June 21, 2026

Strategic Supply Chain Vulnerabilities: Understanding Critical Energy Dependencies

Global energy markets operate through intricate networks of interdependent chokepoints, where single maritime corridors carry disproportionate volumes of the world's petroleum supplies. These critical passages represent potential system failure points that can cascade through international markets within hours, transforming from localized disruptions into worldwide economic shocks. The Strait of Hormuz oil market disruption creates systemic vulnerabilities that extend far beyond immediate supply concerns, affecting everything from currency stability to manufacturing costs across multiple continents.

Investment strategists increasingly recognise that modern energy security depends not merely on production capacity, but on the resilience of transportation networks that connect producers with consumers. When these pathways face operational constraints, the resulting market dynamics reveal the true interdependence of global economic systems and the speed at which local conflicts can reshape international trade patterns.

When big ASX news breaks, our subscribers know first

Understanding the Critical Energy Chokepoint

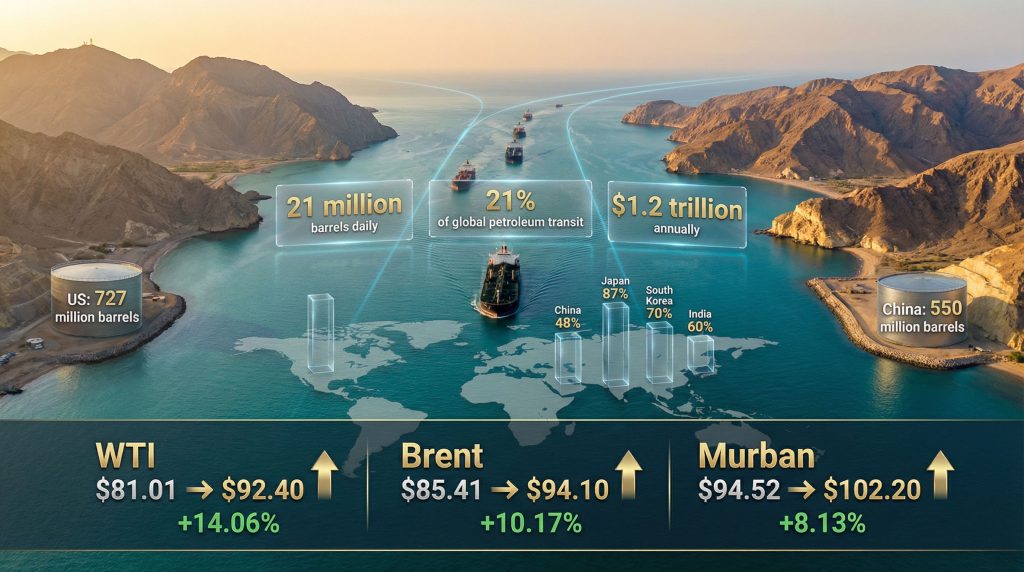

The Strait of Hormuz functions as the world's most strategically significant maritime energy corridor, handling approximately 21% of global petroleum liquids and substantial volumes of liquefied natural gas. This narrow waterway, measuring just 21 miles at its most constrained point, serves as the primary export route for Persian Gulf crude destined for international markets.

Recent market data illustrates the corridor's strategic importance through its daily throughput metrics. Furthermore, these volumes demonstrate the concentrated nature of global energy flows through this critical chokepoint.

| Commodity Type | Daily Volume | Global Share |

|---|---|---|

| Crude Oil | ~21 million barrels | 21% of global liquids |

| LNG | Significant volumes | ~20% of global supply |

| Refined Products | Variable | Regional distribution |

Geographic and Strategic Constraints

The strait's physical characteristics create inherent operational vulnerabilities that extend beyond simple navigation concerns. Maritime traffic must navigate through defined shipping lanes under specific draft restrictions, with limited manoeuvring space for the ultra-large crude carriers that transport the majority of petroleum volumes.

These vessels, some exceeding 300 metres in length, require precise coordination and optimal weather conditions to traverse safely. Insurance markets recognise these constraints through specialised premium structures for Hormuz transit, with rates fluctuating based on geopolitical risk assessments and seasonal navigation conditions.

Lloyd's of London and other major maritime insurers maintain dedicated risk models for strait passage, incorporating factors ranging from vessel congestion to regional military activity. Consequently, shipping costs reflect these heightened risk premiums during periods of uncertainty.

Immediate Market Consequences of Strait of Hormuz Oil Market Disruption

When maritime operations through the strait face restrictions, oil markets demonstrate immediate price volatility driven by supply uncertainty rather than actual shortages. Current benchmark data reveals the magnitude of these market responses, particularly as oil price movements reflect geopolitical tensions.

| Benchmark | Current Price | Weekly Change | Percentage Increase |

|---|---|---|---|

| WTI Crude | $92.40 | +$23.00 | +33.1% |

| Brent Crude | $94.10 | +$20.00 | +27.0% |

| Murban Crude | $102.20 | +$7.68 | +8.1% |

Price Formation Mechanisms During Disruptions

The market's response to Strait of Hormuz oil market disruption follows predictable patterns that reflect both psychological and logistical factors. Goldman Sachs recently adjusted their quarterly Brent forecasts upward by $10 per barrel, indicating institutional recognition of sustained risk premiums.

Similarly, JP Morgan has warned of potential catastrophic supply losses, suggesting major financial institutions view extended disruption scenarios as economically severe. Daily shipping traffic data provides concrete evidence of operational impact, with vessel counts dropping from normal levels of 138 ships per day to just 2 vessels during acute disruption phases.

This represents approximately a 98.6% reduction in maritime transit, demonstrating the binary nature of strait operations. However, the impact on global supply chains extends far beyond immediate petroleum flows.

Transportation Cost Escalation

Alternative shipping routes impose significant cost premiums that transmit directly into commodity pricing. LNG shipping rates have surged to $300,000 per day, representing a 650% increase from baseline levels.

These transportation costs create lasting price differentials even after physical supply restoration, as market participants factor route diversification expenses into long-term contracts. Tanker positioning becomes a critical bottleneck during disruptions, with dozens of Asia-flagged vessels reportedly stranded near the strait during recent tensions.

The economic value tied up in stranded cargoes compounds supply concerns, as floating storage reduces available transportation capacity for alternative routes. For instance, these factors contribute significantly to trade war global impact as supply chains face multiple simultaneous pressures.

Asian Economic Vulnerability to Supply Disruptions

Asian economies demonstrate the highest exposure to Strait of Hormuz oil market disruption due to their concentrated reliance on Middle Eastern crude supplies. Import dependency ratios reveal the extent of regional vulnerability, particularly as countries struggle with energy exports challenges.

| Country | Hormuz Dependency | Economic Exposure |

|---|---|---|

| Japan | 87% of crude imports | Manufacturing-heavy economy |

| South Korea | 70% of crude imports | Petrochemical sector risk |

| India | 60% of crude imports | Industrial gas supply impact |

| China | 48% of crude imports | Refining margin volatility |

Real-Time Impact Assessment

Recent market headlines demonstrate the cascading effects across Asian economies. Asian markets experienced significant declines as oil price surges stoked inflation concerns, while Japanese refiners urged government strategic petroleum reserve releases.

India's industrial gas supply faced cuts after Qatar suspended output, highlighting downstream manufacturing vulnerabilities. Reliance Industries exemplified regional adaptation strategies by pivoting back to Russian oil supplies through U.S. waivers.

Furthermore, two Russian Urals tankers diverted 1.4 million barrels to Indian ports. These supply diversification efforts illustrate the immediate tactical responses available to major regional refiners.

Refining Sector Dynamics

Despite supply constraints, Asia's refining margins reached 4-year highs during recent disruptions, as product prices escalated faster than crude costs. This margin expansion provides temporary compensation for operational challenges, though sustainability depends on demand elasticity and alternative supply activation.

Singapore complex margins often double during extended disruptions, reflecting the hub's role in regional product distribution. However, these margin improvements require balancing against increased crude procurement costs and supply chain uncertainties.

Alternative Supply Route Analysis

Several bypass options provide partial mitigation during Hormuz closures, though none match the strait's capacity or cost efficiency. Route alternatives demonstrate varying degrees of operational feasibility, whilst also facing challenges related to OPEC production impact.

Maritime Route Options

Suez Canal Route: Adds approximately 2,400 nautical miles to typical Persian Gulf-Asia routes, increasing shipping costs by 15-20%. Port congestion at Suez terminals can extend delays beyond pure transit time calculations, particularly during peak traffic periods.

Cape of Good Hope Route: Extends journey distances by 6,000 nautical miles, effectively doubling transportation time and fuel consumption. This route provides maximum flexibility but imposes significant cost penalties that make it economically viable only during sustained high-price environments.

Pipeline Infrastructure Limitations

Pipeline alternatives offer limited capacity relief, with combined systems handling maximum 60% of normal Hormuz volume. Saudi Arabia's East-West pipeline provides the largest single alternative, though capacity constraints limit throughput to 5-7 million barrels daily.

Turkish pipeline networks, including routes through the Baku-Tbilisi-Ceyhan system, offer additional capacity but serve primarily different crude grades and destinations. These systems require significant lead times for volume redirection and technical modifications.

What Are the Capacity and Infrastructure Constraints?

Alternative route activation faces several practical limitations that compound during crisis periods:

- Tanker availability becomes critical during extended disruptions

- Insurance premiums escalate for longer routes and higher-risk navigation

- Port facilities may lack adequate storage and handling capacity

- Pipeline utilisation requires coordination among multiple national systems

In addition, these constraints highlight the critical nature of strategic chokepoints in global energy transportation networks.

Strategic Petroleum Reserve Functions and Limitations

Strategic Petroleum Reserves provide temporary supply buffers during acute disruptions, though effectiveness depends on international coordination and release timing. Global SPR capacity demonstrates varying degrees of import coverage across major consuming nations.

| Country | SPR Capacity (Million Barrels) | Days of Import Coverage |

|---|---|---|

| United States | 727 | 143 days |

| China | 550 | 90 days |

| Japan | 324 | 133 days |

| South Korea | 96 | 106 days |

Release Coordination Mechanisms

Historical analysis suggests coordinated SPR releases can moderate price spikes by 15-25% during initial disruption phases. However, sustained effectiveness requires simultaneous demand destruction and alternative supply activation to prevent reserve depletion.

Japanese refiners recently urged government SPR releases, illustrating the political and economic pressures that accompany disruption scenarios. These releases must balance immediate supply needs against long-term strategic security considerations.

Policy Response Frameworks

International Energy Agency coordination provides the primary mechanism for multilateral SPR releases, though individual nation decisions often reflect domestic political considerations over optimal global allocation. China's strategic reserve policies remain less transparent than Western counterparts, creating uncertainty about coordinated response capabilities.

Consequently, energy transition security concerns become paramount as nations seek to reduce dependency on volatile supply routes.

The next major ASX story will hit our subscribers first

Financial Market Response Patterns

Energy sector equity performance typically demonstrates immediate valuation increases during Hormuz crisis periods, with upstream producers benefiting most from higher commodity prices. Recent market data illustrates sector-specific response patterns that reflect both short-term volatility and long-term structural implications.

Equity Market Dynamics

Energy sector performance during acute disruption phases shows characteristic patterns across different industry segments:

- Upstream E&P companies: +20-35% valuation increases

- Integrated oil majors: +10-15% with margin variability

- Independent refiners: +5-25% based on complexity and location

- Tanker companies: +40-60% due to increased day rates

Currency and Bond Market Implications

Oil-importing nations typically experience currency weakness against the dollar during extended disruptions, while oil-exporting countries see appreciation. U.S. government bond yields in major importing economies often rise due to inflation concerns and fiscal impact expectations.

Asian currencies face particular pressure during Strait of Hormuz oil market disruption scenarios, as import dependency creates sustained trade balance deterioration. Central banks must balance currency stability objectives against domestic economic stimulus needs.

Long-Term Strategic Infrastructure Adaptations

Extended disruption periods accelerate investment in alternative energy infrastructure and supply route diversification. These adaptations create lasting changes in global energy trade patterns that extend well beyond immediate crisis resolution.

Infrastructure Investment Acceleration

Pipeline expansion projects receive priority funding during crisis periods, with Trans-Arabian and alternative route development gaining political and financial support. Storage capacity expansion becomes strategically important, as commercial and strategic inventories provide operational flexibility.

Renewable energy deployment often accelerates during oil price shock periods, as economic competitiveness improves and energy security concerns drive policy support. LNG infrastructure development benefits from supply diversification needs, particularly in Asian markets seeking alternatives to pipeline gas.

Geopolitical Realignment Patterns

Prolonged disruptions catalyse shifts in energy partnership structures, with consuming nations diversifying supplier relationships and developing closer ties with non-Persian Gulf producers. Russia's increased crude exports to Asian markets exemplifies this diversification process, as consumers seek supply security through multiple provider relationships.

European LNG cargoes diverting to Asian markets during recent disruptions illustrate the dynamic nature of global gas trade, where supply flexibility responds to price differentials and security considerations.

Investment Portfolio Positioning for Hormuz Risk

Sophisticated investors employ multiple positioning strategies during uncertainty periods, combining direct commodity exposure with indirect hedging approaches. These strategies must account for both immediate price volatility and longer-term structural shifts in energy markets.

Direct Commodity Strategies

Oil futures and options provide direct price appreciation exposure, though timing and contract selection require careful consideration of backwardation and contango market structures. Tanker equity positions offer leverage to transportation premium increases, with day rates providing operational income streams during disruption periods.

Energy infrastructure REITs benefit from long-term structural shifts toward supply diversification, though performance depends on specific asset locations and pipeline utilisation rates.

Indirect Positioning Approaches

Currency hedging becomes important for exposure to oil-importing nations, as exchange rate fluctuations compound commodity price impacts. Inflation-protected securities preserve purchasing power during energy-driven price increases, though real yields may turn negative during acute phases.

Alternative energy investments benefit from accelerated deployment and improved economic competitiveness during high oil price periods, creating structural shift opportunities beyond immediate disruption scenarios.

Risk Management Framework Implementation

Effective risk management requires scenario-based portfolio construction with defined trigger points for position adjustments. Escalation indicators include shipping rate increases, insurance premium changes, and government SPR release announcements.

De-escalation signals such as resumed tanker traffic, normalised shipping rates, and production restart announcements provide exit timing guidance for crisis positioning strategies.

How Does Economic Modelling Assess Recession Risk?

Macroeconomic modelling suggests sustained Strait of Hormuz oil market disruption would trigger global recession within 6-9 months absent coordinated policy responses. GDP impact projections vary significantly by regional exposure and existing economic vulnerabilities.

| Region | Projected GDP Impact (12-month closure) |

|---|---|

| Asia-Pacific | -2.1% to -3.4% |

| European Union | -1.2% to -1.8% |

| United States | -0.7% to -1.1% |

| Global Average | -1.5% to -2.2% |

Inflation Transmission Mechanisms

Energy price increases transmit through multiple economic channels beyond direct fuel costs. Transportation and manufacturing cost increases create secondary inflationary pressures, while wage pressure emerges as workers demand compensation for reduced purchasing power.

Central bank policy responses face complex trade-offs between supporting economic growth and controlling inflation during extended disruptions. Federal Reserve and other major central banks maintain specialised models for energy shock scenarios, though policy effectiveness depends on disruption duration and severity.

Economic Vulnerability Assessment

Manufacturing-dependent economies in Asia face the highest vulnerability to sustained energy price increases, as industrial production costs escalate rapidly. Service-oriented economies demonstrate greater resilience, though consumer spending typically declines as energy costs consume larger budget shares.

Government fiscal impacts include both direct subsidy costs for energy price stabilisation and indirect revenue losses from reduced economic activity. These fiscal pressures compound currency stability challenges in energy-importing nations.

Moreover, the interconnected nature of modern economies means that disruptions in one region quickly cascade through global supply chains, amplifying the overall economic impact beyond initial projections.

Investment decisions involving energy market volatility and geopolitical risk carry significant uncertainty. This analysis is for informational purposes only and should not be considered as investment advice. Market conditions can change rapidly, and past performance does not guarantee future results. Readers should consult with qualified financial professionals before making investment decisions based on energy market disruption scenarios.

Looking to Position Your Portfolio Ahead of Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries that could benefit from energy security concerns and commodity price volatility, helping investors identify actionable opportunities in critical resources sectors. Explore why major mineral discoveries can generate substantial returns during market uncertainty by visiting Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to secure your market-leading advantage.