June 13, 2026

Understanding the Strategic Shift in Global Reserve Management

The acceleration of alternative reserve strategies among emerging economies reflects calculated responses to demonstrated vulnerabilities in traditional financial systems. When comprehensive asset freezes targeted approximately $300 billion in sovereign reserves during 2022, it exposed fundamental risks of maintaining wealth in systems controlled by potentially adversarial powers.

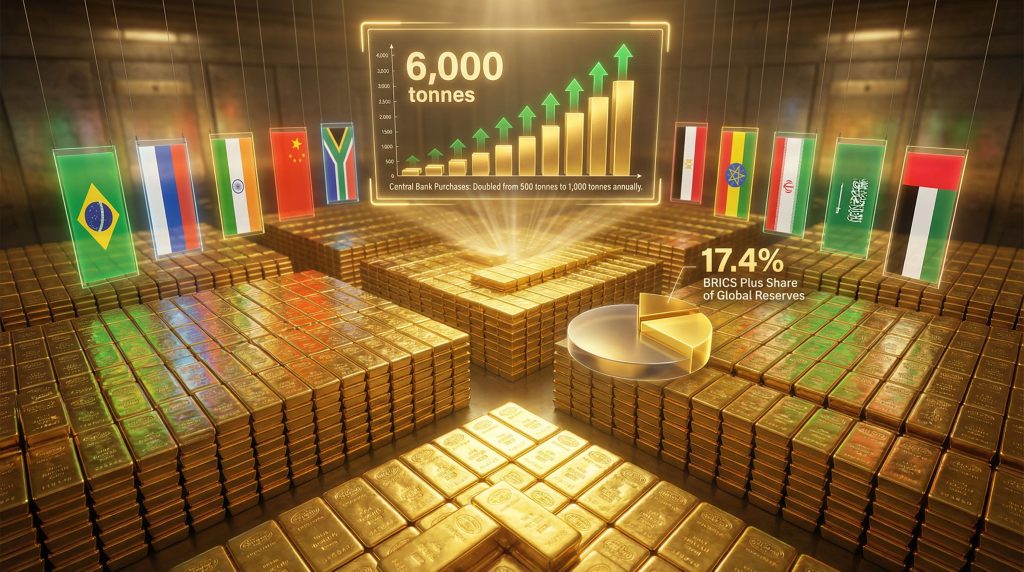

BRICS Plus nations have collectively accumulated over 6,000 tonnes of gold reserves, representing a dramatic increase from 11.2% of global central bank holdings in 2019 to 17.4% by April 2026. This transformation extends beyond simple portfolio rebalancing to encompass development of entirely new settlement mechanisms and payment infrastructure.

The mathematical scale of this reallocation becomes clear when examining specific holdings. Russia leads with 2,336 tonnes, whilst China maintains 2,298 tonnes, with India contributing 880 tonnes to collective reserves. Together, these three nations control approximately 77.2% of BRICS Plus gold holdings, demonstrating concentrated strategic positioning among the bloc's largest economies.

Currency Reserve Evolution Patterns

The declining dominance of dollar-denominated reserves provides crucial context for understanding this historic gold price surge strategy. International Monetary Fund data reveals the dollar's share of global reserves falling from 71% in 1999 to approximately 57% by late 2025, marking its lowest reading since 1994.

Critically, foreign central bank holdings of dollar-denominated assets have remained essentially flat since 2014. This indicates that reserve diversification occurs through alternative asset growth rather than active dollar liquidation. Furthermore, this pattern suggests coordinated strategic repositioning rather than panic-driven selling.

When big ASX news breaks, our subscribers know first

What Economic Forces Drive This Unprecedented Gold Accumulation?

Central bank gold purchases have doubled from pre-2022 levels of approximately 500 tonnes annually to over 1,000 tonnes per year throughout the subsequent three-year period. This sustained accumulation represents roughly 20% of global annual mine production being absorbed by sovereign buyers regardless of price fluctuations.

The BRICS nations now control a significant portion of global gold reserves, demonstrating their commitment to alternative financial architecture.

Key Economic Drivers Behind Gold Accumulation:

- Protection against asset seizure through international banking systems

- Reduced exposure to currency volatility in reserve holdings

- Enhanced bargaining power in international trade negotiations

- Diversification away from single-currency dependency

- Geopolitical neutrality during international disputes

The 2022 demonstration of financial vulnerability fundamentally altered risk assessment calculations across emerging market central banks. Gold stored in domestic vaults cannot be frozen through the Society for Worldwide Interbank Financial Telecommunication system, providing operational independence from Western-controlled payment infrastructure.

Regional Accumulation Analysis

Between 2020 and 2024, BRICS Plus member central banks purchased more than 50% of all gold acquired by sovereign buyers globally. In the first nine months of 2025 alone, these nations added 663 tonnes valued at approximately $91 billion to their holdings.

Brazil's re-entry into gold markets exemplifies the expanding participation within this strategy. The country made its first gold purchase since 2021, adding 16 tonnes in September 2025. This signals renewed commitment to gold diversification among BRICS Plus members.

| Economic Metrics | 2019 Baseline | Current Levels | Change |

|---|---|---|---|

| BRICS Plus Share of Global Central Bank Reserves | 11.2% | 17.4% | +6.2 percentage points |

| Annual Central Bank Gold Purchases | ~500 tonnes | 1,000+ tonnes | 100% increase |

| Gold's Share of Official Reserve Assets | <10% (2015) | >23% | 130%+ increase |

| Dollar Share of Global Reserves | ~61% (2015) | ~57% | -4 percentage points |

How Do Current Holdings Compare to Historical Reserve Patterns?

The transformation in reserve composition becomes apparent when examining gold's increased significance within official portfolios. Gold's share of total reserve assets more than doubled from below 10% in 2015 to over 23% currently. This reflects both price appreciation and deliberate allocation increases by central banks.

The current record-high gold prices have reinforced the strategic value of these accumulation strategies across BRICS Plus nations.

Strategic Positioning Analysis

Russia's 2,336 tonnes represent 38.9% of total BRICS Plus gold holdings, directly correlating with the nation's exposure to financial sanctions. China's parallel accumulation of 2,298 tonnes (38.3% of the bloc's total) demonstrates similar strategic positioning despite different geopolitical risk profiles.

This concentration suggests that gold accumulation reflects systemic structural concerns rather than nation-specific vulnerabilities. India's substantial holdings of 880 tonnes (14.7% of BRICS Plus total) reinforce the broad-based nature of this reserve strategy.

Notable Reserve Allocation Patterns:

- High Concentration: Russia and China control 77.2% of BRICS Plus gold

- Significant Scale: Combined holdings exceed 4,600 tonnes

- Strategic Distribution: Major emerging economies leading accumulation

- Growth Trajectory: 55% increase in bloc's share since 2019

Comparative Global Context

Saudi Arabia's position illustrates the potential for accelerated accumulation among newer BRICS Plus members. With approximately $500 billion in total reserves, the Kingdom currently holds only 323 tonnes of gold, representing just 2.6% of its reserve portfolio.

Analysis indicates that increasing Saudi Arabia's gold allocation from 2.6% to merely 5% of total reserves would require purchases equivalent to entire projected central bank demand for 2026. This demonstrates the scale of potential market impact from strategic repositioning.

What Role Does Gold Play in Alternative Financial Architecture?

Gold provides the foundation for developing payment and settlement mechanisms that operate independently from traditional Western financial infrastructure. Unlike currency-based reserves subject to freezing through banking system controls, gold offers geopolitical neutrality and maintains value during periods of financial market stress.

The gold market performance throughout 2025 has validated these strategic positioning decisions amongst BRICS Plus members.

Structural Market Impact

The consistent absorption of approximately 20% of yearly global mine supply through central bank purchases creates a structural demand floor that functions independently of price levels. This one-directional flow has made each market correction shallower than previous cycles, establishing higher baseline valuations for gold.

Infrastructure Development Components:

- Independent Settlement Systems: Mechanisms bypassing SWIFT infrastructure

- Bilateral Trade Arrangements: Gold-backed payment frameworks

- Reserve Diversification: Reduced dependency on single-currency systems

- Geopolitical Insurance: Protection against financial weaponisation

Central bank demand receives reinforcement from institutional flows, with gold exchange-traded fund inflows accelerating throughout 2025. China's insurance sector has received pilot allocations for gold positions. This indicates expanding institutional adoption beyond central bank strategies.

Technical Settlement Mechanisms

The development of alternative payment systems creates practical frameworks for utilising gold reserves in international trade. These mechanisms reduce dependency on traditional Western financial infrastructure whilst maintaining liquidity for cross-border transactions.

Saudi Arabia's participation in the mBridge platform demonstrates the practical implementation of alternative financial architecture. Combined with deepening ties with Beijing and BRICS Plus membership, this suggests strategic repositioning that could logically include expanded gold holdings.

Which Economic Indicators Signal Continued Accumulation?

World Gold Council survey data reveals unprecedented central banker sentiment regarding future reserve composition. Seventy-three percent of central bankers globally believe the dollar's reserve share will decrease further over the next five years. Meanwhile, 43% of surveyed central banks plan to increase gold holdings, both representing record-high readings.

The gold price forecast for 2025 supports continued strategic accumulation by BRICS Plus nations seeking monetary sovereignty.

Acceleration Catalysts

Three specific developments could significantly accelerate current accumulation trends:

1. China's Reporting Resumption

If China resumes public reporting of gold reserve additions and reveals larger-than-expected holdings, this would serve as an immediate catalyst. The country has not publicly reported purchases since May 2024, creating speculation about undisclosed accumulation.

2. Gulf State Allocation Increases

Formal gold allocation increases by Saudi Arabia or the United Arab Emirates would confirm that newest BRICS Plus members are following the Russia-China strategic model. Given Saudi Arabia's massive reserve base, even modest percentage increases would require substantial absolute purchases.

3. Dollar Share Decline Continuation

Further decreases in the dollar's reserve share in subsequent International Monetary Fund Currency Composition of Official Foreign Exchange Reserves releases would reinforce the narrative driving sovereign gold demand. This could potentially accelerate accumulation strategies.

Market Psychology Factors

The World Gold Council projects 750 to 850 tonnes of central bank purchases for the current year, maintaining levels far above historical norms. This sustained demand represents fundamental shifts in how central banks perceive reserve adequacy and portfolio optimisation.

Sentiment Indicators:

- Record Central Banker Pessimism: Regarding dollar's future dominance

- Unprecedented Accumulation Plans: 43% planning gold increases

- Structural Demand Floor: 20% of global mine supply absorbed annually

- Institutional Flow Acceleration: Beyond central bank purchases

How Do Supply Dynamics Support Higher Gold Prices?

The structural nature of central bank demand creates price dynamics fundamentally different from previous market cycles. Unlike speculative or investment flows that reverse during market stress, sovereign accumulation continues regardless of short-term price movements.

Effective gold market strategies must account for this structural shift in demand patterns driven by BRICS Plus accumulation.

Production Constraint Analysis

Global gold mine production faces increasing geological challenges, with ore grades declining across major producing regions. The absorption of 1,000+ tonnes annually by central banks represents 20% of total mine supply. This creates supply-demand dynamics that support higher price baselines.

This structural support mechanism functions independently of traditional market forces, as central bank purchases reflect strategic policy decisions rather than price sensitivity. The result is price correction patterns that demonstrate reduced volatility and shallower downturns compared to historical precedents.

Investment Flow Reinforcement

Beyond central bank demand, institutional investment flows provide additional price support through 2025. Exchange-traded fund accumulation and pilot allocations within China's insurance sector demonstrate expanding adoption across multiple investor categories.

The combination of sovereign strategic demand and institutional portfolio allocation creates reinforcing price dynamics. These reduce traditional gold market volatility whilst establishing higher valuation floors.

The next major ASX story will hit our subscribers first

What Are the Broader Economic Implications?

The coordinated gold accumulation strategy among BRICS Plus nations extends beyond monetary policy to encompass fundamental changes in international economic architecture. This transformation challenges the traditional dominance of dollar-denominated international finance through creation of alternative settlement mechanisms.

Multipolar Financial System Development

The strategic positioning represents more than commodity diversification; it signals construction of financial infrastructure capable of independent operation from Western-dominated systems. As BRICS Plus nations collectively control increasing shares of global gold reserves whilst developing alternative payment mechanisms, traditional monetary dominance faces structural challenges.

System Architecture Changes:

- Independent Payment Mechanisms: Bypassing traditional banking systems

- Bilateral Settlement Frameworks: Direct trade arrangements

- Reserve Diversification: Reduced single-currency dependency

- Strategic Monetary Sovereignty: Enhanced negotiating positions

Trade Settlement Evolution

Gold reserves provide foundations for trade settlement mechanisms that eliminate traditional currency conversion requirements, potentially reducing transaction costs and exchange rate risks for participating nations. These developments create practical alternatives to established financial infrastructure.

The economic logic driving this transformation encompasses practical risk management, portfolio optimisation, and creation of resilient monetary systems capable of operating in an increasingly multipolar global economy.

Investment Considerations:

- Structural Demand: Central bank accumulation provides price floor

- Supply Constraints: Limited mine production versus sovereign demand

- Geopolitical Insurance: Portfolio protection against systemic risks

- Alternative Architecture: Parallel financial system development

The BRICS Plus gold reserves increase represents fundamental shifts toward monetary independence and reduced systemic financial risk. As these nations collectively expand their gold reserve shares whilst constructing alternative financial infrastructure, the traditional dominance of dollar-denominated international finance confronts its most significant structural challenge in decades.

This transformation reflects economic logic extending beyond geopolitical considerations to encompass comprehensive risk management strategies, optimal portfolio construction, and development of resilient monetary frameworks designed for multipolar economic realities.

Ready to Identify the Next Major Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX gold and mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns and begin your 14-day free trial today to position yourself ahead of the market.