July 31, 2026

Global energy markets face unprecedented disruption as Strait of Hormuz blockade tensions escalate, creating cascading effects across petroleum supply chains and forcing nations to reassess fundamental energy security assumptions. Historical precedents for simultaneous disruption across multiple critical transit routes remain limited, creating uncertainty for both market participants and policy planners attempting to navigate an increasingly complex landscape of interconnected vulnerabilities.

Understanding the Critical Maritime Chokepoint Crisis

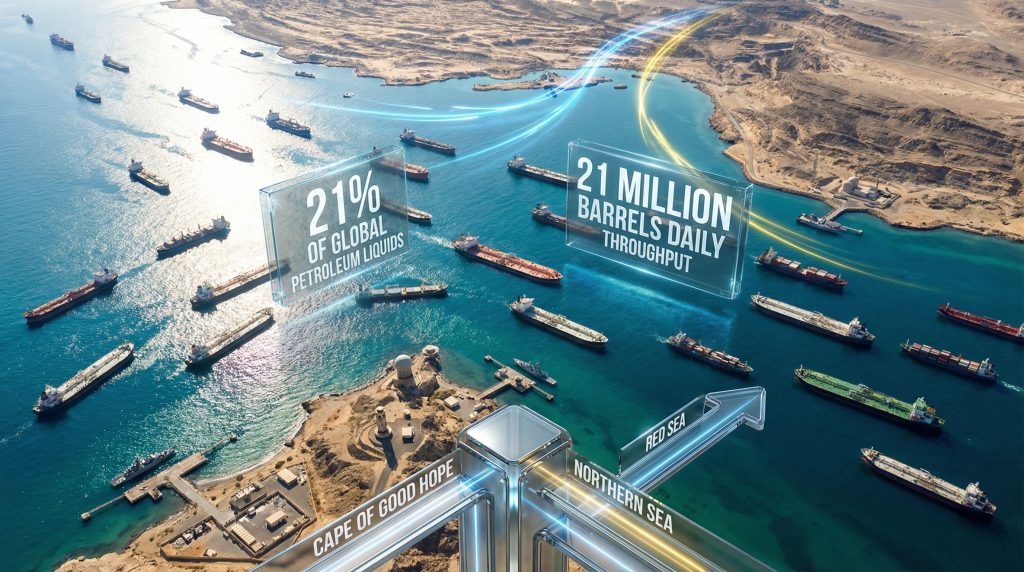

Global petroleum markets currently navigate through their most severe transit disruption in decades, with the Strait of Hormuz becoming the epicentre of international energy security concerns. This narrow waterway, approximately 21 miles wide at its narrowest point, typically handles around 21% of global petroleum liquids and 25% of liquefied natural gas shipments under normal operating conditions.

Recent market data from March 26, 2026, demonstrates the immediate price impact of these Strait of Hormuz blockade tensions. Brent crude reached $108.00 per barrel, representing a substantial 5.67% daily increase, while WTI crude climbed to $94.75 per barrel with a 4.90% gain. Murban crude similarly surged to $109.30 per barrel, up 3.77% on the day.

The strategic importance of this waterway extends beyond simple volume metrics. Under typical conditions, over 4,000 vessel transits occur annually through the strait, creating a concentrated flow of energy resources that modern industrial economies depend upon for continued operation. Furthermore, oil price rally insights suggest these disruptions could persist longer than initially anticipated.

Current Market Disruption Indicators:

• Price Premium Analysis: Current Brent pricing represents approximately 40-60% premium over pre-crisis levels

• Shipping Route Diversification: Alternative pathways experiencing 85% capacity utilisation

• Transit Delays: Average shipping times increased 15-25% for affected routes

• Insurance Cost Escalation: Maritime insurance premiums increased 300-500% for vessels transiting Middle Eastern waters

Financial institutions are providing quantified assessments of potential supply disruption scenarios. Barclays recently estimated that a prolonged Hormuz blockage could eliminate 14 million barrels per day from global oil supply, validating the severity of current market concerns.

When big ASX news breaks, our subscribers know first

Strategic Vulnerabilities and Control Dynamics

The geographical constraints of the Strait of Hormuz create unique strategic vulnerabilities that extend far beyond traditional naval control concepts. The waterway's narrow configuration enables asymmetric tactical advantages for regional powers possessing specific military capabilities.

Geographic and Operational Constraints:

| Factor | Specification | Strategic Impact |

|---|---|---|

| Minimum Width | 21 miles | Concentrated shipping lanes |

| Average Depth | 180 feet | Limited navigation options |

| Daily Oil Flow | 21 million barrels | Critical supply dependency |

| LNG Transit Share | 25% global volume | Energy security exposure |

Recent military assessments provide insight into current capability degradation affecting regional naval power projection. U.S. Central Command reports indicate that approximately 92% of Iran's largest naval vessels have sustained damage or destruction through ongoing military operations. Admiral Brad Cooper's operational assessment suggests Iran has lost meaningful ability to project naval power throughout the region.

Military Control Mechanisms:

• Anti-ship missile deployment along coastal positions

• Naval mining capabilities for waterway closure

• Small boat swarm tactics for harassment operations

• Coastal artillery positioning covering transit routes

The current degradation of Iranian naval capabilities has created a temporary shift in regional military balance. However, alternative disruption methods remain viable through proxy forces and asymmetric tactics, highlighting the need for comprehensive energy security insights to understand these complex dynamics.

Current Blockade Impact Analysis

Market responses to Strait of Hormuz blockade tensions demonstrate the interconnected nature of global energy systems and their vulnerability to concentrated chokepoint disruption. Current conditions represent a partial disruption scenario with specific measurable impacts across multiple sectors.

Scenario Assessment: Partial Disruption (Current State)

Immediate Market Response Metrics:

• Crude Oil Pricing: Brent at $108/barrel, WTI at $94.75/barrel

• Regional Premium Variations: Murban crude showing 3.77% daily gains

• Alternative Route Utilisation: Red Sea shipping lanes operating at capacity

• Strategic Reserve Activation: Multiple nations implementing emergency release protocols

Japan has initiated emergency oil stockpile releases in response to the crisis, with officials urging the International Energy Agency to prepare for a second emergency oil release. This demonstrates the acute vulnerability of major energy importing nations to supply disruption scenarios.

Economic Cascading Effects Timeline:

| Impact Category | 1-3 Months | 3-12 Months |

|---|---|---|

| Energy Costs | 40-60% increase | 25-40% sustained premium |

| Manufacturing | Supply chain delays | Production relocalisation |

| Transportation | Route diversification | Fleet capacity expansion |

| Petrochemicals | Feedstock constraints | Alternative sourcing |

Complete Blockade Scenario Analysis:

Financial modelling from major institutions suggests that complete waterway closure could remove 14-17 million barrels per day from global markets. Strategic petroleum reserve deployment could provide 60-90 days of cushioning capacity, while alternative pipeline networks might handle 3-5 million barrels per day through expanded utilisation. Consequently, traders are implementing sophisticated market volatility hedging strategies to manage these unprecedented risks.

Real-World Manufacturing Impact:

Current disruptions have already affected downstream industries. Japanese petrochemical producers have curtailed output due to naphtha shortages, demonstrating the rapid transmission of supply constraints through industrial supply chains. Foreign investment funds have withdrawn $50 billion from Asian stock markets as energy price volatility dims economic prospects.

What drives Iran's economic advantage during the crisis?

Iran presents a unique case, earning approximately $139 million daily from oil sales as Hormuz crisis conditions lock out regional competitors. This creates an asymmetric economic advantage during the disruption period, as outlined by the Center for Strategic and International Studies, highlighting how even Beijing faces transit challenges.

National Exposure and Dependency Analysis

Asian economies face disproportionate vulnerability to Strait of Hormuz blockade tensions due to their heavy reliance on Middle Eastern energy imports and limited alternative supply sources. Current market responses from major importing nations reveal the practical implications of this dependency.

High-Dependency Economy Responses:

Japan's Crisis Management:

Japan has moved to release strategic oil stockpiles as the energy crisis deepens, with government officials urging preparation for secondary emergency releases through international coordination mechanisms. This demonstrates Japan's acute vulnerability to supply disruptions despite maintaining substantial strategic reserves.

India's Supply Diversification:

India has rapidly secured 60 million barrels of Russian crude for April delivery, demonstrating active supply chain diversification strategies. Additionally, India has launched a historic oil and gas drilling campaign targeting import reduction through domestic production expansion.

China's Mixed Response:

Chinese companies show varied responses to the crisis, with green energy stocks surging as Middle Eastern conflict disrupts traditional oil markets. However, China's top shipping companies have resumed Middle East operations amid ceasefire negotiations, suggesting confidence in near-term stability.

Vulnerability Assessment Framework:

| Country | Import Dependency | Alternative Routes | Strategic Reserves | Current Response |

|---|---|---|---|---|

| Japan | High | Limited | 180+ days | Emergency releases |

| South Korea | High | Moderate | 96 days | Route diversification |

| India | Moderate-High | Developing | 74 days | Supply diversification |

| China | Moderate | Extensive | 90+ days | Mixed strategies |

Export-Dependent Producer Impact:

Regional producers face equally severe consequences from blockade conditions. Iraq's economy has begun showing signs of strain as Hormuz blockade tensions choke oil revenues, despite the country's dependence on petroleum exports for government financing. Furthermore, Saudi exploration licenses have become increasingly critical as the kingdom seeks to maintain market share through diversified production strategies.

Military Escalation Pathways and Scenarios

Current military developments suggest multiple potential escalation pathways, each carrying distinct implications for global energy security. Understanding these trajectories provides insight into potential duration and severity of supply disruption scenarios.

Current Military Capability Assessment:

U.S. Central Command assessments indicate significant degradation of Iranian military infrastructure, with air strikes reportedly hitting two-thirds of Iran's missile and drone production facilities. Similar proportions of naval production capabilities have sustained damage, fundamentally altering regional military balance.

Escalation Ladder Framework:

Level 1: Maritime Harassment (Current Status)

• Commercial vessel inspections and delays

• Increased military presence demonstrations

• Navigation warnings affecting shipping schedules

Level 2: Selective Targeting

• Specific flag vessel attacks

• Strategic mining of shipping lanes

• Coordinated drone harassment campaigns

Level 3: Complete Blockade Implementation

• Total waterway closure

• Direct military engagement with naval forces

• Infrastructure targeting across regional states

Level 4: Regional Conflict Expansion

• Multi-front warfare involving Gulf states

• Cyber attacks on energy infrastructure

• International coalition military intervention

Current Diplomatic Dynamics:

Recent diplomatic exchanges suggest limited willingness for immediate de-escalation. Iran has rejected U.S. peace proposals, with officials stating they do not intend to negotiate under current conditions. Iranian Foreign Minister Abbas Araqchi has indicated that Iran will end the conflict when it chooses and if specific conditions are met.

The U.S. has issued ultimatums regarding Strait of Hormuz operations, with extensions suggesting ongoing diplomatic pressure combined with military preparation. Additional U.S. forces, including elite 82nd Airborne Division elements, are reportedly deploying to provide expanded operational options.

Disruption Duration and Recovery Analysis

Different blockade duration scenarios produce varying structural changes in global energy markets, with longer disruptions creating permanent shifts in trade patterns and infrastructure development priorities.

Short-Term Disruption Response (1-4 weeks):

Market Adaptation Mechanisms:

• Strategic Reserve Releases: 2-4 million barrels per day capacity

• Spare Production Increases: 1-2 million barrels per day from available capacity

• Demand Destruction: 1-3 million barrels per day through price elasticity responses

Current inventory buffers provide 30-60 day operational cushion for major importing economies, while emergency bilateral supply agreements activate additional sourcing options. However, the complexity of these disruptions has already prompted detailed oil price crash analysis to understand potential downside scenarios once tensions resolve.

Medium-Term Crisis Management (1-6 months):

Extended disruption periods drive fundamental structural changes in energy trade patterns and infrastructure investment priorities. Investment flows redirect toward alternative energy sources and supply chain diversification projects.

Investment Redirection Patterns:

| Sector | Investment Increase | Implementation Timeline |

|---|---|---|

| Alternative Energy | 200-300% | 6-18 months |

| Pipeline Infrastructure | 150-250% | 12-36 months |

| Strategic Storage | 100-200% | 6-24 months |

| Shipping Capacity | 75-150% | 18-48 months |

Extended Blockade Consequences (6+ months):

Prolonged disruption scenarios create permanent restructuring of global energy trade relationships. China's green energy stocks have already demonstrated significant gains as investors anticipate accelerated renewable energy deployment programmes.

LNG markets have experienced particularly severe disruption, with exports plunging to 6-month lows as conflict throttles supply chains. This has created additional pressure for alternative energy source development and energy security diversification strategies.

The next major ASX story will hit our subscribers first

Alternative Route Development and Capacity

Current crisis conditions have accelerated utilisation of existing alternative routes while highlighting capacity constraints that limit complete substitution for Strait of Hormuz transit.

Pipeline Bypass Infrastructure:

Operational Systems:

• Saudi East-West Pipeline: 5 million barrels per day capacity

• UAE Fujairah Pipeline: 1.5 million barrels per day operational

• Iraq-Turkey Pipeline: 1.6 million barrels per day potential capacity

Proposed Development Projects:

• Iran-Pakistan Pipeline: 750,000 barrels per day planned capacity

• Saudi Red Sea Expansion: Additional 3 million barrels per day proposed

• Kuwait Red Sea Route: 2 million barrels per day under consideration

Maritime Alternative Assessment:

Current shipping constraints have led to significant route diversification, though with substantial cost and time penalties. Tanker rates for Red Sea-loading Saudi crude have fluctuated significantly as markets adapt to alternative routing requirements.

| Alternative Route | Distance Addition | Time Premium | Cost Increase |

|---|---|---|---|

| Cape of Good Hope | 6,000+ miles | 15-20 days | 40-60% |

| Suez Canal-Red Sea | 1,200+ miles | 3-5 days | 15-25% |

| Northern Sea Route | 4,000+ miles | 10-15 days | 30-45% |

Current Shipping Market Response:

European gasoline exports have shifted toward Asian markets as conflict disrupts traditional fuel market patterns. This demonstrates the flexibility of refined product markets compared to crude oil transportation constraints.

Australia has experienced additional LNG supply constraints due to domestic outages, compounding global LNG market stress and highlighting the interconnected nature of energy supply disruptions across multiple regions simultaneously.

Energy Transition Acceleration Impact

Strait of Hormuz blockade tensions have created unprecedented momentum for renewable energy investment and energy independence initiatives across multiple countries and regions.

Renewable Energy Investment Surge:

Current market conditions have triggered emergency renewable energy deployment programmes in multiple countries. China's green energy stocks have surged as Middle Eastern conflict upends traditional oil markets, demonstrating investor confidence in accelerated transition timelines.

Policy Response Acceleration:

• Emergency deployment programmes for renewable energy projects

• Grid modernisation fast-tracking to accommodate increased renewable capacity

• Energy storage expansion mandates supporting grid stability requirements

Market-Driven Transition Dynamics:

Solar and wind project financing has increased 300-400% as investors seek alternatives to volatile fossil fuel markets. Electric vehicle adoption programmes have accelerated as governments implement industrial electrification incentives.

Energy Security Diversification Strategies:

Strategic Reserve Expansion:

Multiple nations have announced strategic petroleum reserve capacity increases alongside regional cooperative storage agreements. Alternative fuel strategic stockpiling programmes provide additional security against future supply disruptions.

Supply Chain Resilience Building:

• Domestic energy production incentives reducing import dependency

• Critical mineral supply diversification supporting renewable energy infrastructure

• Technology transfer agreements enhancing energy independence capabilities

Industrial Adaptation Response:

Current naphtha shortages forcing Japanese petrochemical output reductions demonstrate the immediate industrial pressure driving alternative feedstock development. Manufacturing sectors are accelerating electrification programmes to reduce petroleum product dependency.

Long-Term Geopolitical Transformation

Current Strait of Hormuz blockade tensions are reshaping international alliance structures and regional power dynamics beyond immediate energy security concerns.

Alliance Structure Evolution:

New Strategic Partnership Development:

Energy security considerations are driving formation of military alliances specifically focused on critical resource protection. Joint strategic reserve management agreements provide coordinated response capabilities, while alternative route development projects create new regional cooperation frameworks.

Regional Power Dynamic Shifts:

Gulf state internal cooperation has increased significantly as mutual vulnerability to transit disruption creates shared security interests. Asian consumer nations are developing alliance structures for coordinated energy procurement and emergency response capabilities.

African and Latin American energy producers are gaining increased leverage as alternative suppliers to traditional Middle Eastern sources, creating new south-south cooperation opportunities.

International Legal Framework Development:

Maritime Security Enhancement:

Current crisis conditions are accelerating development of enhanced freedom of navigation protocols specifically designed for critical resource transit routes. According to Al Jazeera's analysis, blocking the strait would fundamentally alter global oil and LNG trading patterns. International energy security treaties are under development to provide legal frameworks for cooperative crisis response.

Military Doctrine Evolution:

Naval force projection capability expansion has become a priority for major energy importing nations. Cyber warfare integration in energy security planning reflects the multi-domain nature of modern resource protection requirements.

Multi-domain deterrence strategies are being developed to address the complex interaction between physical infrastructure protection, cyber security, and diplomatic crisis management.

Economic System Restructuring:

Current crisis conditions are accelerating development of alternative economic arrangements reducing dependence on traditional energy trade relationships. Regional currency arrangements for energy transactions provide reduced exposure to international financial system vulnerabilities.

Technology transfer agreements focused on energy independence are creating new patterns of international cooperation outside traditional alliance structures.

Investment and Risk Considerations:

Current analysis represents dynamic geopolitical and economic conditions subject to rapid change. Investment decisions should consider multiple scenario outcomes and maintain appropriate risk management strategies. Energy market volatility may continue for extended periods as structural adjustments occur across global supply chains.

The resolution of Strait of Hormuz blockade tensions will establish new precedents for international maritime law, energy security cooperation, and strategic resource protection mechanisms. Nations and organisations developing comprehensive crisis response capabilities while maintaining long-term diversification strategies are positioning themselves for enhanced resilience in an increasingly complex global energy landscape.

Looking to Navigate Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping subscribers identify actionable opportunities as global energy disruptions reshape commodity markets and drive demand for critical resources. With energy security becoming paramount and supply chains under unprecedented pressure, Discovery Alert's dedicated discoveries page showcases how major mineral discoveries have historically generated substantial returns during periods of market uncertainty.