July 8, 2026

The Strategic Architecture of Critical Materials Control

Global supply chains for advanced technologies face an unprecedented concentration of control as processing capacity consolidates within specialised industrial ecosystems. The rare earth metals sector exemplifies how technical expertise, scale advantages, and coordinated policy frameworks can create formidable barriers to competition in strategic materials markets. China Northern Rare Earth capacity expansion represents a critical development that could reshape global supply dynamics across multiple industries.

Understanding these dynamics requires examining how vertical integration across mining, separation, refining, and manufacturing stages creates compounding advantages that extend far beyond simple production volume metrics. The interplay between technological innovation, automation innovations in mining, and governance structures shapes competitive positioning in ways that traditional market analysis often overlooks.

When big ASX news breaks, our subscribers know first

What Does China Northern Rare Earth Capacity Expansion Mean for Global Markets?

China's approach to rare earth supply chain development demonstrates how systematic capacity building across interconnected processing stages creates structural market advantages. The country's dominance extends beyond raw material extraction to encompass 70% of global rare earth processing capacity, with particularly strong control over separation and refining operations that Western competitors struggle to replicate cost-effectively.

Furthermore, this concentration reflects broader trends in the mining industry evolution where technological sophistication and scale economies create increasingly formidable competitive moats.

Vertical Integration as Strategic Defence

The integration of mining, processing, and manufacturing capabilities within coordinated industrial clusters provides multiple defensive advantages against potential competitors. This approach recognises that controlling downstream processing creates more sustainable competitive positioning than mining operations alone, as separation and refining require specialised technical knowledge, significant capital investment, and extended development timelines.

Key Integration Elements:

- Raw material processing facilities co-located with separation plants

- Specialised refining capacity integrated with magnet manufacturing

- Quality control systems spanning multiple processing stages

- Coordinated logistics and inventory management across the value chain

- Technical expertise concentrated within geographic clusters

Market Positioning Through Technical Barriers

China Northern Rare Earth capacity expansion reflects broader industrial strategy focused on creating technical and financial barriers that discourage alternative supply chain development. The combination of scale economies, process optimisation, and integrated infrastructure raises the minimum viable investment threshold for potential competitors entering separation and refining markets.

The global rare earth elements market, valued at approximately $8.2 billion in 2023 with projected growth of 8.2% annually through 2032, represents significant economic value concentrated within relatively few processing facilities. This market structure enables coordinated capacity planning that can influence pricing dynamics and supply availability across multiple downstream industries simultaneously.

Moreover, ongoing US–China trade impacts have highlighted the strategic importance of controlling critical material supply chains, making capacity expansion decisions increasingly significant for global market dynamics.

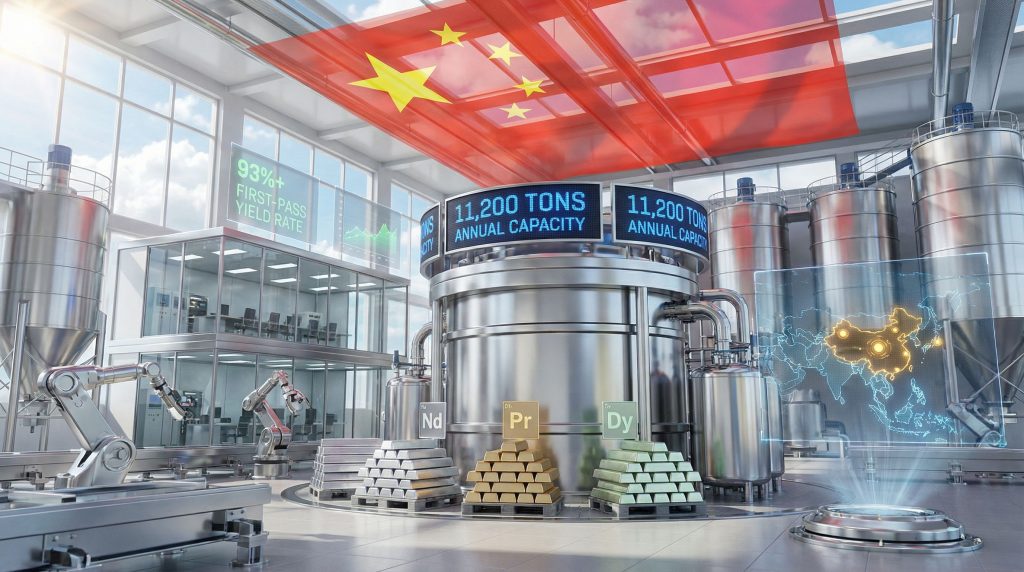

How Will Expanded Electrolysis Capacity Impact Global Supply Dynamics?

The commissioning of 11,200 tons of annual rare earth metal electrolysis capacity by Huaxing Rare Earth represents a significant addition to global processing capability. This expansion focuses on the highest-value stage of rare earth processing, where purified metals are produced for direct use in magnet manufacturing and specialised alloy production.

Production Efficiency and Quality Control

Advanced electrolysis operations achieve first-pass yields consistently above 93%, representing substantial improvements over traditional processing methods. These efficiency levels reduce waste generation, lower chemical consumption, and improve product consistency compared to older separation technologies.

| Performance Metric | Achieved Level | Strategic Impact |

|---|---|---|

| Annual Metal Capacity | 11,200 tons | Sufficient for large-scale magnet production |

| First-Pass Yield Rate | 93%+ | Reduces reprocessing costs and waste |

| Automation Integration | Full process control | Minimises operator variation |

| Quality Monitoring | Real-time systems | Ensures consistent product specifications |

Automation and Process Control

Implementation of intelligent weighing and feeding systems with real-time quality monitoring represents significant technological advancement in rare earth processing. These automation capabilities reduce labour requirements, improve process consistency, and enable rapid response to quality variations during production.

The integration of automated process control across electrolysis operations creates operational advantages that extend beyond simple cost reduction. Consistent product quality becomes a competitive differentiator for customers requiring precise material specifications for advanced manufacturing applications.

Supply Chain Bottleneck Control

Rare earth metal production represents a critical bottleneck between separated rare earth compounds and finished products like permanent magnets. Controlling electrolysis capacity provides leverage over downstream manufacturers who depend on purified metals for their production processes.

Critical Bottleneck Characteristics:

- Limited global alternative suppliers for rare earth metals

- High technical barriers to entry for electrolysis operations

- Significant capital requirements for competitive-scale facilities

- Extended development timelines for new processing capacity

- Complex environmental and regulatory approval processes

What Are the Geopolitical Implications of Integrated Party-State Governance?

The implementation of integrated governance frameworks within strategic industries creates alignment between commercial objectives and national policy priorities. China Northern Rare Earth's "153-Value-Driven" Party-building system represents systematic coordination between corporate strategy and state-directed industrial planning.

In addition, this approach contrasts sharply with Western approaches to industrial policy, particularly in the context of developing a comprehensive critical minerals strategy.

Governance Integration Framework

Structural Coordination Elements:

- Strategic planning aligned with national industrial policies

- Personnel management coordinated with state objectives

- Innovation priorities directed by policy frameworks

- Investment decisions integrated with broader economic planning

- Information management policies supporting strategic communication

This governance approach differs fundamentally from Western corporate structures, where commercial objectives typically operate independently from direct state policy coordination. The integration enables long-term strategic planning that can prioritise market positioning and capacity development over short-term profitability optimisation.

Information Control and Market Signalling

Formal training programmes addressing public opinion and media risk management demonstrate how information coordination is treated as an operational capability. This approach enables coordinated messaging across multiple channels to support both commercial objectives and broader strategic positioning in international markets.

Information Coordination Benefits:

- Consistent messaging across corporate communications

- Aligned narrative development with policy priorities

- Coordinated response to market developments

- Strategic timing of capacity announcements

- Integrated approach to stakeholder management

Strategic Decision-Making Alignment

The integration of Party governance structures into corporate decision-making processes creates mechanisms for coordinating commercial strategy with national industrial objectives. This enables synchronised capacity planning across multiple companies within the same strategic sector.

However, this concentration of control also creates potential vulnerabilities in global supply chains, as highlighted by recent analyses of critical mineral dependencies.

Governance Structure Impact: Chinese state-owned enterprises in strategic industries operate under policy frameworks that align commercial objectives with national security and foreign policy goals, representing a structural difference from Western corporate governance models.

How Do Process Innovations Strengthen China's Competitive Moat?

Technical breakthroughs in hydrometallurgical processing deliver compound competitive advantages that become increasingly difficult for international competitors to replicate. Process innovations by engineers like Hu Guangshou at Gansu Rare Earth Group demonstrate systematic investment in efficiency improvements across separation and refining operations.

Hydrometallurgy Advancement Impact

Recent innovations in rare earth separation processes focus on reducing chemical consumption while improving separation efficiency and product purity. These improvements include enhanced calcium-ion removal, suppression of tetravalent cerium interference, and optimisation of acid and alkali usage in extraction processes.

Process Optimisation Results:

- Reduced acid and alkali consumption in separation

- Improved efficiency in calcium-ion removal processes

- Enhanced separation selectivity between similar elements

- Upgraded extraction line capacity to 11,000 tons annually

- Minimised chemical waste generation

Innovation Ecosystem Development

Recognition of technical achievements through state media channels signals systematic investment in process innovation within China's rare earth industry. This approach ensures continuous improvement in manufacturing efficiency while maintaining technological leadership in critical processing stages.

The concentration of technical expertise within integrated industrial clusters enables rapid diffusion of innovations across multiple processing facilities. Knowledge transfer between research institutions, engineering teams, and production facilities accelerates the implementation of efficiency improvements industry-wide.

Barriers to Entry Reinforcement

Each incremental process improvement raises technical and financial barriers for potential competitors seeking to establish alternative rare earth processing capacity. The combination of scale advantages, process expertise, and integrated supply chains creates increasingly formidable obstacles for new entrants.

Competitive Barrier Categories:

- Technical knowledge requirements for efficient separation processes

- Capital investment thresholds for competitive-scale facilities

- Environmental compliance and waste management capabilities

- Quality control systems for consistent product specifications

- Integrated logistics and inventory management systems

What Does This Mean for Western Supply Chain Diversification Efforts?

Current developments in Chinese rare earth capacity suggest that competitive gaps between Chinese and international suppliers may be widening rather than narrowing. While Western initiatives focus primarily on mining development and basic processing, China continues advancing in higher-value separation, refining, and manufacturing segments.

Furthermore, European efforts to establish an European CRM facility face significant challenges in competing with established Chinese processing capabilities and expertise.

Alternative Capacity Development Challenges

Western Rare Earth Processing Status:

- United States: Minimal domestic separation capacity; MP Materials operates primary mining facility at Mountain Pass, California

- Australia/Malaysia: Lynas Rare Earths produces approximately 10,000-12,000 tons of rare earth hydroxide concentrate annually

- Europe: Critical Raw Materials Act launched but commercial-scale production not yet operational

- Canada: Several development projects but limited operational separation capacity

The technical complexity and capital requirements for competitive rare earth separation facilities exceed initial projections for Western supply chain development. Process optimisation, automation integration, and quality control systems require specialised expertise that takes years to develop independently.

Strategic Investment Priorities

Critical Areas Requiring Western Investment:

- Advanced separation and refining technologies

- Automated electrolysis and metal production systems

- Integrated magnet manufacturing capabilities

- Specialised alloy production facilities

- Quality control and process optimisation systems

Timeline and Resource Implications

The scale and sophistication of ongoing China Northern Rare Earth capacity expansion indicates that meaningful Western supply chain alternatives will require substantially longer development timelines and higher capital investments than previously anticipated. Process expertise, automation capabilities, and quality control systems represent significant technical barriers.

Development Timeline Challenges:

- Environmental permitting and regulatory approval processes

- Technical expertise development and training requirements

- Capital equipment procurement and facility construction

- Process optimisation and quality certification

- Market development and customer qualification

The next major ASX story will hit our subscribers first

How Will Market Dynamics Shift in Response to Increased Capacity?

Expanded processing capacity provides greater flexibility for strategic pricing policies that can influence international investment decisions in competing projects. The ability to temporarily adjust pricing while maintaining long-term profitability through volume advantages represents a significant strategic tool.

In addition, analysis shows that China's dominance in critical mineral refining is likely to continue through 2030, reinforcing current market positioning.

Pricing Strategy Implications

Strategic Pricing Capabilities:

- Volume-based cost advantages enabling competitive pricing

- Ability to adjust pricing in response to alternative supply development

- Coordination across multiple processing facilities for market influence

- Integration with downstream manufacturing for value optimisation

- Flexible response to demand variations across different applications

Customer Relationship Deepening

Increased production capacity enables more attractive supply terms for international customers, potentially deepening dependency relationships with manufacturers requiring consistent rare earth metal supplies. Long-term contracts and integrated logistics can create switching costs that discourage customer diversification efforts.

Customer Dependency Factors:

- Consistent product quality and specification compliance

- Reliable delivery schedules and inventory management

- Competitive pricing relative to alternative suppliers

- Technical support and application development assistance

- Integrated logistics and supply chain coordination

Market Concentration Trajectory

Current Market Control Indicators:

- China accounts for approximately 70% of global rare earth processing

- Limited alternative suppliers with competitive scale and efficiency

- High technical and financial barriers to new capacity development

- Integrated supply chains from mining through manufacturing

- Coordinated capacity planning across multiple facilities

What Strategic Scenarios Should International Stakeholders Consider?

Understanding potential future developments requires analysis of multiple scenarios based on current capacity expansion trends, technological advancement patterns, and geopolitical considerations affecting rare earth supply chains.

Scenario 1: Accelerated Market Consolidation

Continued capacity expansion combined with strategic pricing coordination could effectively eliminate most international competition within strategic planning horizons. This scenario would create comprehensive dependency on Chinese suppliers for materials essential to renewable energy, electric vehicles, and defence applications.

Consolidation Indicators:

- Sustained investment in processing capacity expansion

- Coordinated pricing policies across multiple producers

- Technical advancement pace exceeding international competition

- Integration of downstream manufacturing capabilities

- Policy coordination supporting strategic objectives

Scenario 2: Selective Supply Management

Expanded capacity could enable differentiated supply policies that provide reliable access to cooperative partners while creating constraints for strategic competitors. This approach would maximise geopolitical leverage while minimising broad economic disruption.

Selective Management Characteristics:

- Preferential pricing and contract terms for allied countries

- Priority allocation during supply constraint periods

- Coordinated export policies supporting foreign policy objectives

- Technical assistance and joint venture opportunities

- Long-term partnership development with strategic customers

Scenario 3: Technology Transfer Leverage

Market dominance could enable demands for technology transfers or joint venture arrangements as conditions for continued supply access. International companies might face difficult decisions between market access and intellectual property protection.

Risk Mitigation Strategies

Recommended Approaches for International Stakeholders:

- Accelerated alternative supply development: Increase investment in Western separation and processing capacity

- Strategic material stockpiling: Build strategic reserves of critical rare earth materials

- Technology development partnerships: Collaborate with allied nations on processing innovation

- Diplomatic engagement frameworks: Establish supply security agreements and coordination mechanisms

- Circular economy investment: Develop recycling and material recovery capabilities

Financial and Timeline Considerations:

- Alternative supply chains require 5-10 year development timelines

- Capital investments may exceed $1 billion for competitive-scale facilities

- Technical expertise development requires sustained multi-year programmes

- Environmental compliance adds complexity and approval timeline extensions

- Market development requires customer qualification and certification processes

The strategic implications of current rare earth market developments extend beyond commercial competition to encompass national security considerations for countries dependent on rare earth-intensive technologies. Policymakers must recognise that evolving market dynamics could create dependencies that constrain future strategic options across multiple critical industries.

Understanding these dynamics requires comprehensive analysis of technical capabilities, capacity development timelines, and geopolitical factors affecting long-term supply security. The window for establishing meaningful alternative suppliers continues to narrow as technological and scale advantages expand within existing supply chain structures.

Ready to Capitalise on Critical Materials Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in critical materials before they reach broader market awareness. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 30-day free trial today to position yourself ahead of evolving market dynamics.