July 17, 2026

Strategic Uranium Partnerships Transform Energy Security in an Interconnected World

The evolution of nuclear energy markets reflects shifting geopolitical dynamics, where long-term fuel supply agreements have become strategic assets rather than simple commercial transactions. In an era where energy independence defines national security priorities, uranium procurement strategies reveal broader patterns of alliance-building and technological sovereignty across major economies.

Modern nuclear powers increasingly recognise that reactor construction represents only the beginning of energy security planning. The fuel cycle dependencies that follow operational commissioning create multi-decade relationships between supplier and consumer nations, making uranium contracts instruments of both economic cooperation and strategic positioning.

When big ASX news breaks, our subscribers know first

Understanding the Strategic Context of Sovereign Uranium Procurement

Why Nuclear Powers Are Securing Long-Term Fuel Contracts

The global uranium market volatility is experiencing structural tightening that extends far beyond typical commodity cycles. Supply constraints between 2024 and 2026 have prompted nuclear operators to reassess procurement strategies, moving from spot market optimisation toward long-term contract security. This shift reflects fundamental changes in how governments perceive nuclear fuel supply chains within broader energy security frameworks.

Several converging factors drive this transformation:

- Market concentration risks with Kazakhstan controlling over 40% of global uranium production

- Secondary supply depletion as inventory stockpiles accumulated during previous market downturns reach critical levels

- Geopolitical supply chain vulnerabilities exposed by recent energy market disruptions

- Nuclear renaissance acceleration across Asia-Pacific regions requiring fuel supply certainty

The emergence of sovereign buyers represents a significant departure from utility-driven procurement models. Government entities now directly negotiate fuel supply agreements, reflecting strategic recognition that uranium supply transcends commercial considerations to encompass national energy security imperatives.

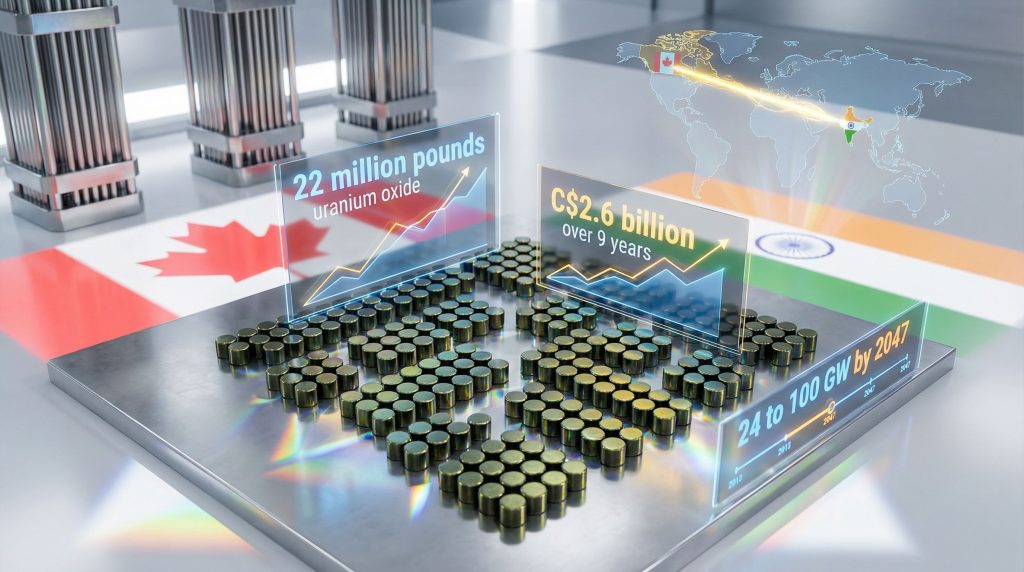

Recent market dynamics demonstrate this evolution clearly. The Cameco uranium deal with India, spanning nine years with 22-million-pound uranium commitment valued at C$2.6 billion, illustrates how long-term agreements provide mutual benefits: supply certainty for expanding nuclear programs and revenue visibility for uranium producers navigating volatile spot markets.

India's Nuclear Expansion Blueprint: Ambitious Growth Through Strategic Partnerships

India's nuclear expansion trajectory represents one of the world's most ambitious civilian nuclear programs. From 24 operational reactors today, the nation targets 100 GW of nuclear capacity by 2047, requiring unprecedented fuel supply coordination and international partnership development.

This expansion timeline creates specific procurement challenges:

| Expansion Phase | Capacity Target | Timeline | Fuel Requirements |

|---|---|---|---|

| Current Operations | ~7 GW | Present | Existing contracts |

| Phase 1 Expansion | 25 GW | 2030-2035 | New long-term agreements |

| Phase 2 Growth | 50 GW | 2035-2042 | Diversified supply base |

| Target Achievement | 100 GW | 2047 | Indigenous + imports |

Market-related pricing mechanisms in recent agreements reflect sophisticated risk management approaches. Rather than fixed-price structures that transfer commodity price risk entirely to suppliers, index-based pricing allows both parties to share market volatility exposure while maintaining contract predictability.

India's reactor fleet composition influences fuel procurement strategies significantly. Heavy water reactors and pressurised heavy water reactors require specific uranium concentrates, creating technical specifications that limit supplier options and increase the strategic value of established relationships with qualified producers like Cameco.

The 2.44 million pounds annually implied by the recent Cameco uranium deal with India represents substantial commitment relative to India's current fuel consumption, suggesting accelerated reactor commissioning schedules aligned with the 2047 capacity targets.

Geopolitical Dimensions of the Canada-India Energy Reset

Strategic Partnership Architecture Beyond Uranium

The uranium supply agreement forms one component of a comprehensive bilateral energy partnership that extends across multiple critical resource sectors. Canada and India have committed to doubling bilateral trade to C$70 billion by 2030, with energy and critical minerals cooperation serving as foundational elements of this expansion.

The Strategic Energy Partnership encompasses:

- Liquefied natural gas and liquified petroleum gas supply arrangements

- Solar energy technology collaboration and project development

- Hydrogen production partnerships aligned with both nations' clean energy transitions

- Critical minerals cooperation spanning lithium, rare earths, and graphite supply chains

- Clean energy infrastructure development across wind, biofuels, and hydropower sectors

Commercial agreements exceeding $5.5 billion signed during recent high-level visits demonstrate the breadth of economic integration beyond uranium supply. These arrangements include technology transfer provisions, manufacturing partnerships, and investment protection mechanisms designed to facilitate long-term industrial cooperation.

The partnership structure reveals strategic alignment between Canadian resource abundance and Indian manufacturing capabilities. Canada's mineral wealth combined with India's technological capacity creates complementary advantages that extend uranium cooperation into broader critical materials supply chains essential for Canada's energy transition technologies.

Diplomatic Recalibration: Renewed High-Level Engagement

The resumption of Prime Ministerial visits after an eight-year hiatus signals systematic diplomatic recalibration between Canada and India. High-level Canadian delegations including Cabinet members, Parliamentarians, and senior pension fund executives indicate institutional commitment across government and private sector stakeholders.

This diplomatic reset occurs within broader geopolitical realignments where resource-rich nations and major consuming economies seek diversified partnership arrangements. The Cameco uranium deal with India provides tangible demonstration of renewed cooperation while establishing frameworks for expanded collaboration across multiple sectors.

The partnership reflects mutual recognition that energy security requires diversified supply chains and strategic relationships that transcend traditional commercial arrangements.

Parliamentary and Cabinet-level participation in commercial agreement ceremonies demonstrates government recognition that resource partnerships constitute strategic rather than purely commercial relationships. This institutional engagement provides political foundation for long-term cooperation that outlasts individual administrations or market cycles.

The Comprehensive Economic Partnership Agreement targeted for completion in 2026 creates legal frameworks for expanded trade and investment flows, with energy cooperation serving as an anchor for broader economic integration between the two nations.

Market Structure Analysis: Cameco's Strategic Positioning

Contract Economics and Pricing Mechanisms

Cameco's uranium supply strategy demonstrates sophisticated market positioning that balances production planning with price risk management. The nine-year delivery commitment from 2027 through 2035 provides revenue visibility whilst utilising market-related pricing to share commodity price volatility between supplier and buyer.

Contract structure analysis reveals several strategic advantages:

Revenue Predictability: Multi-year volume commitments enable production planning and capital allocation optimisation across Cameco's mining operations, particularly at flagship facilities like McArthur River and Cigar Lake.

Price Risk Distribution: Market-related pricing mechanisms protect both parties from extreme price movements while ensuring contracts remain economically viable throughout the supply period.

Strategic Relationship Building: Long-term agreements create institutional relationships that facilitate future contract negotiations and partnership opportunities in expanding nuclear markets.

Supply Chain Integration: Extended delivery schedules allow optimisation of production, processing, and logistics coordination to minimise operational costs while meeting customer specifications.

The C$2.6 billion contract valuation based on February 2026 uranium prices provides baseline revenue expectations while acknowledging that actual payments will fluctuate with market conditions. However, historical legal disputes have shown how complex international uranium agreements can face regulatory challenges that affect contract performance.

Global Uranium Supply Chain Concentration Risks

Uranium market structure presents significant concentration risks that influence procurement strategies for nuclear operators worldwide. Kazakhstan's dominance of over 40% of global production creates systematic vulnerabilities that strategic buyers seek to mitigate through diversified supply arrangements.

Supply chain risk factors include:

- Geographic concentration in politically sensitive regions

- Transportation vulnerabilities for landlocked production centres

- Regulatory dependency on export licensing from supplier governments

- Currency exposure from pricing in multiple international currencies

- Technical specifications that limit supplier substitutability for specific reactor types

Canadian uranium suppliers like Cameco provide strategic diversification benefits for nuclear operators seeking to reduce concentration risks. Western hemisphere production offers geopolitical stability and transportation advantages compared to suppliers in regions experiencing political tensions or infrastructure limitations.

Secondary supply market dynamics complicate procurement planning as previous uranium inventory stockpiles decline. Utilities and government agencies accumulated substantial uranium reserves during market downturns, but these stockpiles are approaching depletion as nuclear capacity expands globally without proportional primary production increases.

Furthermore, US uranium market disruptions have demonstrated how trade policy changes can rapidly alter global supply dynamics, reinforcing the strategic value of diversified procurement relationships.

Investment and Industry Impact Assessment

Cameco's Operational Capacity and Production Planning

The substantial volume commitments in recent contracts require sophisticated production planning across Cameco's mining operations. Twenty-two million pounds over nine years represents significant output allocation that influences workforce planning, infrastructure investment, and operational scheduling across multiple facilities.

Production capacity considerations include:

McArthur River Operations: The world's largest high-grade uranium mine requires careful production scheduling to meet multiple contract commitments whilst optimising operational efficiency and environmental compliance.

Cigar Lake Integration: Advanced extraction technologies and processing capabilities provide flexibility for meeting customer specifications whilst maintaining cost competitiveness in global markets.

Workforce Scaling: Long-term contracts justify investment in workforce development and training programmes essential for maintaining technical expertise in specialised uranium extraction and processing operations.

Infrastructure Investment: Multi-year revenue visibility enables capital allocation for facility upgrades, environmental protection systems, and operational efficiency improvements.

Capital allocation strategies benefit from contract predictability that reduces market uncertainty whilst providing financial foundation for operational expansion and technological advancement. Revenue recognition over extended periods smooths cash flow patterns and supports strategic planning across mining, processing, and logistics operations.

Competitive Landscape Shifts in Uranium Markets

The emergence of sovereign buyers fundamentally alters competitive dynamics in uranium markets. Traditional utility-driven procurement focused primarily on cost optimisation and technical specifications, whilst government-level purchasing incorporates strategic considerations that transcend purely economic calculations.

Market structure evolution includes:

Long-term Contract Premiums: Sovereign buyers demonstrate willingness to pay premiums over spot pricing for supply security, creating market differentiation between short-term and strategic supply arrangements.

Supply Security Prioritisation: Government purchasers emphasise reliability and geopolitical alignment alongside cost considerations, rewarding suppliers offering strategic partnership benefits beyond commodity delivery.

Diversification Requirements: Nuclear programmes increasingly require multiple supplier relationships to reduce concentration risks, creating opportunities for qualified producers to capture market share through strategic positioning.

Technology Integration: Advanced reactor development creates demand for specialised fuel products that reward suppliers investing in technical capabilities and research partnerships.

Additionally, the US Senate uranium ban on Russian imports has created significant supply chain disruptions that benefit Western suppliers like Cameco, demonstrating how geopolitical developments can rapidly reshape competitive positioning in uranium markets.

Regional Nuclear Development Scenarios

Asia-Pacific Nuclear Growth Trajectories

Nuclear capacity expansion across the Asia-Pacific region creates substantial demand growth that influences global uranium supply allocation and pricing dynamics. Multiple major economies simultaneously pursuing nuclear expansion requires unprecedented coordination of fuel supply chains and long-term procurement strategies.

Regional development patterns include:

China's reactor construction pipeline with over 150 units planned represents the largest single source of uranium demand growth globally. Chinese procurement strategies emphasise supply chain control and domestic production development alongside strategic import relationships.

Japan's restart programme following Fukushima creates renewed demand for uranium supplies whilst emphasising enhanced safety standards and supply chain resilience requirements that influence global market standards.

South Korea's nuclear export ambitions combine domestic capacity expansion with international project development, creating complex fuel supply requirements that blend domestic and export market considerations.

These overlapping expansion programmes create competition for available uranium supplies whilst driving innovation in fuel cycle technologies and supply chain management. Regional cooperation frameworks emerge as governments recognise mutual benefits from coordinated procurement and technology development strategies.

Western Supplier Consolidation Dynamics

Uranium production in Western nations demonstrates increasing consolidation as market dynamics favour large-scale, technically sophisticated operations capable of meeting evolving customer requirements. Canadian uranium industry leadership reflects advantages in geological resources, technical expertise, and regulatory frameworks that support long-term operations.

Industry consolidation trends include:

- Australian export policy evolution under changing governments affects global supply availability

- African uranium development projects face political stability and infrastructure challenges

- Environmental and regulatory compliance requirements favour established operators with proven track records

- Indigenous community engagement frameworks become essential for project development and social licence maintenance

Technical expertise requirements for uranium extraction and processing create barriers to entry that benefit established producers like Cameco whilst limiting new supply development in regions lacking specialised knowledge and infrastructure.

The next major ASX story will hit our subscribers first

Risk Factors and Mitigation Strategies

Regulatory and Compliance Considerations

Uranium trade operates within complex regulatory frameworks that influence contract performance and market access. Nuclear Suppliers Group guidelines and export controls create systematic requirements that affect supplier qualification and market participation capabilities.

Regulatory risk management involves:

Export Licensing Compliance: Uranium suppliers must maintain regulatory approval from home governments whilst meeting destination country import requirements, creating multi-jurisdictional compliance obligations.

Environmental Assessment Requirements: Expanded production to meet growing demand triggers environmental review processes that influence project timelines and operational parameters.

Indigenous Community Consultation: Mining operations in Saskatchewan and other regions require ongoing consultation and benefit-sharing agreements with indigenous communities as part of social licence maintenance.

Nuclear Non-Proliferation Obligations: All uranium supply agreements must comply with international non-proliferation treaties and safeguards agreements that affect contract terms and monitoring requirements.

Consequently, industry analysis reports have highlighted the complex environmental and economic challenges facing major uranium producers, emphasising the importance of comprehensive risk assessment in long-term supply agreements.

Market Volatility and Contract Performance Risks

Uranium price volatility creates performance risks for long-term contracts that require sophisticated risk management strategies from both suppliers and buyers. Market-related pricing mechanisms distribute price risk whilst maintaining contract viability across different market conditions.

Risk mitigation approaches include:

- Force majeure provisions addressing supply disruption scenarios from operational, regulatory, or geopolitical causes

- Currency hedging strategies for multi-billion dollar contracts denominated in different currencies

- Volume flexibility mechanisms allowing adjustment for demand variations whilst maintaining core supply commitments

- Technical specification standards ensuring fuel quality meets reactor requirements throughout contract duration

Contract performance monitoring requires ongoing assessment of market conditions, operational capabilities, and regulatory compliance to identify potential issues before they affect supply delivery or commercial terms.

Strategic Implications for Global Energy Security

Nuclear Fuel Diplomacy and Alliance Building

Uranium supply relationships increasingly function as components of broader alliance structures and strategic partnerships between nations. Energy security cooperation extends beyond commercial transactions to encompass technology sharing, regulatory coordination, and joint development initiatives.

Strategic alliance dimensions include:

QUAD Partnership Energy Security: Cooperation among democratic allies in nuclear technology and fuel supply creates alternative supply chains to geopolitically problematic suppliers.

Indo-Pacific Economic Framework: Regional cooperation initiatives incorporate energy security provisions that facilitate uranium trade and nuclear technology development among partner nations.

Advanced Reactor Development: Joint research and development programmes require coordinated fuel cycle planning and supply chain development for next-generation nuclear technologies.

Technology Transfer Agreements: Nuclear cooperation extends beyond fuel supply to encompass reactor technology, safety systems, and regulatory framework development through partnership arrangements.

Long-Term Supply Chain Resilience Building

Diversification strategies across uranium supply chains reflect broader recognition that energy security requires multiple supplier relationships and strategic reserve policies. Nuclear powers increasingly implement portfolio approaches to fuel procurement that balance cost, reliability, and strategic considerations.

Supply chain resilience elements include:

- Strategic uranium reserves maintained by government agencies to provide supply security during market disruptions

- Advanced reactor fuel requirements creating demand for specialised products that require dedicated supply chain development

- Domestic production incentives in consuming nations to reduce import dependency whilst maintaining international partnership benefits

- Regional cooperation frameworks enabling shared procurement and supply chain development among allied nations

Market structure evolution toward long-term partnerships between sovereign entities creates stability that benefits both suppliers and consumers whilst reducing market volatility and investment uncertainty.

The transformation of uranium markets from purely commercial transactions to strategic partnerships reflects broader geopolitical realignments where energy security defines national competitiveness and alliance structures.

The Cameco uranium deal with India exemplifies this evolution, demonstrating how bilateral energy cooperation creates mutual benefits that extend far beyond commodity supply arrangements. As nuclear capacity expands globally, these strategic relationships will increasingly determine market access, technology development, and energy security outcomes for participating nations.

Investment implications for uranium markets include sustained demand growth, pricing premium for strategic supply arrangements, and operational advantages for suppliers capable of providing comprehensive partnership benefits beyond commodity delivery. The sector's evolution toward strategic cooperation creates opportunities for qualified participants whilst establishing barriers for purely transactional market participants.

This analysis is for informational purposes only and should not be considered investment advice. Uranium market investments involve substantial risks including commodity price volatility, regulatory changes, and geopolitical factors that may affect investment outcomes. Investors should conduct thorough due diligence and consult qualified financial advisors before making investment decisions in the uranium sector.

Considering Investments in Strategic Uranium Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant uranium and critical minerals discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.