July 31, 2026

Strategic Positioning Within Chile's Evolving Lithium Framework

Chile's lithium sector experienced three decades of concentrated development around the Salar de Atacama, with SQM and Albemarle controlling approximately 95% of national production capacity as of 2023. This operational duopoly generated substantial revenues but limited exploration of alternative deposits and processing methodologies across Chile's northern regions. The absence of major greenfield lithium developments since the mid-1990s created a strategic vulnerability as competing jurisdictions expanded their productive capacity.

Furthermore, the emergence of argentina lithium brine insights illustrates this competitive pressure. The neighbouring country increased output from minimal levels in 2010 to approximately 110,000 tonnes lithium carbonate equivalent in 2023, with industry projections indicating potential capacity of 300,000+ tonnes by 2030. Projects like Olaroz-Cauchari and Fenix brought new productive capacity online whilst demonstrating alternative approaches to lithium extraction in high-altitude brine environments.

In addition, australia lithium innovations through hard-rock spodumene operations, particularly the Greenbushes expansion, further diversified global lithium supply sources. This geographic distribution reduced Chile's strategic dominance despite maintaining substantial production volumes. The Chilean government recognised these competitive pressures and initiated regulatory reforms to attract investment whilst capturing greater state revenues from lithium development.

Regulatory Innovation Through the CEOL Framework

The introduction of Chile's Special Lithium Operating Contract (Contrato Especial de Operación de Litio) framework in 2023 represented a fundamental shift from traditional concession-based mining development. The CEOL structure provides 40-year operational terms with standardised fiscal arrangements, replacing the individual concession negotiations that previously deterred large-scale international investment.

Under the CEOL framework, lithium royalties are established at 5% with an additional 14% royalty on potassium byproducts. This compares favourably to standard mining royalties of 5-14% depending on project profitability, providing clarity for long-term investment planning. The contracts specify operational requirements, production targets, environmental compliance metrics, and workforce development obligations whilst maintaining state oversight through contractual partnerships.

The Laguna Verde lithium project in Chile represents the first major development approved under this reformed regulatory structure. This project serves as a reference case for evaluating the CEOL framework's effectiveness in attracting strategic investment whilst balancing state revenue objectives. The framework's success could influence similar regulatory approaches across Latin America's lithium-producing regions.

Industry analysts noted that Chile's CEOL approach attempts to balance investor certainty with state revenue capture, positioning itself between Bolivia's state-controlled model and purely private concession systems. The 40-year contract terms provide sufficient operational visibility for project financing whilst reducing regulatory uncertainty that previously complicated lithium development planning.

When big ASX news breaks, our subscribers know first

Advanced Processing Technologies and Economic Viability

Direct lithium extraction technologies have emerged as viable alternatives to traditional evaporation-pond methodologies, particularly for moderate-grade brine resources. These technologies employ solvent extraction or adsorption-based separation processes to concentrate lithium directly from brine solutions without requiring massive evaporation surface areas.

However, the implementation of geothermal lithium extraction techniques represents another innovative approach being explored globally. Furthermore, mining industry evolution has driven these technological advancements alongside environmental considerations.

Capital Investment Comparison

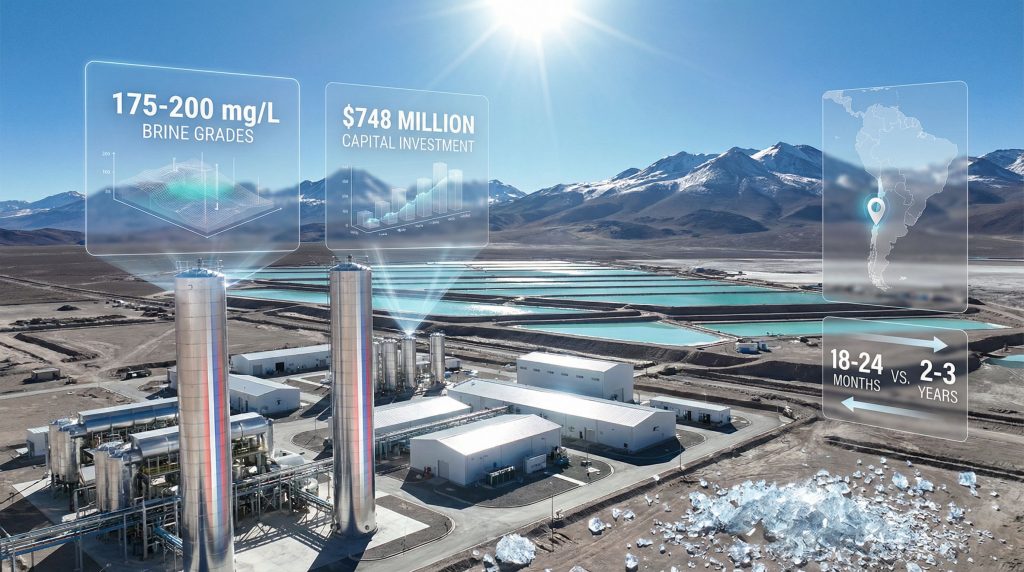

Traditional evaporation-pond operations require capital expenditures of $300-500 million for 15,000 tonnes per annum production capacity. DLE technologies demonstrate similar or slightly higher capital requirements ($400-700 million) but offer substantially reduced operational timelines to first production. The Laguna Verde lithium project in Chile's $748 million capital requirement falls within documented ranges for early-stage commercial DLE deployments.

Operational Timeline Advantages

Traditional evaporation ponds require 18-36 months from first brine processing to commercial production due to the time needed to establish stable evaporation and precipitation cycles. DLE processes can achieve commercial production in 12-18 months following processing equipment installation, providing earlier cashflow generation and reduced project risk exposure.

Water Consumption Reduction

Environmental considerations increasingly influence lithium extraction methodology selection. Evaporation-pond lithium operations in the Atacama region consume approximately 65 million cubic metres of water annually per 15,000 tpa production facility. DLE technologies typically reduce water consumption by 40-50%, requiring approximately 30-40 million cubic metres annually depending on specific process design.

This water efficiency provides regulatory advantages under Chile's increasingly stringent water-use regulations, particularly in the Atacama Region where prolonged drought conditions have intensified scrutiny of industrial water consumption. Additionally, renewable mining solutions are becoming essential for sustainable operations. DLE operators benefit from reduced regulatory compliance risk and potential operational cost advantages in water-constrained environments.

Brine Grade Economics and Processing Efficiency

The Laguna Verde lithium project in Chile features brine concentrations of 175-200 mg/L, positioning it within the moderate-grade category for global lithium brine resources. Understanding these grade implications requires benchmarking against established operations and economic thresholds.

| Project | Location | Grade (mg/L) | Processing Method | Status |

|---|---|---|---|---|

| Salar de Atacama | Chile | 1,500-1,800 | Evaporation | Operating |

| Salar de Olaroz | Argentina | 650-750 | Evaporation | Operating |

| Clayton Valley | USA | 200-350 | DLE Development | Development |

| Laguna Verde | Chile | 175-200 | DLE | Development |

| Maricunga | Chile | 300-400 | Various | Exploration |

Hydrometallurgists observe that moderate-grade brines represent optimal conditions for DLE technologies because traditional evaporation methods become increasingly uneconomical at these concentrations. At 175-200 mg/L grades, processing one tonne of brine yields approximately 0.175-0.20 kg of lithium carbonate equivalent. For a 15,000 tpa production target, approximately 75-85 million tonnes of brine must be processed annually.

Processing Cost Implications

Industry data indicates that for every 100 mg/L decrease in brine grade, processing costs increase by approximately 8-12% per unit of lithium produced using conventional evaporation methods. DLE technologies demonstrate lower sensitivity to grade variations, with cost increases of only 3-5% per 100 mg/L decrease, justifying higher capital expenditure at moderate grades.

At the Laguna Verde lithium project grade range, DLE technology can achieve 70-80% lithium extraction efficiency compared to 50-70% for evaporation methods. This efficiency differential supports the economic viability of DLE deployment despite higher initial capital requirements.

Financial Structure and Investment Considerations

The $748 million capital requirement for the Laguna Verde lithium project in Chile represents mid-tier scale within current lithium market context. Projects in the $500-1,000 million capital expenditure range typically employ balanced debt-to-equity structures optimised for long-term operational stability and acceptable investor returns.

Typical Financing Architecture

Recent lithium project financings demonstrate debt-to-equity ratios ranging from 1:1 to 1.5:1, with senior debt comprising $400-600 million of total capital expenditure and equity accounting for $300-400 million. The 25-year operational timeline provides sufficient cashflow visibility to support long-term debt structures, with typical debt tenors of 10-12 years representing approximately 40-50% of project operational life.

Strategic Investor Categories

Lithium projects have attracted diversified capital sources reflecting the mineral's critical status in energy transition supply chains:

• Battery manufacturers seeking secure feedstock supply arrangements

• Automotive OEMs pursuing vertical integration strategies

• Infrastructure funds targeting critical mineral exposure

• Mining majors expanding portfolio diversification

• Government-backed investment vehicles supporting supply chain security

Risk Assessment Framework

Investment considerations for the Laguna Verde lithium project in Chile include regulatory stability under Chile's evolving lithium policy, DLE technology scalability risks, and competitive positioning against lower-cost operations in Argentina and Australia. The 40-year CEOL framework provides operational certainty whilst requiring careful evaluation of fiscal terms relative to alternative jurisdictions.

Key investment risk factors include technology deployment at commercial scale, brine chemistry variability, equipment durability in harsh desert conditions, and long-term lithium price volatility. The project's moderate-grade resource requires advanced processing technology validation to ensure consistent production economics.

Operating Cost Structure

DLE operations typically demonstrate higher operating expenditure ($4,000-6,000 per tonne lithium) compared to mature evaporation operations ($2,500-4,000 per tonne), reflecting increased processing complexity and chemical consumption. However, DLE's reduced water requirements and faster production ramp-up can offset these cost differentials through operational risk reduction and earlier revenue generation.

Environmental Advantages and Regulatory Compliance

Water resource management represents a critical consideration for lithium extraction operations in Chile's hyperarid northern regions. The Atacama Desert experiences average annual precipitation of less than 1mm, making water conservation essential for sustainable industrial operations and community relationships.

Comparative Environmental Impact

Traditional evaporation-pond lithium extraction requires massive surface areas and extended brine exposure periods, resulting in significant evaporation losses beyond productive water consumption. DLE technologies employ closed-loop processing systems that minimise brine exposure and reduce overall water consumption per unit of lithium production.

Environmental scientists note that whilst DLE technologies reduce water consumption, they introduce considerations including chemical usage, brine chemistry management, and equipment maintenance in extreme environmental conditions. These factors require ongoing technological refinement and environmental monitoring to ensure sustainable operations.

Community Relations and Social Licence

Lithium development in Chile's northern regions involves complex relationships with indigenous communities and local stakeholders concerned about water resource impacts. The Laguna Verde lithium project's location along the Highway 31 corridor provides infrastructure advantages whilst requiring careful community engagement to maintain social licence for operations.

Socioeconomic benefits for the Atacama Region include employment opportunities, infrastructure development, and local supplier engagement. The project's advanced technology profile may support higher-skilled employment compared to traditional mining operations, potentially providing additional community benefits.

Global Supply Chain Positioning and Strategic Value

The Laguna Verde lithium project in Chile's development timeline aligns with anticipated demand growth cycles for electric vehicle battery materials. Industry projections indicate substantial lithium demand increases through 2030-2035 as automotive electrification accelerates globally and stationary energy storage deployments expand.

Geopolitical Supply Chain Considerations

Chile's lithium resources provide strategic value for North American and European battery manufacturers seeking supply chain diversification away from Chinese processing dominance. The country's established mining infrastructure, regulatory frameworks, and trade relationships support long-term partnership development with consuming regions prioritising supply security.

Market Timing and Demand Alignment

Electric vehicle adoption projections suggest continued lithium demand growth through the 2030s, with potential production from the Laguna Verde project aligned with this demand trajectory. However, lithium markets demonstrate significant price volatility influenced by technology developments, competing supply sources, and macroeconomic factors affecting automotive and energy storage sectors.

Technology Transfer and Industry Development

Successful deployment of DLE technology at commercial scale could influence broader Chilean lithium sector development. The project's technological demonstration may support additional CEOL contract awards and encourage further exploration of moderate-grade brine resources across Chile's northern regions.

The next major ASX story will hit our subscribers first

What Are the Scenario Analysis and Strategic Implications?

The Laguna Verde lithium project's development trajectory will significantly influence Chile's competitive position within global lithium markets whilst establishing precedents for future resource development under the CEOL framework.

Success Scenario Outcomes

Project success could validate Chile's reformed regulatory approach and demonstrate DLE technology's commercial viability at scale. This validation might encourage additional international investment in Chilean lithium resources and support technology transfer initiatives benefiting the broader mining sector.

Successful operations could also strengthen Chile's position in global critical minerals competition whilst providing reference case data for evaluating additional CEOL contract applications. Furthermore, the project's environmental performance metrics will influence regulatory standards and community acceptance for future lithium developments.

Development Delay Considerations

Potential project delays could impact Chile's lithium market share as competing jurisdictions advance their production capacity. Argentina and Australia continue expanding their lithium output, potentially capturing market share during periods of Chilean production stagnation.

Regulatory framework adjustments might become necessary if initial CEOL implementations encounter unexpected challenges. Investor confidence in Chile's lithium sector could be affected by project execution difficulties or technological deployment issues at commercial scale.

Alternative Development Pathways

The Chilean government maintains flexibility to modify CEOL terms or consider alternative development models based on initial project outcomes. State partnership approaches, similar to those employed in copper mining, represent potential alternatives if private investment models prove insufficient for lithium sector development objectives.

Consequently, the project's projected value of $1.37 billion demonstrates significant economic potential for Chile's lithium sector. The Laguna Verde lithium project in Chile represents a critical test case for advanced lithium extraction technologies and reformed regulatory frameworks in South America's most established mining jurisdiction.

Its development success or challenges will influence regional lithium development strategies, investor confidence in DLE technologies, and Chile's competitive positioning within global critical mineral supply chains through 2030 and beyond.

Investment in lithium projects involves significant risks including commodity price volatility, technological uncertainties, regulatory changes, and operational challenges. Potential investors should conduct thorough due diligence and consider professional financial advice before making investment decisions.

Are You Positioning for the Next Lithium Discovery?

Discovery Alert's proprietary Discovery IQ model instantly identifies significant lithium and mineral discoveries across the Australian Stock Exchange, providing subscribers with actionable insights ahead of broader market awareness. Explore how major mineral discoveries can generate exceptional returns and begin your 14-day free trial today to secure your competitive advantage in the rapidly evolving critical minerals sector.