July 10, 2026

The Anatomy of a Chokepoint Collapse: Understanding What Happens When Hormuz Stops Moving

Every decade or so, global energy markets receive a sharp reminder that the architecture of modern oil supply rests on a handful of geographic pressure points. The Strait of Hormuz tanker traffic near standstill has become the defining energy story of 2025, with this narrow waterway separating the Arabian Peninsula from Iran sitting at the top of that list. At its narrowest, the strait measures roughly 33 kilometres across, yet through this sliver of water flows approximately one-fifth of the world's entire oil supply and around 25% of global liquefied natural gas trade. No pipeline network, no alternative sea route, and no combination of strategic reserves can fully substitute for what moves through Hormuz on a normal day.

Understanding why a disruption here cascades so rapidly into global markets requires more than a news headline. It demands a structural analysis of how the waterway functions, what conditions allow commerce to flow, and what specific mechanisms cause that flow to cease almost entirely.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: More Than a Geographic Feature

Why No Alternative Can Replace It

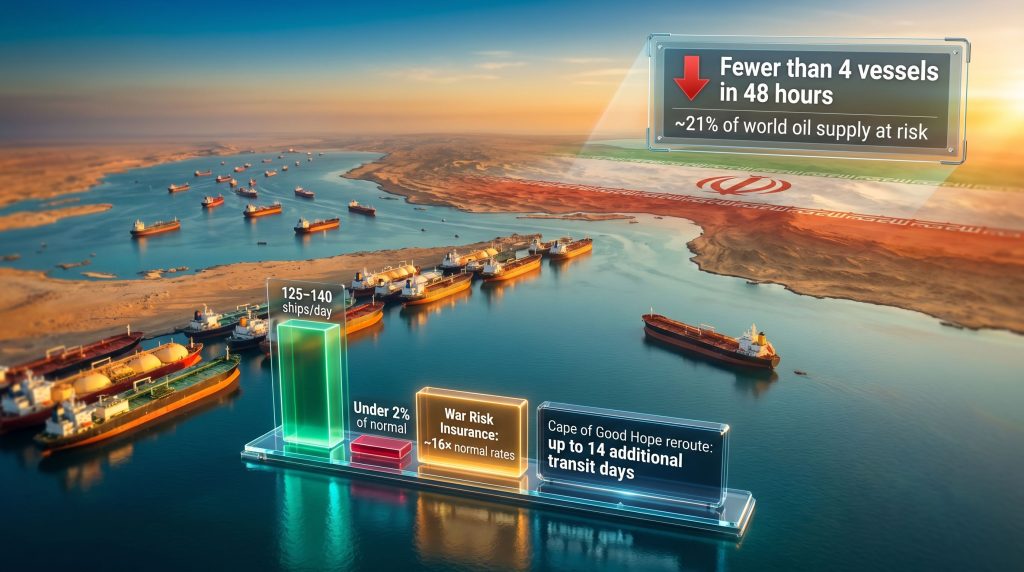

The Strait of Hormuz occupies a position in global energy logistics that has no true equivalent. Saudi Arabia operates the East-West Pipeline, which can redirect some crude exports to the Red Sea, and the UAE has developed the Abu Dhabi Crude Oil Pipeline with capacity to bypass the strait. However, combined alternative pipeline capacity falls far short of replacing total Hormuz throughput, which under pre-conflict conditions averaged between 125 and 140 vessel transits per day.

That daily figure includes crude oil tankers, LNG carriers, refined product tankers, bulk carriers, and container vessels. Furthermore, the pre-conflict baseline was not simply an oil story. Agricultural commodities, industrial goods, and consumer imports destined for Gulf states all moved through the same narrow corridor. Monitoring current crude oil prices reveals just how sensitively markets react to even partial disruptions along this route.

The Physical Constraints That Amplify Risk

The inbound and outbound shipping lanes within the strait are each only two miles wide, separated by a two-mile buffer zone. This extreme concentration of traffic within a confined space means that even a limited number of hostile incidents, mines, or drone strikes can deter the far larger population of vessels that have not been directly targeted.

Risk perception in shipping operates exponentially: one successful attack on a tanker does not deter 1% of traffic; it can suspend decisions across entire fleets as shipowners and insurers reassess every voyage through the affected zone.

How Severe Is the Current Disruption?

The Numbers Behind the Near Standstill

The deterioration from normal operating conditions to what analysts are now describing as a near standstill has been rapid and severe. In the immediate aftermath of the latest escalation cycle, fewer than four vessel transits were recorded across a 48-hour window, representing under 2% of normal daily throughput. The two vessels confirmed by shipping data analytics firm Kpler as having transited the strait included a sanctioned Iranian crude supertanker and a chemical tanker with prior loading destinations in the UAE, neither of which represents mainstream commercial navigation.

The broader picture of stranded capacity is equally striking. Industry estimates suggest more than 150 ships are currently immobilised within Gulf waters, with an additional 700 or more vessels waiting at anchorages outside the strait for conditions to improve.

| Metric | Pre-Conflict Normal | Current Status |

|---|---|---|

| Daily Vessel Transits | 125-140 ships/day | Under 2% of normal throughput |

| Vessels Stranded in Gulf Waters | Negligible | 150+ ships; 700+ vessels waiting |

| War Risk Insurance Premium | Baseline rate | Approximately 16x normal rates |

| Rerouting Penalty (Cape of Good Hope) | Not applicable | Up to 14 additional transit days |

| Share of Global Oil Supply at Risk | Minimal | ~21% of world oil; ~25% of global LNG |

The AIS Blackout Problem

One underappreciated dimension of the current crisis is that official transit figures almost certainly understate actual vessel movements. Shipping industry sources have confirmed that an increasing number of vessels are disabling their Automatic Identification System (AIS) transponders before approaching or transiting the strait. AIS, which is mandatory under international maritime law for most commercial vessels, broadcasts a vessel's identity, position, speed, and heading. When transponders go dark, the ship effectively disappears from publicly accessible tracking systems.

This means analysts relying on AIS data to count transits are working with incomplete information. The true scale of disruption, including how many vessels have successfully passed through versus how many have attempted and turned back, remains partially obscured. What is clear is that even accounting for dark vessel movements, total throughput is a fraction of pre-conflict norms.

Directional Asymmetry as a Strategic Signal

One particularly revealing pattern in the disruption data is the near-complete collapse of eastbound traffic relative to the modest residual westbound movements. Vessels carrying exports from Gulf producers continue to make occasional transits, often through pre-arranged passage or under sanctioned operator status, while inbound commercial traffic carrying imports to Gulf economies has effectively ceased. This directional asymmetry suggests a degree of selective control over the waterway rather than a complete physical blockade, a distinction with significant implications for how the situation may evolve.

The Escalation Sequence That Froze Shipping

A Four-Month Conflict Reaches a Critical Threshold

The current phase of disruption traces its immediate origins to the conflict that erupted on February 28, when U.S. and Israeli military operations against Iran initiated a chain of retaliatory actions that progressively degraded the commercial viability of Hormuz transit. The strait did not close overnight. For several weeks, daily transits averaged around 40 ships, which, while dramatically reduced from the pre-conflict norm, still represented a functioning, if constrained, shipping corridor.

The tipping point arrived with three separate tanker attacks within a single week, an escalation threshold that fundamentally shifted the risk calculus for commercial operators. The attacks were attributed by U.S. officials to Iranian forces, and Iran's Revolutionary Guards Navy subsequently issued warnings that external interference in redirecting shipping would draw severe consequences. For shipowners already managing elevated war risk premiums, three attacks in seven days crossed from manageable risk into operationally unacceptable territory. The oil price geopolitics driving this situation have been building for months, with geopolitical trade tensions reshaping shipping decisions globally.

The Al Rekayyat Incident: A Case Study in Vulnerability

Among the three targeted vessels, the Marshall Islands-flagged LNG tanker Al Rekayyat has drawn particular attention. A projectile strike late on a Tuesday ignited a fire in the vessel's engine room, leaving it stranded off the coast of Oman and awaiting salvage. The incident highlighted a dimension of the crisis that extends beyond crude oil markets: LNG carriers transiting Hormuz serve importing nations across Asia and Europe, and a confirmed attack on one sends an immediate signal to the operators of dozens of similar vessels.

Industry sources indicated that while initial fears of a catastrophic explosion subsided, the vessel's cargo remained in a precarious situation, and no injuries or environmental incidents had been confirmed by the Marshall Islands ship registry. The salvage timeline alone introduces weeks of uncertainty for operators weighing similar routes.

The Insurance Crisis Compounding the Disruption

War Risk Premiums at Historically Extreme Levels

The insurance dimension of the Hormuz crisis may be the most underappreciated factor driving the shipping standstill. War risk insurance premiums for voyages through the strait have reached approximately 16 times their normal baseline rates, a level that fundamentally alters voyage economics for most commercial operators. At these premium levels, a voyage that was marginally profitable under normal conditions becomes loss-making before a single barrel of cargo is loaded.

Marine war underwriters are not simply raising prices; some have advised shipping companies to suspend voyages entirely while others are reviewing their policy terms in light of the sustained vessel loss risk. As one anonymous marine war underwriter noted through Reuters, "the market is now confronting the realistic prospect of severe financial losses tied to vessels of significant value", a professional assessment that carries enormous practical weight for operators seeking coverage.

The Mine Threat: The Invisible Deterrent

Beyond drone strikes and naval harassment, the spectre of sea mines represents a particularly potent deterrent because it is invisible and persistent. Unlike a naval vessel that can be tracked or an aircraft that can be identified, a deployed mine creates an area-denial effect that persists until confirmed clearance operations are completed.

Shipowners are explicit about this: no amount of political assurances or signed agreements will prompt a return to full commercial navigation until verified mine-free corridors are established and independently confirmed. This single factor may extend the timeline for traffic recovery well beyond what political negotiations alone can achieve.

Global Supply Chain Consequences

Oil Price Response and Rerouting Economics

Brent crude has responded to the escalating disruption with a surge of approximately 5% as confidence in the June 17 U.S.-Iran agreement eroded following the latest attacks. The price response, while significant, arguably understates the structural disruption given that strategic petroleum reserves among major consuming nations have been drawn down from levels available during previous Gulf crises.

The Cape of Good Hope reroute, which adds up to 14 additional transit days compared to the Hormuz passage, imposes compounding costs across the entire supply chain. Longer voyages require more fuel, tie up vessel capacity for extended periods, and reduce the effective availability of tanker tonnage globally. Consequently, when dozens of operators simultaneously pivot to the southern African route, freight rates on that corridor spike, creating a secondary inflationary pressure on delivered energy costs.

LNG and Non-Energy Cargo Exposure

Asian LNG importers, particularly those in Japan, South Korea, and China that rely on long-term supply contracts routed through Hormuz, face the most acute short-term exposure. The disruption to global LNG supply from this single chokepoint is already being felt across Asian spot markets. Unlike crude oil, LNG cannot be stored in large volumes at destination terminals, and any sustained supply gap requires immediate market response.

In addition, the container shipping and bulk carrier segments are also absorbing the disruption, as Gulf states import substantial volumes of food, electronics, and industrial materials through the same corridor.

The next major ASX story will hit our subscribers first

The Path to Reopening: Conditions and Scenarios

Why the June 17 Agreement Has Not Restored Traffic

The agreement reached between the U.S. and Iran on June 17 established a formal framework for ceasing hostilities, but the practical gap between a signed document and resumed commercial navigation has proven wider than markets initially anticipated. Ship broker Clarksons described the reopening narrative as increasingly fragile following the latest escalation, and daily transit data has confirmed that assessment.

Commercial operators apply a different standard than diplomats. A ceasefire agreement addresses the parties to a conflict; it does not deactivate deployed mines, repair damaged infrastructure, or restore underwriter confidence overnight. The risk perception embedded in current war risk premiums will not dissolve on the basis of political statements alone.

Four Conditions Shipowners Are Waiting For

Based on industry communications and broker analysis, four conditions broadly need to be met before mainstream commercial navigation resumes:

- Verified mine clearance along designated transit corridors, confirmed by independent naval or maritime authority assessment

- Sustained ceasefire adherence over a meaningful period, not measured in days but in weeks, without further vessel incidents

- War risk premium normalisation to levels that allow profitable voyage economics for standard commercial cargo

- Clear chain of command regarding who controls passage permissions, with transparent communication to vessel operators

| Scenario | Probability Driver | Expected Timeline | Oil Market Impact |

|---|---|---|---|

| Full Reopening (120+ ships/day) | Verified mine-free corridors + sustained ceasefire | 4-8 weeks minimum | Brent crude price normalisation |

| Partial Recovery (40-60 ships/day) | Selective safe passage agreements | 2-4 weeks | Moderate price relief |

| Prolonged Standstill | Further military escalation | Indefinite | Sustained supply premium |

| Alternative Route Dependency | Cape of Good Hope becomes default | Ongoing | Structural freight cost inflation |

What the Hormuz Crisis Exposes About Energy System Design

Single-Point-of-Failure Risk at Global Scale

The current disruption is functioning as an unplanned stress test of the global energy system's resilience against chokepoint failure. The results are not encouraging. Despite decades of awareness that Hormuz represented a single-point-of-failure risk, no credible alternative infrastructure has been developed at the scale needed to absorb a full closure.

Pipeline bypass capacity remains insufficient, strategic reserves provide a buffer measured in weeks rather than months at sustained disruption volumes, and the rerouting capacity of the global tanker fleet is finite. OPEC market influence over supply decisions is also being tested in ways not seen since the 1970s, with member states unable to easily compensate for lost transit capacity.

Geopolitical Risk Repricing

Beyond the immediate market response, the crisis is prompting a longer-term reassessment of geopolitical risk pricing in energy investments. Long-term supply contracts, infrastructure financing for Gulf-adjacent energy projects, and the valuation of tanker fleets are all being revised against a background of structural uncertainty that the June 17 agreement has not resolved.

Analysts tracking leading indicators of recovery are focused less on political statements and more on three specific metrics: daily AIS-confirmed transit counts, war risk premium trajectories, and the progress of any independent mine clearance operations.

The current Strait of Hormuz tanker traffic near standstill is not simply a shipping story. It is a live demonstration of how physical geography, market psychology, insurance economics, and geopolitical conflict interact to determine whether the arteries of global trade remain open.

Frequently Asked Questions: Strait of Hormuz Tanker Traffic Standstill

How much of the world's oil supply passes through the Strait of Hormuz?

Under normal pre-conflict conditions, approximately 21% of global oil supply and around 25% of global LNG trade transited the Strait of Hormuz daily, carried by between 125 and 140 vessels of various types.

Why has tanker traffic through the Strait of Hormuz essentially stopped?

A combination of direct vessel attacks, escalating drone and naval activity, war risk insurance premiums reaching 16 times normal rates, and the unresolved threat of deployed sea mines has made commercial operators unwilling to risk transits under current conditions. Recent tracking data from CNBC confirms how dramatically throughput has collapsed.

What happens to oil prices if the Strait of Hormuz remains closed?

Brent crude has already risen approximately 5% in response to the latest escalation. A prolonged closure would introduce a sustained supply premium into global oil prices, with the severity depending on how much alternative pipeline and reserve capacity consuming nations can deploy.

How are shipping companies responding to the Hormuz disruption?

Most commercial operators have suspended scheduled transits. Some are rerouting via the Cape of Good Hope, accepting the 14-day transit penalty. Others are holding vessels at anchorage outside the strait, waiting for conditions to stabilise before committing to a passage.

What is the Cape of Good Hope reroute and how does it affect costs?

Rerouting around the southern tip of Africa instead of passing through the Strait of Hormuz adds approximately 14 days to a typical voyage. This increases fuel consumption, reduces effective tanker fleet availability, and drives freight rates higher on the alternative corridor, raising delivered energy costs globally.

Has the U.S.-Iran ceasefire reopened the Strait of Hormuz?

Not to any meaningful degree. Even before the latest attacks, daily transits had only recovered to around 40 vessels, less than one-third of the pre-conflict average. Following the most recent escalation, transits collapsed to near zero within a 48-hour window, reflecting the persistent Strait of Hormuz tanker traffic near standstill.

What are war risk insurance premiums and why have they surged?

War risk insurance covers vessel operators against losses caused by military action, mines, or armed conflict in designated high-risk zones. Premiums in the Hormuz region have risen to approximately 16 times their pre-conflict baseline, reflecting the direct vessel losses already sustained and the ongoing threat environment assessed by underwriters.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or trading advice. Forecasts, scenarios, and market projections referenced herein involve inherent uncertainty and should not be relied upon as the basis for any investment decision. Readers should conduct independent research and consult qualified advisors before making any financial commitments related to the topics discussed.

For ongoing coverage of Strait of Hormuz shipping developments and U.S.-Iran geopolitical dynamics, Reuters provides regularly updated reporting at Reuters.com.

Want to Stay Ahead of the Next Major Commodity Market Shock?

When geopolitical disruptions like the Strait of Hormuz standstill ripple through global energy and commodity markets, timing is everything — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly identifying actionable opportunities across 30+ commodities before the broader market reacts. Begin your 14-day free trial at Discovery Alert and position yourself ahead of the next major market move.