June 18, 2026

The Geometry of Energy Dependence: How Asia's Refining Backbone Is Wired to a Single Waterway

Every industrial economy runs on assumptions. One of the most deeply embedded assumptions within Asian energy markets is that crude oil from the Persian Gulf will flow continuously, predictably, and at manageable cost. That assumption is built into refinery investment decisions, long-term supply contracts, and national energy security frameworks across the continent. The Strait of Hormuz reopening oil supply to Asia is therefore not simply a logistical event — it is a stress test of those embedded assumptions. When the strait closes, even partially, those assumptions do not simply become uncertain. They become structurally exposed.

Understanding what happens when the strait reopens requires grasping what its closure actually meant, and why the correction is not simply a return to equilibrium.

When big ASX news breaks, our subscribers know first

The Strategic Weight of a Single Waterway

Roughly 20 million barrels of petroleum liquids transited the Strait of Hormuz every day in 2024, a volume representing approximately 20% of total global petroleum consumption. No other maritime chokepoint concentrates such a disproportionate share of energy exposure into a single geographic passage.

The directional breakdown of those flows is what makes the strait so consequential for Asia specifically:

- 84% of all crude oil and condensate passing through Hormuz was bound for Asian destinations in 2024

- 83% of LNG transiting the strait also moved eastward toward Asian buyers

- The four largest Asian recipients, China, India, Japan, and South Korea, collectively absorbed 69% of all Hormuz crude and condensate flows directed toward Asia

No other maritime chokepoint on Earth concentrates so much energy exposure into a single regional bloc. Asia's industrial economies are structurally dependent on Hormuz in a way that no short-term supply diversification strategy can fully neutralise.

These are not marginal dependencies. They are structural ones, embedded across decades of refinery design, pipeline infrastructure decisions, and bilateral supply arrangements. Furthermore, the role of oil in the global economy means that such concentrated exposure carries consequences well beyond the Asian continent. The strait is not merely a transit route. It is, in functional terms, Asia's energy artery.

What the Reopening Actually Means: Beyond the Binary

There is a natural tendency to frame the Strait of Hormuz reopening as a simple binary — either open or closed. Market reality operates differently. Evidence from the disruption period indicates that some tanker traffic continued moving through the strait even during periods of elevated military tension, pointing to a tiered access environment where certain vessel types, flag states, or cargo categories faced differential treatment.

This matters for forecasting because it means the reopening is not a single switch being flipped. It is a progressive restoration of confidence across a layered system involving vessel operators, cargo insurers, flag state authorities, port logistics, and buyer procurement teams.

Goldman Sachs analysts, including Daan Struyven, have projected that Persian Gulf crude exports could normalise to pre-conflict levels by the end of July 2026. However, full market normalisation — covering shipping confidence, insurance premium structures, and freight rate stabilisation — is widely expected to extend across a period of four to six months or longer beyond that initial volume recovery.

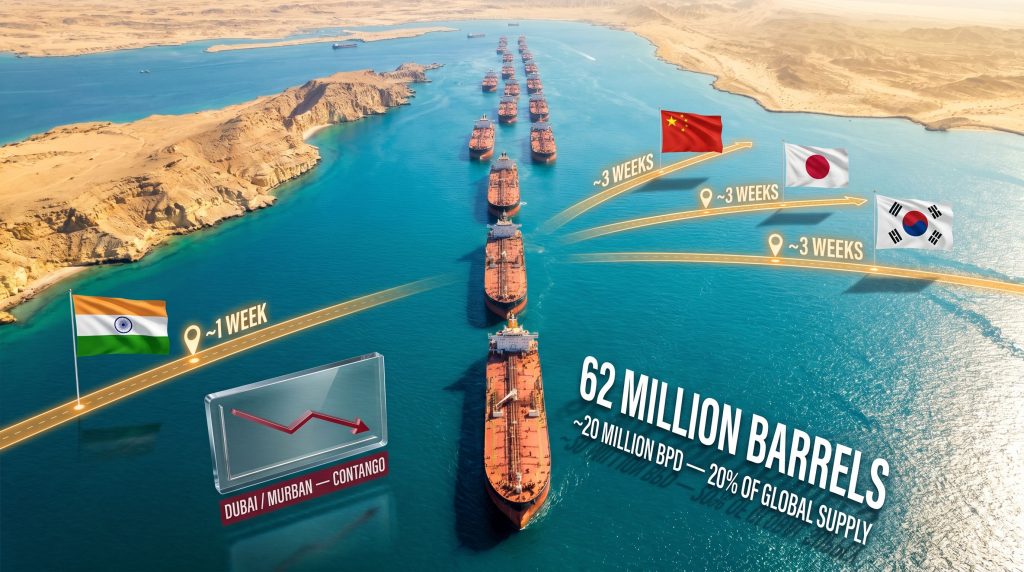

The Tanker Backlog: Quantifying the Immediate Supply Pressure

Vessel tracking data from Signal Group identifies approximately 31 supertankers currently positioned inside the Persian Gulf and awaiting passage. These vessels carry a combined estimated 62 million barrels of crude oil. The actual figure may be higher, as some vessels are believed to have switched off their Automatic Identification System (AIS) transponders to avoid detection or insurance scrutiny — a practice that has become more common during periods of regional maritime tension.

The AIS-dark phenomenon is particularly significant from an analytical standpoint. When vessels disable transponders, they effectively disappear from commercial tracking systems, creating blind spots in supply estimates. This means the 62-million-barrel figure represents a floor, not a ceiling.

Transit timelines from the Persian Gulf following reopening are estimated as follows:

| Destination Region | Estimated Transit Time | Key Buyers |

|---|---|---|

| India | ~1 week | Indian state refiners |

| China | ~3 weeks | State-owned energy majors |

| Japan | ~3 weeks | Utilities, integrated refiners |

| South Korea | ~3 weeks | Major refining complexes |

Three supertankers operated by Bahri, Saudi Arabia's national shipping company, emerged in the Gulf of Oman after spending approximately two months inside the Persian Gulf. As Asia's oil-thirsty economies cautiously welcome the reopening, this provided one of the earliest tangible signals that export logistics are beginning to normalise.

Why Asian Refiners Are Not Simply Opening Their Arms

The arrival of 62 million barrels into Asian markets would typically be welcomed by refinery procurement teams. In the current market context, however, it creates a genuine problem.

A Market That Adapted Before the Reopening

During the disruption period, Asian refiners did not sit idle. They restructured their procurement rapidly:

- Refiners across the region scrambled to lock in alternative crude sources, including US barrels, to replace disrupted Persian Gulf volumes

- China deliberately stayed out of spot markets during the acute disruption phase — a strategic restraint that preserved its buying power for a post-reopening environment

- Japan activated domestic storage reserves to bridge near-term supply gaps without paying elevated spot premiums

- Persian Gulf producers including Abu Dhabi National Oil Company (ADNOC) and Kuwait Petroleum Corporation continued marketing supply and routing some volumes out of Hormuz during the conflict period

- Iraqi crude production increased during the disruption and is expected to continue rising following the reopening, adding a compounding supply layer

The consequence of this adaptive behaviour is that by mid-June 2026, Asian refiners entered the post-reopening period already well-supplied for both current and forward months. The urgency that would normally accompany a large supply release simply does not exist in this market.

Processing Rate Cuts and Demand Suppression

Elevated crude prices during the disruption period introduced a second complicating variable: refiners reduced their throughput rates. When input costs spike and refined product demand softens, the rational response is to process less crude, not more.

This means Asian refinery utilisation entered the reopening period at below-normal levels, reducing immediate absorption capacity precisely when the largest single supply wave in recent memory is approaching.

At least one South Korean refiner had already been offering above-normal volumes of distillate fuel — encompassing diesel and jet fuel categories — into the market ahead of a full Hormuz reopening. This represents a pre-emptive monetisation strategy: sell product now before the crude inflow depresses prices further.

Warning for Market Participants: The convergence of pre-built alternative supply, reduced refinery run rates, and an approaching 62-million-barrel crude wave creates conditions for meaningful near-term price correction across Asian crude benchmarks and refined product markets.

Benchmark Pricing Has Already Moved: Reading the Forward Curve

Markets rarely wait for physical delivery to reprice. The anticipation of the reopening has already produced measurable shifts across key pricing structures, and consequently, these movements are already feeding through into broader oil price movements that extend well beyond the Asian region.

The Contango Signal and What It Reveals

The forward curve for benchmark West Asian crudes, including Dubai and Murban, shifted into contango for the first time since the conflict began. Contango, where near-term prices fall below forward prices, is a structural bearish signal. It means the market expects near-term oversupply relative to demand.

| Market Signal | Pre-Reopening Condition | Post-Reopening Signal |

|---|---|---|

| Dubai/Murban forward curve | Backwardation (bullish) | Contango (bearish) |

| Oman crude vs. Dubai benchmark | Premium | Discount |

| Diesel cargo pricing | Premium to benchmark | Discount to benchmark |

| South Korean distillate offers | Normal volumes | Above-normal (pre-emptive selling) |

Oman crude, which typically commands a premium over its underlying Dubai benchmark due to quality and logistics factors, moved to a discount this week. This is a significant reversal of a structural pricing relationship that has persisted for extended periods. Separately, at least one diesel cargo traded at a discount to its benchmark, compared with the premiums that characterised the disruption period.

These are not noise signals. They represent coordinated repricing across multiple linked markets simultaneously — each confirming the same underlying expectation: supply is about to overwhelm near-term demand. Indeed, participants monitoring oil futures markets will recognise these structural shifts as consistent with broader forward curve dynamics observed during major supply realignment events.

Country-Level Exposure: Who Faces What, and When

India: The One-Week Exposure Window

India occupies a structurally unique position in this supply wave scenario. Its refining sector, anchored by large state-owned operators, faces repricing pressure within approximately one week of any vessel departing the Persian Gulf. Indian refiners had been actively diversifying procurement during the disruption, which means the return of Persian Gulf supply creates a potential inventory overhang that will need to be managed through either storage absorption or throughput increases.

The decision refiners face is not straightforward. Increasing processing rates generates more refined product into a market where product prices are already softening. Placing barrels into operational storage, furthermore, consumes tankage capacity that may be needed for other purposes. Notably, India's oil supply risks are expected to ease materially as Persian Gulf flows resume, though near-term inventory management remains a key operational challenge.

China: Strategic Patience, Now Potentially Rewarded

China's deliberate absence from spot markets during the disruption period was not passive. It was calculated positioning. By avoiding elevated spot prices while allowing its contracted volumes and storage reserves to absorb near-term demand, China preserved significant purchasing power for the post-reopening environment.

Chinese state-owned energy majors possess substantial storage infrastructure — including both commercial tankage and strategic petroleum reserves — capable of absorbing opportunistic volume purchases at depressed prices. The three-week transit window from the Persian Gulf to Chinese ports provides a useful buffer period for procurement teams to assess price trajectories before committing to large-volume spot contracts.

Japan and South Korea: Contract Leverage in a Buyer's Market

Both Japan and South Korea rely heavily on long-term supply contracts with Persian Gulf producers, including ADNOC and Kuwait Petroleum Corporation. Both suppliers had been actively marketing available barrels and routing some volumes out of Hormuz even during the disruption period, meaning neither Japanese nor Korean refiners faced a complete supply vacuum.

The combination of a full Hormuz reopening, continued Iraqi production growth, and pre-built alternative supply positions these two nations' refining sectors to potentially renegotiate contract terms or defer spot market commitments during the oversupply window.

The next major ASX story will hit our subscribers first

The Iraq Variable: An Amplifying Supply Layer

One aspect of the post-reopening supply picture that deserves closer attention is Iraq's production trajectory. Iraqi crude output increased during the conflict period and is projected to continue rising following the reopening. This matters because it adds a supply increment that is independent of the Hormuz backlog itself.

The tanker queue represents a one-time supply bolus. Iraqi production growth, however, represents a structural addition to available supply that persists beyond the initial backlog clearance. The combination of both factors extending into the second half of 2026 could amplify bearish price conditions in Asian crude benchmarks well beyond what the supertanker queue alone would produce. Understanding these dynamics within global crude market trends provides essential context for evaluating how durable this oversupply environment may prove to be.

A Phased Framework for Normalisation

Full market normalisation following the Strait of Hormuz reopening oil supply to Asia is not a single event. It unfolds across overlapping phases, each with its own conditions and market implications:

| Phase | Timeframe | Key Conditions Required |

|---|---|---|

| Phase 1: Initial Flow | Weeks 1-2 post-reopening | Backlogged supertankers transit; spot prices fall |

| Phase 2: Shipping Confidence Rebuild | Weeks 3-8 | Tanker operators and marine insurers resume standard routing |

| Phase 3: Contract Normalisation | Months 2-4 | Long-term supply agreements re-anchor to Persian Gulf benchmarks |

| Phase 4: Full Market Normalisation | 4-6 months or longer | Insurance premiums normalise; freight rates stabilise; storage overhang clears |

A critical and often underappreciated element of this timeline is the marine insurance market. War risk premiums, which surged significantly during the conflict period, do not disappear the moment a geopolitical agreement is signed. Underwriters require sustained, observable safety records before reducing premium loadings. This creates a lagging cost that continues to suppress shipping economics even after physical flows resume.

LNG Markets: A Parallel Normalisation Story

The crude oil market is not the only segment affected by the Hormuz reopening. The broader LNG supply outlook for Asia will shift meaningfully as normalisation progresses — and with 83% of LNG transiting the strait directed toward Asia, the disruption had pushed Asian LNG spot prices sharply higher. Japanese and South Korean utilities, which depend significantly on LNG for electricity generation, absorbed materially higher procurement costs throughout the conflict period.

The reopening eases this pressure, with Persian Gulf LNG export capacity returning to normal routing. Asian spot LNG prices are expected to soften as supply normalises, providing some relief to power generation costs across the region's two most LNG-dependent major economies.

Key Takeaways for Energy Market Participants

The Strait of Hormuz reopening oil supply to Asia represents one of the most complex near-term market dynamics in the global energy sector. Several points deserve emphasis:

- 62 million barrels across approximately 31 supertankers are positioned to enter Asian markets within weeks, with the real volume likely higher given AIS-dark vessels

- Asian refiners enter this supply wave already well-stocked through alternative procurement, creating genuine risk of storage saturation

- Benchmark pricing has already shifted bearish across Dubai, Murban, and Oman crude structures, confirming market anticipation of oversupply

- China's strategic buying position is the most significant demand-side variable determining how quickly the supply overhang is absorbed

- Iraqi production growth extends the bearish supply environment beyond the immediate backlog, adding duration to the price pressure

- Marine insurance market recovery will lag physical flow normalisation, continuing to affect shipping economics well into the second half of 2026

- Full market normalisation is a process spanning four to six months or longer, not a single reopening event

For readers seeking independent data on global oil transit volumes and maritime chokepoint vulnerability assessments, the U.S. Energy Information Administration publishes detailed analyses of critical energy infrastructure at eia.gov. These resources provide useful context for understanding the systemic importance of the Strait of Hormuz within global energy supply chains.

This article contains forward-looking projections and market analysis based on available data as of mid-June 2026. Forecasts from third-party analysts, including Goldman Sachs, are cited for informational purposes only and do not constitute investment advice. Energy market conditions are subject to rapid change, and readers should conduct their own due diligence before making any investment or procurement decisions.

Want to Capitalise on the Next Major Energy or Commodity Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex data to surface actionable opportunities for both short-term traders and long-term investors. Explore Discovery Alert's discoveries page to see the historic returns that major discoveries have generated, and begin your 14-day free trial today to position yourself ahead of the market.