July 23, 2026

Strategic Market Leverage Through Supply Management

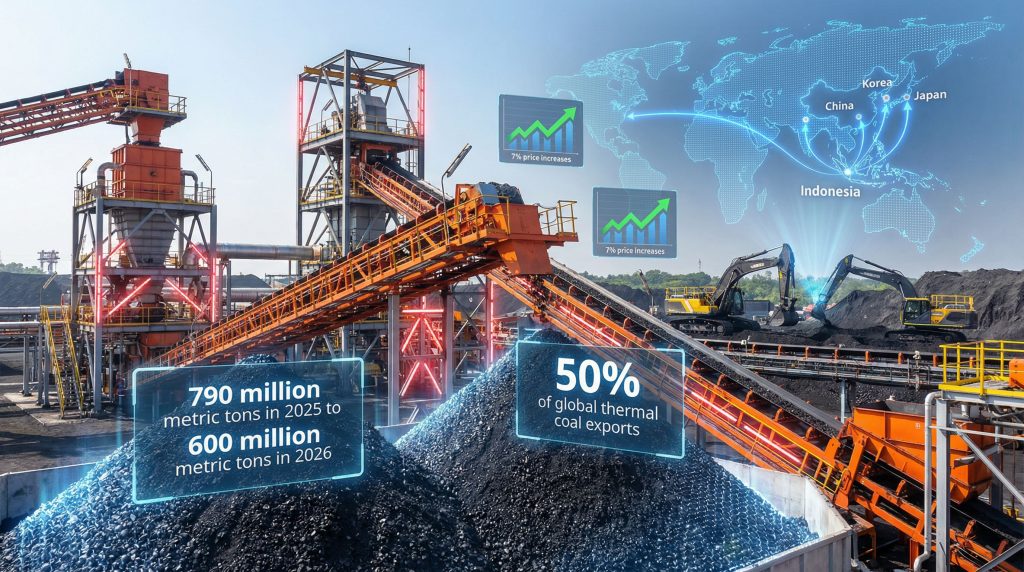

Indonesia commands approximately 50% of global thermal coal exports, representing nearly half of the 960 million metric tons of electricity-grade coal exported worldwide in 2025, according to Kpler data. This dominant market position establishes Indonesia as the critical supplier in international thermal coal markets, where any significant policy adjustment creates immediate ripple effects across global supply chains.

The nation's recent implementation of production quotas reflects a calculated economic strategy rather than operational constraints. Furthermore, Indonesian miners halt coal exports exceeded 510 million tons in 2025, demonstrating the scale at which supply modifications impact international markets. This volume represents substantial market power that enables the government to influence global pricing through production management decisions.

Indonesian coal reserves consist predominantly of lower-grade thermal coal suitable for electricity generation, with deposits concentrated across multiple mining regions. The established infrastructure includes port facilities, logistics networks, and trading relationships developed over decades of market participation. This infrastructure advantage reinforces Indonesia's competitive position and makes rapid supply chain substitution challenging for importing nations.

The government's approach acknowledges that thermal coal markets have experienced oversupply conditions in recent periods, creating downward pressure on prices and reducing export revenues. However, rather than competing purely on volume in a buyer's market, Indonesian policymakers have chosen to exercise market leverage through strategic supply management, considering various mining permitting insights that affect production decisions.

When big ASX news breaks, our subscribers know first

Production Quota Implementation and Revenue Optimization

The Indonesian government's decision to reduce total coal production from approximately 790 million metric tons in 2025 to 600 million metric tons in 2026 represents a production contraction of roughly 190 million tons, or approximately 24% of total output. This planned reduction demonstrates a deliberate policy choice prioritizing value maximization over volume expansion.

Domestic Market Obligation Framework

Mining companies must now allocate 30% of production to meet Domestic Market Obligations for state utility PLN, with government officials indicating potential increases in this percentage as quotas tighten further. This requirement effectively guarantees domestic coal availability for Indonesia's power generation sector while reducing volumes available for export markets.

The DMO allocation mechanism operates through direct contracts between mining companies and PLN, requiring detailed documentation of compliance as part of the approval process for Work and Budget Plans. In addition, mining companies must submit these revised plans for government approval, creating administrative bottlenecks in implementation while maintaining compliance with multiple regulatory frameworks simultaneously.

This framework prioritizes energy security for Indonesia's domestic economy over export revenue maximization. By reserving substantial production for domestic consumption, the government ensures reliable coal supplies for electricity generation, supporting Indonesia's economic development objectives and industrial policy goals.

Administrative and Compliance Challenges

The quota system operates through Indonesia's Ministry of Energy and Mineral Resources, requiring comprehensive documentation of production plans, budgets, and environmental compliance measures. This approval process creates administrative delays that prevent immediate implementation of revised production strategies while maintaining oversight of industry operations.

Nearly 300 mining operations face potential shutdowns due to non-compliance with forest permit requirements, adding regulatory pressure beyond quota restrictions. H. Kristiono, deputy chairman of the Indonesian Coal Mining Association, acknowledged that mining companies continue production but not at full capacity, with coal shipments limited pending final government decisions on quota allocations.

Market Response and Price Dynamics

Lower-grade 4,200 kcal/kg Indonesian coal experienced approximately 7% price increases in January 2026, according to data from India-based coal trader I-Energy Natural Resources. This price movement occurred in anticipation of announced quota restrictions, demonstrating immediate market responsiveness to policy signals before actual supply constraints materialised.

Industry analysts project potential 40% to 70% price increases for lower-grade coal under scenarios involving 20% output reductions, according to London-based DBX Commodities analysis. Moreover, higher-grade coal varieties may experience 10% to 20% price appreciation under similar reduction scenarios, indicating substantial market sensitivity to Indonesian supply constraints.

Supply Availability and Trading Patterns

An Indian trader at the Coaltrans India conference in New Delhi reported that Indonesian spot coal cargoes were not available even at premiums of $1-$2 per ton over current prices. This indicates that supply restrictions have rendered spot coal essentially unavailable regardless of price premiums offered.

A Singapore-based trader stated that spot shipments are unlikely to resume this quarter unless Indonesia eases output cuts, suggesting supply unavailability rather than price equilibration resolving the shortage. Consequently, long-term contracts continue being honoured, though some miners are considering cancellations based on unforeseen circumstances clauses.

Regional Buyer Adaptation Strategies

Asian utilities representing major coal-consuming economies are actively increasing bids for alternative coal sources in response to Indonesian supply concerns. DBX Commodities CEO Alexandre Claude observed that the supply shock from Indonesia is driving other coal premiums higher, with bids from Japan, China, and Korea increasing as these nations seek stable supplies.

However, Claude also noted constraints on upward price movement, warning that policy reversals under labour or fiscal pressure, sharper-than-expected slowdowns in top buyer China, and sustained low gas prices could limit desired upside to coal prices. Furthermore, this assessment indicates that despite supply constraints, multiple demand-side and policy-side factors could moderate price appreciation, requiring careful analysis of tariff impact analysis on broader market dynamics.

Vasudev Pamnani, director at I-Energy Natural Resources, expects short-term supply and price shocks for Indian buyers while noting that continued cuts would provide India options to diversify imports from Russia, South Africa, and Mozambique. This diversification capability demonstrates that whilst Indonesian supply restrictions create immediate disruptions, medium-term adaptation through supply chain modification remains feasible.

Mining Operations and Quota Impact Analysis

Indonesian miners halt coal exports face quota reductions ranging from 40% to 70% below 2025 production levels, with specific reduction percentages varying by mining company. This variation creates a tiered impact structure across the approximately 300 mining operations in Indonesia, with consequences ranging from operational optimisation to potential mine closures.

| Impact Category | Quota Reduction Range | Operational Consequences |

|---|---|---|

| Severe Impact Miners | 60-70% reduction | Potential mine closures, workforce reductions |

| Moderate Impact Miners | 40-60% reduction | Operational scaling, contract renegotiations |

| Limited Impact Miners | 20-40% reduction | Production optimisation, efficiency focus |

| Minimal Impact Miners | <20% reduction | Continued normal operations |

The industry body's opposition to the quota system reflects concerns about employment and economic impacts, particularly in mining-dependent regions. The Indonesian Coal Mining Association has warned that production restrictions could trigger layoffs and mine closures, emphasising that production continues but not at full capacity pending final government decisions.

Financial Sector Implications

High-cost Indonesian coal producers face significant financial stress from reduced production volumes, with potential loan defaults and supply contract breaches creating broader financial sector risks. For instance, the government reportedly considers additional export levies, further pressuring profit margins for mining operations already constrained by production quotas.

This financial pressure creates particular challenges for marginal producers operating on thin profit margins, where reduced production volumes may render operations economically unviable. The combination of production restrictions and potential additional levies establishes a framework where only efficient, low-cost producers maintain profitability.

Long-Term Strategic Market Implications

Supply Chain Restructuring Opportunities

Alternative suppliers in Australia, Colombia, and South Africa may capture increased market share as Indonesian supplies become constrained. The current supply shock creates market opportunities for competing suppliers to establish or expand relationships with previously Indonesia-dependent buyers, potentially leading to permanent supply chain modifications.

This restructuring accelerates a broader global coal market diversification trend, reducing over-dependence on any single supplier whilst creating opportunities for competing producers. However, the transition to alternative suppliers requires contract renegotiations, quality adjustments, and logistics modifications that create transition costs and timeline constraints for importing utilities, necessitating sophisticated commodity trading insights.

Downstream Industrial Development Strategy

Indonesia's approach reflects a strategic pivot from primary commodity export dependence toward industrial development based on domestic resource processing. The 30% DMO allocation ensures domestic coal availability for downstream industrial applications, supporting government objectives for economic diversification through value-added manufacturing.

This policy acknowledges that coal processing and manufacturing create greater employment and economic value than raw coal exports alone. By prioritising domestic coal availability for industrial development, the government aims to establish Indonesia as a regional manufacturing hub rather than solely a raw material supplier.

The strategy aligns with broader economic development objectives targeting industrial policy goals and downstream value creation. Nevertheless, success depends on developing sufficient domestic industrial capacity to utilise the coal allocated for domestic consumption rather than export markets.

Risk Factors and Policy Sustainability

Demand-Side Variables

Continued weak demand from China and India could limit price appreciation despite supply restrictions, potentially undermining the quota strategy's effectiveness. Economic slowdowns in major Asian economies may reduce coal consumption regardless of supply constraints, creating scenarios where production restrictions fail to generate intended price improvements.

Buyers' preferences for higher-grade coal from alternative suppliers, combined with sustained weak demand patterns, could limit sharp price increases even under tight supply conditions. This dynamic suggests that demand fundamentals remain critical variables in determining whether supply management strategies achieve intended outcomes, particularly given ongoing trade war market impact considerations.

Policy Reversal Scenarios

Labour pressure from mining communities and fiscal revenue concerns could prompt government policy modifications or reversals. The Indonesian Coal Mining Association continues lobbying against the quota system, citing employment and economic impacts that may influence future policy decisions.

Historical precedent exists for policy reversals when economic or social pressures exceed government tolerance levels. For example, Indonesia's brief export ban in January 2022 was lifted after domestic market obligation compliance, demonstrating that export restrictions can be modified based on evolving circumstances.

Alternative Energy Transition Effects

Accelerated renewable energy adoption in key Asian markets may reduce long-term thermal coal demand, potentially undermining the quota strategy's long-term effectiveness. Energy transition policies in major consuming nations create structural headwinds for thermal coal demand that transcend supply-side management strategies.

The timeline for renewable energy deployment varies significantly across Asian markets, with some nations maintaining coal dependence for baseload power generation whilst others accelerate transition planning. This variation creates uncertainty regarding the duration of thermal coal demand that supports Indonesia's supply management approach.

The next major ASX story will hit our subscribers first

Market Rebalancing and Strategic Positioning

Indonesia's production quota implementation represents a calculated shift from volume-based to value-based coal export strategy, prioritising government revenue optimisation over market share maximisation. Whilst creating short-term supply pressures and price volatility, the policy aims to demonstrate market power and promote domestic industrial development simultaneously.

Success depends on maintaining market discipline whilst avoiding economic disruption that could prompt policy reversals. The government must balance export revenue objectives against domestic economic impacts, including employment effects in mining-dependent regions and broader fiscal considerations. In this context, understanding market volatility hedging becomes crucial for market participants.

The global coal market must adapt to this new supply reality through diversification strategies, alternative sourcing arrangements, and potentially accelerated energy transition planning. Indonesian miners halt coal exports policy decisions will continue serving as critical variables in global energy market dynamics, particularly given the nation's dominant export position.

Furthermore, mining industry sources suggest that the suspension of spot coal exports represents a coordinated response by mining companies to government production cut proposals, indicating significant industry opposition to the quota system.

Disclaimer: This analysis involves projections and market assessments that are inherently speculative. Coal market dynamics, government policies, and economic conditions may change significantly, affecting actual outcomes compared to current projections. Readers should conduct independent research and consider multiple perspectives when making investment or policy decisions related to thermal coal markets.

Want to Capitalise on Indonesia's Strategic Coal Market Shift?

Discovery Alert's proprietary Discovery IQ model provides real-time notifications on significant ASX mineral discoveries, helping investors identify opportunities in energy and commodity sectors before market disruptions like Indonesia's coal production cuts create broader impacts. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of evolving global commodity markets.