July 13, 2026

The global energy infrastructure operates as a delicate network of interdependent systems, where single points of failure can cascade into worldwide economic disruption. When examining systemic risk within petroleum markets, few scenarios present greater threat multipliers than a Strait of Hormuz oil supply disruption that can completely halt maritime chokepoints facilitating international crude oil flows. Understanding these vulnerabilities requires analysis of both immediate market mechanics and long-term structural adaptations that emerge when established supply chains face existential threats.

How Does the Strait of Hormuz Control Global Energy Markets?

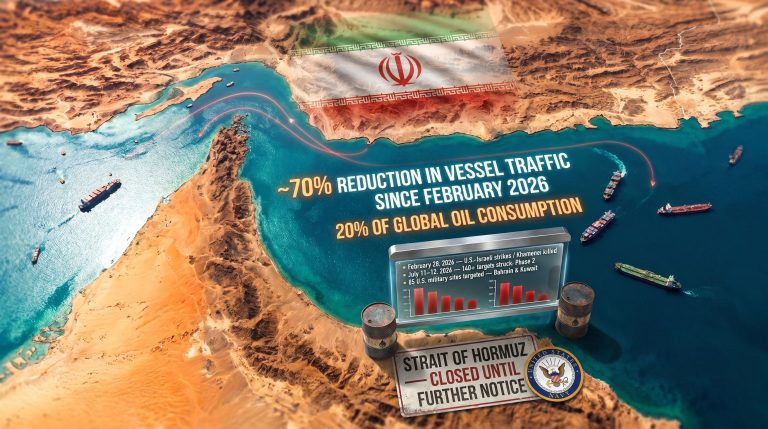

The Persian Gulf waterway functions as the world's most critical energy transit corridor, with approximately 20% of global oil supply flowing through its narrow passage under normal operating conditions. This concentration creates an asymmetric dependency structure where consuming nations face disproportionate vulnerability to supply disruptions regardless of their domestic production capabilities.

The Economics Behind the World's Most Critical Oil Chokepoint

Current market data demonstrates the immediate price transmission effects when a Strait of Hormuz oil supply disruption occurs. As of March 2026, WTI crude surged 8.5% to $81 per barrel, reaching levels not observed since July 2024, while Brent crude climbed 7% to $85 per barrel. These developments align with broader WTI & Brent energy forecasts that anticipate elevated volatility during geopolitical tensions.

The economic magnitude becomes clearer when examining traffic patterns during crisis periods. Ship-tracking data reveals that maritime activity through the strait collapsed by more than 95% during recent geopolitical tensions, as reported by NBC News. Furthermore, this demonstrates how quickly psychological risk factors translate into operational decisions by tanker operators and cargo owners.

Geographic dependency analysis reveals that major consuming nations maintain varying degrees of exposure to Persian Gulf supply chains:

- China: Implemented immediate export restrictions on diesel and gasoline to prioritise domestic supply

- Japan: Refiners formally requested government consideration of Strategic Petroleum Reserve releases

- Kuwait: Actively reduced refinery processing rates as regional supply chains tightened

Supply Chain Architecture Through Persian Gulf Waters

Export terminal infrastructure throughout the Gulf region concentrates massive throughput capacity at strategically vulnerable locations. Saudi Arabia's Ras Tanura facility, UAE's Fujairah terminal complex, and Kuwait's export infrastructure collectively handle millions of barrels daily under normal operations, creating bottleneck effects when alternative routing becomes necessary.

Pipeline bypass systems provide limited relief during maritime disruptions. Saudi Arabia's East-West Pipeline offers theoretical capacity to transport crude to Red Sea export terminals, bypassing Strait transit requirements. However, practical limitations include maintenance requirements, competing domestic demand, and finite surge capacity during emergency scenarios.

Tanker fleet logistics present additional constraints during crisis periods. Vessel owners demonstrate risk aversion despite insurance coverage remaining technically available, indicating that commercial decisions incorporate broader geopolitical assessment beyond pure coverage availability. Consequently, this behavioural pattern suggests that alternative routing requires not just infrastructure capacity but also commercial risk tolerance from logistics providers.

When big ASX news breaks, our subscribers know first

What Are the Immediate Economic Shockwaves of Supply Disruption?

Price volatility mechanisms during chokepoint closures operate through layered risk assessment rather than simple supply-demand calculations. Market analyst Priyanka Sachdeva from Phillip Nova Pte noted that incremental geopolitical events can trigger disproportionate price responses when markets already operate in heightened sensitivity modes.

| Price Impact Timeline | WTI Response | Brent Response | Market Driver |

|---|---|---|---|

| Day 1-3 | +8.5% to $81/bbl | +7% to $85/bbl | Initial risk premium |

| Week 1-2 | Potential +35% | Potential +40% | Supply shortage reality |

| Month 1+ | $110-130 range | $115-135 range | Strategic reserve depletion |

The differential performance between WTI and Brent crude provides insight into market psychology during supply disruptions. WTI has demonstrated faster rally characteristics as traders actively seek crude sources with reduced exposure to Gulf shipping bottlenecks. In addition, this creates regional price arbitrage opportunities that align with broader oil price movements amid trade war scenarios.

Cascading Effects on Regional Energy Security

Regional supply chain tightening occurs through multiple transmission mechanisms. Chinese government directives to suspend refined product exports while maintaining domestic supply prioritisation reflects hierarchical decision-making where national energy security takes precedence over export revenues. This policy shift indicates expectations that refining margins may compress significantly as competing demand prioritises local consumption.

European LNG market disruption emerges as a secondary effect when Qatar's massive liquefied natural gas export capacity faces similar transit constraints. The interconnected nature of energy infrastructure means that crude oil supply disruption often coincides with natural gas supply chain stress, compounding regional energy security challenges.

Freight rate escalation affects all alternative routing options, though specific multiplication factors require continuous monitoring as market conditions evolve. Rising transportation costs create inflationary pressure that extends beyond energy markets into broader commodity sectors dependent on petroleum inputs.

Which Industries Face the Greatest Disruption Risk?

Refining Sector Operational Challenges

Processing rate adjustments represent the most immediate industrial response to supply chain disruption. Kuwait's decision to reduce refinery processing rates demonstrates proactive capacity management in response to anticipated input constraints rather than reactive adjustment to existing shortages.

Crude slate optimisation becomes critical when traditional supply sources face disruption. Refineries designed for specific crude oil characteristics must adjust processing parameters, potentially affecting:

- Product yield ratios between petrol, diesel, and heavy fuel oil

- Processing efficiency and energy consumption

- Equipment maintenance scheduling and operational reliability

- Regional product price differential patterns

Refining margin impacts vary by geographic location and facility configuration. Asian refineries with higher dependency on Middle Eastern crude face immediate input cost pressure, whilst refineries with flexible crude slate capabilities maintain greater operational resilience.

Transportation and Logistics Cost Escalation

Maritime freight rate increases affect global supply chains beyond petroleum products. Alternative routing through the Cape of Good Hope adds approximately 8,000 nautical miles and 7-10 days transit time compared to Suez Canal routing, creating cost multiplication effects throughout international trade networks.

Insurance premium adjustments reflect risk assessment evolution as geopolitical events develop. Whilst technical coverage remains available, commercial terms adjust to incorporate perceived risk levels, affecting transportation economics for all cargo types transiting alternative routes.

Supply chain rerouting requires logistical coordination across multiple transportation modes. Companies dependent on just-in-time inventory management face particular vulnerability when transit times extend unexpectedly, forcing adjustment to inventory carrying costs and working capital requirements.

How Do Strategic Petroleum Reserves Function During Crisis?

National Emergency Response Mechanisms

Strategic petroleum reserves serve dual functions as physical supply buffers and market psychology management tools. The Trump administration's announcement regarding potential U.S. Strategic Petroleum Reserve releases preceded actual inventory deployment, suggesting that announcement effects may provide temporary market stabilisation before quantified supply injection occurs.

Key Insight: Strategic reserves provide varying import coverage duration by country, but coordinated releases require international cooperation to prevent market manipulation and maximise psychological impact on price volatility.

Reserve capacity utilisation presents optimisation challenges for policymakers. Release timing involves trade-offs between early intervention to prevent extreme price volatility versus preserving inventory for extended disruption scenarios. Historical analysis suggests that market participants respond to release announcements before physical supply actually enters commercial channels.

Japanese refiner requests for Strategic Petroleum Reserve releases indicate downstream industry assessment that crude availability concerns may develop before refined product shortages materialise. This progression suggests refining margin pressure precedes consumer-level supply disruption.

Reserve Release Economics and Market Stabilisation

International Energy Agency coordination frameworks facilitate multilateral response to supply disruptions, though implementation requires member country compliance and synchronised timing. The effectiveness of coordinated releases depends on aggregate volume relative to market shortage estimates and participant confidence in sustained cooperation.

Market timing considerations affect reserve release impact. Early-stage releases may stabilise prices at artificially elevated levels, potentially discouraging market-driven supply adjustments. Delayed releases risk failing to prevent economically disruptive price spikes that trigger broader macroeconomic effects.

Strategic reserve economics involve sunk-cost inventory held specifically for emergency deployment. Replacement costs vary significantly depending on market conditions at the time of replenishment, creating fiscal considerations that influence release decision-making timelines.

What Alternative Supply Routes Emerge During Disruptions?

Pipeline Bypass Infrastructure Analysis

Saudi Arabia's East-West Pipeline system provides the most significant bypass capacity for Gulf crude exports, with theoretical throughput capabilities that could partially offset Strait transit limitations. However, practical capacity depends on maintenance status, competing domestic refinery demand, and surge capability during emergency operations.

UAE's Abu Dhabi Crude Oil Pipeline represents another bypass option, though operational limits and current utilisation rates affect incremental capacity availability. These pipeline systems require coordination between producing nations and receiving terminals to optimise throughput during crisis periods.

Iraq-Turkey pipeline infrastructure offers partial Gulf alternative routing, though capacity constraints and geopolitical considerations between Iraq and Turkey influence operational reliability. Historical disruptions demonstrate vulnerability to political tensions affecting sustained throughput capability.

Shipping Route Diversification Economics

Cape of Good Hope routing presents the primary maritime alternative to Strait of Hormuz oil supply disruption and Suez Canal transit. This routing involves significant economic trade-offs:

- Additional transit time: 7-10 days extension

- Distance increase: 8,000+ nautical miles

- Fuel consumption: Substantially higher operating costs

- Charter rates: Extended voyage duration affects vessel availability

Red Sea corridor utilisation depends on Egyptian Suez Canal capacity and regional security conditions. Canal transit fees and potential congestion during high-volume periods create additional cost considerations for alternative routing strategies.

Arctic shipping routes provide seasonal alternatives for Asian markets, though ice conditions limit availability to approximately May through September in most Arctic passages. Climate conditions and specialised vessel requirements restrict practical utilisation during winter months when many supply disruptions occur.

How Do Geopolitical Risk Premiums Affect Long-term Energy Investment?

Capital Allocation Shifts in Uncertain Supply Environments

Upstream investment acceleration in non-Gulf regions reflects investor response to concentrated supply risk exposure. Projects in politically stable jurisdictions with diversified export options receive capital allocation preference during periods of heightened Middle Eastern supply uncertainty.

Strategic storage expansion projects gain investment priority as consuming nations seek to reduce dependency on continuous supply chain operation. These infrastructure investments provide buffer capacity that reduces vulnerability to temporary supply disruptions whilst creating employment and industrial capacity in importing regions.

Renewable energy transition timeline acceleration occurs when supply security concerns compound environmental and economic motivations for alternative energy development. Policy frameworks supporting renewable deployment often receive enhanced political support during periods of fossil fuel supply uncertainty.

Insurance and Financial Market Responses

Energy commodity derivatives markets experience elevated volatility patterns during supply disruption periods. Options markets reflect increased uncertainty through higher implied volatility levels, whilst futures curves develop contango or backwardation patterns based on expected disruption duration.

Political risk insurance premium calculations incorporate both probability assessment and potential loss magnitude evaluation. Coverage costs increase substantially when insurers assess elevated likelihood of sustained supply disruption, affecting project economics across energy-dependent industries.

Sovereign wealth fund energy security investment strategies evolve to emphasise supply diversification and strategic reserve capacity. These institutional investors increasingly prioritise energy infrastructure assets that enhance national energy security over purely financial return optimisation.

The next major ASX story will hit our subscribers first

What Historical Precedents Guide Current Market Responses?

Comparative Analysis of Previous Chokepoint Disruptions

Historical supply disruption events provide frameworks for understanding market response patterns and policy effectiveness. Each major disruption generated specific lessons that influence contemporary response strategies:

| Event | Duration | Peak Price Impact | Recovery Timeline | Lessons Applied |

|---|---|---|---|---|

| Iran-Iraq War (1980s) | 8 years intermittent | +150% | 2-3 years | Strategic reserve creation |

| Gulf War (1991) | 6 months | +100% | 12 months | OPEC spare capacity protocols |

| Iraq Invasion (2003) | 3 months | +40% | 18 months | Supply chain diversification |

The Iran-Iraq War period demonstrated that extended regional conflicts could sustain elevated price levels for multiple years whilst spurring strategic reserve development programmes globally. This experience influenced policy frameworks for emergency response coordination among consuming nations.

Gulf War disruption patterns showed that coordinated military action could restore supply flows relatively quickly, though price recovery required additional time for market confidence restoration. OPEC production strategies developed during this period continue to influence production adjustment strategies.

Iraq invasion market response illustrated how anticipated supply disruption could generate price volatility exceeding actual physical supply losses. Market psychology management became recognised as equally important to physical supply replacement during crisis response planning.

Which Economic Sectors Experience Secondary Impact Waves?

Manufacturing and Industrial Production Adjustments

Petrochemical feedstock cost transmission creates cascading effects throughout plastics and chemical manufacturing sectors. Production facilities dependent on petroleum-derived inputs face margin compression that often triggers output reduction decisions and supply chain adjustment throughout downstream industries.

Transportation-intensive industries experience immediate operational cost increases. Airlines implement fuel surcharges and route optimisation strategies, whilst shipping companies adjust charter rates to reflect increased fuel costs and extended voyage requirements for alternative routing.

Energy-intensive manufacturing sectors including steel, aluminium, and cement production face particular vulnerability to sustained energy price elevation. These industries often operate with thin margins that cannot absorb substantial energy cost increases without production adjustment or price pass-through to end consumers.

Consumer Price Index and Inflation Transmission Mechanisms

Petrol and heating oil price pass-through follows predictable timelines based on regional distribution infrastructure and inventory turnover rates. Retail fuel prices typically reflect crude oil cost changes within 1-2 weeks, though regional variations depend on local refining capacity and distribution logistics.

Regional inflation differential patterns emerge based on energy import dependency levels. Countries with higher petroleum import ratios experience more pronounced inflationary pressure than nations with substantial domestic production or strategic reserve utilisation capability.

Central bank monetary policy responses to energy-driven inflation present complex trade-offs between addressing inflationary pressure and supporting economic growth during supply shock periods. Historical precedents suggest that temporary supply disruptions warrant different policy responses than sustained structural supply changes.

How Effective Are Emergency Market Interventions?

Government Policy Tool Assessment

Strategic reserve releases demonstrate variable effectiveness depending on deployment volume, timing, and coordination with other policy measures. Historical analysis indicates that announcement effects often provide immediate market response before physical supply injection occurs, suggesting psychological intervention may complement quantified supply replacement.

Export restrictions and domestic supply prioritisation policies, as demonstrated by China's recent diesel and petrol export suspension, represent trade-offs between international market cooperation and domestic energy security. These policies can exacerbate global supply constraints whilst protecting domestic consumers from price volatility.

Price ceiling mechanisms create market distortion risks that may discourage supply adjustment responses needed for long-term market stability. Whilst providing short-term consumer protection, administratively controlled prices often generate shortages or black market activity when sustained over extended periods.

International Coordination Frameworks

IEA emergency response protocols require member country compliance and coordinated timing to maximise market impact. Historical deployment suggests that synchronised releases achieve greater price stabilisation effect than individual country actions, though coordination complexity can delay response implementation.

OPEC+ spare capacity deployment decisions involve geopolitical considerations beyond pure market economics. Producer nations balance revenue optimisation against market stability objectives, with deployment timing influenced by diplomatic relationships and strategic policy objectives.

G7 and G20 energy security cooperation mechanisms provide diplomatic frameworks for coordinating international response to supply disruptions. These multilateral institutions facilitate information sharing and policy coordination, though implementation depends on individual member country policy priorities and domestic political considerations.

What Long-term Structural Changes Result from Supply Shocks?

Energy Security Architecture Evolution

Domestic production investment acceleration in importing nations reflects strategic policy shifts toward reduced dependency on unstable supply sources. These investments often receive government support through fiscal incentives, regulatory fast-tracking, or direct financial participation in development projects.

Strategic alliance formation for supply diversification creates new bilateral and multilateral energy cooperation agreements. Consuming nations develop preferential trading relationships with politically stable producing regions whilst investing in transportation infrastructure to support diversified supply chains.

Infrastructure development for alternative transport corridors requires substantial capital investment and international cooperation. Pipeline projects, terminal expansion, and shipping infrastructure development respond to demonstrated vulnerability in existing supply chain architecture.

Market Structure Adaptation Patterns

Spot versus long-term contract ratio adjustments reflect changed risk assessment by market participants. Companies increase long-term contract coverage to ensure supply security, whilst maintaining spot market participation for operational flexibility and price optimisation during normal market conditions.

Regional price benchmark development outside Gulf influence creates alternative pricing mechanisms that reduce dependency on Middle Eastern crude price discovery. These benchmarks provide hedging instruments and contract reference points for transactions involving non-Gulf crude sources.

Financial instrument innovation for supply security hedging generates new risk management tools for companies exposed to supply disruption risk. Furthermore, these instruments include supply interruption insurance, force majeure derivatives, and geopolitical risk hedging products designed to provide financial protection during supply chain disruption.

The implications of an oil price rally under tariffs become particularly significant when combined with chokepoint vulnerabilities. However, understanding these dynamics alongside oil price stagnation insights helps market participants prepare for various scenarios.

According to analysis by Fitch Ratings, whilst temporary closures may have limited long-term price impact, the immediate market disruption remains substantial for global energy security planning.

Investment Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Energy markets involve substantial risk, and geopolitical events can cause rapid and unpredictable price movements. Historical performance does not guarantee future results, and investors should conduct their own research and consult qualified financial advisors before making investment decisions.

Looking to Capitalise on Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including critical energy transition minerals that become increasingly valuable during global supply disruptions. Subscribers gain immediate access to actionable trading opportunities whilst understanding how historic discoveries can generate exceptional returns through early identification of market-moving announcements. Begin your 14-day free trial today to position yourself ahead of market-shifting energy and commodity discoveries.