July 5, 2026

Energy infrastructure vulnerability has long represented one of the most significant risks to global economic stability. Maritime chokepoints, where critical shipping lanes narrow to create geographical bottlenecks, function as single points of failure for international commerce. When these strategic waterways face disruption, the Strait of Hormuz oil crisis consequences ripple through interconnected supply chains, financial markets, and consumer economies worldwide. The complexity of modern energy security extends far beyond simple supply and demand calculations, encompassing diplomatic relationships, insurance frameworks, and emergency response protocols that require coordination across dozens of nations.

Understanding the Strategic Chokepoint Vulnerability

What Makes the Strait of Hormuz Critical to Global Energy Markets?

The Strait of Hormuz operates as the world's most critical energy transit corridor, with geographic constraints that create unavoidable vulnerability for global petroleum markets. This narrow waterway measures approximately 21 miles (34 kilometers) at its narrowest point, forcing all maritime traffic through established shipping lanes that measure just 2 miles wide in each direction under international maritime law.

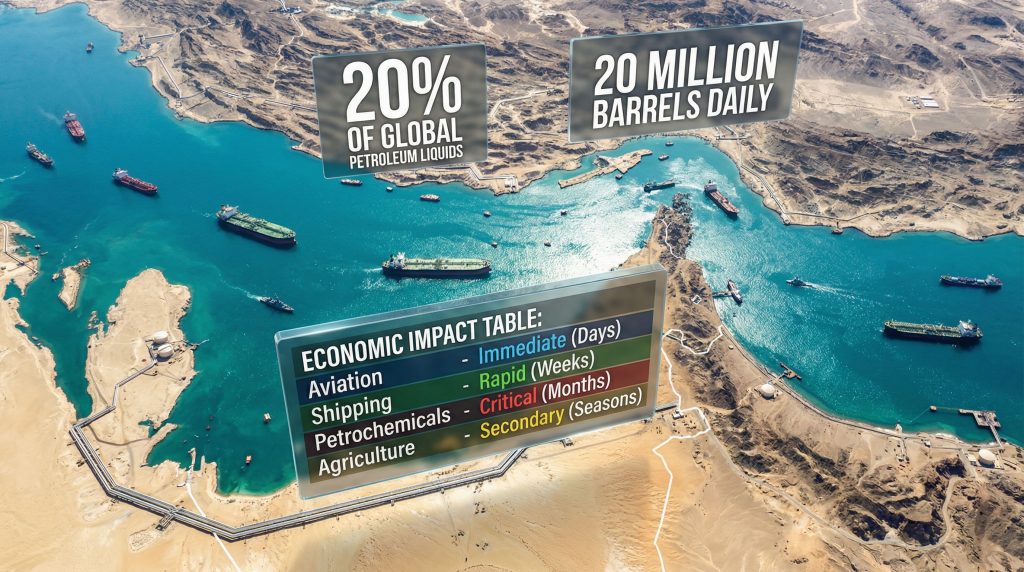

Daily throughput statistics demonstrate the strait's overwhelming importance to global energy security. The waterway handles approximately 20-21 million barrels per day of crude oil and refined petroleum products, representing roughly 20-25% of global seaborne oil trade depending on whether refined products are included in calculations. Additionally, 20% of global liquefied natural gas shipments transit through these constrained waters, creating a concentration of energy resources that has no viable alternative route for most commercial operations.

The economic dependency mapping reveals stark regional vulnerabilities, particularly across Asia-Pacific markets. Major consuming nations including Japan, South Korea, India, and China import 60-85% of their crude oil from Arabian Gulf producers, with the majority transiting through the Strait of Hormuz. This geographic concentration creates systemic risk that extends far beyond individual supply contracts. Furthermore, understanding oil price rally dynamics becomes crucial during these periods of heightened tension.

Technical constraints amplify the vulnerability. Large crude carriers (Ultra Large Crude Carriers) transiting the strait carry 300,000+ deadweight tons and require deep draft channels exceeding 15 meters when fully laden. The underwater topography and shallow waters surrounding the main shipping channels prevent significant route deviation, forcing all traffic through monitored corridors that represent a single point of failure for global energy flows.

How Do International Maritime Laws Apply During Energy Crises?

International maritime law provides the regulatory framework governing transit through strategic chokepoints, but enforcement mechanisms remain limited during active conflicts. The United Nations Convention on the Law of the Sea (UNCLOS) establishes freedom of navigation principles, yet these protections conflict with territorial sovereignty claims when coastal nations assert control over adjacent waters.

Historical precedents demonstrate the legal complexity of chokepoint closures. During the 1973 Yom Kippur War oil embargo, OPEC producers implemented selective restrictions on nations supporting Israel, with Arabian Gulf exporters halting shipments through the Strait of Hormuz. Global oil prices increased 300-400% within months, creating cascading economic disruption across industrial economies. The legal framework provided limited recourse for affected importing nations.

Insurance and liability frameworks create additional complications during energy crises. Maritime insurance classifications change based on transit risk assessments, with elevated premiums for passage through high-risk zones. Lloyd's of London and other major insurers typically suspend coverage or impose prohibitive premium increases when military actions threaten commercial shipping, effectively creating economic blockades even when physical passage remains possible.

The 2011 Iranian threat to close the Strait of Hormuz demonstrated how psychological impacts on market pricing can exceed actual physical disruptions. Brent crude prices increased 5-8% on announcement alone despite the threat remaining unrealized, illustrating the critical importance of market confidence to energy security beyond pure supply calculations.

When big ASX news breaks, our subscribers know first

Macro-Economic Impact Assessment Framework

Which Economic Sectors Face the Greatest Disruption Risk?

Energy supply disruptions create cascading effects across multiple economic sectors, with impact severity varying based on inventory levels, alternative supply availability, and operational flexibility. Primary impact zones include transportation, manufacturing, and agriculture, while secondary effects ripple through supply chains affecting virtually every economic activity. Consequently, examining trade war market impacts reveals additional layers of complexity in these situations.

Transportation sector vulnerability operates on the shortest timeline. Commercial aviation typically maintains 2-4 weeks of operational jet fuel inventory at major hubs, creating crisis conditions within this timeframe unless alternative supplies are mobilised. The global shipping industry faces immediate bunker fuel cost increases of 5-12% for every $10-15 per barrel increase in crude oil prices, with direct transmission to freight rates affecting international trade competitiveness.

| Economic Sector | Direct Impact | Timeline to Crisis | Mitigation Capacity |

|---|---|---|---|

| Aviation | Jet fuel shortages | 2-4 weeks | Limited alternatives |

| Shipping | Bunker fuel costs | Immediate | Route diversification |

| Petrochemicals | Feedstock disruption | 1-3 months | Regional substitution |

| Agriculture | Fertilizer supply | 3-6 months | Seasonal flexibility |

Australian market data provides concrete evidence of rapid price transmission mechanisms. Following recent Strait of Hormuz disruptions, fuel prices experienced a 17-cent rise in average retail prices, with regional peaks reaching A$3.40 per litre in some areas. This price acceleration occurred despite Australia importing approximately 90% of its liquid fuel from Asian refineries, demonstrating how global market psychology affects local pricing even with multiple intermediary steps in the supply chain.

How Do Energy Price Shock Mechanisms Function?

Energy price shocks operate through complex transmission mechanisms that amplify initial supply disruptions through financial market speculation, inventory adjustments, and psychological factors. Spot market pricing responds immediately to supply concerns, while long-term contract pricing provides some stability but cannot prevent overall market volatility.

Futures market speculation creates volatility amplification beyond fundamental supply-demand calculations. The 2003-2008 oil price spike demonstrated this mechanism, with crude prices rising from approximately $25 per barrel to $147 per barrel, correlating with global inflation acceleration and reduced manufacturing output. Supply chain disruption, rather than actual production shortfall, amplified economic consequences through precautionary inventory building and speculative trading.

Central bank monetary policy responses to energy inflation create additional complications for economic stability. Supply-side price shocks present difficult policy choices between controlling inflation through interest rate increases (which can trigger recession) and accommodating temporary price increases to maintain economic growth. In addition, the US oil production impact adds another dimension to these considerations.

The European energy crisis following Russian sanctions provided recent case study data on this transmission mechanism, with natural gas prices increasing 600-800% and triggering cascading effects through fertiliser production, agricultural input costs, and food price inflation reaching 15-20% across certain categories.

"Recent market disruptions demonstrate unprecedented coordination challenges, with the International Energy Agency characterising current conditions as requiring collective emergency action equivalent to the scale of disruption faced by global energy markets."

International Emergency Response Protocols

What Authority Does the International Energy Agency Hold?

The International Energy Agency operates under legal frameworks established following the 1974 oil embargo, with authority derived from the International Energy Program agreement rather than supranational enforcement powers. The organisation coordinates emergency responses among 32 member nations, but activation requires consensus or supermajority agreement among member governments, creating potential coordination challenges during ideologically divided periods.

Emergency response mechanisms function through coordinated government authorisation rather than IEA direct control. Member states commit to maintaining strategic reserves equal to 90 days of average net imports, providing the foundation for collective emergency releases. The recent 400 million barrel emergency release represents the largest coordinated response in IEA history, constituting 26% of total member strategic reserves (1.5 billion barrels total capacity).

Release rate limitations constrain emergency response effectiveness during major disruptions. Maximum emergency release capacity reaches 4.1 million barrels per day across all member nations, representing meaningful but limited supplementation to global daily petroleum consumption of approximately 100 million barrels. During Strait of Hormuz oil crisis scenarios involving 20 million barrels daily transit volume, emergency reserves address only 20% of disrupted flow for the available release duration.

Non-member producer engagement becomes critical during major emergencies, as the IEA's formal authority extends only to member nations. Coordination with major oil-producing countries outside the organisation (including Russia, Iran, and Iraq) requires diplomatic engagement rather than institutional mechanisms, creating potential gaps in global response coordination.

How Effective Are Strategic Petroleum Reserves During Supply Shocks?

Strategic petroleum reserves provide critical market stabilisation tools during supply disruptions, but capacity limitations and geographical constraints affect their operational effectiveness. The United States maintains approximately 600 million barrels (roughly 40% of total IEA reserves), with storage occurring primarily in underground salt caverns along the Gulf Coast.

Reserve extraction bottlenecks limit emergency response speed and duration. At maximum release rates of 4.1 million barrels daily, the current 400 million barrel emergency release provides approximately 97 days of supplementation. However, refilling these reserves at current market prices ($80-100 per barrel) requires $32-40 billion capital allocation, creating fiscal constraints on future emergency responses.

Historical effectiveness data demonstrates both capabilities and limitations of strategic reserve deployments. The 2011 Japan earthquake and tsunami response involved a coordinated 60 million barrel release from member strategic reserves following the Fukushima nuclear disaster, successfully preventing sustained price spikes. However, the scale of current disruptions requires unprecedented reserve utilisation, with the 26% drawdown of total strategic reserves reflecting institutional assessment that market stabilisation justifies deploying reserves requiring months to replenish.

"The magnitude of current emergency releases indicates institutional judgement that disruption severity justifies deploying strategic reserves that require extended periods and substantial financial resources to replenish, demonstrating assessment priorities favouring immediate market stabilisation over reserve conservation."

Alternative Supply Route Analysis

Which Pipeline Systems Can Compensate for Maritime Disruptions?

Pipeline infrastructure provides the most viable alternative to maritime petroleum transport during Strait of Hormuz disruptions, though capacity limitations prevent complete substitution for sea-borne shipments. The Saudi East-West Pipeline system offers the highest alternative capacity at 5 million barrels per day, while the UAE Abu Dhabi Crude Oil Pipeline contributes an additional 1.5 million barrels per day to global supply route diversification.

Capacity calculations reveal significant supply gaps despite pipeline alternatives. Combined Middle Eastern pipeline capacity totals approximately 8-10 million barrels per day when including smaller systems and the operational Iraqi-Turkish pipeline network. However, this represents only 40-50% of the 20 million barrels daily normally transiting the Strait of Hormuz, requiring substantial demand reduction or alternative supply sources to maintain market balance. Moreover, OPEC production impact decisions play a crucial role in these scenarios.

Time-distance economics create additional constraints for maritime route diversification. Circumnavigation via the Cape of Good Hope adds 12-14 days transit time and substantial fuel costs, rendering such routes economically viable only during extreme spot price premiums. Commercial shipping companies typically absorb these additional costs only when Strait of Hormuz passage becomes impossible rather than merely dangerous or expensive.

Regional energy security partnerships attempt to address these infrastructure limitations through coordinated planning and investment. The ASEAN+3 emergency oil sharing mechanism and European Union oil supply security regulations provide frameworks for alternative supply coordination, though implementation depends on available spare capacity and political cooperation among participating nations.

How Do Regional Energy Security Partnerships Respond?

Regional energy security frameworks operate through pre-established agreements and coordination mechanisms, but effectiveness depends on available spare capacity and political alignment among participating nations. The ASEAN+3 emergency oil sharing mechanism includes major Asian importers and provides coordination protocols, though actual supply availability varies based on individual national circumstances.

European Union oil supply security regulations evolved significantly following the 2022 Russian energy crisis, with emphasis on supplier diversification and emergency coordination mechanisms. Current EU frameworks require member states to maintain strategic reserves and coordinate release timing to maximise market impact while preventing premature price deflation that could undermine release effectiveness.

North American energy independence capabilities provide relative insulation from Middle Eastern supply disruptions, with continental production meeting substantial portions of regional demand. However, global market integration means that North American prices still respond to international supply disruptions, even when physical supply security remains intact through domestic production.

China's strategic petroleum reserve deployment protocols remain less transparent than Western counterparts, but capacity estimates suggest reserves capable of 90-120 days of import coverage under normal consumption patterns. Chinese reserve releases operate through state-controlled mechanisms rather than market coordination frameworks, creating potential timing misalignments with IEA member responses.

Geopolitical Risk Escalation Scenarios

What Triggers Activate Naval Convoy Protection Systems?

International Maritime Organisation emergency procedures establish protocols for commercial vessel protection during maritime conflicts, though implementation requires coordination among multiple naval forces and shipping companies. Rules of engagement for commercial vessel protection must balance defensive capabilities with risk escalation potential, creating complex operational constraints.

Combined Maritime Forces coordination mechanisms provide established frameworks for multi-national naval cooperation in critical shipping lanes. However, effectiveness depends on participating nations' willingness to deploy naval assets and accept potential combat risks. Insurance market responses to military escort operations create additional economic considerations, as coverage typically excludes losses during active military operations.

Historical precedents from the 1980s "Tanker War" during the Iran-Iraq conflict demonstrate both capabilities and limitations of naval convoy protection. Operation Earnest Will provided U.S. naval escorts for Kuwaiti tankers, successfully maintaining petroleum exports despite ongoing military actions. However, several escort vessels and commercial ships sustained damage, illustrating inherent risks in such operations.

Maritime security frameworks must address technological evolution in naval warfare, including drone attacks, mine warfare, and missile threats that complicate traditional convoy protection strategies. Recent attacks on commercial vessels in the Strait of Hormuz using projectiles and reportedly including mine deployment demonstrate evolving threat profiles requiring adapted defensive responses. The USSC research on these escalating tensions highlights the risks of a global energy crisis.

How Do Sanctions Regimes Interact with Energy Security Needs?

Sanctions regimes create complex interactions with energy security requirements, as humanitarian exemptions for energy supplies must be balanced against policy objectives and compliance enforcement. Third-country compliance requirements often extend sanctions effects beyond direct bilateral relationships, affecting energy trade through intermediary nations and companies.

Financial system disruptions affecting energy trade operate through banking restrictions, payment processing limitations, and currency exchange constraints. The 2022 Russian sanctions regime provided extensive case study data on these mechanisms, with energy payments requiring specialised arrangements to maintain supply flows while complying with financial restrictions.

Bilateral energy cooperation agreements during crises often require temporary modifications or exemptions from existing sanctions frameworks. Humanitarian considerations and energy security needs may justify continued trade relationships despite broader political conflicts, creating policy tensions between economic stability and diplomatic objectives.

Legal complexity increases when sanctions regimes affect multiple jurisdictions simultaneously. International companies operating across different regulatory frameworks must navigate conflicting requirements, often leading to over-compliance that exceeds actual legal requirements but reduces operational risk exposure.

Long-Term Energy Infrastructure Resilience

Which Alternative Energy Sources Gain Strategic Priority?

Energy security crises accelerate policy discussions regarding renewable energy deployment, nuclear power strategic importance, and domestic fossil fuel production capabilities. However, timeline constraints limit short-term alternatives during acute supply disruptions, requiring emergency response measures until longer-term infrastructure transitions can be completed. Therefore, renewable energy transformations gain increased attention during these periods.

Renewable energy acceleration policies gain political support during energy crises, but physical infrastructure requirements create multi-year implementation timelines. Wind and solar installations require substantial grid infrastructure modifications, battery storage systems, and regulatory framework adjustments that cannot address immediate supply shortfalls.

Nuclear power strategic importance receives renewed emphasis during energy security crises, as nuclear generation provides baseload capacity independent of fossil fuel imports. However, nuclear plant construction timelines extend across decades, limiting crisis response utility while potentially affecting long-term energy planning priorities.

Hydrogen economy development timelines face similar constraints, with current production capacity insufficient to replace petroleum products during short-term crises. However, hydrogen infrastructure investment may accelerate as nations seek energy security through diversified supply sources and reduced import dependencies.

How Do Nations Redesign Energy Import Diversification?

Supplier concentration risk assessment methodologies become critical policy tools following energy supply disruptions, as nations evaluate over-dependence on specific supply sources or transit routes. Infrastructure investment priorities shift toward route diversification, alternative supplier development, and emergency supply capacity expansion.

Regional energy hub development strategies attempt to create multiple supply pathway options and emergency coordination capabilities. These initiatives require substantial capital investment, international cooperation agreements, and long-term political commitment extending beyond individual crisis periods.

Technology transfer agreements for energy independence may accelerate during supply crises, as importing nations seek domestic production capability development. However, technological complexity and capital requirements for petroleum exploration, refining, and distribution create substantial barriers to rapid energy independence achievement.

Investment coordination between public and private sectors becomes essential for infrastructure resilience improvements, as commercial entities typically optimise for cost efficiency rather than emergency supply security. Government incentives and regulatory frameworks must align private investment with public energy security objectives.

The next major ASX story will hit our subscribers first

Economic Recovery and Market Stabilisation

What Indicators Signal Energy Market Normalisation?

Energy market normalisation indicators include tanker insurance premium stabilisation, spot price convergence with futures markets, and strategic reserve refill rate planning. These metrics provide measurable benchmarks for assessing crisis resolution progress and economic recovery trajectories.

Tanker insurance premium stabilisation typically occurs weeks after physical supply route security improves, as insurance companies require sustained risk reduction before adjusting coverage terms and pricing. Lloyd's of London and other major maritime insurers serve as leading indicators for commercial shipping confidence levels.

Spot price convergence with futures markets indicates reduced short-term supply anxiety and restored confidence in longer-term market stability. Persistent price divergence between spot and futures contracts suggests continued crisis conditions and market uncertainty regarding supply security.

Supply chain inventory rebuilding timelines extend for months following crisis resolution, as companies restore depleted stockpiles and resume normal operational patterns. Inventory rebuilding creates continued demand pressure even after supply routes reopen, potentially extending price elevation periods beyond actual supply restoration.

How Do Central Banks Address Energy-Driven Inflation?

Central bank responses to energy-driven inflation require careful balance between controlling price increases and maintaining economic growth during supply shock periods. Monetary policy tools designed for demand-side inflation may prove counterproductive when applied to supply-side price increases caused by energy disruptions.

Exchange rate intervention strategies become relevant for energy-importing nations experiencing currency depreciation during oil price spikes. Currency weakness amplifies imported energy costs, creating additional inflationary pressure beyond baseline commodity price increases. Central bank intervention in foreign exchange markets may help stabilise energy import costs but requires substantial reserve utilisation.

Coordination mechanisms between fiscal and monetary authorities become essential during energy crises, as government emergency spending on strategic reserves and economic stabilisation may conflict with central bank inflation control objectives. Policy coordination prevents conflicting objectives that could worsen economic stability.

Communication strategies for managing inflation expectations require clear messaging regarding temporary versus permanent price increases. Market participants and consumers must understand whether energy price increases represent short-term crisis responses or longer-term structural changes requiring behavioural adjustments.

Investment and Industry Transformation

Which Energy Companies Face the Greatest Strategic Risk?

Integrated oil companies face varying risk exposure based on production geography, supply chain integration, and market exposure patterns. Companies with substantial operations in politically unstable regions or dependence on specific transport corridors experience heightened vulnerability during geopolitical energy crises.

Shipping and logistics sector vulnerability extends beyond petroleum transport to include container shipping, bulk cargo, and specialised vessel operations affected by route disruptions and insurance cost increases. Maritime companies must balance operational flexibility against cost optimisation, often requiring premium pricing for alternative routing capabilities.

Renewable energy investment acceleration may occur as institutional investors and governments seek supply security through domestic energy generation capabilities. However, renewable energy companies face their own supply chain vulnerabilities, including critical mineral dependencies and manufacturing capacity constraints.

Energy infrastructure resilience upgrades require substantial capital allocation across pipeline systems, storage facilities, and distribution networks. These investments provide long-term strategic value but create near-term financial pressure on energy companies already facing volatile commodity prices and operational disruptions.

How Do Sovereign Wealth Funds Respond to Energy Crises?

Sovereign wealth funds possess substantial capital resources and long-term investment horizons that enable strategic responses to energy market disruptions. Emergency market stabilisation interventions may include direct commodity purchases, strategic asset acquisitions, and coordinated market support operations.

Strategic asset acquisition opportunities emerge during energy crises as market volatility creates undervalued investment possibilities. Sovereign wealth funds may acquire energy infrastructure, production assets, or supply chain components at crisis-discounted prices while supporting broader economic stability objectives.

Currency reserve management becomes critical during commodity volatility periods, as energy-exporting nations experience revenue fluctuations while importing nations face increased foreign exchange requirements for energy purchases. Sovereign wealth fund currency operations can help stabilise national balance of payments during extended crisis periods.

Long-term energy transition investment reallocation may accelerate following supply crises, as sovereign wealth funds balance immediate crisis response with strategic positioning for future energy market evolution. These investment decisions shape global energy infrastructure development and market structure transformation over decades.

During periods of heightened tension, Strait of Hormuz oil crisis scenarios force rapid reassessment of global energy security arrangements. The combination of geopolitical instability, infrastructure vulnerability, and economic interdependence creates systemic risks that require coordinated international response mechanisms extending well beyond traditional market forces.

Disclaimer: This analysis involves forecasts and speculation regarding energy market dynamics, geopolitical developments, and economic outcomes. Market conditions change rapidly during crisis periods, and actual developments may differ substantially from analytical projections. Investment and policy decisions should incorporate multiple information sources and professional advice appropriate to specific circumstances.

Ready to Navigate Market Volatility During Energy Crises?

When geopolitical tensions threaten global energy supplies, astute investors position themselves to capitalise on the resulting market opportunities before broader recognition occurs. Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, helping subscribers identify actionable investment opportunities that emerge as markets seek alternative energy and commodity sources during periods of heightened uncertainty.