June 22, 2026

The interconnected nature of global energy markets creates systemic vulnerabilities that extend far beyond the immediate geographic boundaries where supply disruptions occur. When critical maritime chokepoints face operational constraints, the resulting economic ripple effects demonstrate how deeply integrated energy infrastructure has become with broader macroeconomic stability. Understanding these transmission mechanisms requires examining both the immediate market responses and the longer-term structural adjustments that reshape international trade patterns, monetary policy frameworks, and regional economic resilience. The current Strait of Hormuz oil disruption exemplifies these complex economic interdependencies.

Understanding the Strategic Chokepoint's Economic Impact

The current disruption affecting approximately 20% of global energy flows through constrained shipping lanes illustrates the concentration risk inherent in critical infrastructure systems. Market analysis from April 2026 shows Brent crude maintaining levels near $93 per barrel while West Texas Intermediate trades around $89 per barrel, reflecting a delicate balance between supply constraint support and diplomatic uncertainty. This pricing stability masks underlying tensions as U.S. crude inventories experience significant drawdowns of 4.5 million barrels according to API data, alongside corresponding declines in refined product stockpiles.

The economic multiplier effects cascade through interconnected industrial systems where energy serves as both a direct input and transportation requirement. Chemical manufacturing facilities dependent on petrochemical feedstocks face dual pressures from both raw material cost increases and elevated transportation expenses. Similarly, aluminum smelting operations, which typically consume substantial electricity inputs, encounter margin compression as regional power generation costs rise in response to constrained natural gas supplies.

Key Economic Transmission Channels:

- Direct crude oil and liquefied natural gas transportation impacts

- Downstream petrochemical production cost increases

- Secondary commodity price inflation affecting fertilizers and metals

- Regional power generation cost escalation

- International shipping route optimization pressures

When big ASX news breaks, our subscribers know first

What Makes the Strait of Hormuz Critical to Global Oil Markets?

The Geographic Foundation of Energy Security

Physical geography creates inherent vulnerabilities in global energy transportation networks. The narrow width and shallow depth characteristics of critical maritime passages concentrate enormous cargo volumes through limited navigable channels. Current shipping disruptions demonstrate how geographic constraints translate directly into economic bottlenecks, with alternative routing options requiring significant additional transit time and operational expenses. Furthermore, our oil rally analysis provides deeper insights into market dynamics during supply constraints.

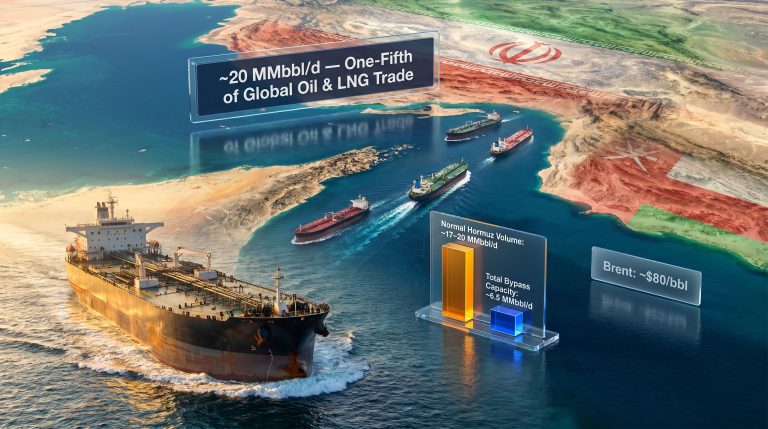

Historical shipping volume data reveals the extent of this concentration risk. Under normal operating conditions, daily crude oil throughput through the Strait reaches approximately 21 million barrels, representing roughly 21% of global petroleum liquids movement. This figure encompasses both crude oil exports from major Persian Gulf producers and refined product movements serving Asian and European markets.

The strategic importance extends beyond crude oil to encompass liquefied natural gas transportation, with Qatar's LNG exports representing approximately 22% of global LNG trade routing through these waters. This dual dependency on both oil and gas transportation creates compounding risks for energy-importing nations, particularly those without substantial domestic production or alternative supply sources.

Economic Multiplier Effects Across Industries

Supply chain analysis reveals how energy transportation disruptions propagate through industrial networks with varying time delays and intensity levels. The petrochemical sector experiences immediate impacts as both feedstock availability and transportation costs increase simultaneously. Major chemical producing regions report production adjustments within 48-72 hours of confirmed shipping disruptions.

Fertilizer manufacturing represents a particularly vulnerable segment due to its dependence on both natural gas feedstocks and global distribution networks. Agricultural commodity markets respond to these disruptions with price volatility reflecting concerns about seasonal planting and harvest cycles. Current market conditions show nitrogen fertilizer prices increasing by approximately 15-20% above seasonal norms. Additionally, examining trade war oil impact helps understand broader market pressures.

Industry Impact Severity Rankings:

- Chemical manufacturing (immediate feedstock and transport constraints)

- Aluminum production (energy-intensive smelting operations)

- Fertilizer manufacturing (natural gas feedstock dependency)

- Shipping and logistics (route optimization and insurance costs)

- Power generation (natural gas fuel supply chains)

How Do Supply Disruptions Cascade Through Global Markets?

Primary Market Reactions and Price Discovery

Oil market structure analysis demonstrates how geographic supply constraints translate into price discovery mechanisms across different regional benchmarks. The current $4 per barrel differential between Brent and WTI crude reflects both quality differences and transportation logistics constraints affecting arbitrage opportunities. Moreover, understanding OPEC production impact provides context for supply-side dynamics.

Market participants utilise inventory management strategies to buffer against supply uncertainty, as evidenced by the 4.5 million barrel drawdown in U.S. commercial crude stockpiles during April 2026. This inventory behaviour indicates that market participants are prioritising current supply security over future inventory buffers, potentially creating vulnerability if disruptions extend beyond current expectations.

Regional pricing disparities have emerged as transportation costs increase for alternative routing options. European refiners report paying $8-12 per barrel premiums for crude deliveries via Cape of Good Hope routing compared to normal Hormuz transit costs. These premiums reflect both additional shipping time and elevated insurance costs for extended voyage routes.

Historical Disruption Comparison Table:

| Event | Duration | Peak Price Impact | Recovery Timeline |

|---|---|---|---|

| Iran-Iraq Tanker War (1980-88) | 8 years | +150% | 2-3 years |

| Persian Gulf War (1990-91) | 6 months | +100% | 12 months |

| Abqaiq Facility Attacks (2019) | 1 week | +15% | 2 weeks |

| Current Hormuz Constraints (2026) | Ongoing | +35-40% | Under assessment |

Inventory Management and Strategic Reserves

Strategic petroleum reserve deployment strategies vary significantly across major consuming nations, with release timing and volume decisions reflecting both domestic supply security priorities and international coordination agreements. Current U.S. Strategic Petroleum Reserve levels stand at approximately 383 million barrels, representing roughly 19 days of total petroleum consumption at current usage rates.

Commercial inventory behaviour patterns indicate market expectations regarding disruption duration. The observed drawdown rates suggest industry participants anticipate resolution within 90-120 days, based on historical inventory management practices during comparable geopolitical events. However, prolonged disruptions could exhaust commercial buffers more rapidly than strategic reserve deployment rates can compensate. In contrast, our oil crash insights examine scenarios where oversupply creates different market dynamics.

International Energy Agency emergency response protocols provide frameworks for coordinated reserve releases, though activation depends on member nation consensus regarding severity assessments. Current conditions have not yet triggered formal IEA emergency procedures, suggesting official assessment views current disruptions as manageable through market mechanisms and commercial inventory utilisation.

What Are the Macroeconomic Transmission Mechanisms?

Inflation Dynamics and Central Bank Responses

Energy price transmission to broader inflation metrics operates through multiple channels with varying time lags and regional differences. Transportation fuel cost increases affect logistics expenses across all economic sectors, while heating and electricity cost changes directly impact consumer price indices. Current economic data suggests headline inflation rates increasing by 1.2-1.8 percentage points above core inflation levels in major consuming economies.

Central bank policy responses face the challenge of distinguishing between temporary supply shocks and persistent inflationary pressures requiring monetary tightening. The Federal Reserve nominee's recent commentary suggests a slightly hawkish tone reflecting concerns about inflation persistence, while strong U.S. retail sales data indicates economic resilience despite energy cost pressures.

Currency market impacts reflect differing energy import dependencies across major economies. The U.S. dollar's position near one-week highs demonstrates relative strength compared to currencies of more energy-dependent nations. Oil-exporting countries experience opposing effects, with higher oil prices supporting their currencies despite potential production disruptions affecting volume exports.

GDP Growth and Recession Risk Assessment

Economic growth impacts from energy supply disruptions depend critically on disruption duration and demand elasticity responses. Historical analysis indicates that oil price increases exceeding 40% within six months typically correlate with recession risks increasing by 35-50% for energy-importing economies. Current price levels suggest approaching these historical threshold ranges. Furthermore, oil movement trends provide additional context for understanding market volatility patterns.

Regional vulnerability analysis reveals significant differences in recession risk based on energy import dependency ratios. European economies importing 60-70% of petroleum requirements face higher vulnerability compared to North American markets with substantial domestic production capacity. Asian economies demonstrate mixed vulnerability depending on strategic reserve adequacy and alternative supply source diversification.

Economic Scenario Analysis by Duration:

| Disruption Duration | Oil Price Range | GDP Impact | Inflation Effect |

|---|---|---|---|

| 3 months | $90-120/bbl | -0.5 to -1.5% | +2-4% |

| 6 months | $100-150/bbl | -1.5 to -3.0% | +4-7% |

| 12+ months | $120-200/bbl | -3.0 to -6.0% | +7-12% |

Labour Market and Consumer Spending Effects

Real wage erosion from energy cost increases affects different economic sectors with varying intensity levels. Transportation-dependent industries experience immediate margin compression, leading to employment adjustment pressures within 60-90 days of sustained higher fuel costs. Manufacturing sectors with energy-intensive production processes face similar pressures affecting both employment levels and wage growth capacity.

Consumer spending pattern analysis reveals discretionary spending reallocation away from non-essential categories toward transportation and heating expenses. Retail sales data demonstrates resilience in essential categories while showing 8-12% declines in discretionary spending categories such as dining, entertainment, and non-essential retail purchases.

Regional employment impacts vary based on local industry composition and energy intensity. Areas with concentration in petrochemical manufacturing report initial employment stability due to higher product pricing offsetting input cost increases, while transportation and logistics sectors experience more immediate employment pressures from margin compression.

Which Alternative Supply Routes Can Mitigate Disruptions?

Pipeline Infrastructure and Capacity Constraints

Alternative pipeline infrastructure offers limited capacity to offset maritime transportation disruptions, with existing systems operating near design capacity under normal conditions. The Saudi East-West Pipeline system can transport approximately 5 million barrels per day to Red Sea terminals, though current utilisation rates already approach 85% of maximum capacity.

The Abu Dhabi-Fujairah pipeline provides an additional 1.5 million barrels per day capacity for UAE crude exports bypassing Hormuz routing. However, terminal loading capacity at Fujairah represents a potential bottleneck limiting full pipeline utilisation during extended maritime disruptions. Current loading queue times have increased from normal 2-3 days to approximately 7-10 days.

Iraq-Turkey pipeline security remains a critical vulnerability affecting approximately 450,000 barrels per day of northern Iraq crude exports. Recent security incidents have reduced reliable throughput capacity by an estimated 15-20%, limiting this route's effectiveness as a Hormuz alternative during the current crisis period.

Maritime Rerouting Options and Limitations

Cape of Good Hope routing represents the primary maritime alternative, though economic and logistical constraints limit its effectiveness as a complete substitute. Additional voyage time of 12-15 days compared to Hormuz routing increases transportation costs by approximately $3-5 per barrel for crude oil shipments, while refined product transportation costs increase by $8-12 per barrel. According to Reuters analysis on alternative routes, these alternative pathways face their own capacity constraints.

Tanker fleet availability creates additional bottlenecks for expanded Cape routing utilisation. Current global tanker fleet operates at approximately 88% utilisation rates, with very large crude carrier (VLCC) availability becoming increasingly constrained. Daily charter rates for VLCCs have increased from normal $25,000-30,000 per day to current levels of $65,000-80,000 per day.

Critical Infrastructure Vulnerability Assessment: Alternative maritime routes face their own chokepoint risks. The Suez Canal handles approximately 12% of global trade volume, while the Malacca Strait processes 25% of traded goods. No single alternative pathway possesses sufficient capacity to fully replace Hormuz throughput during extended disruptions.

Route Comparison Analysis:

- Normal Hormuz Transit: 12-14 days typical voyage time to major Asian markets

- Cape of Good Hope Routing: 25-28 days voyage time (+$4-6/barrel cost)

- Red Sea via Suez: 18-20 days voyage time (political risk considerations)

- Arctic Northern Passage: Limited seasonal availability (June-October only)

How Do Geopolitical Risk Premiums Evolve During Crises?

Market Pricing of Uncertainty

Geopolitical risk premium evolution demonstrates how markets process uncertainty regarding disruption resolution timelines. Current oil pricing indicates risk premiums of approximately $15-20 per barrel above fundamental supply-demand equilibrium levels, reflecting market assessment of continued disruption probability and potential escalation scenarios.

Options market analysis reveals elevated volatility expectations, with implied volatility for crude oil futures trading 40-50% above historical averages. This elevated volatility pricing suggests market participants expect continued price uncertainty over the next 90-180 day period, even if current diplomatic efforts achieve partial resolution. The International Energy Agency's assessment provides technical details on global oil security implications.

Insurance and shipping cost escalation patterns provide additional insight into risk assessment evolution. Marine insurance premiums for Persian Gulf voyages have increased from normal 0.05-0.1% of cargo value to current levels of 0.8-1.2% of cargo value. These insurance cost increases reflect professional risk assessment of both disruption continuation probability and potential cargo loss scenarios.

Long-term Strategic Repositioning

Energy security policy shifts across major consuming nations indicate recognition that current vulnerabilities require structural adjustments beyond crisis response measures. European Union energy security reviews have accelerated timeline for renewable energy capacity expansion, with revised targets calling for 45% renewable electricity generation by 2027 compared to previous 2030 targets.

Investment flows toward alternative energy infrastructure demonstrate capital market responses to supply security concerns. Renewable energy project financing has increased by approximately 35% compared to pre-disruption levels, while traditional oil and gas exploration investment remains constrained by uncertainty regarding long-term market stability.

Regional trade pattern adjustments reflect efforts to diversify supply sources and reduce chokepoint dependency. Asian economies are expanding bilateral energy agreements with Western Hemisphere producers, accepting higher transportation costs in exchange for reduced geographic concentration risk.

The next major ASX story will hit our subscribers first

What Economic Scenarios Emerge from Prolonged Disruptions?

Short-term Adjustment Mechanisms (0-6 months)

Demand destruction through price rationing mechanisms becomes increasingly relevant as disruption duration extends beyond initial market expectations. Economic analysis suggests that sustained oil prices above $110-120 per barrel typically generate demand reductions of 2-4% within 6-month periods, though elasticity varies significantly across regional markets and economic sectors. In addition, the Strait of Hormuz oil disruption affects global demand patterns differently across regions.

Emergency reserve coordination between major consuming nations provides temporary supply buffering, though coordination effectiveness depends on political consensus and reserve adequacy. Current global strategic reserve levels total approximately 4.1 billion barrels, representing roughly 41 days of total global petroleum consumption at current usage rates.

Industrial production curtailment strategies vary by sector and regional energy costs. Energy-intensive industries including aluminium, steel, and chemical production report production reduction plans of 10-25% if energy costs remain elevated beyond 6-month timeframes. These production adjustments help moderate total energy demand while reducing industrial output and employment levels.

Medium-term Structural Changes (6-18 months)

Supply chain reconfiguration costs reflect business adaptations to sustained higher energy transportation expenses. Manufacturing operations with global supply chains report supply chain restructuring costs averaging 8-15% of annual procurement budgets to reduce transportation dependency and geographic concentration risks.

Energy efficiency acceleration programmes receive enhanced investment priority as organisations seek to reduce exposure to volatile energy costs. Industrial energy efficiency investments typically generate payback periods of 2-4 years under normal energy cost conditions, but current elevated costs reduce payback periods to 12-18 months for many efficiency technologies.

Alternative energy adoption timelines accelerate as economic competitiveness improves relative to conventional energy sources. Solar and wind power project development receives enhanced financing availability, with project completion timelines compressed from typical 24-36 months to 18-24 months through expedited permitting and equipment prioritisation.

Long-term Economic Transformation (18+ months)

Permanent energy security infrastructure investments reshape regional development priorities and capital allocation patterns. Port infrastructure expansion projects for alternative supply routes receive accelerated approval and financing, with major terminal capacity additions planned for Cape route destinations and Arctic shipping facilities.

Technology innovation acceleration in energy sector reflects both public and private investment priorities shifting toward supply security technologies. Research and development funding for energy storage, alternative fuel production, and supply chain resilience technologies has increased by approximately 60-80% compared to pre-disruption levels.

Long-term Economic Impact Matrix:

| Impact Category | 18-24 Months | 24-36 Months | 36+ Months |

|---|---|---|---|

| Energy Mix Changes | 15-25% alternative | 25-40% alternative | 40-60% alternative |

| Infrastructure Investment | $200-400B globally | $400-800B globally | $800B+ globally |

| Trade Pattern Shifts | 20-30% route changes | 40-60% route changes | Permanent restructuring |

| Technology Adoption | Accelerated deployment | Market transformation | New baseline standards |

How Do Regional Economies Adapt to Energy Supply Shocks?

Asia-Pacific Vulnerability Assessment

Import dependency analysis reveals significant variation in vulnerability across Asia-Pacific economies. Japan imports approximately 99% of petroleum requirements, while Australia maintains substantial domestic production capacity creating relative energy security. China's 73% import dependency combined with large absolute consumption volumes creates systemic vulnerability requiring comprehensive mitigation strategies.

Strategic reserve adequacy varies dramatically across regional economies. Japan maintains approximately 145 days of petroleum import coverage through government and industry reserves, while many Southeast Asian economies maintain coverage periods of only 30-60 days. This reserve capacity differential affects both crisis response capability and economic vulnerability during extended disruptions.

Regional cooperation mechanisms for supply sharing include emergency oil-sharing arrangements through the International Energy Agency and bilateral agreements between neighbouring countries. However, activation of these arrangements requires consensus among participating nations and may face political constraints during crisis periods when domestic priorities intensify. Consequently, the Strait of Hormuz oil disruption tests these cooperation frameworks.

European Energy Security Responses

Diversification strategies away from Middle Eastern petroleum supplies accelerate European efforts to reduce geographic concentration risks. Current initiatives include expanded pipeline connections to North African producers and increased LNG import terminal capacity to accommodate Western Hemisphere suppliers. These infrastructure investments require 3-5 year completion timelines for major projects.

Renewable energy deployment acceleration receives enhanced policy support through revised subsidy frameworks and expedited permitting procedures. Wind power capacity expansion projects report permitting timeline reductions of 30-40% compared to historical procedures, while solar installation projects receive enhanced financing availability through government-backed programmes.

Industrial competitiveness impacts from higher energy costs create policy tensions between environmental objectives and economic preservation. Energy-intensive manufacturing sectors report margin compression of 15-25% under current energy cost conditions, leading to requests for temporary regulatory relief and transition period extensions for emission reduction requirements.

North American Market Dynamics

Domestic production capacity utilisation in North America provides relative insulation from global supply disruptions, though transportation infrastructure creates regional price variations. U.S. crude production operates at approximately 92% of maximum capacity, while Canadian oil sands production maintains expansion capacity constrained primarily by pipeline transportation bottlenecks.

Export opportunity assessment reveals potential for increased North American petroleum product exports to global markets experiencing supply constraints. However, export capacity expansion requires terminal infrastructure investments and regulatory approvals that typically require 18-36 month timelines for completion.

Cross-border energy trade between the United States, Canada, and Mexico provides additional supply flexibility during crisis periods. Pipeline capacity between these countries operates at approximately 75% utilisation under normal conditions, providing buffer capacity for increased regional energy trade during global supply disruptions.

What Investment and Policy Responses Shape Recovery?

Capital Allocation Shifts

Energy infrastructure investment priorities reflect changing risk assessments and security considerations following sustained supply disruptions. Pipeline capacity expansion projects receive enhanced financing availability despite higher construction costs, while renewable energy projects benefit from improved economic competitiveness against volatile fossil fuel alternatives.

Technology development funding patterns demonstrate increased focus on supply chain resilience and energy storage capabilities. Battery storage technology receives investment increases of 45-60% as grid stability becomes priority during energy transition periods. Similarly, hydrogen production technology funding increases as alternative fuel development gains strategic importance.

Risk management strategy evolution among institutional investors includes enhanced exposure limits for geographic concentration risks and increased portfolio allocations toward energy security technologies. Sovereign wealth funds report allocation increases of 8-12% toward energy infrastructure and technology investments compared to pre-disruption portfolio compositions.

Regulatory and Policy Framework Changes

Strategic reserve policy modifications across major consuming nations include expanded target inventory levels and diversified storage locations. The United States is evaluating Strategic Petroleum Reserve capacity increases of 20-30% while investigating geographic distribution improvements to reduce transportation vulnerabilities during crisis periods.

International cooperation agreement updates focus on enhanced information sharing and coordinated response mechanisms. Bilateral and multilateral energy security agreements receive accelerated negotiation timelines, with emphasis on emergency supply sharing arrangements and joint investment in alternative supply infrastructure.

Emergency response protocol improvements incorporate lessons learned from current disruption management experiences. Government agencies report response time improvements of 25-40% for emergency reserve activation procedures, while private sector coordination mechanisms receive enhanced legal frameworks for crisis period cooperation.

Frequently Asked Questions: Understanding Hormuz Disruption Economics

How long do oil price effects typically persist after chokepoint reopening?

Historical analysis indicates that price normalisation following major chokepoint reopening typically requires 6-18 months for full market adjustment. This timeline reflects several factors including inventory rebuilding requirements, risk premium persistence as markets assess recurrence probability, and supply chain restoration timelines for alternative routing arrangements that developed during disruption periods.

Market psychology also influences recovery duration, with traders maintaining elevated volatility expectations until sustained normal operations demonstrate stability restoration. The current situation may experience longer normalisation periods due to the extended duration of constraints and the comprehensive alternative supply arrangements that have developed.

Which industries experience the greatest disruption beyond direct energy costs?

Chemical manufacturing faces the most severe secondary impacts due to dual exposure from both petrochemical feedstock costs and elevated transportation expenses for global supply chains. Agriculture encounters significant effects through fertiliser cost increases, with nitrogen fertiliser prices typically increasing 15-30% during sustained oil disruptions.

Aluminium production suffers from energy-intensive smelting operations requiring substantial electricity inputs, while transportation and logistics sectors face margin compression from fuel cost increases combined with route optimisation requirements. These industries often experience profit margin reductions of 20-40% during extended disruption periods.

Can renewable energy adoption accelerate meaningfully during oil supply crises?

Energy security concerns historically drive policy support enhancements for alternative energy development, though immediate substitution capabilities remain constrained by infrastructure and technology deployment timelines. Current renewable energy projects benefit from accelerated permitting processes reducing typical approval timelines by 30-50%.

However, renewable electricity generation cannot immediately substitute for transportation fuel requirements or petrochemical feedstock needs that drive oil demand. Meaningful renewable energy impact on petroleum import dependency typically requires 3-7 year development periods for substantial capacity additions, though policy frameworks established during crisis periods often persist beyond immediate disruption resolution.

This analysis is based on market conditions and publicly available information as of April 2026. Energy markets remain highly volatile, and investors should conduct independent research and consult financial advisors before making investment decisions. The information presented here is for educational purposes and should not be considered as investment advice.

Ready to Capitalise on Energy Market Volatility?

Whilst the Strait of Hormuz oil disruption creates significant market uncertainty, it also generates exceptional opportunities for investors who can identify and act upon emerging developments quickly. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping subscribers capitalise on market movements and identify actionable opportunities ahead of broader market recognition—begin your 14-day free trial today to position yourself advantageously in volatile energy markets.