May 16, 2026

Strategic Resource Reallocation in Critical Minerals Development

The global transition toward electric vehicle adoption has created unprecedented demand pressures on lithium supply chains, forcing mining companies to make increasingly sophisticated capital allocation decisions. When Imerys freezes UK lithium project to focus on France, the decision reflected broader market dynamics that extend far beyond simple project economics. This strategic pivot illuminates how regulatory frameworks, government partnerships, and operational complexity considerations now drive resource allocation in the critical minerals energy transition sector.

The complexity of managing simultaneous international mining developments has reached levels that challenge even well-capitalised operators. Furthermore, multi-jurisdiction projects introduce regulatory arbitrage challenges that compound exponentially rather than additively, creating operational inefficiencies that transcend traditional cost-benefit analysis models.

When big ASX news breaks, our subscribers know first

The Economics of Multi-Project Development in Critical Minerals

European lithium developers face unprecedented capital allocation challenges as battery-grade material demand accelerates beyond current supply capabilities. Resource-constrained companies must now choose between geographic diversification and concentrated development excellence, with implications extending far beyond individual project economics.

Strategic Resource Allocation Comparison

| Factor | Multi-Country Approach | Single-Country Focus |

|---|---|---|

| Capital Efficiency | Diluted across jurisdictions | Concentrated expertise |

| Regulatory Complexity | Multiple frameworks | Streamlined compliance |

| Political Risk | Diversified exposure | Concentrated sovereign risk |

| Operational Synergies | Limited cross-border | Enhanced local integration |

| Management Bandwidth | Stretched across regions | Focused execution |

The Imerys freezes UK lithium project to focus on France case demonstrates how operational bandwidth constraints often prove more limiting than pure capital availability. Alessandro Dazza's acknowledgment that managing two projects of this scale simultaneously presented excessive complexity reflects a fundamental shift in mining industry evolution philosophy. Companies increasingly recognise that execution excellence in a single jurisdiction often delivers superior returns compared to diluted efforts across multiple territories.

Capital Efficiency Metrics in Lithium Development

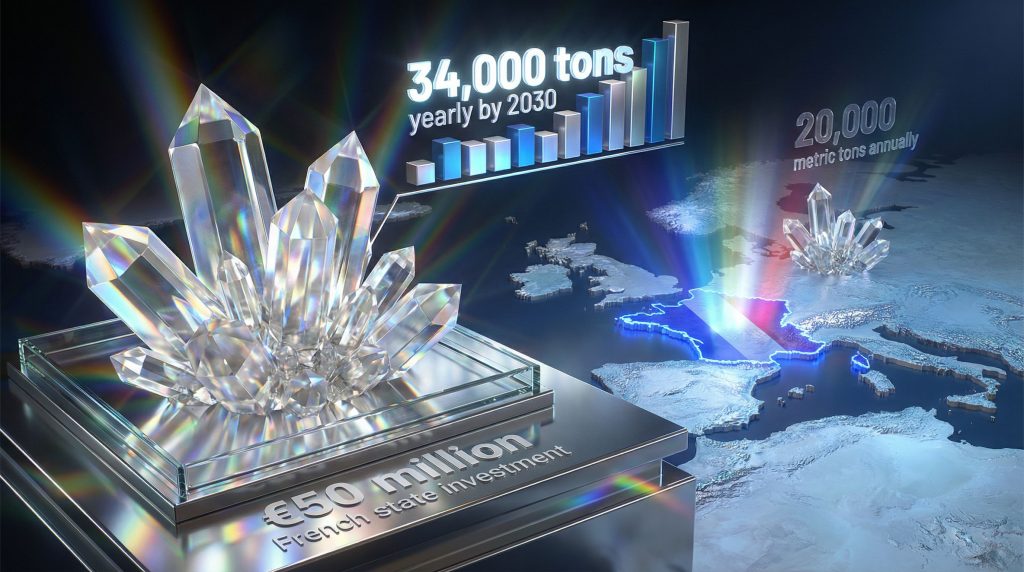

Mining executives increasingly focus on capital efficiency ratios rather than aggregate production capacity when evaluating project portfolios. The French Emili project's target of 34,000 tons annually of lithium hydroxide by 2030 represents 70% higher production volume than the suspended UK operation's 20,000+ metric tons of lithium carbonate target.

However, the production differential alone fails to capture the economic advantages driving strategic prioritisation. In addition, lithium hydroxide commands premium pricing over carbonate due to superior electrochemical performance in high-energy density battery applications, creating margin advantages that compound beyond simple volume metrics.

Government Partnership Dynamics in Strategic Minerals

State investment in lithium projects represents a fundamental shift from traditional mining finance models. When governments acquire minority stakes in domestic lithium operations, they create preferential development environments that international projects cannot match.

The €50 million French state investment in the Emili project demonstrates how sovereign backing transforms project economics through multiple channels beyond direct capital injection:

- Accelerated permitting processes reduce development timeline uncertainty

- Infrastructure development coordination minimises capital requirements

- Supply chain integration guarantees provide market access security

- Long-term offtake commitments stabilise revenue projections

Risk Mitigation Through Government Partnerships

Government partnerships fundamentally alter risk profiles for mining operations by providing institutional stability that private financing cannot replicate. The French state's minority stake in Emili creates alignment between sovereign strategic objectives and corporate operational goals, generating preferential treatment mechanisms unavailable to purely commercial ventures.

Consequently, this partnership structure enables mining companies to achieve development timelines and cost structures that would prove impossible through traditional project financing approaches. The Imerys official lithium website provides detailed information about their lithium operations and strategic focus on European development.

Production Metrics and Market Positioning Strategy

The distinction between lithium carbonate and hydroxide production reveals sophisticated market positioning strategies that extend beyond commodity pricing considerations. Imerys freezes UK lithium project to focus on France reflects understanding of downstream battery chemistry requirements and premium market segment targeting.

Lithium Product Specification Analysis

| Property | Lithium Carbonate | Lithium Hydroxide |

|---|---|---|

| Primary Application | Standard EV batteries, industrial | Premium EV batteries, high-density |

| Price Premium | Baseline reference | 15-25% higher than carbonate |

| Purity Requirements | 99.5% standard grade | 99.8%+ for battery-grade |

| Processing Complexity | Direct mineral extraction | Refined processing required |

| Market Positioning | Mass-market segments | Premium automotive manufacturers |

The UK project's capacity to serve approximately 500,000 electric vehicles annually through lithium carbonate production positions it for volume-oriented market segments. In contrast, the French project's hydroxide focus targets premium automotive manufacturers requiring superior battery performance characteristics.

Supply Chain Integration Advantages

Domestic projects offer superior integration opportunities with downstream battery manufacturers, creating value beyond commodity pricing through direct customer relationships and customised product specifications. Furthermore, European lithium hydroxide production enables proximity-based partnerships with continental battery manufacturers, reducing logistics costs while improving quality assurance coordination.

The geographic concentration strategy allows mining companies to develop specialised expertise in local regulatory frameworks, labour markets, and infrastructure systems. This creates competitive advantages that compound over multiple project phases, similar to approaches seen in Australia's critical minerals strategic reserve initiatives.

Geopolitical Factors Influencing Project Prioritisation

The European Union's Critical Raw Materials Act prioritises domestic sourcing for battery materials, creating policy environments that favour EU-based projects over external operations. This regulatory framework influences corporate decision-making through preferential financing access and streamlined environmental approvals within EU jurisdictions.

Post-Brexit regulatory divergence creates additional complexity for UK-based operations, particularly regarding product certification for EU market access. These regulatory arbitrage challenges introduce execution risks that extend beyond traditional mining project considerations.

Strategic Autonomy Implications

European strategic autonomy objectives create preferential treatment mechanisms for domestic lithium projects through supply chain resilience incentives and trade policy protection measures. Moreover, mining companies developing EU-based operations gain preferential access to continental battery manufacturing markets while benefiting from regulatory streamlining initiatives.

The French state's direct investment in Emili signals alignment between corporate strategy and sovereign critical minerals independence objectives. The latest press release from Imerys details this strategic partnership and its implications for European lithium supply.

Market Dynamics Driving Resource Concentration

Current lithium market conditions favour projects with shorter development timelines and lower execution risk profiles. Companies with limited capital must prioritise operations capable of achieving production before potential commodity price corrections affect project economics.

Market Risk Mitigation Factors:

- Faster time-to-market reduces commodity price exposure duration

- Government partnerships provide price stability mechanisms

- Established infrastructure minimises unexpected development costs

- Proven geology reduces technical execution uncertainty

Lithium Price Volatility Considerations

Mining companies increasingly structure project portfolios to minimise exposure to lithium price volatility through operational flexibility and strategic optionality preservation. The decision to place the UK project on care and maintenance status preserves future development opportunities while concentrating near-term resources on lower-risk operations.

This approach creates strategic flexibility for market condition adaptation, enabling rapid capacity expansion during demand surge scenarios. Similarly, the European approach to establishing an European CRM facility demonstrates coordinated responses to supply chain vulnerabilities.

The next major ASX story will hit our subscribers first

Long-Term Supply Implications for European Markets

Placing the UK project on care and maintenance preserves future development optionality while concentrating near-term resources on execution excellence. This approach creates strategic flexibility for multiple future scenarios involving market condition changes, geopolitical disruptions, or technological advances that reduce multi-country development costs.

Strategic Reserve Development Pathways

The concentration of development resources on domestic European projects accelerates the continent's trajectory toward lithium independence while potentially reducing global market integration dynamics. Companies achieving operational excellence in European markets position themselves for preferential access to the world's second-largest EV market.

Future Scenario Analysis:

- Successful French operations enable UK project restart by 2032

- Market conditions may favour permanent UK project suspension

- Geopolitical tensions could accelerate dual-project development requirements

- Technology advances might reduce multi-country development complexity

Investment Community Response Patterns

Financial markets typically reward focused development strategies during capital-constrained periods, particularly when companies demonstrate clear prioritisation criteria and realistic timeline commitments for primary operations. The preservation of optionality for future expansion while optimising risk-adjusted returns across project portfolios generates positive investor sentiment.

However, mining companies that successfully develop European lithium operations gain competitive advantages extending beyond current project economics. These advantages include established customer relationships, regulatory expertise, and operational infrastructure that enables rapid expansion during favourable market conditions, potentially benefiting from lithium industry tax breaks and similar supportive policies.

Strategic Focus as Competitive Advantage

The decision to concentrate resources on single-country development reflects sophisticated risk management approaches adapted to uncertain global environments. Companies achieving operational excellence in domestic markets position themselves for sustainable competitive advantages as the lithium industry matures beyond its current development phase.

This strategic pivot demonstrates how resource allocation decisions in critical minerals incorporate geopolitical considerations, supply chain integration opportunities, and long-term market positioning objectives. These extend far beyond traditional mining economics frameworks.

The Imerys freezes UK lithium project to focus on France experience illustrates broader industry trends toward strategic concentration rather than geographic diversification. Successful operators increasingly recognise that execution excellence in focused jurisdictions delivers superior risk-adjusted returns compared to diluted international development approaches.

Disclaimer: This analysis incorporates forward-looking statements and industry projections that involve inherent uncertainties. Lithium market conditions, regulatory frameworks, and geopolitical factors may change materially, affecting project economics and strategic positioning. Readers should conduct independent research before making investment decisions based on critical minerals sector analysis.

Looking for Opportunities in Critical Minerals Development?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly identifying actionable opportunities in lithium, rare earths, and other critical minerals sectors. Understand why major mineral discoveries can generate substantial returns whilst positioning yourself ahead of market movements with a 14-day free trial today.