May 22, 2026

Strategic Geography Meets Maritime Security: The Energy Equation

Global shipping networks face unprecedented complexity as traditional transit routes confront evolving security challenges. Furthermore, HSFO prices jump 40% as war chokes key Singapore bunkering hub, demonstrating how maritime fuel markets respond to geopolitical disruptions. Singapore's position within this dynamic illustrates how established infrastructure meets contemporary market pressures.

The bunker fuel sector operates through interconnected supply chains where location, capacity, and operational reliability determine competitive positioning. Market participants evaluate multiple variables when selecting refuelling destinations, including price differentials, inventory availability, and logistical efficiency. These calculations have intensified as global shipping patterns adapt to changing geopolitical landscapes.

When big ASX news breaks, our subscribers know first

What Makes Singapore the World's Most Critical Marine Fuel Hub?

Singapore's maritime dominance stems from a combination of strategic positioning and sophisticated infrastructure development. The port's location at the convergence of major shipping lanes connecting Asia, Europe, and the Middle East creates natural advantages for vessel traffic optimisation.

Strategic Geographic Positioning

The Strait of Malacca handles approximately 25% of global seaborne trade, positioning Singapore as a critical waypoint for international commerce. This geographic advantage translates into consistent vessel traffic, creating steady demand for bunker fuel services.

Key geographic benefits include:

- Direct access to three major shipping routes

- Minimal deviation from established trade corridors

- Deep-water capabilities accommodating vessels up to 400 metres in length

- 24-hour operations supporting continuous traffic flow

Market Share and Volume Statistics

Singapore's bunker sales reached 54.9 million tonnes in 2024, representing approximately 18% of global bunker fuel demand. This volume reflects both the hub's established market position and its ability to scale operations during periods of increased demand.

| Hub | Annual Volume (Million Tonnes) | Market Share |

|---|---|---|

| Singapore | 54.9 | 18% |

| Rotterdam | 12.5 | 4% |

| Fujairah | 11.2 | 3.7% |

| Shanghai | 8.9 | 2.9% |

High Sulphur Fuel Oil (HSFO) accounts for 65% of Singapore's bunker sales, reflecting the port's specialisation in serving vessels operating on traditional fuel systems. This product mix positions Singapore as a critical supplier for the substantial portion of the global fleet that continues operating on HSFO.

The concentration of refinery capacity within Southeast Asia strengthens Singapore's supply chain resilience. Twelve major refineries within a 500-kilometre radius provide consistent feedstock availability, reducing supply disruption risks during market volatility periods.

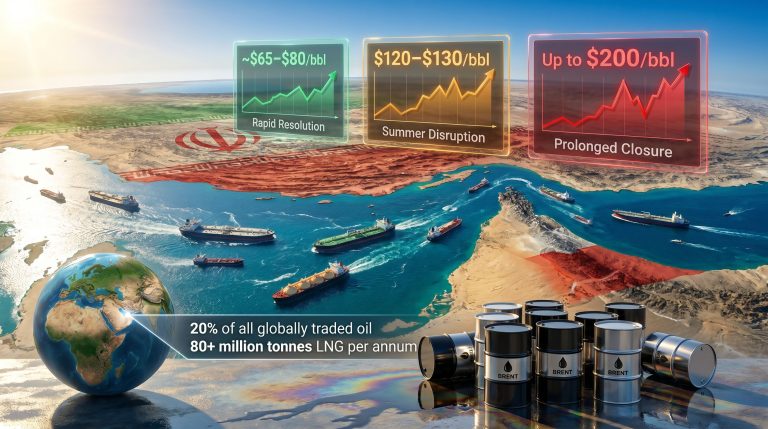

How Are Middle East Conflicts Driving Unprecedented Fuel Price Volatility?

Regional tensions have created significant disruptions to established shipping patterns, fundamentally altering global energy transportation dynamics. The Strait of Hormuz, traditionally handling 20% of global oil transit and 22% of LNG flows, has experienced dramatic traffic reductions. However, these disruptions have also contributed to broader oil price stagnation as markets adjust to new supply realities.

Strait of Hormuz Traffic Analysis

Recent monitoring data indicates vessel transits through the Strait of Hormuz have dropped from 138 ships daily to just 2 vessels, representing a 98.6% reduction in normal traffic patterns. This collapse has forced extensive rerouting of energy shipments, according to recent shipping industry analysis.

Traffic Impact Analysis:

- Crude oil tankers: 95% reduction in daily transits

- LNG carriers: 97% decrease in passage frequency

- Product tankers: 99% drop in normal routing

- Container vessels: 85% traffic diversion to alternative routes

The reduction has created immediate supply chain pressures across Asian markets, where approximately 60% of imported energy traditionally transits through the strait. This dependency has intensified competition for alternative supply sources and transportation routes.

Regional Supply Chain Reconfiguration

Cape of Good Hope diversions have increased voyage times by 14-21 days for shipments redirected from traditional Middle East routes. These extended journeys increase operational costs whilst reducing vessel availability for additional cargo cycles.

UAE Fujairah has experienced reduced competitive positioning as regional instability affects its traditional role as a Middle East bunkering hub. Vessel operators increasingly seek alternatives in more stable operational environments.

Qatar's LNG export capacity has faced significant constraints, with QatarEnergy declaring force majeure on multiple supply contracts. This disruption affects approximately 22% of global LNG supply, creating ripple effects across international energy markets.

Why Are Shipping Companies Paying Premium Rates for Singapore Bunkers?

Market dynamics have shifted dramatically as shipping operators prioritise operational security over cost minimisation. Singapore's stability and infrastructure reliability have created willingness among vessel operators to accept higher fuel costs in exchange for operational certainty.

War Risk Premium Economics

HSFO prices in Singapore have increased by 40% compared to pre-conflict levels, with current pricing reaching $375.79 per tonne during peak demand periods. This represents a premium of $30-70 per tonne compared to Middle East alternatives when those remain accessible. These developments reflect broader oil price movements driven by geopolitical tensions.

The premium structure reflects multiple cost components:

- Base fuel cost: Standard market pricing

- Security premium: 15-20% for operational stability

- Logistics surcharge: 8-12% for guaranteed availability

- Infrastructure access: 5-8% for priority berthing

Charter rates for large crude carriers have reached $400,000 daily for routes serving Asian destinations, compared to typical rates of $150,000-200,000 daily during normal market conditions. These increases reflect both vessel scarcity and elevated operational risks.

Port Congestion and Capacity Constraints

Singapore's port facilities face unprecedented demand, with average waiting times reaching 7 days for vessel services during peak periods. This congestion reflects the concentration of diverted traffic seeking secure refuelling options.

Operational Capacity Metrics:

- Daily vessel arrivals: 45% above normal levels

- Average service time: Extended from 18 to 32 hours

- Storage utilisation: 87% across all fuel grades

- Throughput capacity: Operating at 95% of maximum levels

Inventory management has become increasingly complex as suppliers balance immediate demand against supply chain uncertainties. Strategic reserves have been drawn down to maintain service levels whilst alternative supply sources are secured.

What Economic Forces Are Driving HSFO Market Dynamics in 2026?

HSFO pricing patterns in early 2026 reflect multiple underlying market forces beyond immediate supply disruptions. January 2026 average pricing of $375.79 per tonne represents the interaction of supply constraints, demand concentration, and regulatory transition effects. These dynamics contribute to a broader oil price crash analysis that examines multiple market factors.

Supply-Demand Imbalance Factors

Pre-regulation inventory clearing continues to influence market dynamics as the industry approaches the 2030 sulphur content transition deadline. Many operators are consuming existing HSFO stocks whilst evaluating long-term fuel strategy options.

Asian refining margins have reached 4-year highs as regional processing capacity operates at 92% utilisation rates. This intensive operation reflects both strong demand and the need to maximise output during supply constraint periods.

Monthly volatility patterns show:

- Peak demand periods: 25-35% price variations

- Seasonal adjustments: 12-18% quarterly fluctuations

- Supply disruption events: 40-60% temporary price spikes

- Contract vs. spot differentials: 15-20% premium for immediate delivery

Refinery Output and Distribution Networks

Regional refinery operations have adapted to serve concentrated demand patterns. Processing capacity expansion projects accelerated to meet increased throughput requirements, with $8.2 billion in announced investments across Southeast Asian facilities.

Strategic Petroleum Reserve discussions have emerged across multiple jurisdictions as governments evaluate energy security measures. The U.S. has indicated it will not immediately tap strategic reserves, preferring market-based solutions to current supply challenges.

How Will Prolonged Conflict Reshape Global Bunkering Geography?

Extended regional instability could fundamentally alter the global distribution of marine fuel infrastructure. Current traffic diversions may evolve into permanent routing changes if security conditions do not improve substantially. These shifts could significantly impact OPEC production impact on global energy markets.

Short-Term Market Opportunities

Singapore's revenue per vessel has increased 35-42% despite higher operational costs, reflecting the port's ability to capture value during market disruption periods. This performance demonstrates the premium markets place on operational reliability.

Market share gains from regional instability have strengthened Singapore's competitive position. The port has captured an estimated additional 8.7 million tonnes of annual demand diverted from Middle East alternatives.

Investment in alternative hub development has accelerated across multiple regions. Indian ports, Australian facilities, and West African locations have all announced expansion projects designed to serve as backup options for traditional Middle East routing.

Long-Term Strategic Risks

Permanent shipping route changes could reduce demand for Middle East bunkering facilities whilst creating sustained demand growth for alternative locations. This restructuring would represent a fundamental shift in global maritime fuel geography.

Energy security considerations have become central to Asian economic planning. Japan has requested government intervention to release strategic oil reserves, whilst India faces reduced industrial gas supply due to Qatar production constraints.

Infrastructure investment priorities are shifting toward supply chain diversification and strategic redundancy. Port operators are evaluating expansion projects based on worst-case scenario planning rather than traditional demand forecasting methods.

The next major ASX story will hit our subscribers first

What Are the Broader Economic Implications for Maritime Trade?

Supply chain disruptions extend beyond immediate fuel cost increases to affect broader economic relationships. Asian markets have experienced volatility as energy price increases contribute to inflationary pressures across multiple sectors. Furthermore, these developments highlight global oil market influence on regional economies.

Inflation and Energy Cost Transmission

Electricity and fuel price increases in Singapore reflect broader regional energy market pressures. Industrial users face 15-25% higher energy costs compared to pre-conflict levels, affecting manufacturing competitiveness.

Supply chain disruption effects include:

- Extended delivery timeframes: 20-30% longer for affected routes

- Inventory cost increases: 12-18% higher working capital requirements

- Transportation cost inflation: 25-40% premium for alternative routing

- Contract renegotiation frequency: Quarterly vs. annual adjustments

Consumer price transmission varies by sector, with energy-intensive industries experiencing the most significant impacts. Transportation, chemicals, and manufacturing sectors show 8-15% cost structure increases due to elevated energy expenses.

Investment and Policy Response Scenarios

Government intervention possibilities range from strategic reserve releases to coordinated international responses. Policy makers balance market stability concerns against long-term energy security objectives.

Private sector adaptation includes accelerated investment in alternative energy sources, supply chain diversification projects, and enhanced risk management capabilities. Insurance premium increases of 200-400% for certain routes have prompted fundamental reassessment of operational strategies.

Which Market Indicators Should Traders Monitor for Future Price Movements?

HSFO price forecasting requires analysis of multiple interconnected variables beyond traditional supply-demand fundamentals. Current market conditions necessitate expanded monitoring frameworks incorporating geopolitical risk assessment.

Geopolitical Risk Assessment Framework

Conflict escalation indicators include diplomatic communication patterns, military deployment announcements, and international intervention discussions. These factors provide early warning signals for potential supply disruption expansion.

Key monitoring metrics:

- Daily vessel transit counts through critical chokepoints

- Regional refinery utilisation rates and maintenance schedules

- Strategic reserve inventory levels across major consuming nations

- Alternative route development progress and capacity additions

Goldman Sachs has increased Q2 Brent oil price forecasts by $10, reflecting expectations that current disruptions may persist longer than initially anticipated. This adjustment suggests professional forecasters are incorporating extended timeline scenarios into their analysis.

Technical Market Analysis Tools

HSFO futures contract behaviour shows increased volatility and steeper contango structures, indicating market expectations of sustained near-term tightness with eventual normalisation. Contract liquidity has decreased 30-40% as participants reduce speculative positions.

Correlation analysis reveals stronger relationships between crude oil prices and bunker fuel costs, with correlation coefficients reaching 0.85-0.90 compared to typical ranges of 0.65-0.75. This increased correlation reflects supply chain concentration effects, as detailed in maritime industry reports.

Seasonal demand patterns have become less predictable as extraordinary circumstances override typical consumption cycles. Traditional forecasting models require adjustment factors of 15-25% to account for current market conditions.

"Investment Professional Disclaimer: Market analysis presented reflects current conditions and available data. Energy markets involve substantial risk, and past performance does not guarantee future results. Investors should conduct independent research and consider professional advice before making investment decisions. Geopolitical events may significantly impact market outcomes beyond traditional forecasting capabilities."

Ready to Invest in the Next Major Energy Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including critical energy minerals that could benefit from current market disruptions and supply chain reconfigurations. Begin your 14-day free trial today to position yourself ahead of the market as energy security concerns drive increased focus on domestic resource development.