June 13, 2026

Strategic Mineral Classification and Geopolitical Dependencies

Western governments increasingly recognise that traditional market-based approaches to resource security prove inadequate when facing concentrated supply chains controlled by geopolitical competitors. Antimony's classification as a strategic critical mineral reflects this strategic recalibration, acknowledging that certain materials require government intervention to ensure consistent availability for defence and technological applications.

Global antimony production concentrates primarily in three nations: China, Russia, and Tajikistan. According to the U.S. Geological Survey's 2024 Mineral Commodity Summaries, China maintains dominant market position through both mining and refining operations, particularly concentrated in Hunan Province. This geographic concentration creates systemic vulnerabilities in Western supply chains, as disruptions in any single region can cascade through multiple downstream applications.

The strategic importance extends beyond mere supply statistics. Furthermore, antimony serves critical functions in several key areas:

- Defence Systems: Armour-piercing ammunition components, night vision equipment, and targeting systems

- Nuclear Infrastructure: Specialised applications in nuclear weapons and reactor systems

- Technological Applications: Semiconductor manufacturing, flame retardants, and energy storage systems

- Industrial Processes: Lead-acid battery production, plastics manufacturing, and glass production

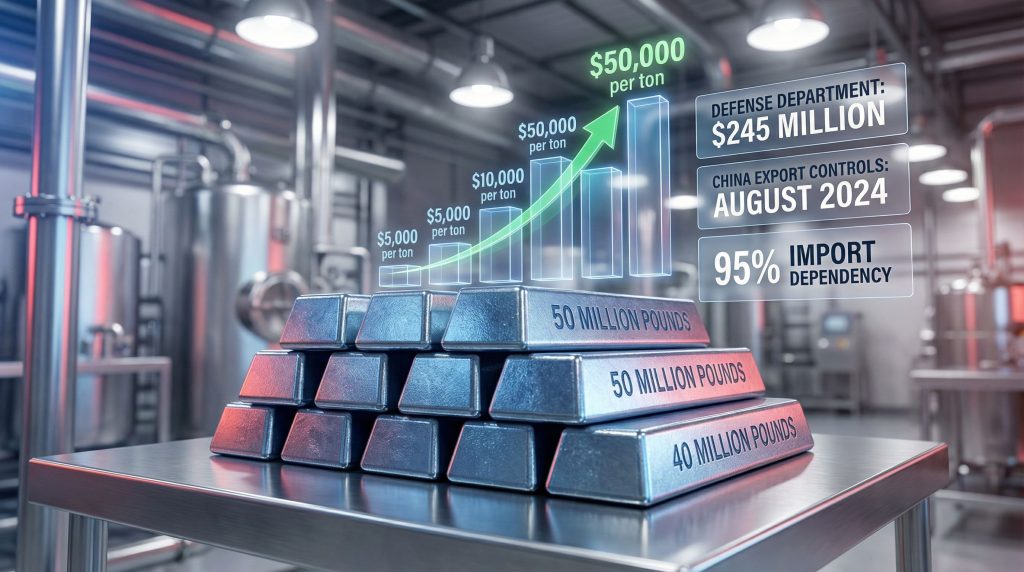

Current U.S. import dependency exceeds 95% according to USGS assessments, with minimal domestic production limited to by-product recovery from copper and silver operations. This dependency structure becomes particularly concerning given antimony's dual-use nature, where civilian industrial demand competes directly with defence requirements during supply constraints.

When big ASX news breaks, our subscribers know first

Federal Stockpiling and Strategic Procurement Programs

The Biden administration's commitment to critical mineral supply security includes substantial funding allocations designed to rebuild domestic processing capacity and establish strategic reserves. While specific antimony procurement targets require verification through official Department of Defence sources, industry discussions suggest federal requirements spanning both domestic consumption and allied nation support.

The strategic stockpiling framework creates what economists classify as inelastic demand – government procurement that continues regardless of price fluctuations. In addition, this demand structure differs fundamentally from industrial consumption patterns, as defence-related purchases prioritise availability over cost optimisation. Such procurement creates pricing floors unavailable in traditional commodity markets.

Recent policy developments, including the critical minerals order and US mineral production order, have reinforced government commitment to domestic supply chain development. These measures complement broader initiatives like Australia's strategic reserve program to strengthen allied supply relationships.

Federal support mechanisms include:

Direct Procurement Programs:

- Defence Logistics Agency purchasing agreements

- Strategic National Stockpile accumulation targets

- Cost-plus pricing arrangements for qualified suppliers

- Premium pricing for defence-grade specifications

Development Incentives:

- Department of Energy loan guarantee programmes

- Critical mineral production tax incentives

- Expedited permitting for strategic projects

- Research and development grants for processing technology

The absence of U.S. antimony processing facilities since 1942 represents an 82-year gap in domestic refining capability. Consequently, this infrastructure deficit cannot be rapidly addressed through market mechanisms alone, requiring sustained government support to rebuild essential processing knowledge and equipment capacity.

Supply Chain Weaponisation and Market Response

China's implementation of export controls on strategic minerals demonstrates how quickly resource access can become geopolitical leverage. These restrictions create immediate supply disruptions that cascade through dependent industries, forcing importing nations to rapidly develop alternative sources regardless of cost considerations.

Recent export control implementations have highlighted vulnerabilities in Western antimony supply chains. While specific pricing data requires verification through commodity trading databases, industry reports suggest significant price volatility following restriction announcements. Such volatility reflects both immediate supply constraints and longer-term concerns about reliable access to essential materials.

However, the market response reveals several critical dynamics:

Immediate Effects:

- Spot price volatility and premium expansion

- Contract renegotiation and supply agreement reviews

- Inventory accumulation by strategic users

- Alternative source evaluation and qualification

Longer-term Adaptations:

- Domestic processing capacity development

- Allied nation supply agreement negotiations

- Technology transfer and knowledge acquisition

- Strategic reserve accumulation programmes

These supply disruptions accelerate government intervention in markets previously left to private sector mechanisms. The transition from market-based sourcing to strategic procurement represents a fundamental shift in how critical minerals are valued and allocated within Western economies.

By-Product Economics and Operational Leverage

Antimony as a strategic critical mineral emerges as a valuable by-product that creates distinctive economic advantages not available to primary metal producers. Most North American antimony occurs alongside silver, lead, or gold deposits, enabling miners to allocate primary costs to precious metals while capturing incremental antimony value with minimal additional operating expenses.

This cost structure generates exceptional operational leverage when antimony prices increase. Since mining and milling expenses are allocated to primary metal recovery, antimony price improvements translate directly to margin expansion without proportional cost increases. Furthermore, this leverage effect becomes particularly valuable during periods of supply constraint when antimony commands premium pricing.

By-Product Advantage Analysis:

| Cost Category | Primary Metal Allocation | Antimony Incremental Cost |

|---|---|---|

| Mining Operations | 100% allocated to silver/gold | Minimal additional extraction |

| Milling and Processing | Primary metal recovery costs | Incremental separation costs |

| Labour and Infrastructure | Existing operation support | Limited additional personnel |

| Environmental and Permitting | Covered under existing permits | Modification costs only |

The operational leverage extends beyond basic production economics. By-product antimony operations can scale output through processing improvements without requiring additional mine development or permitting. This scalability provides rapid response capability to demand increases while maintaining low marginal cost structures.

Current production from existing operations provides immediate feed streams for downstream processing without ramp-up delays. For instance, the Galena Complex generates substantial antimony content as a by-product of silver recovery, creating an established foundation for expanded processing operations.

Vertical Integration and Value Capture Strategies

Traditional antimony marketing through concentrate sales to foreign smelters typically results in significant value leakage through processing penalties and transportation costs. Concentrate sales often realise only 60-80% of spot pricing due to smelter charges, quality penalties, and logistical constraints.

Domestic refining eliminates these penalties while capturing downstream processing margins. Vertical integration from mine to finished metal enables producers to realise full market pricing plus processing premiums, creating substantial value enhancement compared to concentrate marketing strategies.

Value Realisation Comparison:

- Traditional Concentrate Sales: 60-80% of spot antimony pricing

- Domestic Refining Operations: 100% of market price plus processing margins

- Government Contract Sales: Market pricing plus cost-plus premiums

- Strategic Stockpile Purchases: Premium pricing above commodity rates

The scarcity of domestic antimony refining creates significant barriers to entry for new processing operations. Established facilities command premium positions through existing customer relationships, technical expertise, and regulatory approvals. These competitive advantages become particularly valuable when government procurement prioritises domestic supply sources.

Joint venture structures enable mining companies to access specialised refining expertise while maintaining majority economic interest in their antimony streams. Such partnerships distribute technical risk while preserving upside participation in antimony value creation.

Joint Venture Models and Risk Distribution

Complex antimony processing requirements favour partnership structures that combine mining assets with technical refining capability. These joint ventures enable resource companies to access specialised metallurgical knowledge while maintaining control over their mineral feed streams and economic upside.

Successful antimony joint ventures typically incorporate several key elements:

Feed Supply Security:

- Long-term concentrate availability from controlled mining operations

- Predictable antimony grades and metallurgical characteristics

- Expansion potential through additional mineral resources

- Protection against supply disruption from external sources

Technical Capabilities:

- Proven antimony refining experience and equipment

- Quality control systems meeting defence specifications

- Environmental compliance and regulatory expertise

- Continuous improvement and process optimisation capacity

Market Access:

- Existing government contractor relationships and qualifications

- Established customer base and sales channels

- Strategic positioning within domestic supply chains

- Ability to capture premium pricing for specialised products

The governance structure of such partnerships requires careful balance between operational control and economic participation. Successful models often feature mining companies retaining majority economic interest while technical partners provide specialised expertise and market access.

Third-party processing capabilities create additional revenue streams beyond internal production. Facilities designed with surplus capacity can process concentrate from other domestic or allied sources, generating toll-processing revenue that scales returns without additional mining investment.

The next major ASX story will hit our subscribers first

Policy-Driven Demand and Investment Risk Profiles

The strategic classification of antimony as a strategic critical mineral creates fundamentally different risk-return profiles compared to traditional commodity investments. Government procurement operates independently of economic cycles, providing recession-resistant demand that supports pricing during broader market downturns.

Non-Cyclical Demand Characteristics:

- Defence Spending Stability: Military procurement continues regardless of economic conditions

- Strategic Reserve Building: Government stockpiling creates sustained demand periods

- Allied Nation Requirements: International cooperation agreements extend demand beyond domestic needs

- Premium Pricing: National security considerations support pricing above industrial commodity rates

This demand structure provides unusual visibility and predictability for mining investments. Multi-year government contracts offer revenue certainty unavailable in volatile commodity markets, while cost-plus pricing arrangements protect producers from input cost inflation.

The broader critical minerals strategy provides additional context for understanding how government support mechanisms are evolving. These programmes create comprehensive frameworks for supply chain development that extend beyond immediate procurement needs.

Critical mineral support programmes provide additional risk mitigation:

Federal Programme Benefits:

- Department of Energy loan guarantees for processing facility development

- Tax incentives including accelerated depreciation and production credits

- Expedited permitting processes for strategically important projects

- Technical assistance and research support for process optimisation

Technical Processing and Infrastructure Risks

Antimony refining requires specialised technical knowledge and equipment not commonly available in traditional mining operations. The metallurgical complexity creates execution risks that must be carefully managed through appropriate partnership structures and technical expertise acquisition.

Processing Risk Factors:

- Metallurgical Complexity: Antimony chemistry requires specialised separation and purification techniques

- Equipment Sourcing: Limited global suppliers for antimony-specific refining equipment

- Environmental Compliance: Strict regulations governing antimony processing and waste management

- Quality Standards: Defence applications require precise purity specifications and quality control

The 82-year gap in U.S. antimony processing represents significant knowledge transfer requirements. Rebuilding processing expertise involves both equipment procurement and technical skill development, requiring sustained investment and patience during learning curve periods.

Environmental permitting for antimony processing involves complex regulatory frameworks addressing air emissions, water treatment, and waste disposal. However, these requirements extend development timelines and increase capital costs, but also create barriers to entry that protect established operations.

According to industry analysis, Australia's antimony boom demonstrates how countries can rapidly develop domestic processing capabilities when strategic priorities align with market opportunities.

Market Development and Infrastructure Timeline

The transition from import dependency to domestic supply security requires substantial infrastructure development spanning multiple years. Realistic timeline expectations include permitting, construction, commissioning, and market penetration phases that cannot be compressed through additional capital alone.

Development Phase Timeline:

Engineering and Permitting (12-18 months):

- Process design and equipment specification

- Environmental impact assessment and permitting

- Site preparation and construction planning

- Contractor selection and project management setup

Construction and Installation (18-24 months):

- Facility construction and equipment installation

- Utility infrastructure and support systems

- Testing and commissioning of processing systems

- Worker training and operational procedure development

Market Integration (6-12 months):

- Customer qualification and contract negotiation

- Product specification validation and quality certification

- Supply chain integration and logistics optimisation

- Production scaling and efficiency improvement

The extended development timeline requires patient capital and realistic expectation setting. Successful projects balance rapid progress with thorough execution, avoiding shortcuts that compromise long-term operational capability.

Consequently, companies must plan for significant upfront investment periods before achieving commercial production. This timeline consideration becomes critical when evaluating project financing requirements and investor expectations.

Strategic Investment Framework and Performance Metrics

Evaluating antimony investments requires modified analytical frameworks that account for strategic value beyond traditional mining metrics. Policy-driven demand creates non-standard risk-return profiles that justify different valuation approaches and performance expectations.

Research indicates that antimony's role in defence applications creates particularly compelling investment dynamics when combined with government support programmes.

Primary Investment Evaluation Criteria:

Resource Base Assessment:

- Antimony resource quantity and grade consistency

- Mine life and expansion potential

- By-product synergies and cost allocation benefits

- Metallurgical characteristics and processing requirements

Strategic Positioning Analysis:

- Domestic supply chain integration potential

- Government relationship development and contractor qualification

- Processing capability and vertical integration opportunities

- Allied nation market access and international cooperation potential

Financial Structure Optimisation:

- Capital efficiency and development cost management

- Government support programme access and utilisation

- Revenue diversification through multiple product streams

- Risk mitigation through appropriate partnership structures

The investment thesis centres on policy-driven transformation of antimony from industrial commodity to strategic resource. This transformation creates unique opportunities for appropriately positioned companies but requires careful evaluation of execution capabilities and market development timelines.

What Are Risk-Adjusted Return Considerations?

Successful antimony investments balance substantial upside potential against technical execution challenges and extended development timelines. The strategic nature of demand provides unusual downside protection, while supply constraints and government support create exceptional upside scenarios.

Investment success likely requires diversified exposure across multiple value chain segments rather than concentrated bets on single assets or companies. The complexity of antimony processing and marketing favours experienced operators with established technical capabilities and government relationships.

For instance, strategic partnerships between mining companies and processing specialists create risk distribution while preserving upside participation. These structures enable investors to participate in antimony's strategic value creation without accepting full technical execution risk.

The critical mineral classification of antimony as a strategic critical mineral suggests long-term government support for domestic processing development. This support creates investment opportunities with risk-return profiles distinct from traditional mining sector investments, justifying specialised analytical approaches and patient capital deployment strategies.

Furthermore, the evolving geopolitical landscape reinforces antimony's strategic importance, creating sustained demand drivers that operate independently of traditional commodity cycles. This unique market structure provides compelling opportunities for appropriately positioned investors willing to navigate the technical and regulatory complexities of strategic mineral development.

Ready to Capitalise on Strategic Mineral Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in strategic commodities like antimony ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage in the evolving critical minerals landscape.