July 31, 2026

The Structural Forces Reshaping Global Uranium Markets

Few commodity sectors illustrate the tension between long-cycle capital investment and rapidly shifting demand signals as clearly as uranium. Unlike oil or copper, uranium demand in Southern Africa and globally is not primarily driven by economic growth cycles or industrial activity. It is anchored to something far more durable: the irreversible physics of baseload power generation, where large populations require consistent electricity output regardless of weather conditions, time of day, or seasonal variation. That foundational reality is now colliding with a global energy transition narrative that, after years of overlooking nuclear power, has brought it back to the centre of decarbonisation strategy.

The result is a supply-demand equation that favours producers in ways not seen for nearly two decades, and nowhere is this dynamic more consequential than across Southern Africa's expanding uranium corridor. Understanding uranium supply-demand volatility is therefore essential for anyone tracking this sector with genuine rigour.

When big ASX news breaks, our subscribers know first

Why the Global Nuclear Renaissance Is Different This Time

Previous nuclear revivals have often stalled under the weight of capital cost overruns, public opposition, or energy policy reversals. The current resurgence, however, carries different structural characteristics that give it considerably more staying power.

At COP28 in December 2023, an initial group of approximately 22 nations signed the UAE Consensus, a formal commitment to triple global nuclear capacity to roughly 1,200 gigawatts (GW) by 2050. That coalition has since grown broader as governments across Asia, Europe, and North America have layered nuclear expansion into their national energy frameworks. The distinction that matters for uranium markets is this: the demand these reactors will generate is not discretionary. Once a reactor is commissioned and fuelled, uranium consumption becomes a contractual and operational necessity for decades.

Why Renewables Cannot Replace Nuclear on Their Own

The engineering case for nuclear as a baseload complement to renewables rests on capacity factors. Modern nuclear plants operate at capacity factors exceeding 90%, generating power continuously regardless of grid conditions. By comparison, onshore wind and solar photovoltaic installations typically operate at capacity factors between 25% and 35%, requiring either large-scale storage or complementary baseload sources to maintain grid stability.

As grids incorporate higher proportions of variable renewable generation, the value of firm, dispatchable baseload power actually increases rather than diminishes. This creates an important insight that is frequently underappreciated in mainstream energy commentary: nuclear power and renewable energy are not competing technologies in a well-designed grid. They are complementary ones. The policy trajectory across Europe, Japan, and South Korea reflects growing recognition of this reality, with governments reversing earlier phase-out decisions in favour of life extensions and new-build programmes.

The Supply Contraction Problem

On the supply side, the uranium market faces a structural squeeze driven by decades of underinvestment. Several operating mines globally are approaching the end of their productive lives, and the pipeline of replacement projects is insufficient to offset the decline. The compounding issue is timeline: bringing a new uranium mine from discovery to production typically requires 10 to 15 years when factoring in exploration, feasibility studies, permitting, and construction.

Projects that should have entered development a decade ago, when uranium prices were too low to justify investment, are only now receiving capital. The consequence is a narrowing window between rising reactor demand and contracting mine supply, with the deficit projected to widen materially through the late 2020s. This is the environment in which Southern Africa's production ramp-up is occurring, and the timing carries significant strategic weight.

Southern Africa's Position in the Global Uranium Supply Chain

Africa as a whole contributes approximately 18% of global uranium output, with Southern and East Africa holding the majority of that capacity. What distinguishes the region from other uranium-producing zones is not just the volume of its resource base but the concentration of projects currently moving through construction, commissioning, and early production phases simultaneously. For a deeper look at African uranium and its role in the global nuclear expansion, specialist sources confirm this strategic positioning is well-founded.

| Country | Current Status | Strategic Role |

|---|---|---|

| Namibia | Active and expanding production | Primary regional contributor |

| Malawi | Restarted production (2025) | Emerging supply addition |

| Tanzania | Development stage (commissioning 2029) | Future supply corridor |

| South Africa | Historical producer, legacy infrastructure | Monitoring and maintenance phase |

Why Geological Endowment Matters for Cost Competitiveness

Southern Africa's uranium resources are predominantly hosted in sedimentary and calcrete-type deposits. These deposit types are geologically significant because they tend to occur in large, laterally continuous ore bodies near the surface, characteristics that lend themselves to open-pit extraction with relatively straightforward metallurgical processing. This contrasts with unconformity-associated deposits found in Canada's Athabasca Basin, which deliver exceptionally high grades but require costly underground mining at considerable depth.

The practical implication is a cost structure that, while not matching Kazakhstan's uranium dominance through ultra-low-cost in-situ recovery (ISR) operations, positions Southern African producers competitively against the marginal cost of supply globally. In a rising price environment, lower-grade but lower-cost surface operations can generate attractive margins that are more resilient to price volatility than high-capital underground alternatives.

It is worth noting that deposit grade alone does not determine project economics. Strip ratios, processing recovery rates, water availability, infrastructure proximity, and royalty regimes all contribute to the all-in sustaining cost figure that determines whether a project is genuinely competitive at prevailing uranium prices.

How Namibia Became Africa's Uranium Powerhouse

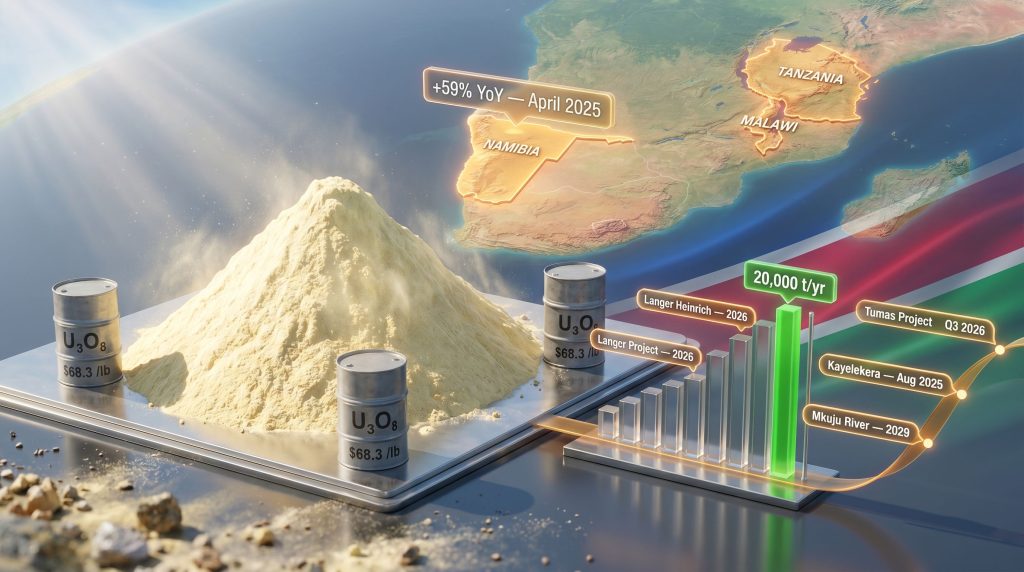

Namibia's emergence as the anchor of Africa's uranium production capacity is the result of deliberate resource development over several decades, but the current phase of expansion represents something qualitatively new. Namibian uranium output recorded a surge of approximately 59% year-on-year in April 2025, a growth rate that reflects the simultaneous ramp-up of restarted and newly commissioned operations rather than incremental improvements at legacy facilities.

National production targets aim to more than double annual output capacity to exceed 20,000 tonnes per year, a level that would position Namibia as the supplier of approximately 10% of global nuclear fuel demand at full capacity. That figure places the country in a tier-one strategic position alongside Canada and Australia as a jurisdiction capable of materially influencing global uranium supply dynamics.

From Raw Commodity Exporter to Nuclear Energy Participant

One of the most underreported dimensions of Namibia's uranium story is the country's presidential-level declaration of intent to pursue negotiations for a domestic nuclear power facility. This represents a fundamental conceptual shift in how Namibia views its uranium endowment: not merely as a mineral resource to be extracted and exported, but as a potential foundation for domestic energy sovereignty.

The implications extend beyond energy policy. If Namibia advances toward domestic nuclear power consumption, a portion of its uranium production would effectively be retained for internal use rather than entering the export market. For utilities negotiating long-term offtake agreements with Namibian producers, this introduces a new variable into supply security calculations. It is precisely the kind of demand-layer addition that does not appear in standard commodity forecasting models and is consequently underpriced by markets.

The Long-Term Contract Dynamic

A structural feature of uranium markets that differentiates them from most other commodities is that the majority of supply does not trade on open spot exchanges. Instead, the bulk of uranium moves through long-term contracts between producers and utility operators, typically spanning 5 to 15 years with fixed or formula-based pricing. This creates a price stickiness effect: when spot prices rise, utilities that locked in contracts at lower prices are insulated, but those seeking new supply must negotiate against current market conditions.

For Southern African producers currently bringing capacity online, the bargaining dynamic is unusually favourable. They are entering the market at a moment when constrained supply has shifted negotiating leverage toward producers, allowing them to secure contract terms that reflect current tight market conditions rather than the depressed pricing of a decade ago. Furthermore, understanding spot and term price divergence is essential context for evaluating how these contracts are likely to be structured going forward.

The Project Pipeline Driving Southern Africa's Uranium Expansion

The breadth of the development pipeline across Southern Africa is one of its most compelling features. No other single region outside Kazakhstan currently has as many uranium projects transitioning from development to production within a compressed multi-year window.

Langer Heinrich Mine, Namibia

Operated by Paladin Energy, Langer Heinrich is one of the world's largest independent uranium operations and is actively targeting a return to full operational capacity by end of 2026. Paladin's Namibia uranium operations have been a closely watched indicator of sector health, and the mine's trajectory toward full nameplate capacity is a key variable in near-term Namibian production totals.

Deep Yellow's Tumas Project, Namibia

Deep Yellow's Tumas project represents a genuine greenfield addition to Namibia's production base rather than the restart of an existing operation. Commissioning is scheduled for Q3 2026, with the project targeting commercial production from a calcrete-hosted deposit. The geological characteristics of Tumas are particularly relevant: calcrete deposits in Namibia's uranium-bearing zones have been extensively studied and generally respond well to heap leach processing, a relatively low-capital extraction method that contributes to competitive operating cost structures.

Kayelekera Mine, Malawi

Kayelekera's operational recommencement in August 2025 marks Malawi's re-entry into the global uranium supply chain after an extended hiatus driven by low uranium prices. Full production capacity is targeted by end of 2026. The restart is significant not just for its supply contribution but for what it signals about investor confidence in Malawian mining governance and the viability of lower-grade operations at current price levels.

Mkuju River Project, Tanzania

Expected commissioning in 2029 positions Tanzania as the next frontier of Southern African uranium development. Mkuju River extends the producing corridor into East Africa and adds geographic diversification to the region's supply profile. Its longer development timeline provides a useful indicator of how the market expects uranium demand to evolve beyond the immediate 2026 commissioning wave.

Between 2025 and 2029, Southern Africa is set to add multiple producing uranium assets to the global supply chain simultaneously. No other region outside Central Asia can currently match this concentration of near-term production additions.

Understanding the Uranium Price Environment

Spot uranium prices have recovered substantially from multi-year lows, with benchmark U₃O₈ prices reaching approximately $68.3 per pound in recent reporting periods. This price recovery reflects both physical market tightening and a reassessment of uranium's strategic value by utilities, financial investors, and sovereign wealth funds that have begun participating directly in upstream asset ownership.

How Uranium Pricing Differs From Other Resource Markets

Several features of uranium market structure are poorly understood outside specialist circles:

-

No centralised exchange: Unlike copper, gold, or crude oil, uranium is not traded in real time on a transparent public exchange. Price discovery occurs through bilateral negotiations and periodic spot tender processes, making market signals slower and less visible.

-

Contract price versus spot price: A utility operator may be purchasing uranium at contract prices negotiated years earlier that bear little relationship to current spot levels. This creates the appearance of price insensitivity in the short term but stores up significant repricing exposure when contracts roll over.

-

Secondary supply effects: Government stockpile releases, downblending of highly enriched uranium (HEU), and underfeeding by enrichment facilities have historically supplemented primary mine supply. These sources are depleting, which means primary mine production must increasingly fill the gap without secondary supply buffers.

-

Enrichment separative work units (SWU): The amount of uranium required to fuel a reactor depends not just on the quantity of uranium ore but on the enrichment level and the efficiency of the conversion and enrichment process. Changes in enrichment economics can shift effective uranium demand independently of reactor count changes.

Project Economics at Current Price Levels

At approximately $68 per pound of U₃O₈, the current price environment is broadly supportive of project economics across Southern Africa's development pipeline. Higher-grade and lower-strip-ratio operations can achieve profitability at considerably lower price thresholds, while newer greenfield developments with higher capital intensity require sustained prices to justify ongoing investment. The critical threshold for most Southern African projects is generally considered to sit in the $50 to $60 per pound range, providing a meaningful margin of safety at current spot levels. Investors seeking broader context on uranium market dynamics will find this pricing context essential for evaluating near-term opportunities.

Disclaimer: Uranium price forecasts and project economic assessments involve significant uncertainty. Investors should conduct independent due diligence and consider the full range of market, operational, and geopolitical risks before making any investment decisions. Past commodity price trends are not indicative of future performance.

The next major ASX story will hit our subscribers first

Infrastructure, Governance, and the Risks That Could Derail the Bullish Case

The enabling conditions for Southern Africa's uranium expansion are real, but they exist alongside structural vulnerabilities that deserve clear-eyed assessment.

Factors Supporting Long-Term Viability

-

Established mining regulatory frameworks in Namibia and South Africa provide a foundation of investment certainty for long-cycle projects requiring multi-decade planning horizons.

-

Port and logistics infrastructure, particularly Namibia's Walvis Bay port and the road and rail connections serving it, provides a workable export pathway for uranium concentrate shipments.

-

A skilled mining workforce with experience across open-pit, underground, and processing operations reduces the human capital risk associated with rapid production scaling.

-

International capital from Australian, Canadian, and European listed mining companies brings both financial capacity and governance standards that underpin investor confidence in regulatory and operational outcomes.

Risks Requiring Active Monitoring

-

Water scarcity: Uranium mining in Namibia's Namib Desert corridor operates in one of the driest environments on Earth. Water availability is a genuine constraint on production scaling, and operations dependent on desalination or long-distance water transfer carry additional cost and operational risk that must be factored into project economics.

-

Capital deployment concentration: Multiple projects requiring simultaneous capital deployment across a single region creates execution risk. Cost overruns or financing delays at one project can affect investor appetite for others in the same geography.

-

Strategic commodity classification: As uranium's strategic importance grows, the potential for export restrictions, preferential supply agreements, or sovereign intervention in pricing terms increases. Namibia's own exploration of domestic nuclear consumption is one early indicator of how this dynamic may evolve.

-

Kazakhstan's pricing power: Kazakhstan controls approximately 43% of global uranium supply through its state-owned enterprise Kazatomprom, primarily via low-cost ISR operations. Any significant expansion or price-discounting strategy from Kazatomprom could compress margins for higher-cost producers elsewhere, including in Southern Africa.

Frequently Asked Questions: Uranium Demand in Southern Africa

Why is uranium demand in Southern Africa rising in significance?

Southern Africa's growing significance in uranium markets is primarily a supply-side phenomenon rather than a domestic demand story. The region is scaling its production capacity in direct response to surging international demand driven by nuclear energy expansion across Asia, Europe, and North America. Uranium demand in Southern Africa as a domestic energy consideration remains nascent, though Namibia's pursuit of a domestic nuclear facility could change this over the longer term.

Which Southern African country produces the most uranium?

Namibia is the dominant uranium-producing nation in the region and ranks among the top producers globally. Its near-60% year-on-year output increase recorded in early 2025 and its ambitious capacity targets place it in a different league from other African producers in terms of near-term supply impact.

What uranium price supports project viability across the region?

Project economics vary by operation, but the current spot price environment around $68 per pound is generally supportive across the Southern African project pipeline. Most operations in the region are considered economically viable at prices above approximately $50 to $60 per pound, providing a buffer against moderate price softening.

How does Southern Africa compare to Kazakhstan as a uranium source?

The comparison is instructive but should not be framed as a direct competition. Kazakhstan produces at a scale and cost level that Southern Africa cannot match in the near term. The strategic value of Southern African production lies in geographic diversification: utilities seeking to reduce supply concentration risk are actively seeking non-Kazakh sources, which positions Southern African producers as premium counterparties in long-term contract negotiations regardless of absolute cost comparisons.

What is the production outlook through 2030?

The outlook is constructive across multiple dimensions. Several major projects are scheduled to reach full production between 2026 and 2029, Namibia's government is pursuing both expanded export capacity and domestic nuclear energy development, and the global pricing environment remains supportive. The primary execution risk is commissioning delays or capital deployment shortfalls that could defer the supply response the market is currently pricing in.

The Strategic Verdict: A Rare Alignment of Conditions

The convergence of structurally rising global nuclear demand, a constrained global supply base, and a concentrated pipeline of Southern African development projects represents an unusually clear alignment of favourable conditions. What makes this moment analytically distinct from previous uranium upcycles is the policy permanence underlying demand growth: reactor construction commitments are multi-decade investments that cannot be easily reversed, creating a demand floor that commodity price volatility cannot easily erode.

Namibia's trajectory from commodity exporter to potential domestic nuclear energy participant is a development that extends well beyond standard mining sector analysis. If realised, it would transform the country's relationship with uranium demand in Southern Africa from a finite extraction resource into the foundation of a long-term national energy architecture, with implications for supply availability, contract structures, and regional energy geopolitics.

For investors, the calculus involves balancing the genuine upside of a well-timed production ramp-up against execution risks that are inherent in large-scale mining development in arid, capital-intensive environments. For policymakers and energy planners, Southern Africa's uranium sector warrants serious strategic attention across the 2025 to 2030 horizon and beyond.

What needs to go right for the bullish case to fully materialise:

-

Timely commissioning of Langer Heinrich, Tumas, and Kayelekera without material cost overruns or operational disruptions.

-

Sustained uranium price support above project breakeven thresholds, maintaining producer margins and encouraging continued capital deployment.

-

Continued international investment appetite for African uranium assets, particularly from Australian and Canadian capital markets that have historically supported the region's development pipeline.

-

Stable governance environments across Namibia, Malawi, and Tanzania, preserving the regulatory certainty that long-cycle mining investments require.

The conditions are in place. Execution is now the determining variable.

This article is intended for informational purposes only and does not constitute financial or investment advice. Uranium markets involve significant commodity price, operational, and geopolitical risks. Readers should seek independent professional advice before making any investment decisions. For ongoing coverage of Southern Africa's uranium sector and broader African mining developments, Mining Weekly provides regular reporting on regional production trends and project developments. Additionally, World Nuclear Association offers comprehensive country profiles and resource data for Africa's uranium-producing nations.

Want to Capitalise on the Next Major Uranium Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including uranium — instantly translating complex geological data into actionable investment insights for traders and long-term investors alike. Explore historic discovery returns to understand the scale of opportunity major mineral finds can generate, and begin your 14-day free trial today to position yourself ahead of the market.