict.

Qatar is the world's largest LNG exporter, and its export model is entirely seaborne. There is no pipeline alternative for Qatari LNG. When maritime routes through Hormuz become operationally unreliable, the consequences flow directly to buyers in Japan, South Korea, India, and across Europe. Shifts in global LNG supply availability at this scale trigger immediate spot market responses as buyers activate contingency procurement strategies, including alternative crude grades, accelerated storage drawdowns, and spot purchases from Atlantic Basin suppliers.

Ships, Crew, and the Human Cost of Contested Transit

The United Arab Emirates confirmed that Iranian cruise missiles struck two of its oil tankers, the Mombasa and the Al Bahiyah, while they were transiting Omani waters. One crew member was killed and eight others were wounded. The IRGC claimed responsibility, asserting that the vessels had ignored repeated warnings before being disabled.

A separate incident near Qeshm Island saw a bulk carrier collide with another vessel, forcing an emergency evacuation of 23 foreign crew members, according to Iran's Fars news agency.

War-risk insurance premiums for Gulf transit have reached levels that make some voyages economically unviable without corresponding adjustments to cargo pricing. For tanker operators, the calculus has shifted from route optimisation to fundamental risk management.

The Transit Fee Dispute: A Legal and Commercial Flashpoint

President Trump announced a proposal to levy a 20% fee on vessels transiting the Strait of Hormuz to offset US security costs, a measure without precedent in international maritime law. Iran's Foreign Minister Abbas Araghchi responded publicly, suggesting the proposed figure was excessive while implying Tehran would develop its own framework for the waterway.

The International Maritime Organization moved quickly to reject the concept of unilateral transit tolls, citing established international law provisions guaranteeing free passage through international straits.

Legal Flashpoint: The IMO's position under the United Nations Convention on the Law of the Sea is unambiguous: international straits cannot be subject to unilateral tolls or charges. Any enforcement of such fees would represent a direct challenge to the foundational framework of international maritime law and would likely trigger legal proceedings from multiple flag states.

The transit fee proposal introduces a new commercial and legal dimension to an already complex crisis. Even if never formally implemented, the proposal creates uncertainty for shipping operators, cargo insurers, and flag-state governments that must factor the possibility into voyage risk assessments.

The next major ASX story will hit our subscribers first

Broader Implications: Energy Transition, Strategic Reserves, and Import Dependency

Price spikes of this magnitude carry secondary consequences that extend beyond the immediate commodity market reaction. Historically, sustained energy price shocks at this level delay the economics of fuel-switching in industrial and power generation sectors. Nations that had been accelerating coal-to-gas switching programmes may face temporary reversals as LNG spot prices climb. Renewable energy investment timelines are unlikely to be directly disrupted, but government fiscal capacity to sustain energy transition subsidy programmes may be constrained by broader macroeconomic pressures.

The crisis is simultaneously accelerating policy conversations about the adequacy of International Energy Agency strategic petroleum reserve release mechanisms. Several major economies are expected to coordinate strategic reserve releases if Brent sustains above the US$100 threshold. Over the longer term, this episode reinforces the investment case for energy diversification infrastructure, including alternative pipeline routes where technically feasible, floating LNG terminals, and demand-side flexibility programmes that reduce exposure to single-corridor supply risk.

Saudi Arabia's East-West Pipeline, known as Petroline, provides a partial alternative for crude oil, with capacity to carry some volumes to Red Sea terminals. However, it cannot absorb full Hormuz transit volumes. For LNG, no scalable alternative exists at all. This asymmetry in bypass capacity is precisely why the Hormuz strait carries disproportionate strategic weight relative to its modest physical dimensions. Consequently, understanding oil volatility trends in this context is essential for any market participant with Gulf energy exposure.

Frequently Asked Questions: Strait of Hormuz Crisis 2026

What percentage of global oil passes through the Strait of Hormuz?

Approximately 20% of global oil consumption transits the strait daily, alongside roughly 30% of the world's LNG supply, making it the single most consequential maritime energy chokepoint on Earth.

Is the Strait of Hormuz actually closed right now?

The situation is actively contested. Iran's IRGC has declared the strait closed. The US Central Command maintains that the waterway remains accessible and that Iran does not hold sovereign authority over it. In practice, significant numbers of vessels are diverting due to physical safety concerns, creating functional disruption regardless of the legal designation. Sky News' live coverage of the Iran-US conflict provides ongoing updates on the Strait of Hormuz shut again as US-Iran fighting restarts situation as it develops.

How high could oil prices go if the conflict continues?

Commonwealth Bank's commodity research team has modelled two key thresholds: Brent reaching approximately US$100 per barrel within 10 days of sustained conflict, and potentially US$150 per barrel within ten weeks if hostilities escalate to include energy infrastructure targeting.

What is the current status of ceasefire negotiations?

The 60-day ceasefire agreed in mid-June 2026 has effectively collapsed. Diplomatic channels through Qatari and Pakistani mediation remain active, but no new framework had been agreed as of mid-July 2026.

What alternative routes exist for Gulf oil and LNG exports?

Saudi Arabia's Petroline can carry partial crude volumes to Red Sea terminals, but cannot absorb full Hormuz throughput. For LNG, no viable pipeline alternative exists. Qatar's entire export programme is seaborne, which is why any sustained Hormuz disruption creates immediate spot market consequences for Asian and European buyers.

The 10-Day Window Markets Are Watching

Energy market analysts have identified the next ten days from the point of renewed escalation as the critical window for determining whether this episode remains a contained exchange or transitions into a sustained conflict phase. If Qatari and Pakistani diplomatic channels produce a new framework before that window closes, markets are likely to retrace a meaningful portion of the recent price premium.

If hostilities continue or expand, particularly if targeting logic shifts back toward energy infrastructure, the inventory depletion mechanism identified by commodity researchers will begin to manifest in physical supply data. At that point, price discovery enters genuinely uncharted territory where historical analogues provide limited guidance.

The Strait of Hormuz shut again as US-Iran fighting restarts is not a headline that energy markets can absorb as routine noise. It represents the re-emergence of the most consequential supply-access risk in the global energy system, operating through a geographic chokepoint that cannot be bypassed at volume and cannot be managed through demand-side responses alone. How the next weeks unfold will determine whether 2026 is remembered as the year the energy system absorbed an acute shock, or the year it failed to.

This article is intended for informational purposes only and does not constitute financial or investment advice. All price projections and scenario analyses referenced are drawn from independent commodity research and represent modelled outcomes under specified assumptions. Actual market outcomes will depend on geopolitical developments that remain highly uncertain. Readers should conduct their own due diligence before making any investment decisions.

For ongoing coverage of geopolitical developments affecting global energy markets, visit Energy Digital Magazine.

Want to Know Which ASX Resource Stocks Could Benefit From Rising Energy Commodity Prices?

When geopolitical shocks send commodity prices surging, the window to act on emerging ASX mineral discoveries can close rapidly — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant discoveries across more than 30 commodities so subscribers can make informed decisions ahead of the broader market. Explore historic examples of exceptional discovery outcomes and begin your 14-day free trial today to position yourself before the next major market move.