June 17, 2026

Global supply chain dynamics for critical minerals have fundamentally shifted from cost optimisation toward security prioritisation, creating unprecedented opportunities for strategic infrastructure development outside traditional manufacturing centers. This transformation represents more than temporary market adjustment; it signals permanent recalibration of how nations approach resource security in an increasingly multipolar world.

Industrial policy frameworks now prioritise supply chain resilience over pure economic efficiency, establishing new valuation metrics where security premiums justify production costs multiples higher than historical benchmarks. Ex-China rare earth supply chains exemplify this strategic pivot, as governments deploy unprecedented capital to establish processing capabilities that ensure access to materials essential for defence systems, renewable energy infrastructure, and advanced manufacturing technologies.

What Drives the Strategic Imperative for Ex-China Rare Earth Diversification?

The Geopolitical Risk Matrix

Export control mechanisms have evolved into strategic economic tools, creating supply vulnerability scenarios that extend far beyond traditional trade disputes. China maintains control over approximately 80% of global rare earth refining capacity and 90% of magnet manufacturing worldwide, positioning these materials as potential leverage points in geopolitical negotiations. Recent tightening of export licensing restrictions has demonstrated how quickly supply accessibility can shift, forcing downstream manufacturers to recalculate their procurement strategies entirely.

Technology transfer restrictions compound these supply risks by limiting Western access to specialised processing knowledge accumulated over decades of industrial development. These constraints create dual vulnerabilities: immediate supply disruption risks and longer-term technological dependence that prevents indigenous capability development. Furthermore, the combination forces strategic planners to consider scenarios where cost considerations become secondary to supply security.

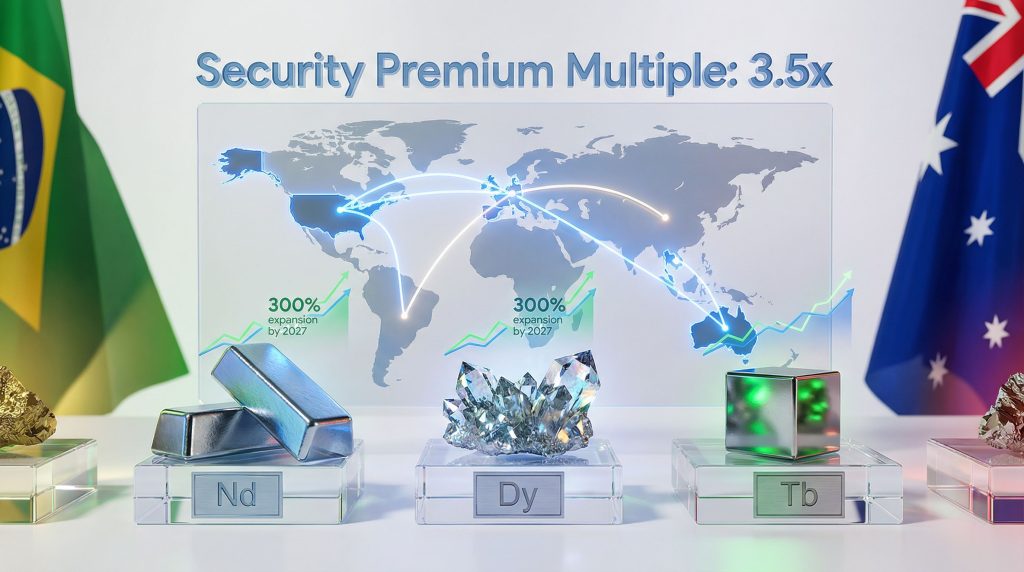

Price volatility mechanisms emerging from these dynamics reveal the true cost of supply concentration. Dysprosium oxide pricing illustrates this transformation starkly: Rotterdam markets price this critical heavy rare earth element at $900 per kilogram while Chinese domestic markets maintain $255 per kilogram pricing. This 3.5x security premium reflects not temporary market distortion but permanent structural repricing for supply reliability.

Economic Security Calculations

Cost-plus pricing structures represent fundamental departure from commodity market dynamics, establishing new frameworks where buyers pay production costs plus negotiated margins rather than accepting spot market volatility. These arrangements transfer price risk from producers to established buyers while guaranteeing revenue streams that enable project financing. In addition, long-term offtake contracts replacing spot market dependencies demonstrate buyer commitment to paying security premiums for reliable supply access.

Government subsidy requirements have become essential components of ex-China rare earth project viability rather than optional enhancement mechanisms. Federal funding programmes, loan guarantees, and strategic equity investments provide risk mitigation that private capital markets cannot replicate when evaluating projects competing against subsidised Chinese production. Security premium valuations reaching 250-350% above domestic Chinese prices require government backing to maintain commercial competitiveness.

National security implications across defence and clean energy sectors justify these economic premiums by quantifying the cost of supply disruption against infrastructure investment requirements. Defence applications for rare earth elements span from precision-guided munitions to advanced radar systems, while clean energy transition goals depend on rare earth permanent magnets for wind turbine generators and electric vehicle motors.

When big ASX news breaks, our subscribers know first

Which Regional Strategies Are Proving Most Effective for Supply Chain Resilience?

North American Industrial Policy Acceleration

Midstream processing breakthrough scenarios demonstrate how targeted investment can address the most critical supply chain gaps while building competitive advantages in specialised technologies. REAlloys' Saskatchewan facility expansion exemplifies this approach through focused heavy rare earth separation capacity targeting 300% expansion by 2027. The company's $21 million investment will increase dysprosium and terbium capacity approximately threefold while expanding neodymium-praseodymium capacity by 50%, with offtake agreements covering 80% of planned production volumes through cost-plus arrangements.

Key Infrastructure Developments:

• REAlloys Saskatchewan Expansion: Target production of 30 tonnes per year dysprosium oxide and 15 tonnes per year terbium oxide by early 2027

• HyProMag Texas Facility: Hydrogen Processing of Magnet Scrap technology achieving 90-100% recovery rates for critical elements, commissioning targeted for mid-2027

• Phoenix Tailings DOE Funding: $1.6 million ARPA-E funding for ligand-based extraction from wastewater and brines, projecting 200 tonnes annual rare earth refining capacity

• Ucore Rare Metals Louisiana Processing: $22.4 million DoD agreement supporting 2026 commercialisation of RapidSX solvent extraction technology

Magnet recycling infrastructure creates circular supply loops that reduce dependence on primary mining while establishing domestic manufacturing redundancy. However, with developments like the recent China battery recycling breakthrough, competition in this space is intensifying. HyProMag's Dallas-Fort Worth facility represents practical implementation of Hydrogen Processing of Magnet Scrap technology, which achieves 90-95% recovery efficiency for critical light and heavy rare earth elements from end-of-life magnets.

Technology innovation pathways emerging from federal funding programmes target non-traditional feedstock sources that could fundamentally expand supply base definitions. Phoenix Tailings' ligand-based extraction technology development targets wastewater, brines, and industrial waste streams as rare earth sources, potentially creating "mine-less" supply concepts that bypass traditional geological constraints. This approach could scale to thousands of tonnes annually while avoiding many environmental and permitting challenges associated with conventional mining operations.

Federal funding mechanisms de-risk private sector investments through structured support programmes that address multiple project development stages. The Department of Energy's ARPA-E programme provides research and development funding, while Department of Defence agreements offer commercialisation support and end-user demand certainty. For instance, the Trump critical minerals order has provided additional momentum to these initiatives.

European Strategic Autonomy Challenges

Policy framework evolution demonstrates European commitment to strategic autonomy while revealing execution challenges relative to North American programme velocity. The EU's RESourceEU initiative allocates €3 billion for strategic raw material projects, representing substantial government commitment to supply chain diversification. However, European industrial policy struggles to match North American subsidy intensity and deployment speed, creating competitive disadvantages in global project acquisition competitions.

Export restrictions on scrap materials prevent value leakage by retaining critical mineral feedstock within European processing ecosystems. Starting in 2026, the European CRM facility plans export restrictions on critical mineral-bearing scrap materials, designed to capture domestic rare earth value within EU borders rather than exporting raw materials for third-country processing.

European Competitive Positioning Challenges:

| Factor | European Performance | North American Performance |

|---|---|---|

| Subsidy Intensity | Moderate | High |

| Project Velocity | Constrained | Accelerating |

| Technology Access | Developing | Advanced |

| Feedstock Acquisition | Losing to Americans | Competitive Advantage |

Shared infrastructure models reduce individual project risks through open-access facilities that distribute capital requirements across multiple participants. This approach enables smaller companies to access commercial-grade processing capabilities without building bespoke pilot plants, potentially accelerating project development timelines. Regulatory harmonisation efforts aim to streamline environmental and permitting processes across EU member states, though implementation remains more complex than single-jurisdiction approaches used in North America.

Competitive positioning gaps become apparent in international project acquisition competitions, particularly in Latin American feedstock development opportunities. European companies reportedly lose deals to American competitors in Brazilian rare earth projects, suggesting that U.S. industrial policy provides more attractive terms for project developers and host governments.

What Processing Infrastructure Gaps Are Being Addressed Most Effectively?

Australia's National Infrastructure Strategy

Shared processing facility models represent innovative approaches to reducing individual project capital requirements while building national processing capabilities. The Australian Nuclear Science and Technology Organisation (ANSTO) is constructing Australia's first open-access rare earth processing facility specifically designed for clay-hosted deposits, scheduled for 2026 commissioning. This shared national infrastructure enables hydrometallurgical testwork standardisation across deposits while providing smaller companies access to commercial-grade processing capabilities.

Social licence challenges addressed through government backing demonstrate how national infrastructure strategies can overcome obstacles that individual projects cannot resolve independently. Australian Rare Earths' Koppamurra ionic adsorption clay project serves as the inaugural test case for ANSTO's shared facility, though the project remains early-stage and faces landholder opposition plus licensing gaps. Nevertheless, this situation illustrates how processing infrastructure can arrive before social licence and permitting approvals.

Technical risk distribution across multiple project participants reduces individual company exposure while building collective expertise in specialised processing technologies. Clay-hosted rare earth deposits require different processing approaches than conventional mineral ores, utilising ionic adsorption clay leaching with dilute acid solutions rather than traditional roasting and fusion methods. ANSTO's facility provides standardised processing pathways that reduce technical uncertainty for new projects while building Australian expertise in these specialised techniques.

Processing expertise concentrated in specialised facilities creates centres of excellence that can support multiple projects simultaneously. Rather than each junior mining company developing individual pilot plants, the shared facility model concentrates technical knowledge and equipment in a single location optimised for clay-hosted rare earth processing.

Southeast Asian Processing Hub Development

Malaysia's strategic positioning between competing geopolitical interests creates both opportunities and challenges for supply chain development. Japanese partnership frameworks through JOGMEC advance exploration and processing capabilities while positioning Malaysia as a potential processing hub for regional rare earth resources. However, Malaysia's contested geopolitical positioning between Chinese and Western interests creates uncertainty about long-term strategic alignment and technology access.

Existing processing infrastructure provides scale advantages that new facilities cannot immediately replicate, giving Southeast Asian locations competitive advantages in rapid capacity expansion scenarios. Malaysia's established rare earth processing capabilities, including Lynas Corporation's operations, provide technical expertise and infrastructure foundations that can support additional capacity development more rapidly than greenfield facilities in other regions.

Regional cooperation models emerging for technology transfer demonstrate how smaller nations can leverage partnerships to access specialised capabilities while maintaining strategic autonomy. Japan's JOGMEC collaboration with Malaysia exemplifies this approach, providing exploration technology and expertise in exchange for processing partnerships that secure Japanese access to rare earth materials outside Chinese control.

How Are Pricing Mechanisms Evolving Under Supply Chain Stress?

Security Premium Valuation Models

Heavy rare earth price divergence analysis reveals the scale of security premium valuations that have emerged from supply chain stress. Dysprosium oxide pricing demonstrates this divergence clearly: Chinese domestic markets maintain $255 per kilogram pricing while ex-China Rotterdam markets reach $900 per kilogram, creating a 3.5x security premium multiple. This pricing gap reflects not temporary market distortion but permanent structural repricing for supply reliability and geopolitical security.

Magnet manufacturing cost structures show even more dramatic pricing divergence, with ex-China magnet premiums reaching 2-4x domestic Chinese pricing levels. These premiums reflect the cumulative impact of rare earth feedstock costs, processing capabilities, and manufacturing expertise concentrated in Chinese supply chains. Consequently, Western magnet manufacturers face significant cost disadvantages that require either government subsidies or end-user acceptance of security premiums to maintain commercial viability.

Pricing Structure Analysis:

Heavy Rare Earth Security Premiums:

• Dysprosium Oxide: $900/kg (ex-China) vs $255/kg (China domestic)

• Security Multiple: 3.5x

• Terbium Oxide: Similar premium structures

• Magnet Products: 2-4x ex-China premiums

• Strategic Stockpile Valuations: Cost-plus agreements

Strategic stockpile valuations operate under cost-plus structures that eliminate commodity price volatility while providing producers with guaranteed revenue streams. These arrangements represent fundamental departures from commodity trading mechanisms, establishing pricing frameworks based on production costs plus negotiated margins rather than market-determined spot prices. Government-backed stockpiling programmes use these structures to build strategic reserves while supporting domestic production capabilities.

Contract Structure Innovation

Risk allocation mechanisms emerging in ex-China rare earth supply chains redistribute traditional commodity market risks between buyers and sellers through innovative contract structures. Cost-plus pricing eliminates commodity price volatility by basing payments on actual production costs plus fixed margins, transferring price risk from producers to buyers who value supply security over cost minimisation.

Security-premium components represent explicit compensation for supply reliability and geopolitical de-risking, separate from underlying commodity base pricing. These premiums acknowledge that ex-China production carries higher costs but provides strategic value that justifies premium pricing. Moreover, government backing reduces counterparty credit concerns while providing implicit guarantees that support long-term contract viability.

Take-or-pay agreements shift demand risk from suppliers to buyers by establishing minimum purchase commitments regardless of actual consumption requirements. These structures provide producers with revenue certainty that enables project financing while ensuring buyers maintain access to strategic materials during supply disruptions. Staged commissioning reduces execution risk exposure by allowing capacity additions in phases rather than requiring full-scale facility commissioning.

Long-term contract pricing provides cost certainty in volatile market environments while establishing strategic partnerships between suppliers and end-users. These agreements often extend 5-10 years or longer, providing both parties with predictable cash flows and supply access.

Which Emerging Supply Sources Show Greatest Strategic Promise?

Latin American Feedstock Development

Brazilian project acquisition activity accelerates as companies recognise the strategic value of securing future feedstock optionality outside Chinese influence. Power Minerals completed acquisition of the Santa Ana carbonatite rare earth project, while Core Energy Minerals signed binding agreements to acquire the Itambé project in Bahia. These early-stage acquisitions represent strategic positioning for future supply development rather than immediate production capabilities.

American investors outcompeting European counterparts in Brazilian rare earth project acquisitions demonstrates the effectiveness of U.S. industrial policy support mechanisms. The ongoing US-China trade tensions have amplified this dynamic, with American companies benefiting from government backing, federal funding programmes, and strategic partnership opportunities that provide competitive advantages in international project competitions.

Carbonatite rare earth project consolidation provides access to deposits with different geological characteristics than Chinese ionic clay sources, potentially offering processing advantages and supply diversification benefits. Carbonatite-hosted rare earth deposits typically contain different element distributions than ionic adsorption clays, potentially providing better access to light rare earth elements needed for magnet manufacturing while reducing dependence on Chinese heavy rare earth sources.

Early-stage optionality building creates future supply flexibility by securing rights to develop projects when market conditions and processing infrastructure reach commercial viability thresholds. Companies acquiring Brazilian projects today position themselves for development opportunities over 3-5 year timelines, when ex-China processing infrastructure and market demand reach levels that justify commercial production investments.

Chilean Heavy Rare Earth Potential

Ionic adsorption clay deposits in Chile offer processing advantages similar to Chinese sources while providing Western companies with access to heavy rare earth elements outside Chinese control. These deposits utilise similar leaching technologies as Chinese ionic clay operations, potentially reducing technology development risks while providing access to valuable dysprosium and terbium resources essential for high-performance magnet applications.

Virginia Tech pilot facilities prove commercial viability for Chilean ionic clay processing, providing technical validation that reduces investment risks for commercial-scale facility development. Successful pilot operations demonstrate that processing technologies developed for Chinese ionic clays can adapt to Chilean feedstock sources, reducing technology transfer barriers while maintaining processing efficiency.

Louisiana refining infrastructure planning advances toward commercial deployment, creating integrated supply chains from Chilean feedstock through American processing to end-user applications. This vertical integration approach reduces supply chain complexity while maintaining Western control over critical processing stages. Additionally, this aligns with broader mining innovation trends across the industry.

European interest creates competitive acquisition dynamics that could drive up project values while ensuring multiple potential development pathways for Chilean resources. Competition between American and European companies for Chilean rare earth projects demonstrates global recognition of these resources' strategic value, potentially accelerating development timelines while increasing capital availability for project advancement.

What Technology Pathways Offer Greatest Supply Chain Resilience?

Recycling and Circular Economy Solutions

Magnet recovery technology scaling achieves commercial viability through hydrogen processing techniques that recover 90-95% of critical elements from end-of-life magnet applications. HyProMag's Texas facility demonstrates practical implementation of Hydrogen Processing of Magnet Scrap technology, creating circular supply loops that reduce primary mining dependencies while providing domestic sources of rare earth materials for magnet remanufacturing.

End-of-life magnet collection systems require infrastructure investment to capture material flows from automotive, electronics, and industrial applications before these valuable resources reach waste streams. Successful recycling programmes depend on reverse logistics capabilities that can efficiently collect and transport used magnets to processing facilities. Government policies supporting collection infrastructure development become essential components of circular economy strategies.

Recycling yields approaching 90-95% for critical elements demonstrate that circular supply chains can provide meaningful material volumes when scaled to industrial levels. These recovery rates make recycling economically competitive with primary mining for certain applications, particularly when security premiums justify higher processing costs. Advanced recycling technologies continue improving recovery efficiency while reducing processing costs.

Circular supply chains reduce primary mining dependencies by creating renewable sources of rare earth materials from existing applications reaching end-of-life status. As electric vehicle and renewable energy infrastructure ages over coming decades, recycling capabilities become increasingly important for maintaining adequate material supplies without expanding mining operations proportionally.

Alternative Feedstock Development

Wastewater and brine extraction technologies advance toward commercial viability through specialised ligand-based extraction methods that can recover rare earth elements from unconventional sources. Phoenix Tailings' $1.6 million ARPA-E funding supports development of these extraction technologies, targeting wastewater, brines, and industrial waste streams as rare earth sources rather than traditional mineral ores.

Industrial waste stream rare earth recovery proves feasible for creating additional supply sources from existing operations without requiring new mining permits or environmental approvals. Many industrial processes generate waste streams containing recoverable rare earth concentrations that current technologies cannot economically capture. Advanced extraction methods could unlock these resources while providing environmental benefits through waste stream processing.

Tailings reprocessing creates additional supply sources from previously mined materials that contain rare earth values not recovered during initial processing operations. Modern extraction technologies can often recover elements that were not economically recoverable when original mining operations occurred, effectively expanding resource bases without new exploration or permitting requirements.

Non-traditional deposits expand resource base definitions by targeting geological formations previously considered uneconomic or technically challenging to process. Clay-hosted rare earth deposits, coal ash resources, and phosphate rock byproducts represent potential sources that could supplement traditional carbonatite and alkaline igneous deposits currently dominating global production.

The next major ASX story will hit our subscribers first

How Should Companies Navigate Ex-China Supply Chain Transition Risks?

Strategic Sourcing Framework

Dual-sourcing implementation balances cost competitiveness with supply reliability by maintaining primary Chinese suppliers while developing secondary ex-China sources for security assurance. This approach recognises that immediate replacement of Chinese supply sources remains economically impractical while establishing backup capabilities that can scale during supply disruptions. Contract structures must balance cost optimisation with supply reliability requirements.

Primary Chinese suppliers maintained for cost competitiveness continue providing bulk material volumes at market-competitive pricing while companies develop alternative sources for strategic portions of their supply requirements. This hybrid approach manages transition costs while building ex-China capabilities that can expand if geopolitical tensions increase or Chinese export restrictions tighten further.

Secondary ex-China sources developed for security assurance provide supply reliability during disruption scenarios while potentially offering quality or specification advantages for specialised applications. These sources typically operate under premium pricing structures but provide strategic value through supply diversification and reduced geopolitical risk exposure.

Inventory strategies managing transition period volatility require increased working capital commitments to buffer supply disruptions while alternative sources reach commercial capacity. Companies must balance inventory carrying costs against supply security benefits, particularly for critical applications where material shortages could disrupt entire production lines.

Investment Timing Considerations

Early-stage project investments capture development upside by securing access to future production capacity at lower capital costs than commercial-stage acquisitions. Companies investing in rare earth projects during exploration and development phases potentially secure future supply sources at lower per-unit costs while gaining influence over project development decisions and timing.

Technology partnerships access specialised capabilities that individual companies cannot develop economically while sharing technology development risks across multiple participants. Partnerships with universities, government laboratories, and specialised technology companies provide access to advanced extraction and processing methods without requiring full internal capability development.

Government partnership leveraging policy support mechanisms provides access to funding, loan guarantees, and regulatory support that reduces project development risks while potentially offering preferential access to government stockpiling programmes. Companies aligning with government strategic priorities gain competitive advantages through reduced financing costs and regulatory support.

Regional diversification reduces single-point-of-failure risks by developing supply sources across multiple geographic regions and political jurisdictions. This approach provides protection against regional conflicts, natural disasters, or policy changes that could disrupt supply from any single location while enabling companies to optimise supply chains based on changing geopolitical conditions.

Risk Management Protocols

Supply chain monitoring systems track export licensing, price volatility, and geopolitical developments that could affect supply reliability and cost structures. These systems provide early warning capabilities that enable proactive responses to emerging supply risks while supporting contract negotiation and inventory management decisions.

Export licensing tracking prevents delivery disruptions by monitoring regulatory changes that could affect material flows from various source countries. Companies must understand export control regimes across multiple jurisdictions while maintaining compliance with import regulations in destination countries.

Price volatility hedging through contract structuring utilises long-term agreements, cost-plus pricing, and government backing to reduce exposure to commodity price swings while maintaining access to strategic materials. These structures transfer certain risks between parties while providing predictable cost structures for budgeting and planning purposes.

Geopolitical risk assessment informs sourcing decisions by evaluating political stability, trade relationships, and regulatory frameworks across potential supply sources. This assessment process guides investment allocation decisions while supporting contingency planning for various geopolitical scenarios.

What Long-Term Scenarios Shape Ex-China Supply Chain Evolution?

Scenario Planning Framework

Accelerated Decoupling Pathway assumes continuing deterioration of U.S.-China trade relationships leads to comprehensive separation of critical mineral supply chains. Under this scenario, government subsidies maintain ex-China project viability despite cost disadvantages while technology transfer restrictions force indigenous capability development. Security considerations override cost optimisation as primary procurement criteria, enabling regional supply chains to achieve strategic autonomy by 2030 despite higher production costs.

Technology transfer restrictions forcing indigenous capability development create opportunities for Western companies to develop specialised processing technologies without Chinese competition. This scenario drives innovation investment while potentially creating competitive advantages in next-generation extraction and processing methods. Government funding supports technology development programmes that might not achieve commercial viability under pure market conditions.

Managed Interdependence Model envisions Chinese export controls creating managed scarcity that maintains Chinese market dominance while allowing limited ex-China capacity development as strategic backup. This scenario involves hybrid sourcing strategies balancing cost and security considerations while maintaining technology cooperation under controlled frameworks. Chinese authorities manage export availability to prevent complete supply chain decoupling while maintaining strategic leverage.

Ex-China capacity develops as strategic backup rather than primary supply source, maintaining cost premiums that prevent full Chinese supply displacement while providing adequate backup capabilities during supply disruptions. This scenario requires sustained government support for ex-China projects that cannot achieve full cost competitiveness against Chinese production.

Market Reintegration Scenario assumes eventual resolution of trade tensions through multilateral agreements that restore Chinese market access under transparency mechanisms. Ex-China investments create permanent supply diversification that survives trade normalisation while competitive dynamics drive innovation across all regions. This scenario results in globally diversified supply chains with multiple competitive sources rather than Chinese dominance or complete decoupling.

Chinese market access restored under transparency mechanisms enables Western buyers to resume Chinese sourcing while maintaining alternative capabilities developed during transition periods. Competitive dynamics between Chinese and ex-China sources drive technology innovation and cost reduction across all regions.

Investment Implications by Scenario:

| Scenario | Ex-China Capacity Development | Chinese Market Role | Investment Strategy |

|---|---|---|---|

| Accelerated Decoupling | Rapid Scale-Up Required | Minimal Access | Aggressive Ex-China Investment |

| Managed Interdependence | Steady Backup Development | Controlled Primary Source | Balanced Portfolio Approach |

| Market Reintegration | Competitive Pressure | Restored but Diversified | Selective Technology Leaders |

Investment strategies must account for scenario uncertainty by maintaining flexibility to adapt as geopolitical and market conditions evolve. Companies pursuing ex-China supply chain development should structure investments to capture value under multiple scenarios rather than optimising for single outcomes. Early-stage investments in technology and feedstock access provide optionality that can scale under multiple development pathways.

Government policy coordination becomes essential under all scenarios to maintain project viability and strategic coherence across changing political cycles. Successful ex-China supply chain development requires sustained support mechanisms that survive electoral changes and evolving geopolitical priorities. Private sector investments must align with long-term policy frameworks rather than responding to short-term political signals.

Ex-China rare earth supply chains represent fundamental transformation from cost-optimised to security-prioritised sourcing strategies that require strategic patience while maintaining operational flexibility. Current initiatives constitute early-stage infrastructure development rather than immediate supply replacement, demanding understanding that meaningful diversification requires sustained government support, technology advancement, and capital deployment across multiple regions and processing stages. Companies must balance near-term Chinese supply dependencies with long-term ex-China capacity investments, recognising transformation timelines extend beyond current political cycles while adaptation capabilities remain essential as geopolitical and market conditions evolve.

Ready to Position Yourself Ahead of Critical Minerals Supply Chain Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in the evolving critical minerals landscape. Explore how major mineral discoveries can generate substantial returns by examining historic examples, then begin your 30-day free trial today to secure your market-leading advantage.