June 20, 2026

Strategic Transatlantic Partnerships Transform Critical Mineral Supply Networks

Western nations face an unprecedented challenge in securing reliable access to materials essential for clean energy transitions and national defence capabilities. As traditional supply chains concentrate production in single geographic regions, governments and private sector partners explore innovative approaches to distribute processing capacity across allied territories. USA Rare Earth reinforces Euro supply chain initiatives create new opportunities for technology transfer, investment diversification, and geopolitical risk mitigation in sectors ranging from permanent magnet manufacturing to advanced electronics production.

The complexity of rare earth element processing has historically favoured established facilities with decades of operational experience and regulatory familiarity. However, recent technological advances and policy frameworks enable sophisticated separation and metallisation processes to operate efficiently in multiple jurisdictions, provided adequate capital investment and technical expertise align properly.

When big ASX news breaks, our subscribers know first

French Industrial Heritage Meets American Mining Innovation

Southwestern France represents one of Europe's most established chemical processing regions, with industrial clusters dating back over a century. The Lacq region specifically offers unique advantages for advanced materials manufacturing through existing infrastructure, skilled workforce availability, and proximity to major European automotive and aerospace manufacturers requiring specialised alloys and magnetic materials.

Recent developments in this region demonstrate how historical industrial expertise can adapt to meet contemporary strategic material requirements. The establishment of integrated processing facilities combining oxide separation with downstream metallisation creates vertical integration opportunities previously unavailable in Western markets.

Key Strategic Advantages of French Facilities:

• Established chemical industry infrastructure reducing startup timelines

• Skilled workforce experienced in complex separation processes

• Regulatory framework supporting green industrial development

• Geographic proximity to major European end-use manufacturers

• Access to Mediterranean and Atlantic shipping networks for global distribution

The integration of American mining feedstock with French processing capabilities represents a fundamental shift in how Western nations approach critical material security. This model leverages complementary strengths rather than attempting to replicate complete supply chains within individual countries.

Investment Architecture Enabling Transatlantic Integration

Multi-national financing structures have emerged as essential mechanisms for scaling rare earth processing operations outside traditional manufacturing centres. The complexity of these investments reflects both technical requirements and geopolitical considerations affecting long-term supply security.

Financial Structure Analysis:

| Funding Source | Investment Amount | Strategic Purpose |

|---|---|---|

| Japanese Co-Investment (JOGMEC/Iwatani) | €110 million | Technology transfer and Asian market access |

| French Government Support | €106 million | Domestic processing capability development |

| Infrastructure Development | €130 million | Real estate and facility construction |

| Private Equity (InfraVia) | Proportional stake | Commercial optimisation and scaling |

This investment architecture demonstrates how allied nations coordinate capital deployment to achieve mutual strategic objectives. Japan's participation reflects its critical dependence on rare earth imports for electronics manufacturing, while French government support indicates European commitment to reducing processing dependencies.

Government Incentive Mechanisms:

• Tax credits covering up to 45% of specialised equipment costs

• Direct subsidies reducing operational risk during startup phases

• Expedited permitting processes for strategically classified projects

• Infrastructure development funding for supporting facilities

• Long-term regulatory stability commitments

Furthermore, the scale of government support reflects policy recognition that rare earth processing requires substantial initial investment with extended payback periods. Traditional market mechanisms alone typically cannot justify the capital requirements and technical risks associated with establishing new processing facilities.

Processing Capacity Metrics and Competitive Positioning

Understanding processing capacity distribution across Western facilities reveals both opportunities and constraints in developing alternative supply networks. The technical complexity of rare earth separation varies significantly between light and heavy rare earth elements, with heavy rare earths representing particular strategic importance despite comprising small percentages of total ore content.

Western Rare Earth Processing Capacity Overview:

| Facility Location | Annual Capacity | Processing Focus | Strategic Significance |

|---|---|---|---|

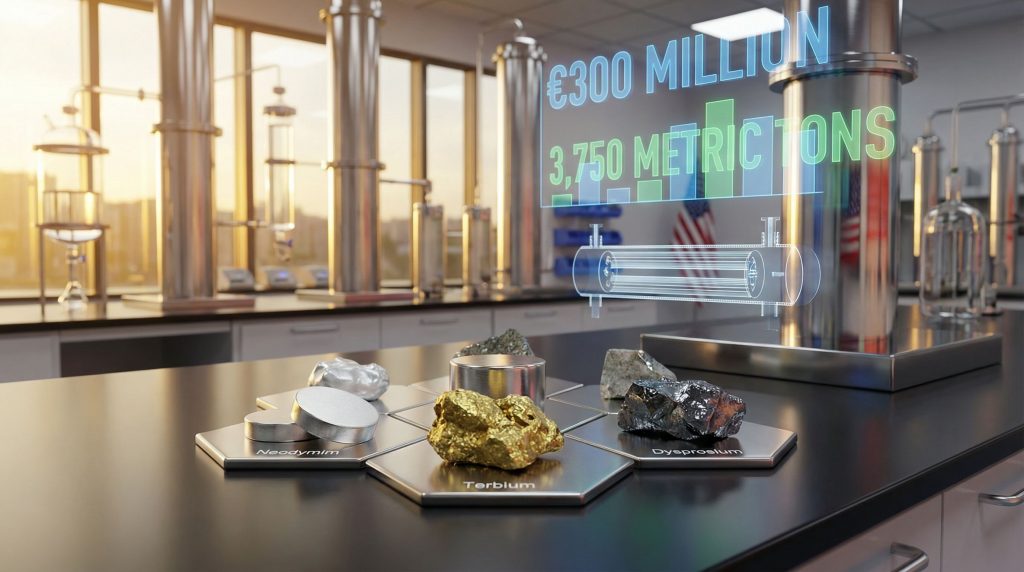

| Lacq, France (Metals) | 3,750 metric tons | Alloy production | European market integration |

| Lacq, France (Separation) | 1,600 metric tons | Oxide processing | Heavy rare earth capability |

| Mount Weld/Malaysia (Lynas) | ~11,000 metric tons | Integrated processing | Established commercial operation |

| Mountain Pass, USA | Variable | Concentrate production | Domestic feedstock security |

The capacity figures reveal Western processing capabilities remain substantially smaller than Chinese facilities, which process an estimated 70,000-80,000 metric tons annually across multiple sites. However, Western facilities increasingly focus on high-value heavy rare earth elements and specialised applications rather than competing directly on volume.

Heavy Rare Earth Separation Expertise:

Heavy rare earth elements including terbium, dysprosium, and holmium command premium pricing due to their essential role in high-performance permanent magnets. These elements typically represent 2-3% of rare earth ore content but account for 15-20% of total value in many applications.

The technical complexity of heavy rare earth separation has historically concentrated this capability in specialised facilities with decades of operational experience. Recent advances in separation chemistry and process optimisation enable new facilities to achieve comparable separation efficiency, provided adequate technical support and quality control systems.

Technology Transfer and Intellectual Property Integration

Advanced rare earth processing requires sophisticated understanding of separation chemistry, metallisation techniques, and quality control procedures developed over decades of industrial operation. Technology transfer agreements enable new facilities to access this expertise while contributing additional innovation and process improvements.

Critical Technology Components:

• Solvent extraction cascade design for selective separation

• Precipitation chemistry optimised for heavy rare earth recovery

• Metallisation processes producing high-purity elemental metals

• Recycling technologies for permanent magnet and electronic waste

• Quality assurance protocols ensuring consistent product specifications

The intellectual property aspects of rare earth processing create both opportunities and constraints for new entrants. Established companies possess valuable process knowledge accumulated through years of operational experience, while new facilities can implement updated equipment and digital optimisation technologies.

Recycling Integration Opportunities:

End-of-life permanent magnets and electronic components represent increasingly important feedstock sources for rare earth processing facilities. Recycled materials often contain higher concentrations of valuable heavy rare earth elements compared to primary ore, creating economic incentives for integrated recycling operations.

European markets generate substantial quantities of rare earth-containing waste through automotive, wind energy, and electronics sectors. Localised recycling capabilities reduce transportation costs while providing consistent feedstock independent of international mining operations.

Market Dynamics and Pricing Considerations

Rare earth element pricing reflects complex interactions between supply constraints, technological demand, and geopolitical factors affecting international trade. Heavy rare earth elements exhibit particular price volatility due to limited alternative sources and concentrated production capabilities.

Price Volatility Factors:

• Export quota policies implemented by major producing nations

• Demand fluctuations in electric vehicle and renewable energy sectors

• Currency exchange rates affecting international transactions

• Substitute material development reducing consumption requirements

• Strategic stockpiling activities by governments and manufacturers

The establishment of additional processing capabilities in Western markets could potentially stabilise pricing through increased supply diversity. However, the capital-intensive nature of rare earth facilities requires long-term contracts and stable demand projections to justify investment.

Regional Market Integration:

European automotive manufacturers increasingly require traceability and sustainability certification for rare earth materials used in electric vehicle production. Localised processing capabilities can provide enhanced supply chain transparency while reducing logistics complexity and associated carbon emissions.

In addition, the proximity of French facilities to major European industrial centres creates advantages in transportation costs, technical support, and customer relationship management compared to traditional Asian suppliers.

The next major ASX story will hit our subscribers first

Risk Assessment and Scenario Analysis

Investment in rare earth processing facilities involves multiple categories of risk requiring comprehensive evaluation and mitigation strategies. Technical, market, regulatory, and geopolitical factors all influence long-term project viability and return potential.

Technical Risk Factors:

• Process optimisation challenges during initial operational periods

• Environmental compliance requirements varying across jurisdictions

• Workforce development needs for specialised technical positions

• Equipment reliability and maintenance complexity

• Quality control consistency achieving customer specifications

Market Risk Considerations:

• Competition from established processing facilities with lower operating costs

• Demand volatility in end-use sectors including automotive and renewables

• Substitute material development potentially reducing rare earth requirements

• Currency fluctuations affecting international competitiveness

• Long-term contracts necessary for financial viability

Geopolitical Risk Scenarios:

Trade policy changes could significantly impact rare earth supply chains through tariffs, export restrictions, or technology transfer limitations. For instance, the evolving industry landscape demonstrates how various nations implement strategic material controls affecting international commerce.

The development of diversified processing capabilities across allied nations provides some protection against single-country policy changes while maintaining technological cooperation frameworks essential for continued innovation.

Strategic Implications for Global Supply Chains

The establishment of integrated rare earth processing capabilities spanning American mining and European manufacturing represents a significant evolution in critical material supply chain architecture. This model demonstrates how allied nations can coordinate investment and technology sharing to achieve mutual strategic objectives, highlighting how USA Rare Earth reinforces Euro supply chain partnerships.

Long-term Strategic Benefits:

• Reduced dependence on concentrated processing capabilities

• Enhanced supply chain transparency and traceability

• Technology innovation through international collaboration

• Economic development in strategic industrial sectors

• Improved resilience against trade disruptions or political tensions

The success of this partnership model could influence similar developments in other critical material sectors including lithium processing, battery manufacturing, and semiconductor production. The combination of government support, private investment, and international cooperation creates a framework potentially applicable to various strategic industries.

Innovation Acceleration Opportunities:

Cross-border partnerships enable sharing of research and development costs while accessing diverse technical expertise and market insights. Joint innovation initiatives can advance processing efficiency, environmental performance, and product quality improvements benefiting all participants.

Consequently, the integration of recycling capabilities with primary processing creates circular economy opportunities while reducing raw material requirements and environmental impacts associated with mining operations.

Investment Outlook and Market Development

The rare earth processing sector continues evolving as governments and private investors recognise strategic importance of supply chain diversification. Multiple projects across Western nations indicate growing confidence in market demand and technological feasibility of new processing facilities.

Market Development Indicators:

• Government policy frameworks supporting critical material processing

• Private equity investment in rare earth infrastructure projects

• International cooperation agreements facilitating technology transfer

• End-user demand for supply chain transparency and sustainability

• Strategic stockpiling initiatives by governments and corporations

The timeline for achieving significant market impact extends over multiple years as facilities complete construction, optimise operations, and develop customer relationships. Initial production typically occurs at reduced capacity levels while technical processes undergo refinement and workforce training progresses.

What Are the Capacity Scaling Projections?

New rare earth processing facilities typically achieve 60-70% of design capacity during first-year operations, reaching full capacity within 2-3 years depending on market conditions and technical optimisation progress. The complex nature of separation chemistry requires extensive testing and adjustment periods.

Long-term capacity expansion potential depends on feedstock availability, market demand growth, and continued government support for strategic material processing initiatives. The capital requirements for additional capacity often necessitate demonstrated operational success and stable customer contracts.

Furthermore, comprehensive critical minerals strategies increasingly emphasise the importance of international partnerships in securing supply chains. As the EU and US implement their different approaches to critical minerals, USA Rare Earth reinforces Euro supply chain initiatives through strategic partnerships with French facilities.

Moreover, the establishment of processing capabilities demonstrates how USA Rare Earth reinforces Euro supply chain security through technological cooperation and investment coordination. This approach addresses both immediate supply needs and long-term strategic independence in critical materials sectors.

Investment Disclaimer: This analysis contains forward-looking projections based on current market conditions and policy frameworks. Actual results may differ materially due to technical, market, regulatory, or geopolitical factors. Readers should conduct independent due diligence and consult qualified professionals before making investment decisions.

Looking to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify emerging opportunities in critical materials and strategic commodities before they reach mainstream attention. Explore how major discoveries have generated substantial historical returns and begin your 14-day free trial today to position yourself ahead of evolving supply chain developments and strategic mineral partnerships.