June 26, 2026

Strategic Framework Evolution in U.S. Critical Minerals Policy

American industrial policy has entered a transformative phase where government intervention in strategic sectors reflects broader geopolitical realignments. The intersection of national security imperatives with domestic manufacturing capabilities creates unprecedented opportunities for public-private partnerships in resource extraction and processing industries.

This shift represents more than traditional market dynamics, signaling a fundamental recalibration of how federal resources engage with private capital to achieve strategic independence. Investment frameworks combining equity participation with debt financing mechanisms demonstrate sophisticated risk-sharing approaches that could reshape entire industrial sectors.

The emergence of hybrid financing structures bridges traditional venture capital models with government-backed development programmes, creating new pathways for domestic resource development that prioritise both commercial viability and national security objectives.

When big ASX news breaks, our subscribers know first

Federal Equity Participation in Critical Minerals Development

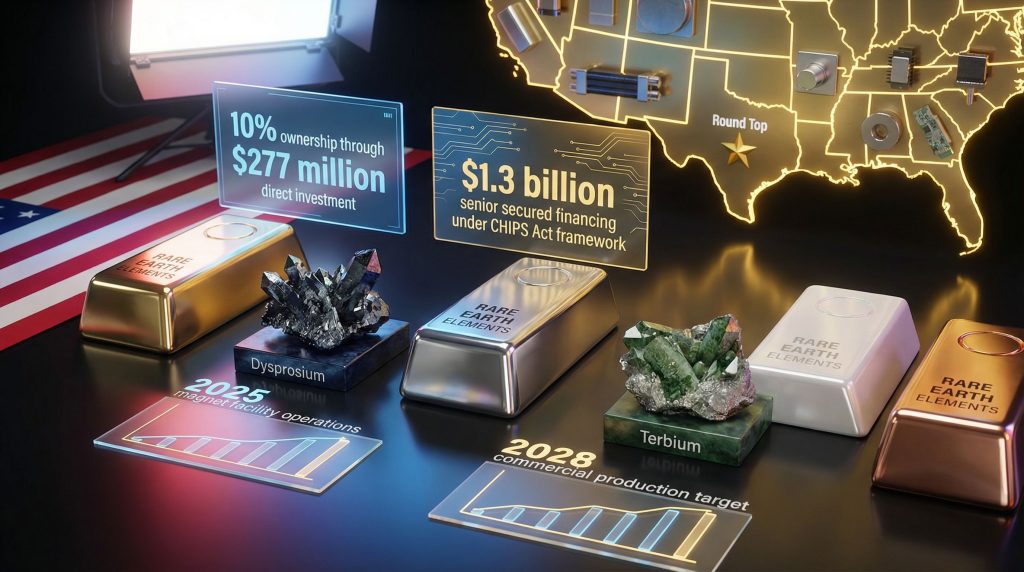

The Trump administration investment in USA Rare Earth establishes a precedent through its comprehensive $1.6 billion financing structure that combines multiple investment vehicles. The federal government's 10% equity stake, acquired through a $277 million direct investment, represents strategic minority participation rather than operational control.

Furthermore, this approach aligns with the broader Trump critical minerals order that emphasises domestic resource security. The multi-layered strategy provides the government with upside participation through warrant structures whilst maintaining private sector leadership in operational decisions.

Investment Structure Breakdown:

- Direct equity acquisition: $277 million for 16.1 million shares at $17.17 per share

- Warrant positioning: 17.6 million additional shares with $17.17 strike price

- Senior secured debt: $1.3 billion facility under CHIPS Act framework

- Private institutional investment: $1 billion PIPE arrangement

The warrant component offers potential returns exceeding $300 million based on current market valuations, creating taxpayer value alignment with project success. Additionally, this structure reflects the evolving critical minerals strategy that prioritises comprehensive supply chain development.

The Department of Commerce's involvement through CHIPS Act financing demonstrates how existing legislative frameworks can support critical minerals development beyond their original semiconductor-focused mandates. This flexibility indicates broader applications for government-backed industrial development programmes.

Comparative Analysis of Strategic Mining Investments

The Trump administration's portfolio approach to critical minerals investment reveals escalating federal commitment across multiple resource categories. Each investment targets specific supply chain vulnerabilities whilst building comprehensive domestic capabilities.

| Investment Target | Sector Focus | Strategic Value | Timeline Impact |

|---|---|---|---|

| MP Materials | Light rare earth processing | Existing production capacity | Immediate supply availability |

| Lithium Americas | Battery metal extraction | Electric vehicle supply chain | Medium-term capacity building |

| Trilogy Metals | Copper-zinc diversification | Base metals independence | Long-term mining development |

| USA Rare Earth | Heavy rare earth integration | Advanced manufacturing capability | Comprehensive vertical integration |

The USA Rare Earth investment represents the most comprehensive approach, combining mining development with downstream processing capabilities. This vertical integration strategy addresses multiple supply chain vulnerabilities simultaneously, from raw material extraction through finished magnet production.

Previous investments focused primarily on equity stakes in existing operations, whilst the current structure incorporates debt financing for infrastructure development. This evolution suggests increasing government willingness to support capital-intensive development projects requiring extended timelines for commercial production.

Consequently, the mining industry evolution reflects these changing investment patterns that emphasise strategic over purely commercial considerations.

Heavy Rare Earth Elements and National Security Implications

Heavy rare earth elements, particularly dysprosium and terbium, represent critical vulnerabilities in U.S. defence and technology supply chains. China's dominance in processing these materials creates strategic dependencies that extend beyond commercial considerations into national security planning.

Critical Applications and Dependencies:

- Defence systems: Precision-guided munitions requiring temperature-stable magnets

- Radar technology: High-performance electronics for military surveillance

- Electric vehicle motors: Permanent magnets for transportation electrification

- Wind turbine generators: Renewable energy infrastructure components

The Round Top deposit in Texas contains unique geological compositions with higher concentrations of heavy rare earths compared to most global sources. This geological advantage provides potential cost competitiveness against Chinese processing operations that rely on lower-grade feedstock requiring more intensive separation processes.

Moreover, this development occurs amid broader US-China trade impacts that have highlighted supply chain vulnerabilities in strategic materials. USA Rare Earth's mine-to-magnet integration strategy addresses the most significant supply chain gap in U.S. capabilities.

Whilst domestic light rare earth production exists through MP Materials' Mountain Pass facility, heavy rare earth processing remains almost entirely dependent on Chinese facilities. The 2028 production timeline for Round Top mining operations aligns with projected increases in heavy rare earth demand driven by electric vehicle adoption and renewable energy infrastructure development.

Market analysts project global heavy rare earth demand increasing by 300% through 2035, creating substantial market opportunities for new production sources.

Manufacturing Integration Through Stillwater Magnet Operations

The Stillwater, Oklahoma magnet manufacturing facility represents the downstream component of USA Rare Earth's vertical integration strategy. Expected to begin operations in 2025, this facility will provide domestic magnet production capabilities currently absent from U.S. supply chains.

Manufacturing Capabilities and Timeline:

- Initial production: 2025 launch using imported rare earth feedstock

- Integrated operations: 2028 transition to domestic Round Top materials

- Production capacity: Targeting automotive and renewable energy markets

- Technology transfer: Reducing dependence on Chinese magnet imports

The facility's early operation using imported materials provides immediate revenue generation whilst Round Top development proceeds. This staged approach reduces project risk by establishing market relationships and manufacturing expertise before mine production begins.

Furthermore, magnet manufacturing represents the highest value-added component of the rare earth supply chain, with profit margins significantly exceeding raw material extraction. Domestic magnet production could generate economic multiplier effects through supporting industries and high-skilled manufacturing employment.

The geographic positioning in Oklahoma provides transportation advantages for serving both automotive manufacturing in the Midwest and renewable energy installations across the central United States. This logistical efficiency could provide cost advantages over imported magnets facing increasing transportation costs and potential trade restrictions.

Financial Engineering and Valuation Mechanisms

The deal structure demonstrates sophisticated financial engineering that balances government risk mitigation with private capital leverage. The $17.17 share price reflects recent trading ranges whilst providing the government with immediate market-based valuation metrics.

Valuation and Returns Analysis:

- Share price basis: $17.17 represents fair market value at announcement

- Government investment: $277 million for 10% equity stake

- Warrant upside: Additional 17.6 million shares for expansion participation

- Current market response: 50% stock price increase following announcement

The warrant structure provides the government with participation in company growth whilst limiting downside exposure to the initial equity investment. This asymmetric risk profile aligns with public sector investment objectives that prioritise strategic outcomes alongside financial returns.

Cantor Fitzgerald's involvement as financial advisor brings specialised expertise in SPAC structures and institutional fundraising. The firm's connections to government officials through Commerce Secretary Howard Lutnick's family relationships demonstrate the intersection of private sector expertise with public sector objectives.

The $1 billion private investment component validates the commercial viability of the project beyond government backing. Institutional investors' willingness to commit substantial capital suggests confidence in both the technical feasibility and market demand for domestic rare earth production.

In addition, this development follows similar patterns seen in the US EXIM loan for antimony projects, demonstrating consistent government support for strategic minerals.

The next major ASX story will hit our subscribers first

Addressing China's Rare Earth Market Dominance

China's control over 85% of global rare earth processing capacity creates systemic vulnerabilities for U.S. industries dependent on these materials. Historical Chinese export restrictions and pricing manipulation demonstrate how resource concentration can be leveraged for geopolitical objectives.

Chinese Competitive Advantages:

- Processing infrastructure: Decades of investment in separation and refining facilities

- Cost structure: Environmental externalities and labour cost advantages

- Market manipulation capabilities: Export quotas and pricing controls

- Technology barriers: Proprietary processing techniques and equipment

The U.S. domestic production strategy faces significant cost disadvantages due to environmental regulations and higher labour costs. However, supply chain security considerations and potential Chinese export restrictions create economic justification for higher-cost domestic production.

Recent Chinese policy statements regarding rare earth export controls indicate increasing willingness to use resource dominance for strategic leverage. This trend strengthens the economic case for domestic alternatives despite higher production costs.

The Biden administration's continuation and expansion of rare earth investment programmes demonstrates bipartisan recognition of supply chain vulnerabilities. This political consensus provides long-term policy stability essential for capital-intensive mining investments with extended development timelines.

Production Timeline Challenges and Market Dynamics

The development timeline for domestic rare earth capabilities faces significant technical and regulatory hurdles. Round Top's 2028 production target requires successful completion of environmental permitting, infrastructure development, and processing facility construction.

Critical Timeline Milestones:

- 2025: Stillwater magnet facility operational launch

- 2026-2027: Round Top mine construction and permitting completion

- 2028: Commercial production commencement

- 2030+: Full-scale integrated operations

Environmental permitting represents the most significant timeline risk, with potential delays from regulatory review processes and community engagement requirements. Mining operations in Texas face water usage concerns and environmental impact assessments that could extend development schedules.

Market timing considerations include rapidly growing demand for heavy rare earths driven by electric vehicle adoption and renewable energy infrastructure development. Delays in domestic production could result in continued dependence on Chinese suppliers during peak demand growth periods.

The global rare earth market exhibits significant price volatility based on Chinese policy changes and demand fluctuations from technology and automotive sectors. This volatility creates both opportunities and risks for new production ventures requiring substantial upfront capital investment.

Investment Pattern Implications for Mining Sector Development

The government's equity participation model establishes precedents that could attract additional private capital to critical minerals development. Risk-sharing structures reduce private investor concerns about regulatory and market uncertainties inherent in resource development projects.

Policy Framework Evolution:

- Government equity participation: Precedent for strategic mineral investments

- Risk-sharing mechanisms: Public-private partnership models

- Industrial policy integration: Manufacturing and extraction coordination

- National security prioritisation: Defence considerations in investment decisions

The success of these investments could encourage expanded government participation in other critical mineral sectors including lithium processing, copper extraction, and battery manufacturing. This industrial policy approach represents a significant shift from traditional free-market approaches to resource development.

International competitiveness considerations may drive similar programmes in allied nations seeking to reduce Chinese dependencies. Coordination between U.S., Canadian, Australian, and European critical mineral initiatives could create alternative supply chains with strategic alliance benefits.

The capital market implications include potential premiums for domestic resource projects with government backing. This "national security premium" could improve project economics and attract institutional investment that might otherwise avoid resource sector volatility.

How Does Resource Independence Support U.S. Strategic Objectives?

Achieving domestic rare earth production capabilities provides strategic flexibility in international negotiations and reduces vulnerabilities to supply disruptions. This resource independence supports broader geopolitical objectives including alliance strengthening and technological competitiveness.

Strategic Independence Objectives:

- Supply chain resilience: Reduced vulnerability to foreign disruptions

- Alliance coordination: Potential rare earth sharing with partner nations

- Diplomatic leverage: Domestic production as negotiating tool

- Technology security: Control over materials for defence systems

The development of domestic capabilities could enable rare earth exports to allied nations seeking to reduce Chinese dependencies. This reverse resource diplomacy could strengthen alliance relationships whilst generating export revenues for domestic producers.

Regional competition dynamics may intensify as China responds to reduced market dependence through policy adjustments or increased investment in alternative markets. The success of U.S. domestic production could encourage Chinese efforts to maintain market dominance through pricing competition or technology restrictions.

Trade relationship implications extend beyond rare earths to broader technology and manufacturing sectors. Reduced dependence on Chinese critical materials could provide negotiating flexibility in other bilateral trade discussions whilst reducing strategic vulnerabilities.

What Investment Risks Should Investors Consider?

Investors considering exposure to critical minerals development should evaluate multiple risk factors including technology development risks, market price volatility, and regulatory changes affecting government support programmes.

Portfolio Diversification Considerations:

- Sector rotation potential: Critical minerals as infrastructure investment

- Government backing benefits: Reduced political and regulatory risks

- Long-term demand drivers: Renewable energy and defence spending growth

- Supply constraint advantages: Limited global production alternatives

The investment timeline for critical minerals projects typically extends 5-10 years from development through commercial production. This extended timeline requires patient capital and careful evaluation of intermediate milestones that could affect project viability.

Risk Assessment Categories:

- Technical development risks: Unproven extraction and processing methods

- Commodity price volatility: Market cycles affecting project economics

- Regulatory uncertainty: Policy changes impacting government support

- Competition emergence: Other domestic and international production projects

Near-term investment catalysts include magnet facility launch milestones, mine development progress, and capacity expansion announcements. These operational achievements provide measurable progress indicators for evaluating management execution capabilities.

Medium-term value creation depends on successful mine development, processing facility integration, and market penetration in target industries. The transition from imported feedstock to domestic materials represents a critical operational milestone for profitability analysis.

Long-term strategic positioning requires evaluating the sustainability of domestic production cost structures compared to international competition and the durability of government support programmes across different political administrations. The Trump administration investment in USA Rare Earth demonstrates bipartisan support for strategic minerals development that could continue across political cycles.

Disclaimer: This analysis is for informational purposes only and should not be considered investment advice. Critical minerals investments involve significant risks including commodity price volatility, regulatory changes, and technical development challenges. Prospective investors should conduct thorough due diligence and consult with qualified financial advisors before making investment decisions. Government policy changes could materially affect the economics and strategic value of domestic critical minerals projects.

Want to Capitalise on Strategic Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities ahead of the broader market. Explore why major mineral discoveries can generate exceptional returns by visiting Discovery Alert's dedicated discoveries page and begin your 30-day free trial today.