June 18, 2026

The Strait of Hormuz as a Pressure Valve: How Geography Became Geopolitics

Few physical features on Earth carry as much economic consequence as a narrow band of water barely three kilometres wide at its most navigable point. The Strait of Hormuz has long represented the single most concentrated chokepoint in global energy infrastructure, and its vulnerability to disruption has been a persistent undercurrent in energy market risk modelling for decades. What changed in early 2026 was not the geography, but the willingness of a major actor to actually pull that lever.

Understanding why the US Iran peace pact and Strait of Hormuz reopening matter to global markets requires stepping back from the diplomatic theatre and examining what the closure actually did to the physical architecture of energy supply. Furthermore, examining what the phased reopening now means for crude pricing, shipping economics, and geopolitical stability across a region that has never been short of complexity is equally essential.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Structurally Irreplaceable

The numbers that define Hormuz are worth examining carefully, because they explain why the conflict period produced such immediate and severe economic consequences.

Approximately 20 to 21 percent of the world's total petroleum liquids transit the strait on an annual basis. On a daily basis, historical throughput has consistently exceeded 17 to 18 million barrels of crude oil and refined products. Qatar's liquefied natural gas exports, representing roughly 20 percent of global LNG supply, also move through this corridor. These figures alone make the strait the single most economically loaded geographic chokepoint in existence.

The critical infrastructure reality is that no viable alternative exists at scale. Saudi Arabia's Abqaiq-Yanbu pipeline and the Abu Dhabi Crude Oil Pipeline (ADCOP) offer partial bypass capacity, but together they can redirect only a fraction of total Hormuz throughput. When the strait closes, the global energy system does not smoothly reroute. It absorbs the shock through price.

During the three-month conflict period, that price signal was unambiguous. Brent crude surpassed the $80 per barrel threshold, with supply shock premiums embedded into futures curves across multiple delivery months.

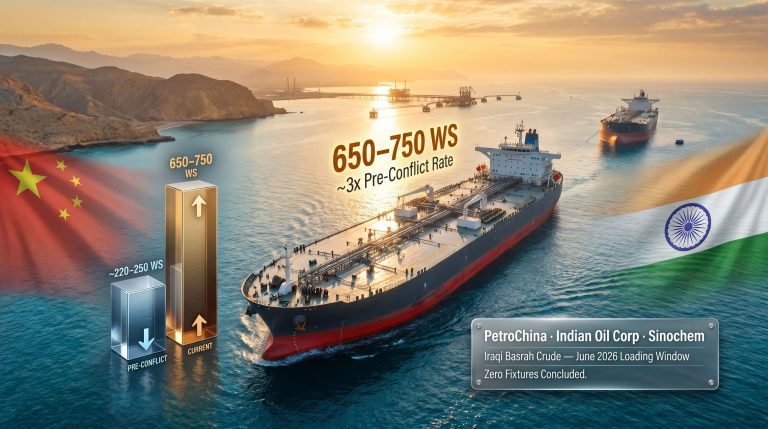

The downstream consequences extended beyond crude pricing. Refining margins in Asia and Europe came under sustained pressure as Gulf supply contracted through Q1 and Q2 2026. Shipping insurers applied war-risk surcharges that effectively priced many commercial operators out of the corridor entirely, pushing tanker traffic onto the much longer Cape of Good Hope route. The additional transit time of approximately 10 to 15 days per voyage added cumulative cost pressure across Asian import supply chains already under strain.

Consumer-level fuel prices in the United States rose materially during the closure period, contributing to political pressure on the Trump administration ahead of November midterm elections. The economic feedback loop from Hormuz to American domestic politics was, consequently, direct and rapid.

What the US-Iran MOU Actually Contains

The agreement that has now taken effect is formally classified as a memorandum of understanding, a designation that carries significant legal and political implications distinct from a ratified international treaty.

MOUs do not require Senate ratification under US constitutional procedure, which allowed the Trump administration to move quickly without congressional approval. The document was initially co-signed digitally by Vice President JD Vance and Iranian Parliament Speaker Mohammad Bagher Ghalibaf, with both heads of state subsequently adding formal signatures. Trump signed the document at the Palace of Versailles near Paris, a location carrying considerable historical resonance as the site where the peace treaty formally ending World War I was signed in 1919.

The choice of an MOU format rather than a formal treaty structure reflects the political constraints on both sides. Tehran cannot be seen domestically as capitulating to a binding US-imposed framework, while Washington avoids the Senate ratification process that would expose the deal to congressional scrutiny and potential veto.

The core provisions of the agreement break down as follows:

| Provision | Detail |

|---|---|

| Strait of Hormuz reopening | Phased, conditional reopening with de-mining operations required |

| Sanctions waivers | Immediate waivers on Iranian oil exports envisioned under draft text |

| Nuclear negotiations | Deferred to a 60-day follow-on talks period |

| Ballistic missile program | Excluded from MOU scope; addressed in subsequent negotiations |

| Development financing | $300 billion economic development program envisaged; no direct US government funding |

| Frozen Iranian assets | Release signalled as probable; framed by Trump as necessary for dollar credibility |

| Enforcement mechanism | US military re-engagement threatened if Iran does not comply |

The $300 billion development program envisaged for Iran has attracted particular attention. Trump clarified that no direct US government funding would be involved, and that Iran's access to the program remains conditional on behavioural compliance. The structural details, funding sources, and governance architecture of this program have not been fully defined in the interim agreement.

The Physical Reality of Reopening: Why It Takes Time

A political declaration and a commercially navigable strait are not the same thing. The MOU establishes the framework for reopening, but the physical implementation involves a series of operational steps that impose their own timeline.

Iran is expected to remove obstacles it deployed during the conflict period. Simultaneously, the US naval blockade is to be lifted as commercial traffic resumes. Shipping experts and analysts cited in post-agreement coverage estimate the next 40 to 50 days represent the operationally critical implementation window, with traffic potentially recovering to approximately 50 percent of pre-conflict levels within the first 30 days if implementation proceeds without major disruption.

Before major commercial operators recommit vessels to the corridor, however, several conditions must be met:

- War-risk insurance classifications must be formally downgraded by underwriters

- Tanker operators that rerouted around Africa face significant cost recalculation as strait economics shift

- Port congestion in alternative routing hubs including Fujairah and Oman's Duqm may temporarily persist even after Hormuz traffic resumes

- Spot freight rates on VLCC (very large crude carrier) routes are expected to reprice rapidly once the corridor is certified as operationally safe

Shipping companies and insurers will make their own independent risk assessments rather than simply following the political declaration. The commercial reopening of the strait is therefore a process, not an event.

How Energy Markets Have Responded

The market reaction to the US Iran peace pact and Strait of Hormuz reopening announcement was immediate and directionally clear, though not without residual uncertainty. The crude oil price trends observed during the conflict period began to reverse sharply as news of the agreement broke.

Brent crude fell below $80 per barrel in the days following the peace pact announcement. WTI crude was trading at approximately $75.33 at the time of reporting, reflecting a -1.9 percent single-session move. Natural gas prices held relatively stable at approximately $3.15, indicating the market's primary relief response was concentrated in crude rather than gas. The price decline partially reversed mid-week, signalling residual uncertainty about implementation timelines and political durability.

In contrast to the oil price rally witnessed during the escalation phase, the forward-looking scenarios energy analysts are now modelling break down along implementation trajectories:

| Scenario | Brent Crude Trajectory | Key Variable |

|---|---|---|

| Smooth implementation | Further decline toward $70-72/bbl | De-mining completed; shipping resumes at 50%+ capacity |

| Partial reopening with delays | Range-bound $76-80/bbl | War-risk insurance reclassification lag |

| MOU breakdown or non-compliance | Spike back above $85-90/bbl | Iranian non-compliance triggers US military response |

| Full normalization and sanctions relief | Potential test of $65-68/bbl | Iranian oil volumes re-enter global supply |

The broader macroeconomic relief thesis was articulated publicly by Trump himself, who acknowledged that continued military escalation risked triggering what he described as an international depression. Bloomberg Economics analysts characterised the preliminary accord as trading Hormuz reopening for economic relief, while noting the exchange appeared asymmetric in Tehran's favour, with Iran's gains described as substantial and new while Washington's gains largely represented a partial recovery of conditions that existed before the conflict began in February.

The Geopolitical Ledger: Winners, Concessions, and Gaps

Iran's Strategic Extraction From the Agreement

Assessing the MOU through the lens of what each party extracted reveals a lopsided initial balance sheet. Iran secured immediate sanctions waivers on oil exports, representing a significant near-term economic lifeline. The $300 billion development program, while conditional, constitutes a substantial long-term economic incentive. Critically, Iran's ballistic missile program was excluded from the MOU's scope entirely, preserving a core strategic deterrent asset that Tehran had made clear was non-negotiable.

Iran also demonstrated something strategically valuable independent of any specific provision: that Hormuz closure works as a coercive instrument. This validation of the strategy carries implications for future negotiations that extend well beyond the current agreement.

Washington's Calculus: What Was Retained and What Was Conceded

The administration secured a cessation of hostilities and the reopening of a critical global energy corridor. These are not trivial outcomes. However, nuclear disarmament, the stated original justification for initiating military action in February, was deferred rather than achieved. Sanctions relief and asset releases represent tangible concessions that critics argue exceed what existed before the conflict began.

Trump's framing of frozen asset release as necessary for dollar credibility represented a notable pivot from earlier hardline positions. His public statement that failing to return frozen assets would discourage investment in the dollar reflects a pragmatic economic argument that critics have characterised as post-hoc rationalisation.

The Israeli Dimension and Republican Fracture

Israeli officials had cited Iran's ballistic missile program as a primary justification for military action. Its exclusion from the MOU represents a notable gap from Israel's stated objectives and is likely to be a central pressure point during the 60-day follow-on talks.

The domestic Republican reaction has been unusually fractious. Senior party figures expressed reservations with notable directness:

- Senator Ted Cruz invoked historical precedent in arguing that providing financial concessions to adversarial theocratic regimes has consistently produced negative strategic outcomes

- Senator Lindsey Graham characterised the MOU as a framework for reaching a deal rather than a deal itself, expressing reservations about specific provisions while acknowledging Trump's intent

- Senator Bill Cassidy argued that the pre-war status quo — characterised by an open strait, maximum sanctions pressure, and no American casualties — was superior to the post-MOU outcome on every measurable dimension

- Former Vice President Mike Pence raised concerns about the absence of verifiable nuclear dismantlement language, noting that the MOU reiterates prior Iranian commitments without introducing new verification mechanisms

The next major ASX story will hit our subscribers first

Benchmarking the 2026 MOU Against the 2015 JCPOA

Critics from both parties have drawn comparisons to the 2015 Joint Comprehensive Plan of Action, the agreement Trump withdrew from in 2018 and repeatedly characterised as the worst deal in history. The comparative analysis is, furthermore, instructive:

| Dimension | 2015 JCPOA | 2026 MOU |

|---|---|---|

| Nuclear enrichment limits | Specific caps with IAEA verification | Deferred to 60-day talks; no new caps established |

| Sanctions relief | Phased, tied to IAEA compliance milestones | Immediate waivers on oil exports; broader relief signalled |

| Ballistic missiles | Not covered | Not covered |

| US Congressional approval | Not ratified (executive agreement) | Not ratified (MOU format) |

| Duration | 10-15 year sunset clauses | 60-day interim framework |

| Verification mechanism | IAEA inspections regime | Not yet defined |

| Financial concessions | Asset releases and sanctions relief | Asset releases, sanctions relief, and $300B development program |

The comparative framework suggests the 2026 MOU offers Iran comparable or greater financial benefits than the 2015 agreement while providing the United States with less structured nuclear verification in return, at least in its current interim form.

The 60-Day Window: What Remains Unresolved

The follow-on negotiation period will determine whether the MOU becomes the foundation for a durable agreement or collapses into a strategic retreat with lasting consequences.

Iran's stockpiles of highly enriched uranium represent the most technically sensitive proliferation concern and were explicitly deferred. The MOU contains no language requiring verifiable dismantlement of nuclear weapons infrastructure. Trump characterised the 60-day deadline as a soft target rather than a hard constraint, a framing that critics argue undermines negotiating leverage by signalling flexibility before talks begin.

Iran's ballistic missile and drone capabilities, which demonstrated continued potency during the conflict period, remain entirely outside the MOU's scope. Regional Gulf states including Saudi Arabia and the UAE will be watching subsequent talks closely, as Iranian missile reach directly affects their own security calculations.

The frozen assets question also lacks a clearly defined conditionality mechanism. The concept that assets will be released only if Iran behaves has no specified verification or enforcement architecture in the current MOU text, leaving significant interpretive flexibility for both sides.

Supply Chain and OPEC+ Implications of Iranian Oil Re-Entry

Immediate sanctions waivers on Iranian crude exports could add meaningful barrels to global supply within weeks of implementation. Iran's pre-sanctions production capacity was estimated at approximately 3.8 million barrels per day. Current capacity following conflict-related damage is likely reduced, but the directional impact on global supply balances remains material.

OPEC's influence on oil markets will be tested considerably as Iranian volumes return. Member states, particularly Saudi Arabia and the UAE, will need to recalibrate their own production strategies, creating coordination complexity that the cartel has navigated before but under very different geopolitical conditions. In addition, the trade war impact on oil markets remains a concurrent pressure weighing on the broader demand outlook as Iranian barrels re-enter the equation.

For shipping economics, the unwinding of the Cape of Good Hope rerouting premium represents a deflationary force on global freight rates. European refiners that adjusted crude sourcing away from Gulf grades during the closure will face feedstock strategy recalibration. The beneficiaries of normalisation are concentrated among Asian importers who absorbed the highest rerouting cost premiums during the conflict period.

Key Questions for Energy Market Participants

Is the Strait of Hormuz Fully Open?

Not yet. Physical implementation, including de-mining and the formal lifting of naval blockades, is still underway. Analysts estimate 40 to 50 days before the corridor returns to operational normalcy.

Does the Deal Address Iran's Nuclear Programme?

No substantive new commitments exist. Nuclear negotiations are deferred to the 60-day follow-on period with no new verification mechanisms or enrichment caps currently established. Reporting from Al Jazeera confirms that the nuclear question remains the most contested unresolved element of the broader agreement.

What Happens if Iran Does Not Comply?

Trump has publicly stated US military forces would re-engage if Iran fails to adhere to the agreement's terms. However, the enforcement framework in the MOU itself is not architecturally defined.

What Does Iranian Oil Re-Entry Mean for Crude Prices?

Full normalisation combined with sanctions relief could push Brent crude toward the $65 to $68 per barrel range in a smooth implementation scenario, representing significant further downside from current levels. This outcome would represent the most material repricing event for the US Iran peace pact and Strait of Hormuz reopening's longer-term economic legacy.

This article reflects publicly available information as of the date of publication. Energy market projections and geopolitical scenario analysis involve significant uncertainty and should not be construed as investment advice. Readers are encouraged to consult independent financial and geopolitical analysis before making decisions based on the scenarios described above.

Want to Stay Ahead of the Next Major Resource Discovery Triggered by Shifting Energy Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex market shifts — including those driven by geopolitical disruptions like Hormuz closures — into actionable investment opportunities for subscribers at every experience level. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.