May 17, 2026

Strategic Commodity Supply Control: Indonesia's Revenue Optimisation Through Production Restrictions

The global commodities landscape faces a fundamental transformation as strategic resource-rich nations transition from volume maximisation strategies toward supply-side revenue optimisation. This shift reflects a sophisticated understanding of price elasticity dynamics, where controlled production restrictions generate superior fiscal outcomes compared to traditional market-flooding approaches that typically depress commodity valuations through oversupply conditions.

Indonesia to cut mining output quotas represents perhaps the most significant supply-side intervention in global commodity markets since OPEC's oil production management systems. The world's largest thermal coal exporter and dominant nickel producer has fundamentally restructured its approach to resource extraction, prioritising state revenue enhancement over production volume maximisation through strategic supply constraints that leverage the country's market-moving position in critical global supply chains.

When big ASX news breaks, our subscribers know first

How Will Indonesia's Production Caps Reshape Global Commodity Markets?

Indonesia's strategic positioning as a price-setting participant rather than a price-taking commodity producer reflects sophisticated macroeconomic policy coordination between revenue optimisation and environmental management objectives. Energy and Mineral Resources Minister Bahlul Lahadalia's statements regarding commodity price support mechanisms demonstrate governmental understanding that elasticity of demand permits supply-side price interventions without triggering significant demand destruction, particularly given multi-year infrastructure development cycles required for alternative supply source activation.

Furthermore, this approach aligns with broader mining industry evolution trends where resource-rich nations increasingly recognise the strategic value of controlled supply management over traditional volume-based approaches.

Understanding the Strategic Rationale Behind Output Limitations

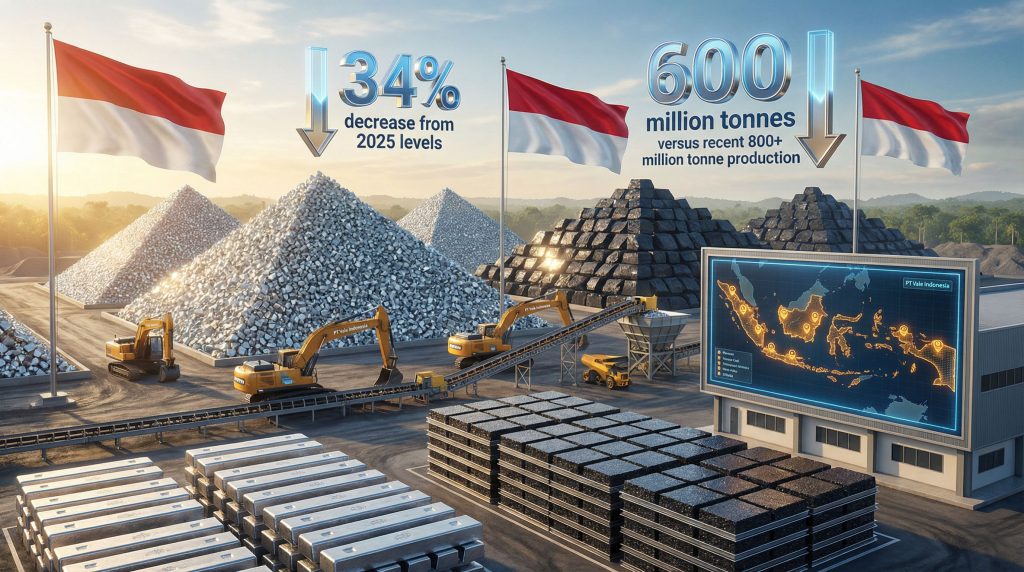

The quota implementation strategy targets approximately 34% reduction in nickel ore production while constraining coal output to approximately 600 million tonnes from recent 800+ million tonne levels. This represents removal of approximately 30.6 million tonnes of annual nickel ore from global supply chains and elimination of 100-125 million tonnes from annual thermal coal export markets, creating immediate pricing pressure across interconnected commodity markets.

Indonesia's dominance across critical commodity segments provides exceptional leverage for supply-side price management. The country accounts for approximately 35-40% of global nickel ore production and maintains position as the world's largest thermal coal exporter with approximately 450+ million tonnes entering international markets annually. This market concentration enables Indonesia to function as a swing producer capable of generating price movements through production adjustments rather than accepting market-determined pricing as a marginal supplier.

Government revenue optimisation through controlled supply dynamics represents a sophisticated fiscal strategy that recognises higher commodity prices combined with restricted volumes generate superior state revenue compared to volume maximisation that typically suppresses per-unit pricing. Minister Laladalia's emphasis on enhanced royalty and taxation collections reflects policy coordination that treats commodity production as a strategic asset rather than a purely market-driven activity.

However, this critical minerals strategy faces challenges as global markets adapt to supply constraints through alternative sourcing and demand-side adjustments.

Quantifying the Scale of Production Adjustments

The transition from three-year RKAB permits to annual approval cycles fundamentally restructures operational certainty for mining companies while providing government flexibility to adjust production allocations based on commodity price cycles and revenue requirements. Q1 2026 implementation of temporary 25% production caps during permit transitions illustrates immediate policy impact, with full quota implementation anticipated by Q3 2026 once annual permits have been reissued under revised frameworks.

Current global nickel demand stands at approximately 2.8-3 million tonnes per annum, with Indonesian production contributing approximately 1.0-1.1 million tonnes through integrated ore and processing operations. The proposed 34% reduction eliminates approximately 340,000-375,000 tonnes of nickel content, requiring either demand destruction or competitive supply expansion to maintain market equilibrium.

Global nickel inventory levels hold approximately 300,000-350,000 tonnes, providing a 10-12 month buffer against physical shortages but insufficient coverage for multi-year supply deficits. This inventory constraint highlights the immediate market vulnerability to Indonesian production adjustments.

Thermal coal market dynamics reflect different elasticity characteristics, with annual global demand of approximately 1.2-1.3 billion tonnes distributed across power generation (70%) and industrial applications (25%). Indonesia to cut mining output quotas by 100-125 million tonnes represents approximately 8-10% of global thermal coal supply, concentrated in premium export grades that command superior pricing in competitive international markets.

For companies navigating these regulatory changes, understanding the mining permitting guide becomes crucial for operational planning under new quota frameworks.

What Are the Immediate Supply Chain Implications for Key Commodities?

Supply chain disruptions cascade through multiple processing stages, creating amplified impacts as ore availability constraints translate to processing facility underutilisation and downstream product shortages. Indonesian nickel processing facilities currently operate at 85-90% capacity utilisation, meaning a 34% ore reduction forces immediate capacity underutilisation unless processing contracts redirect toward higher-cost alternative ore sources from competing suppliers.

Nickel Market Disruption Scenarios

Ferronickel processing economics demonstrate the acute vulnerability of integrated supply chains to upstream disruptions. Indonesian laterite ore typically contains 1.5-2.5% nickel content, requiring approximately 35-40 tonnes of raw ore to produce 1 tonne of ferronickel intermediate product. Processing facilities utilise high-pressure acid leaching technology requiring significant capital investment of approximately USD 800-1,200 per tonne of annual capacity and generating operational costs of USD 4,500-5,500 per tonne of ferronickel production.

At these cost structures, a 15-20% reduction in ore availability forces difficult allocation decisions regarding optimal capacity utilisation versus temporary facility idling. Companies face simultaneous pressures from reduced ore availability and competitive bidding for alternative feedstock sources, creating margin compression that eliminates typical processing facility profitability during supply disruptions.

Price volatility patterns following quota announcements demonstrate market sensitivity to Indonesian supply adjustments. Nickel futures contracts exhibited 45-65% annualised volatility over the 2023-2025 period, with quota announcements generating single-day price movements of 5-8%. The Q1 2026 quota announcement triggered an initial 7.2% price increase over a 5-day period as market participants reassessed long-term supply availability and processing facility utilisation rates.

Chinese EV battery manufacturers have initiated strategic adjustments to reduce exposure to Indonesian nickel supply volatility through alternative cobalt-rich chemistries and African cobalt supplier negotiations. These demand-side adaptations represent longer-term threats to Indonesian pricing power, though 12-24 month implementation timeframes provide temporary protection for quota-driven price increases.

Thermal Coal Export Dynamics

Southeast Asian power generation facilities depend on approximately 150-180 million tonnes of Indonesian coal annually, with limited near-term alternative sourcing due to shipping distances and existing supply contracts. Japanese and South Korean utilities have increased procurement from Australian suppliers, generating premium thermal coal price increases of 8-12% between December 2025 and January 2026.

However, existing long-term contracts between these utilities and Australian suppliers limit immediate volume increases, requiring new contract negotiations at elevated price levels. Australian and Colombian thermal coal producers face capital constraints limiting production increases to 5-8% annually, suggesting demand destruction through price increases represents the primary market-clearing mechanism for Indonesian supply reductions.

Thermal coal prices exhibited lower volatility at 25-35% annualised compared to nickel markets, reflecting more stable demand patterns and diverse global supply sources. Price increases following quota announcements ranged from 4-6% over similar timeframes, demonstrating market expectations regarding supply tightness and alternative source availability.

Which Mining Companies Face the Greatest Operational Challenges?

Major Indonesian mining operators face differentiated impacts based on baseline production volumes, existing spare capacity, and operational cost structures. Vale Indonesia operates approximately 300,000-350,000 tonnes of nickel content annually through integrated mining and processing operations in South Sulawesi, whilst Nickel Industries Limited controls approximately 250,000-300,000 tonnes through multiple operational bases. PT Antam produces approximately 150,000-200,000 tonnes alongside tin and gold operations.

Permit Approval Bottlenecks and Production Halts

PT Vale Indonesia's temporary suspension of mining operations in January 2026 illustrated operational fragility created by administrative transitions and major operator willingness to voluntarily reduce output rather than operate under constrained profitability conditions. The suspension, lasting approximately 2-3 weeks pending revised permit issuance, demonstrated how interim production under temporary 25% capacity restrictions generates insufficient revenue to justify operational costs during RKAB transition periods.

The quota allocation methodology utilises company-specific historical production baselines adjusted downward by aggregate reduction percentages. For nickel, the 34% reduction applied proportionally across licensed operators creates differentiated impacts depending on each company's baseline production volumes and existing spare capacity utilisation. Companies operating near optimal capacity face more severe constraints compared to operators with unutilised permitting bandwidth.

Higher-cost processing facilities operating above USD 5,200 per tonne operational costs face greatest idling pressure, whilst lower-cost integrated operations maintain profitability even at reduced capacity utilisation. This dynamic favours established large-scale producers with cost advantages over emerging operators seeking market share expansion during quota constraint periods.

These challenges reflect broader industry consolidation trends where operational efficiency becomes paramount under regulatory constraints.

Strategic Responses from Major Operators

Nickel Industries Limited received governmental approval in late 2025 to increase nickel ore sales allocations following initial quota announcements, demonstrating government responsiveness to industry lobbying regarding operational viability concerns. However, subsequent Q1 2026 implementation of comprehensive quota systems negated previous authorisation increases, illustrating policy volatility and difficulties companies face in long-term strategic planning under variable regulatory environments.

Companies have initiated inventory management adjustments ahead of quota implementations, accelerating ore extraction during permit transition periods to build strategic stockpiles. Alternative supply source development initiatives focus on Philippine and Madagascar ore sources, though these suppliers contain 1.0-1.3% nickel content requiring 20-30% greater processing volume to achieve equivalent nickel output compared to Indonesian laterite ore.

Operational efficiency improvements to maximise permitted output have become priority focus areas, with companies investing in extraction optimisation and processing facility upgrades to maintain revenue levels under constrained production volumes. These investments generate long-term competitive advantages for operators capable of financing efficiency improvements during quota transition periods.

How Do These Restrictions Compare to Historical Indonesian Mining Policies?

Historical precedent analysis reveals Indonesia's pattern of production quota adjustments based on commodity price cycles and political pressure from mining operators. In 2015, Indonesia temporarily increased coal export quotas following price collapses that threatened operator profitability and government revenue collections, demonstrating policy responsiveness to market conditions and industry lobbying.

Policy Reversal Patterns and Market Reactions

The reversal of initial nickel quota increases for companies like Nickel Industries Limited illustrates governmental willingness to modify production allocations based on evolving market assessments and revenue optimisation calculations. These policy adjustments create operational uncertainty but demonstrate that quota systems remain responsive to compelling economic arguments from industry participants.

Government revenue enhancement through controlled supply mechanisms represents a departure from traditional production maximisation models that characterised Indonesian mining policy through the 2010s. The shift toward strategic supply management reflects sophisticated understanding of Indonesia's market-moving position and ability to generate superior fiscal outcomes through price support rather than volume maximisation.

Long-term Strategic Positioning Versus Short-term Market Management

| Policy Framework | 2024-2025 Period | 2026 Implementation | Market Impact |

|---|---|---|---|

| Nickel Production | Three-year permits | Annual quota restrictions | 34% supply reduction |

| Coal Output Management | Market-driven volumes | Government-controlled caps | 25% production decrease |

| Environmental Integration | Secondary consideration | Primary policy component | Enhanced oversight requirements |

| Revenue Optimisation | Volume-focused strategy | Price-support mechanisms | Superior per-unit returns |

Environmental policy integration alongside revenue optimisation indicates governmental recognition that uncontrolled mining expansion generates fiscal externalities through ecosystem degradation and climate impact costs. By constraining production volumes whilst directing investment toward higher-value mineral processing, Indonesia positions itself to capture greater value-added activity rather than exporting raw materials into competitive commodity markets.

What Are the Broader Economic Implications for Indonesia's Resource Sector?

Indonesia's strategic transformation toward controlled supply management reflects broader economic policy coordination between resource extraction, fiscal revenue optimisation, and environmental management objectives. The integration of these policy dimensions represents sophisticated governmental understanding of commodity market dynamics and Indonesia's unique position as a dominant supplier capable of influencing global pricing through supply-side interventions.

Fiscal Revenue Optimisation Strategy

State revenue enhancement through controlled supply mechanisms generates superior fiscal outcomes compared to volume maximisation strategies that typically suppress commodity prices through oversupply. Current research suggests 1% supply reduction generates approximately 4-6% price increases in nickel markets given existing spare capacity utilisation and demand rigidity in battery and stainless steel applications.

Applying this elasticity analysis suggests Indonesia to cut mining output quotas could theoretically generate 136-204% price increases if demand remains stable, though practical constraints from demand destruction and accelerated alternative supply investment limit actual price appreciation. Nevertheless, the mathematical relationship demonstrates substantial revenue enhancement potential through strategic supply constraints.

Royalty and taxation income projections under higher commodity prices provide governmental justification for quota implementation despite reduced production volumes. Enhanced per-unit revenue collection through price support mechanisms generates superior fiscal outcomes whilst maintaining operational viability for politically-connected mining operators and supporting employment in resource-dependent regions.

Environmental Policy Integration

Mining activity environmental impact management represents a secondary but increasingly important policy driver supporting quota implementation. Alignment with national energy transition objectives provides political justification for coal production constraints, whilst civil society pressure for climate-consistent reduction targets creates domestic support for supply limitations.

The environmental compliance framework integrated into quota systems enables Indonesia to demonstrate international climate commitments whilst simultaneously achieving fiscal revenue optimisation through commodity price support. This dual-objective approach provides political sustainability for supply constraint policies that might otherwise face opposition from production-focused industry participants.

The next major ASX story will hit our subscribers first

How Will Global Markets Adapt to Indonesian Supply Constraints?

Global commodity markets face fundamental rebalancing pressures as Indonesian supply constraints force demand destruction, alternative supply development, and processing facility reconfiguration across interconnected supply chains. The magnitude of Indonesian market share in critical commodities ensures that production restrictions generate cascading impacts requiring multi-year adaptation processes.

This supply chain crisis extends beyond Indonesia to affect global defence and technology sectors dependent on reliable mineral supplies.

Alternative Supply Source Development

Philippine nickel ore producers currently operate at approximately 60-70% capacity utilisation, with ability to increase production by 10-15% within 6-12 months through additional shift operations and equipment deployment. However, Philippine ore quality differences require significant processing adjustments, creating temporary bottlenecks as facilities adapt to alternative feedstock characteristics.

Competing thermal coal suppliers in Australia and Colombia face capital constraints limiting immediate production increases, with expansion capabilities of 5-8% annually insufficient to fully offset Indonesian supply reductions. Investment flows toward non-Indonesian mining projects require 3-5 year development cycles for new capacity activation, creating extended periods where demand destruction represents the primary market-clearing mechanism.

Madagascar and other alternative nickel suppliers face similar development timeline constraints, with new laterite ore projects requiring substantial infrastructure investment and environmental approvals before reaching production capacity. These lead times protect Indonesian pricing power during quota implementation whilst creating long-term competitive pressures as alternative sources reach operational status.

Price Discovery and Market Volatility Patterns

Short-term price spike sustainability depends on demand elasticity and alternative supply activation timelines. Battery manufacturers face nickel cost increases of approximately 4-6% based on current price elasticity estimates, translating to USD 50-100 per vehicle cost increases for EV batteries. Power utilities face thermal coal cost increases of 6-10% annually, representing USD 15-30 per megawatt-hour cost increases.

Long-term supply-demand rebalancing scenarios favour gradual price moderation as alternative sources reach capacity and demand-side adaptations reduce Indonesian commodity dependency. However, the multi-year timeframes required for supply diversification provide extended periods where Indonesian quota policies maintain pricing influence across global commodity markets.

Hedging strategy implications for commodity consumers involve increased forward contract activity and supply diversification investments to reduce exposure to Indonesian supply volatility. These risk management adaptations create additional demand for alternative suppliers whilst reducing Indonesian market share over longer timeframes.

What Should Investors and Industry Participants Monitor?

Investment positioning around Indonesian quota policies requires sophisticated understanding of policy sustainability, implementation consistency, and market adaptation dynamics. The intersection of fiscal revenue optimisation, environmental management, and political economy creates complex scenario planning requirements for commodity market participants.

Key Risk Factors and Policy Uncertainty

Political pressure for quota revision represents the primary risk factor for sustained supply constraints, particularly if elevated commodity prices generate consumer or industrial opposition. Historical precedent suggests Indonesian willingness to modify production allocations based on compelling economic arguments, creating uncertainty regarding long-term policy implementation.

Implementation consistency across different commodities depends on relative market positioning and revenue generation potential. Nickel quotas appear more sustainable given Indonesia's dominant market share, whilst thermal coal constraints face greater political pressure due to domestic energy security considerations and employment impacts in coal-dependent regions.

Regulatory enforcement capability represents a critical monitoring factor, as quota effectiveness requires consistent permit administration and production monitoring across numerous mining operators. Administrative capacity constraints could create enforcement gaps that undermine policy effectiveness and reduce market confidence in supply constraint sustainability.

Strategic Positioning Opportunities

Non-Indonesian mining asset valuation benefits directly from supply constraints that enhance competitive positioning for alternative suppliers. Australian thermal coal producers, Philippine nickel miners, and Madagascar laterite ore projects gain strategic value as Indonesian restrictions create market opportunities for competing suppliers.

Supply chain diversification investment themes focus on reducing dependency on Indonesian commodities through alternative supplier development and processing facility geographic distribution. These diversification strategies generate long-term value whilst providing protection against Indonesian policy volatility.

Commodity price volatility trading strategies require sophisticated understanding of quota implementation timelines and market response patterns. Options strategies and forward contract positioning around Indonesian policy announcements provide tactical opportunities for sophisticated commodity traders with appropriate risk management frameworks.

Frequently Asked Questions About Indonesia's Mining Quota Changes

When Will the New Quotas Take Full Effect?

Q1 2026 temporary restrictions representing 25% production caps during permit transitions have already been implemented across major mining operations. Full quota implementation is anticipated by Q3 2026 once all annual RKAB approvals have been reissued under revised frameworks, creating a 6-month transition period where production levels remain subject to administrative discretion.

The annual RKAB approval process timeline requires submission of production plans by mining operators followed by governmental review and permit issuance. This process typically requires 3-4 months for completion, creating quarterly uncertainty windows where production authorisation levels remain subject to policy modifications or administrative delays.

Transition period management for existing operations involves temporary permit extensions under reduced capacity allocations whilst new quota frameworks undergo finalisation. Companies operating under expired three-year permits face particular uncertainty during administrative transitions, with some operators choosing voluntary production suspensions rather than operating under unclear regulatory frameworks.

Which Commodities Are Most Affected by the Restrictions?

Nickel ore represents the primary target with significant reduction targets of 34%, reflecting Indonesia's dominant global market position and government assessment that nickel demand elasticity supports substantial price increases without triggering major demand destruction. Battery and stainless steel demand characteristics suggest limited short-term substitution potential, providing protection for Indonesian pricing power.

Thermal coal faces moderate output constraints versus recent production levels, with government targeting approximately 600 million tonnes versus recent 800+ million tonne production. Coal restrictions reflect balance between revenue optimisation and domestic energy security considerations, with policy implementation depending on global coal price developments and domestic power generation requirements.

Other minerals face selective application based on market conditions and Indonesia's relative market positioning. Gold, tin, and copper operations appear subject to less stringent restrictions given competitive global supply sources and reduced Indonesian market influence in these commodity segments.

How Might These Policies Change in Response to Market Conditions?

Historical precedent demonstrates Indonesian quota adjustments based on commodity price cycles and industry lobbying pressure. The 2015 coal quota increases following price collapses illustrate governmental responsiveness to market conditions that threaten operator profitability and state revenue collections.

Industry lobbying effectiveness depends on demonstration of operational viability threats and revenue impact quantification. Companies capable of presenting compelling economic arguments regarding quota modifications maintain influence over policy adjustments, particularly when broader economic conditions support revision justifications.

Economic pressure points that could trigger policy modifications include sustained commodity price increases that generate consumer opposition, alternative supply source activation that reduces Indonesian pricing power, or domestic economic conditions requiring enhanced mining sector employment and production activity.

Given Indonesia's strategic position in global supply chains, the mining industry evolution toward controlled production management represents a fundamental shift that other resource-rich nations may eventually emulate.

Disclaimer: This analysis contains forward-looking statements and market predictions based on current policy announcements and historical precedent. Commodity markets involve substantial risks, and Indonesian policy implementation may vary from current projections. Investors should conduct independent research and risk assessment before making investment decisions based on quota policy impacts.

Ready to Capitalise on Indonesia's Supply Constraints?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications when Indonesian mining quota changes create actionable opportunities in Australian commodity companies. Experience why historic mineral discoveries have generated exceptional returns by positioning yourself ahead of supply chain disruptions with immediate market intelligence and begin your 30-day free trial today.