June 5, 2026

Strategic Infrastructure Vulnerabilities in the Modern Supply Chain Era

Critical mineral dependencies have evolved from theoretical supply chain concerns into active geopolitical leverage points. Modern economies rely on complex networks of specialised processing facilities, creating vulnerabilities that traditional stockpiling approaches were never designed to address. The concentration of rare earth element refining capacity in a single nation exemplifies how technological advancement can create strategic chokepoints that transcend simple resource scarcity.

Unlike previous eras where mineral security focused primarily on ore availability, contemporary supply chains face processing bottlenecks that can disrupt entire industries within months. This reality has prompted a fundamental reassessment of how nations approach resource security, leading to the largest strategic minerals accumulation programme since the Cold War era. Furthermore, recent policy developments highlight critical minerals energy security concerns that extend beyond traditional defence applications.

When big ASX news breaks, our subscribers know first

Understanding America's National Defence Stockpile Framework

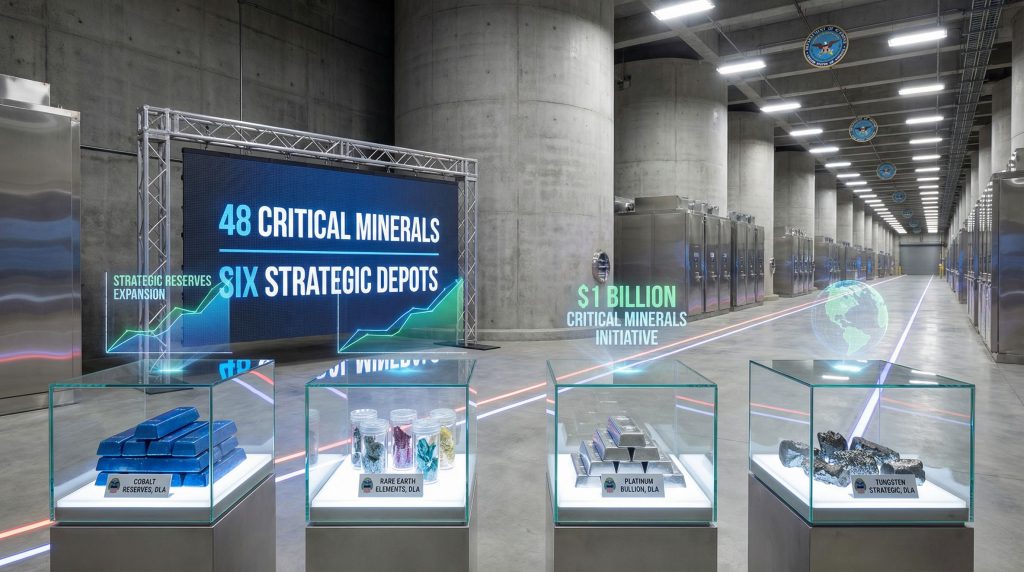

The US strategic minerals stockpile operates through a complex institutional framework managed by the Defense Logistics Agency under Title 50 U.S. Code § 98. This statutory foundation, dating to the Strategic and Critical Materials Stock Piling Act of 1939, establishes the legal framework for accumulating, maintaining, and distributing strategic materials essential to national defence.

The current system encompasses approximately 50 critical minerals distributed across six strategic depots located throughout the continental United States. These facilities serve dual purposes: maintaining emergency reserves for national security scenarios while supporting ongoing defence production requirements through carefully managed material releases.

Operational Framework and Constitutional Mandate

The stockpile operates under a stewardship model rather than active market participation. This distinction proves crucial for understanding operational constraints and funding mechanisms. The Defense Logistics Agency manages materials with security-first priorities, accepting potential economic inefficiency to ensure strategic readiness.

Key operational characteristics include:

• Self-sustaining funding through authorised excess material sales

• Congressional oversight via semi-annual reporting requirements

• Restricted access limited to federal agencies and authorised contractors

• Geographic distribution ensuring regional supply accessibility and redundancy

The funding model creates unique dynamics where surplus material sales generate revenue for maintenance and new acquisitions. However, this mechanism faces constraints under 50 U.S.C. § 98e, which prohibits sales that might depress domestic industry prices or compromise national security objectives.

Evolution from Cold War to Modern Supply Chain Security

Historical context reveals significant shifts in strategic thinking about mineral security. The original 1939 legislation emphasised raw material availability during potential wartime scenarios. Contemporary applications address processing capacity concentration and technological supply chain vulnerabilities that extend beyond simple material scarcity.

Modern threats include dependency on foreign processing facilities for materials available domestically in ore form. Rare earth elements exemplify this challenge where substantial U.S. deposits exist, but processing capacity remains concentrated in China, creating vulnerability despite domestic resource availability.

Geopolitical Context Behind Strategic Stockpiling

China's dominance in critical mineral processing represents the most significant supply chain vulnerability facing the United States and allied nations. Current data indicates approximately 85-90% of global rare earth refining capacity operates within Chinese facilities, creating dependency relationships that transcend traditional trade considerations.

Additionally, developments such as the US Senate ban on uranium imports from Russia highlight the interconnected nature of energy security and mineral dependency issues.

Processing Concentration vs. Resource Availability

The supply chain vulnerability mechanism operates through processing chokepoints rather than ore scarcity. Multiple nations possess significant rare earth deposits, including the United States, Australia, and Brazil. However, Chinese investment in separation and refining technology over the past three decades created processing capabilities that other nations struggle to replicate quickly.

Critical dependency statistics reveal:

• 80%+ U.S. import reliance for rare earth elements, cobalt, and tungsten

• 15-17 major Chinese processing facilities versus 1-2 U.S. refining operations

• 3-6 month disruption timeline for semiconductor and defence applications if Chinese processing access ceased

• 90%+ Chinese control of rare earth separation and purification technology

Allied Coordination Challenges

Unlike energy security coordination through established international frameworks, critical mineral cooperation remains fragmented. Japan maintains strategic reserves through public-private partnerships, while South Korea focuses on technology metals stockpiling. The European CRM facility initiative establishes procurement targets but lacks centralised coordination mechanisms comparable to energy security protocols.

This coordination gap creates inefficiencies where allied nations compete for the same limited processing capacity rather than developing complementary supply chains or shared strategic reserves.

How Does the Current US Strategic Minerals Stockpile Operate?

Institutional Management and Governance Structure

The Defense Logistics Agency Strategic Materials Division oversees day-to-day stockpile operations through a complex governance structure involving multiple federal agencies. Decision-making authority flows through the Under Secretary of Defense for Acquisition & Sustainment, with Congressional oversight provided by both Armed Services Committees.

Governance characteristics include:

• Multi-level personnel access controls requiring security clearances

• Integrated inventory tracking through DoD enterprise resource planning systems

• Quarterly audits with semi-annual Congressional reporting requirements

• Interagency coordination protocols involving State, Commerce, and Defence departments

The self-sustaining funding model operates through a revolving fund mechanism where authorised surplus sales generate revenue for operations and strategic acquisitions. This creates procyclical budget constraints where declining commodity prices reduce sale revenues exactly when strategic acquisition budgets may be needed most.

Current Inventory Composition and Strategic Assessment

Strategic materials classification follows a tier-based vulnerability assessment system that prioritises resources based on supply risk and defence criticality. This framework guides acquisition decisions and rotation protocols for maintaining material quality over extended storage periods.

Strategic Material Classification by Vulnerability Tier

| Tier Level | Materials | Supply Risk Factors | Current Reserve Adequacy |

|---|---|---|---|

| Tier 1 (Critical) | Rare earth oxides, refined cobalt, tungsten | Processing concentration, geopolitical risk | 18-24 months military consumption |

| Tier 2 (Moderate) | Antimony, tantalum, gallium | Limited supplier diversity | 2-3 years military consumption |

| Tier 3 (Lower Risk) | Zinc, chromium, aluminium alloys | Multiple suppliers available | 3+ years military consumption |

Quality Management and Rotation Protocols

Material degradation represents a significant operational challenge, particularly for moisture-sensitive rare earth oxides and oxidation-prone reactive metals. Rotation protocols typically operate on 5-7 year cycles, requiring periodic material processing to maintain specifications.

Critical maintenance requirements include:

• Climate-controlled storage for moisture-sensitive materials

• Nitrogen atmosphere storage for oxidation-prone metals

• Regular quality testing and grade verification

• Scheduled rotation to prevent crystalline structure degradation

These protocols constitute approximately 15-25% of annual operational budgets, representing substantial fixed costs that influence long-term stockpile economics.

Recent Policy Changes Under the Trump Administration

The $1 Billion Critical Minerals Initiative (2024-2025)

The Defence Production Act authorisation represents the largest strategic mineral acquisition programme since the 1950s Cold War buildup. This initiative targets specific vulnerability gaps identified through recent supply chain assessments conducted by defence agencies. In addition, the recent Trump executive order on critical minerals has accelerated these procurement efforts.

Targeted procurement allocations include:

• $500 million for cobalt addressing aerospace and defence battery applications

• $245 million for antimony supporting armour-piercing ammunition production

• $100 million for tantalum ensuring electronics and capacitor manufacturing

• $45 million for scandium supporting advanced aerospace alloy development

• Exploratory purchases in tungsten, bismuth, and indium markets

This procurement strategy emphasises materials where processing concentration creates immediate vulnerability rather than long-term availability concerns.

USGS Critical Minerals List Expansion (2025)

The expansion from 40 to 60 designated critical minerals reflects broader recognition of supply chain vulnerabilities extending beyond traditional defence applications. Notable additions include copper and uranium, materials previously considered abundant but now recognised as strategically critical due to energy transition requirements.

Significant new inclusions encompass:

• Copper for renewable energy infrastructure and EV charging networks

• Uranium for nuclear power and naval propulsion systems

• Silver for solar panel production and electronic applications

• Metallurgical coal for domestic steel production capabilities

These additions reflect expanded strategic thinking about materials essential for economic security beyond immediate military applications.

Proposed Legislative Changes and Strategic Resilience Framework

The Strategic Resilience Reserve Proposal

Congressional proposals for a $2.5 billion Strategic Resilience Reserve would establish governance structures extending beyond pure defence applications to include economic security considerations. This framework represents fundamental expansion of strategic stockpiling philosophy.

Proposed governance structure features:

• Seven-member board with private sector and academic representation

• Allied contribution requirements ($100 million minimum participation)

• Commercial sales authorisation for market stabilisation purposes

• Dual-use objectives balancing defence and economic security

Market Intervention Capabilities

The proposed framework would authorise limited market intervention during extreme price volatility, representing significant departure from current restrictions on commercial market participation. This capability aims to support domestic semiconductor and electric vehicle supply chains during disruption scenarios.

However, this expansion raises complex questions about balancing strategic reserves with market competition principles. Private sector concerns about government market participation could create unintended consequences for domestic investment incentives.

Recycled Materials Integration Strategy

Priority sourcing from domestic recycling operations reflects circular economy principles in strategic stockpile management. This approach addresses both environmental sustainability and supply chain resilience by reducing dependency on virgin material imports.

Integration mechanisms include:

• Technology development incentives for materials recovery

• Procurement preferences for domestically recycled content

• Investment in advanced separation and purification technologies

• Public-private partnerships for recycling infrastructure development

The next major ASX story will hit our subscribers first

Economic Implications for Global Commodity Markets

Market Dynamics and Price Impact Analysis

Government procurement at the scale proposed creates significant demand-side pressure on global commodity markets. Historical precedent from Cold War stockpiling demonstrates potential for sustained price increases when government purchasing represents substantial market share.

Current market dynamics suggest vulnerability to price inflation in several targeted materials:

• Cobalt markets already experiencing supply constraints from Democratic Republic of Congo production challenges

• Antimony prices showing volatility due to Chinese export restrictions

• Rare earth elements facing limited processing capacity relative to growing demand

• Tungsten supplies concentrated among few producers globally

According to Bloomberg's analysis, these market pressures have prompted significant policy responses from major economies.

Investment Opportunities in Strategic Minerals Sector

The strategic stockpiling initiative creates multiple investment opportunities across the minerals value chain, from exploration companies with domestic reserves to processing facilities that can reduce import dependency. However, investors should note that government purchasing may create artificial demand spikes followed by market corrections.

Key investment themes emerging include:

• Domestic mining companies with critical mineral deposits

• Processing and refining technology development

• Recycling and circular economy infrastructure

• Advanced materials and substitution technologies

Impact on Allied Nations and Trading Partners

U.S. strategic stockpiling creates both opportunities and challenges for allied nations and trading partners. Canada's critical minerals strategy aligns with U.S. objectives, potentially creating integrated North American supply chains. Australia's role as alternative supplier to Chinese dominance positions the nation as strategic partner for rare earth elements and critical minerals.

However, developing nations dependent on mineral export revenues may face market volatility as strategic stockpiling alters traditional demand patterns and price relationships. Furthermore, the US–China trade war impact on global markets continues to influence these dynamics.

Implementation Challenges and Constraints

Physical and Logistical Constraints

Geological limitations on domestic mineral availability create fundamental constraints on strategic autonomy objectives. While the United States possesses substantial mineral resources, processing capacity bottlenecks limit near-term self-sufficiency potential.

Critical infrastructure constraints include:

• Limited domestic rare earth processing facilities

• Specialised storage requirements for reactive and hazardous materials

• Transportation infrastructure for secure material movement

• Skilled workforce requirements for advanced processing operations

Current Inventory Adequacy Assessment

Existing strategic reserves demonstrate significant inadequacy relative to expanded security requirements. Recent assessments reveal concerning gaps across multiple critical materials categories.

Adequacy gaps include:

• Germanium reserves covering only six months of U.S. consumption

• Rare earth stockpiles representing 18-24 months military requirements

• Quality degradation in aging stockpile materials requiring replacement

• Rotation scheduling challenges affecting material availability

Budgetary and Political Sustainability

Long-term funding commitments across multiple administrations present political sustainability challenges. Strategic stockpiling requires sustained investment over decades, creating vulnerability to changing political priorities and budget pressures.

Congressional oversight processes may create delays in procurement during time-sensitive market conditions. Competition with other defence spending priorities could affect funding consistency required for effective strategic stockpile management.

International Comparisons and Best Practices

Global Approaches to Critical Materials Management

International experience provides valuable insights for U.S. strategic stockpile development. Japan's hybrid public-private model demonstrates effective coordination between government strategic objectives and private sector capabilities.

Comparative frameworks include:

• Japan's JOGMEC model combining government funding with private sector expertise

• South Korea's technology metals reserves focusing on semiconductor industry needs

• European Union's Critical Raw Materials Act establishing procurement targets and domestic processing incentives

• China's state-controlled reserves integrating strategic stockpiles with industrial policy

Lessons from Historical Stockpiling Programmes

The Strategic Petroleum Reserve provides relevant precedent for large-scale government commodity stockpiling. Peak capacity of 727 million barrels demonstrated sustained political commitment to strategic resource accumulation over multiple decades.

However, 1970s-1980s surplus disposal from defence stockpiles created market disruption when excess materials were sold without careful consideration of industry impacts. These experiences highlight importance of managed disposal protocols and market impact assessment.

Technology Development and Future Strategic Directions

Advanced Materials and Substitution Research

Technology development priorities focus on reducing dependency through material substitution and advanced recycling capabilities. Research investments target synthetic biology applications for materials production and nanotechnology implications for strategic material requirements.

Critical research areas include:

• Alternative rare earth element applications and substitutes

• Advanced separation and purification technologies

• Synthetic biology approaches to material production

• Quantum materials and next-generation electronics applications

Supply Chain Resilience Beyond Stockpiling

Comprehensive supply chain security requires expansion beyond simple material accumulation to include domestic processing capacity development and allied partnership frameworks. Private sector incentives for domestic production investment complement strategic stockpiling objectives.

Trade policy coordination with strategic stockpile objectives ensures consistent approach across government agencies and departments. This integration prevents conflicting policies that might undermine strategic autonomy goals.

Scenario Planning for Geopolitical Outcomes

Strategic planning must account for multiple potential future scenarios affecting global mineral markets and supply chains. Escalating trade tensions could accelerate supply chain fragmentation, requiring expanded domestic capabilities.

Climate change effects on global mining operations may alter traditional supply relationships and create new strategic considerations. Technological breakthroughs in materials science could fundamentally change demand patterns for specific strategic materials.

What Are the Long-Term Implications for Market Stability?

Recent Financial Times reporting on the $17 billion expansion suggests that market stability considerations will become increasingly important. The scale of government intervention in commodity markets creates both stabilising and destabilising effects that require careful management.

Price volatility concerns affect both producers and consumers of strategic materials. Whilst government purchasing provides demand support during market downturns, sudden procurement activities can create artificial price spikes that disadvantage commercial users.

Balancing Strategic Security with Market Efficiency

The evolution of America's US strategic minerals stockpile from Cold War-era emergency preparation to modern supply chain security tool reflects fundamental changes in how nations approach economic resilience. The current expansion represents recognition that critical materials have achieved strategic importance comparable to traditional military assets.

Success depends on careful balance between market intervention and strategic preparedness objectives. Whilst the $12 billion commitment signals serious recognition of supply chain vulnerabilities, effective implementation requires addressing processing capacity constraints, allied coordination mechanisms, and long-term sustainability challenges extending far beyond material accumulation.

For investors and industry participants, strategic stockpiling expansion creates both opportunities and uncertainties. Government purchasing provides demand support for domestic producers whilst creating potential market volatility requiring careful navigation. The intersection of national security policy with commodity markets establishes new dynamics that will influence investment decisions and strategic planning across multiple sectors.

The broader implications extend beyond immediate procurement activities to encompass technological development, international cooperation frameworks, and fundamental questions about the role of government in critical materials markets. As supply chain security becomes increasingly central to national security considerations, the strategic minerals stockpile represents one component of comprehensive approaches to economic resilience in an era of geopolitical competition and technological interdependence.

Ready to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert provides instant notifications on significant ASX mineral discoveries using its proprietary Discovery IQ model, delivering real-time insights into actionable opportunities across critical minerals sectors. Stay ahead of market movements in strategic commodities by exploring Discovery Alert's dedicated discoveries page to see how historic mineral discoveries have generated substantial returns, then begin your 14-day free trial today to secure your market-leading advantage.