May 14, 2026

Strategic Energy Policy Tensions Shape Market Dynamics

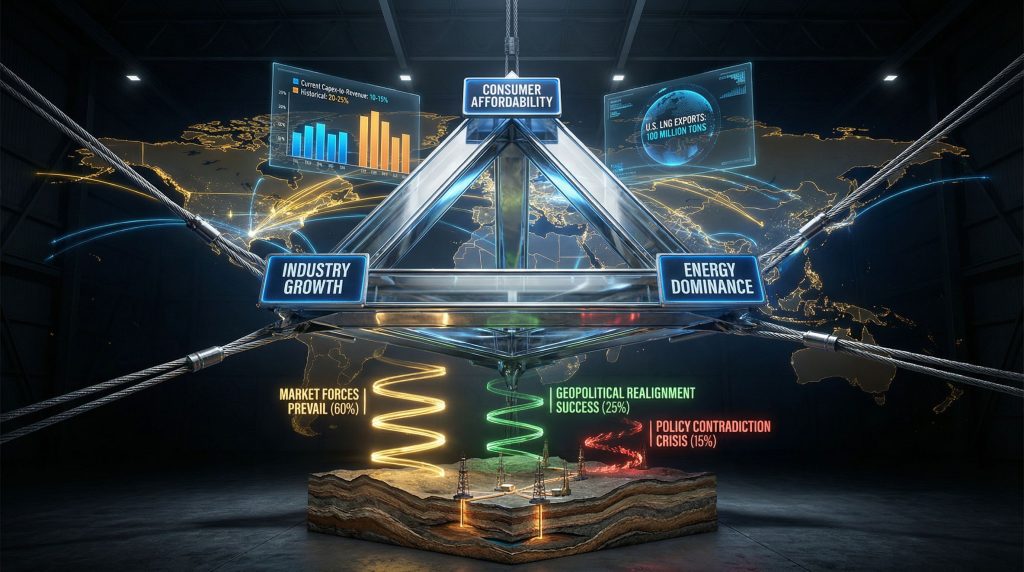

Complex energy policy frameworks often create strategic tensions between competing objectives, revealing fundamental contradictions in national energy approaches. Trump's energy agenda exemplifies these challenges, as policies attempt to simultaneously optimize for consumer affordability, industry profitability, and global market positioning. The intersection of these goals creates a multifaceted optimization challenge that demonstrates how political priorities can conflict with market realities.

Understanding these strategic frameworks requires examining how policy objectives interact with fundamental market forces. Capital allocation decisions, regulatory environments, and global competitive dynamics all influence outcomes in ways that may not align with initial policy intentions. This creates scenarios where achieving one strategic objective may undermine progress toward others.

When big ASX news breaks, our subscribers know first

The Complex Relationship Between Energy Costs and Market Dominance

Energy policy frameworks must navigate the fundamental tension between maintaining affordable domestic energy costs while building global market influence. Lower commodity prices benefit consumers and can stimulate demand growth, but they simultaneously pressure producer margins and reduce incentives for capital investment. Furthermore, understanding oil market dynamics becomes crucial when examining how price fluctuations affect strategic policy objectives.

Market Structure Implications

The relationship between domestic energy costs and global market positioning involves several key dynamics:

- Price elasticity effects: Lower domestic prices can increase consumption but may reduce export competitiveness

- Investment cycle impacts: Sustained low prices discourage upstream capital expenditure

- Technology development: Reduced cash flows limit innovation funding

- Infrastructure development: Lower revenues slow pipeline and processing capacity expansion

These dynamics demonstrate how energy affordability goals can inadvertently undermine the very industry capacity needed to achieve market dominance objectives.

Producer Response to Political Support Versus Market Signals

The evolution of capital discipline in the energy sector represents a fundamental shift in how companies respond to policy signals versus market fundamentals. Despite unprecedented federal support and regulatory streamlining, producers continue prioritising financial discipline over production maximisation. This strategic evolution reflects lessons learned from previous boom-bust cycles and demonstrates the durability of new operational philosophies.

Capital Allocation Strategy Transformation

Modern energy companies have restructured their capital allocation approaches based on several key principles:

Financial Discipline Metrics:

- Maintaining capex-to-revenue ratios below historical averages

- Prioritising free cash flow generation over volume growth

- Emphasising shareholder returns through dividends and buybacks

- Building balance sheet resilience for market volatility

Risk Management Evolution:

- Longer-term planning horizons that account for policy uncertainty

- Technology-driven efficiency improvements reducing drilling requirements

- Portfolio optimisation focusing on highest-return assets

- Hedging strategies to manage commodity price exposure

This transformation indicates that industry responses to policy support may be more muted than historically anticipated, as companies prioritise sustainable business models over rapid production expansion.

Global Competition Dynamics in Energy Markets

Liquefied Natural Gas Market Vulnerabilities

The U.S. achieved significant LNG export growth, surpassing 100 million tons annually, but this success created strategic dependencies that complicate market positioning. European markets absorb approximately half of U.S. LNG exports, creating mutual vulnerability that extends beyond simple buyer-seller relationships. Additionally, examining natural gas forecasts provides insights into future market positioning challenges.

Critical Dependency Factors:

| Risk Category | Impact Level | Mitigation Options |

|---|---|---|

| Geographic Concentration | High | Market diversification |

| Regulatory Changes | Medium | Technology adaptation |

| Demand Volatility | High | Flexible contracting |

| Infrastructure Limits | Medium | Capacity investment |

The European Union's methane regulations exemplify how regulatory frameworks can disrupt established trade relationships. These regulations potentially affect Gulf Coast LNG competitiveness by increasing compliance costs and operational complexity.

Crude Oil Market Competition Intensity

Unlike LNG's regional market characteristics, crude oil operates in a truly global market where pricing power requires substantial market share and coordination. U.S. production leadership does not automatically translate to pricing influence due to several competitive factors, including the broader trade war market impact on global energy flows.

OPEC+ Strategic Responses:

- Maintenance of significant spare production capacity

- Coordinated production adjustments to influence global supply

- Long-term contracts with Asian buyers reducing spot market exposure

- Strategic petroleum reserve management

Non-OPEC Competitive Pressure:

- Brazilian pre-salt field development continuing to ramp production

- Guyana's offshore discoveries adding substantial new supply

- Canadian oil sands maintaining steady output despite cost challenges

- Norwegian shelf production optimisation extending field life

These competitive dynamics limit U.S. influence over global crude oil pricing despite production volume leadership. However, OPEC market influence continues to shape global pricing mechanisms significantly.

Geopolitical Energy Interventions and Market Repositioning

Venezuela Strategy: Multi-Objective Market Intervention

The approach to Venezuelan energy sector intervention represents strategic market repositioning rather than purely humanitarian objectives. This intervention targets multiple strategic goals simultaneously, demonstrating how geopolitical actions can serve economic and security interests under Trump's energy agenda.

Strategic Benefits Analysis:

Supply Chain Security:

- Diversification of heavy crude sources for U.S. refineries

- Reduced Western Hemisphere dependence on Middle Eastern imports

- Enhanced energy security through regional supply integration

Geopolitical Leverage:

- Pressure mechanisms for reducing Russian energy trade

- Strengthened U.S. influence in Latin American energy markets

- Demonstration effects for sanctions enforcement capabilities

The complexity of Venezuelan oil sector rehabilitation presents significant challenges. Infrastructure degradation, technical expertise gaps, and institutional corruption require substantial investment and time to address effectively. For instance, recent Saudi exploration licenses demonstrate how rapidly new production capacity can emerge globally.

India's Crude Sourcing Evolution

India's transition from Russian to alternative crude sources illustrates how economic diplomacy translates into market share gains. This shift demonstrates the effectiveness of coordinated pressure campaigns but also highlights the importance of sustained price competitiveness for maintaining market positions.

Transition Metrics and Implications:

- Russian crude import share declining from peak levels above 40%

- U.S. crude imports increasing substantially year-over-year

- Middle Eastern suppliers competing for displaced Russian volumes

- Long-term contract renegotiations reflecting new supply preferences

The sustainability of these supply chain shifts depends on maintaining price advantages and avoiding supply disruption risks that could encourage buyers to diversify further.

Technology Innovation and Regulatory Framework Tensions

The simultaneous promotion of certain energy technologies while constraining others creates asymmetric development patterns with long-term strategic implications. Nuclear energy advancement receives regulatory streamlining while renewable energy faces reduced investment incentives, creating technological development imbalances within Trump's energy agenda.

Innovation Paradox Dynamics

Accelerated Nuclear Development:

- Streamlined regulatory approval processes

- Enhanced federal funding for advanced reactor designs

- Public-private partnership models for demonstration projects

- Reduced permitting timelines for new facility construction

Renewable Energy Investment Impacts:

- Reduced federal incentives affecting deployment economics

- Slower cost curve improvements due to decreased investment

- Technology development shifts toward private sector funding

- International competitiveness concerns in emerging markets

The emergence of artificial intelligence data centres as major electricity consumers may force technology-neutral approaches to power generation. Consequently, this could resolve some development asymmetries through market demand rather than policy direction. The White House's energy policy framework outlines specific approaches to addressing these challenges.

The next major ASX story will hit our subscribers first

Long-Term Structural Market Implications

Energy Security Versus Market Efficiency Trade-offs

Policy frameworks that prioritise energy security over pure market efficiency create potential long-term market distortions. These distortions manifest through various mechanisms that alter competitive dynamics and resource allocation patterns.

Policy-Induced Market Modifications:

Domestic Production Advantages:

- Regulatory fast-tracking reduces compliance costs for domestic producers

- Tax policy modifications favour domestic over imported energy sources

- Infrastructure development prioritisation benefits national producers

- Strategic petroleum reserve policies influence market dynamics

International Trade Impact Mechanisms:

- Sanctions enforcement increases operational costs for competitor nations

- Bilateral pressure campaigns create artificial market preferences

- Currency policy coordination affects energy trade competitiveness

- Trade agreement negotiations incorporate energy supply commitments

These modifications demonstrate how security-focused policies can reshape market structures in ways that persist beyond immediate political objectives. Furthermore, research on energy policy contradictions reveals how competing objectives create market uncertainties.

Strategic Scenario Analysis: Future Pathway Assessment

Market Forces Dominance Scenario

Under this scenario, fundamental supply-demand dynamics override political interventions, leading to market-driven outcomes. Producer capital discipline continues despite government encouragement, global oil pricing remains determined by traditional market forces, and LNG market evolution follows infrastructure and contract economics rather than political preferences.

This outcome reflects the resilience of market mechanisms and the limits of political influence over complex global commodity markets. The probability of this scenario reflects the historical tendency of energy markets to revert to fundamental economic drivers over extended time periods.

Successful Geopolitical Realignment Scenario

Strategic interventions successfully reshape global energy trade patterns in this pathway. Venezuelan oil integration provides sustained heavy crude supply alternatives, Asian buyers permanently reduce Russian energy dependence, and the U.S. achieves genuine pricing influence in key regional markets.

Success under this scenario requires sustained political coordination, significant infrastructure investment, and maintenance of price competitiveness across multiple market cycles. The lower probability reflects the complexity of maintaining coordinated international pressure while managing domestic economic priorities.

Policy Contradiction Crisis Scenario

Competing objectives create policy paralysis and market confusion in this outcome. Industry uncertainty reduces investment despite supportive rhetoric, consumer energy costs rise due to supply disruptions, and international partners accelerate efforts to diversify away from U.S. energy dependence.

This scenario emerges when the tensions between affordability, industry support, and market dominance objectives become irreconcilable, leading to policy gridlock and market instability under Trump's energy agenda.

Investment and Strategic Positioning Implications

Corporate Strategic Recommendations

Energy companies operating in this environment should maintain capital discipline regardless of political encouragement, recognising that market fundamentals ultimately drive long-term profitability. Geographic diversification reduces concentration risk from policy changes, while investment in technologies that benefit from regulatory streamlining can provide competitive advantages.

Risk Management Priorities:

- Flexible capital allocation frameworks that respond to market signals

- Technology investments aligned with regulatory development trends

- Portfolio diversification across geographic and product markets

- Financial hedging strategies to manage policy uncertainty impacts

Consumer and Industrial Strategy Considerations

Energy consumers should expect continued price volatility as policies compete with market forces. Planning for potential supply disruptions during geopolitical transitions requires robust risk management frameworks and alternative supply arrangements.

Energy efficiency investments provide protection against policy-driven price swings while supporting long-term cost competitiveness. Industrial users particularly benefit from demand flexibility that allows optimisation across different energy sources and timing patterns.

International Partnership Development

International energy partners should develop alternative supply sources to reduce dependency concentration while negotiating flexible contract terms that accommodate policy changes. Strategic reserve development provides buffer capacity against supply disruption risks.

Building relationships across multiple supplier nations creates negotiating leverage and reduces vulnerability to bilateral political tensions. Long-term energy security requires balancing cost optimisation with supply chain resilience considerations.

Market Psychology and Investor Behavior Dynamics

The interaction between policy announcements and market responses reveals important insights about investor psychology in energy markets. Despite supportive political rhetoric, equity markets for energy companies have shown mixed responses, reflecting investor scepticism about the sustainability of policy benefits versus underlying market challenges.

Investor Sentiment Indicators:

- Energy sector relative performance versus broader market indices

- Capital allocation preferences between growth and return of capital

- Valuation multiples reflecting long-term uncertainty discounts

- Merger and acquisition activity patterns indicating consolidation trends

These behavioural patterns suggest that experienced energy investors prioritise fundamental business metrics over political support when making long-term investment decisions. However, the complex dynamics show how political frameworks continue to influence market sentiment significantly.

Disclaimer: This analysis involves forward-looking statements and scenario projections that are inherently uncertain. Energy market dynamics, geopolitical developments, and policy implementations may differ significantly from the scenarios presented. Readers should conduct independent analysis and consult qualified professionals before making investment or business decisions based on this information.

Looking to Capitalise on Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities whilst energy policy tensions create market uncertainty. Explore historic discovery returns to understand why major mineral discoveries can generate substantial market advantages, then begin your 30-day free trial today to secure your competitive edge.