July 14, 2026

The Anatomy of a Chokepoint Crisis: Understanding Why Hormuz Recovery Is Measured in Months, Not Days

The global energy system has long operated with a structural vulnerability hiding in plain sight. A single waterway, barely 21 nautical miles across at its narrowest point, serves as the circulatory valve for roughly one-fifth of the world's combined oil and natural gas exports. When that valve closes, the consequences do not ripple outward uniformly. They cascade through commodity markets, food supply chains, insurance underwriting desks, and diplomatic back-channels simultaneously. The Strait of Hormuz traffic recovery now underway in mid-2026 offers a rare real-time case study in how the world's most consequential maritime chokepoint attempts to heal itself after its deepest wound in recorded history.

When big ASX news breaks, our subscribers know first

The Closure That Rewrote the Record Books

When Iran shut the Strait of Hormuz on March 1, 2026, following US-Israeli military strikes, the decision represented far more than a tactical disruption. It became the longest sustained closure of this waterway since modern maritime records began, surpassing the tension-driven slowdowns recorded during the Iran-Iraq War era of the 1980s.

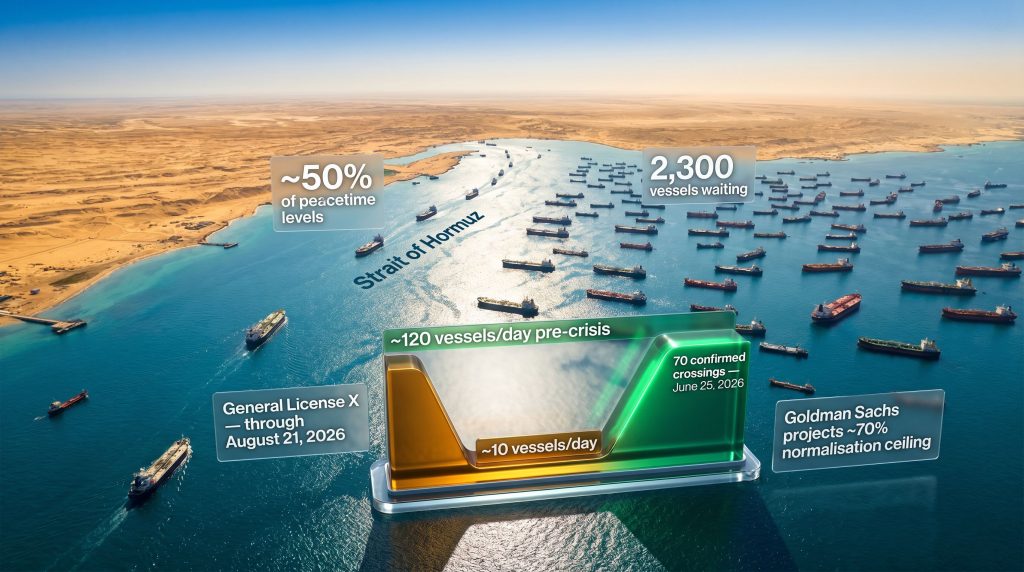

The scale of the collapse was staggering. A waterway that typically processes approximately 120 vessel crossings per day across all commodity categories was reduced to roughly 10 crossings per day during peak closure conditions. That is a contraction exceeding 90%. The practical effect was to strand an estimated 11,000 seafarers within the Gulf, triggering one of the largest coordinated maritime humanitarian operations in modern history.

To understand why full Strait of Hormuz traffic recovery remains so elusive, it helps to understand what the strait actually carries under normal conditions:

- Crude oil: The dominant cargo type, sourced from Saudi Arabia, Iraq, Kuwait, the UAE, and Iran

- Liquefied natural gas (LNG): Particularly from Qatar's vast North Field export terminals, supplying Asian and European buyers. This disruption to global LNG supply reverberated across markets from Tokyo to Rotterdam

- Refined petroleum products: Including jet fuel, diesel, and naphtha bound for refinery-scarce import markets

- Dry bulk cargo: Fertilisers such as potash and urea, representing a critical agricultural input supply chain often overlooked in energy-focused analysis

Each of these categories carries distinct economic and geopolitical weight. The closure did not simply interrupt oil markets. It simultaneously threatened food production cycles dependent on Gulf-sourced fertiliser inputs.

Traffic Recovery Data: What the Numbers Actually Reveal

The Strait of Hormuz traffic recovery that began around June 15, 2026 represents a measurable but incomplete rebound. The data, drawn from vessel tracking platforms including Kpler and AXSMarine, tells a nuanced story.

| Metric | Value | Reference Period |

|---|---|---|

| Pre-crisis daily average | ~120 vessels/day | Pre-March 2026 |

| Crisis-period average | ~10 vessels/day | March 1 to June 14, 2026 |

| Peak single-day recovery crossing count | 70 confirmed crossings | June 25, 2026 |

| Commodity vessels on peak day | 56 vessels | June 25, 2026 |

| Dry bulk crossings on peak day | 22 crossings | June 25, 2026 |

| Mid-morning crossings the following day | 15 by midday | June 26, 2026 |

| Traffic as a share of peacetime baseline | ~50% | Late June 2026 |

The 70-crossing figure recorded on June 25, confirmed by analytics firm Kpler, marked the highest single-day total since the March 1 closure. However, framing this as a recovery milestone requires important qualification: it still represents less than 60% of the pre-war daily baseline. The gap between where traffic stands today and where it needs to be remains significant.

The Dry Bulk Signal: An Underappreciated Indicator

One of the more technically significant data points within the recovery dataset was recorded by maritime tracker AXSMarine: dry bulk tanker traffic through the strait reached its 2025 baseline level for the first time since March 1, driven by the 22 crossings logged on June 25.

This matters beyond the headline number. Dry bulk cargo, encompassing fertilisers and agricultural inputs, had been among the most severely disrupted categories throughout the closure period. Unlike crude oil, which commands immediate geopolitical attention, fertiliser supply disruptions operate on a slower damage timeline, accumulating silently through planting season delays and input cost inflation.

The restoration of dry bulk flows to prior-year baseline levels signals early relief for agricultural supply chains that had been absorbing elevated costs for nearly four months.

AIS Transponder Activity as a Confidence Proxy

A lesser-appreciated metric within the Strait of Hormuz traffic recovery analysis is the rate at which vessels are operating with their Automatic Identification System (AIS) transponders active. During peak conflict conditions, many commercial operators disabled AIS to reduce targeting risk, a practice that also severely distorted traffic measurement accuracy.

The progressive return to AIS-on operations functions as a real-time sentiment indicator. When shipowners are willing to broadcast their vessel's identity and position, they are effectively signalling that their internal risk calculus has shifted in favour of transit. The growing proportion of AIS-active vessels in late June 2026 represents a measurable shift in commercial operator confidence, even if that confidence remains fragile and conditional.

The Three-Part Diplomatic Architecture Behind the Recovery

The partial Strait of Hormuz traffic recovery did not emerge organically from a reduction in hostilities. It was enabled by a specific and interconnected set of diplomatic and regulatory developments that created the conditions under which commercial operators felt sufficiently confident to resume transit activity.

The June 14 Memorandum of Understanding

The US-Iran Memorandum of Understanding signed on June 14, 2026 established the first structured diplomatic channel between the two parties since the conflict escalated. Crucially, vessel crossing data confirms a measurable inflection point beginning on June 15, with daily traffic trending upward in successive days. The MOU did not immediately restore unrestricted transit rights, but it created the political conditions under which the risk-reward calculation for commercial operators began to shift.

General License X and the Sanctions Clarity Problem

One of the most underappreciated barriers to traffic recovery was not physical danger but legal uncertainty. Sanctions exposure had effectively paralysed buyers, traders, and financial institutions, many of whom could not determine whether transacting in Gulf-origin commodities would trigger secondary sanctions penalties.

The US Treasury's issuance of General License X resolved this ambiguity by authorising transactions involving Iranian-origin oil and petrochemical products through August 21, 2026. This temporary mechanism provided a defined legal window during which market normalisation could proceed. Without this clarification, commercial operators would have faced continued paralysis regardless of physical safety conditions.

The Direct US-Iran Maritime Communication Channel

The establishment of a direct US-Iran communication channel for maritime coordination introduced a practical confidence-building mechanism. While this channel does not represent political normalisation, it provides a functional framework for managing incident risk in real time. Market participants have identified it as a material factor in reducing the perceived probability of vessel interception during transit.

The Structural Barriers Preventing Full Normalisation

Despite the diplomatic architecture described above, the Strait of Hormuz traffic recovery faces a set of structural obstacles that diplomatic progress alone cannot resolve on a short timeline. Furthermore, these barriers interact with one another, meaning progress on one front does not automatically unlock progress on another.

The 2,300-Vessel Backlog

As of June 21, 2026, approximately 2,300 vessels were holding position in the Gulf and Gulf of Oman awaiting clearance to transit, according to maritime tracking data. This included 1,566 cargo ships, 705 tankers, and 255 fully loaded oil tankers ready for immediate export dispatch.

The mathematics of this backlog are sobering. Even under a scenario in which daily crossings doubled from current levels, processing all waiting vessels would require weeks of sustained throughput. The asymmetry between inbound recovery traffic and outbound stagnation is the most acute near-term bottleneck for global commodity markets. Some live tracking platforms recorded zero active outbound commercial movements as of early June 23, highlighting that export flows remain severely constrained even as inbound traffic recovered.

Iran's Selective Permit System

Lloyd's List Editor-in-Chief Richard Meade described Iran's approach to northern route access as one of selective permits and phased agreements, with Tehran maintaining tight administrative control over which vessels are authorised to transit and when. This is a fundamentally different operational environment from the pre-war toll-free corridor at the centre of the waterway.

Meade also warned that vessels using the southern Omani corridor under US Navy monitoring should not interpret access through that route as an indicator of broader normalisation. The two routes operate under entirely different risk and authorisation frameworks. Consequently, the oil market disruptions stemming from this bifurcated access system continue to weigh heavily on global supply chains.

Mine Clearance: The Physical Constraint Diplomacy Cannot Dissolve

European naval minesweeping vessels transited the Red Sea in late June 2026 en route to the strait to begin clearing mines blocking safe navigation of the primary corridor. This physical constraint represents a hard timeline bottleneck. Until the main navigational corridor is certified as mine-free, commercial operators must choose between higher-risk transit, alternative routing, or continued waiting.

Mine clearance is a methodical, time-intensive operation that cannot be accelerated by political will alone. It requires systematic sonar sweeping, mine identification, and neutralisation across a defined waterway under conditions that remain operationally sensitive.

Tehran's June 26 Warning: A Legal Confrontation With International Maritime Law

On June 26, 2026, Iran formally warned that vessels crossing the strait without Iranian authorisation would face consequences. This statement places Tehran in direct legal conflict with the United Nations Convention on the Law of the Sea (UNCLOS), which classifies the Strait of Hormuz as an international transit passage zone through which all vessels have the right of passage.

The practical effect is a de facto permit requirement imposed unilaterally by Iran, regardless of the legal framework under which commercial operators believe they are operating. For shipowners, this creates a binary risk scenario: comply with Iran's permit process and navigate administrative delays, or transit under UNCLOS protections and risk enforcement action.

Analyst Projections: What Full Recovery Actually Looks Like

Goldman Sachs has projected that Strait of Hormuz traffic may stabilise at approximately 70% of pre-crisis normal levels following the initial rebound phase, implying that a structural shortfall of roughly 30% may persist even after acute tensions subside. This projection carries significant implications for oil and LNG markets, particularly given the 255 fully loaded oil tankers queued and waiting to export.

The broader crude oil price dynamics at play here are deeply interconnected with the pace of Hormuz normalisation. Shipping industry experts and maritime analysts broadly assess that full normalisation will require weeks to months, contingent on several concurrent developments:

- Completion of mine-clearing operations in the primary navigational corridor

- Resolution of the legal framework governing vessel passage rights under UNCLOS versus Iran's permit system

- Systematic drawdown of the approximately 2,300-vessel backlog

- Sustained absence of new security incidents capable of resetting commercial operator confidence

- Convergence of vessel routing back toward the central corridor as a leading indicator of genuine operational normalisation

The current pattern of ships using dispersed and fragmented routes, rather than the pre-war central corridor, is itself an indicator that analysts monitor closely. Route consolidation back toward the primary corridor would represent a meaningful normalisation signal.

The next major ASX story will hit our subscribers first

The Humanitarian and Commercial Traffic Tension

The UN-coordinated evacuation plan for approximately 11,000 stranded seafarers, which commenced on June 24, 2026, introduced an additional complexity into the traffic management equation. Evacuation vessel movements and commercial cargo transits are competing for the same limited daily permit allocations under Iran's selective access system.

Two Maersk vessels successfully exited the Gulf on June 25 and 26 respectively, with three additional Maersk ships still awaiting clearance. The phasing of humanitarian and commercial movements through a constrained approval bottleneck means that prioritisation decisions carry real economic costs alongside their humanitarian dimensions.

Energy Market Implications: The Deferred Supply Pressure

With 255 fully loaded oil tankers queued in the Gulf, the potential release of this stored supply into global markets represents a meaningful downward price pressure variable. Once outbound flows resume at scale, the concentrated discharge of weeks of accumulated export inventory could weigh on crude oil benchmarks in the near term. However, longer-term supply uncertainty maintains a structural geopolitical risk in commodities that is unlikely to dissipate quickly.

LNG markets, particularly in Asia, face a disproportionate impact given the concentration of Gulf LNG export infrastructure. Asian buyers who had been forced to source alternative supply during the closure period have in many cases locked in replacement contracts at elevated prices, creating both a cost legacy and a contract renegotiation dynamic as Hormuz access gradually resumes.

War risk insurance premiums for Gulf transits surged dramatically following the March 1 closure and are likely to remain elevated. Underwriters are unlikely to normalise pricing until the corridor is physically certified as mine-free, the legal framework governing passage rights is clarified, and a sustained period without new security incidents has been established. This insurance premium functions as a persistent hidden cost embedded in every cargo transiting the strait during the recovery period.

Frequently Asked Questions: Strait of Hormuz Traffic Recovery

What percentage of normal traffic has been restored through the Strait of Hormuz?

As of late June 2026, traffic has recovered to approximately 50% of its pre-crisis peacetime level. The single highest daily count recorded during the recovery phase reached 70 confirmed crossings, compared to a pre-war baseline of approximately 120 vessels per day.

Why is traffic recovering but not yet normalised?

Several structural barriers prevent full normalisation: Iran's selective permit system for northern route access, ongoing mine-clearing operations in the primary corridor, a backlog of approximately 2,300 vessels awaiting transit, and legal ambiguity over passage rights following Tehran's June 26 warning.

What triggered the partial recovery in Strait of Hormuz shipping?

Three concurrent developments catalysed the recovery: the US-Iran Memorandum of Understanding signed June 14, 2026; the US Treasury's issuance of General License X authorising Iranian-origin commodity transactions through August 2026; and the establishment of a direct US-Iran maritime communication channel. The oil price shock that preceded these diplomatic efforts had, in part, created the political urgency to reach an agreement.

How long will full Strait of Hormuz traffic recovery take?

Shipping industry analysts project that full normalisation could require weeks to months. Goldman Sachs has projected that traffic may stabilise at approximately 70% of pre-crisis levels even after the initial rebound phase concludes, suggesting a persistent structural shortfall in the near term.

What commodities are most affected by the Strait of Hormuz disruption?

The most significantly affected commodity categories include crude oil, liquefied natural gas, and dry bulk cargo, particularly fertilisers and agricultural inputs. As of late June 2026, 255 fully loaded oil tankers remained queued in the Gulf awaiting outbound clearance. According to maritime intelligence reporting, international operators remain notably cautious despite the modest traffic rebound.

What is Iran's current position on vessel transit through the strait?

Iran has formally warned that vessels crossing without Iranian authorisation will face consequences. Tehran is managing northern route access through a selective permit and phasing system, effectively imposing discretionary control over commercial transit despite the strait's international transit passage designation under UNCLOS.

This article contains forward-looking assessments and analyst projections regarding Strait of Hormuz traffic recovery timelines and commodity market impacts. These projections involve significant uncertainty and should not be interpreted as investment advice. Maritime conditions, diplomatic developments, and geopolitical risk factors may change rapidly. Readers are encouraged to consult primary data sources and seek independent professional advice before making decisions based on information contained herein.

Want to Invest Ahead of the Next Major Commodity Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly cutting through complex market data to surface actionable opportunities — particularly relevant as geopolitical shocks like the Hormuz closure continue to reshape global commodity supply chains. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market shift.