July 14, 2026

The Hidden Architecture of a Commodity Crisis: How One Waterway Controls Global Food Security

Most commodity disruptions unfold gradually, giving markets time to adjust through rerouting, substitution, and inventory drawdown. The 2026 Strait of Hormuz sulphur vessels exit Hormuz after peace deal story broke every one of those assumptions. Within weeks of conflict onset on 28 February 2026, one of the world's most indispensable agricultural raw materials had been effectively cut off at its primary export artery, exposing a structural fragility that fertilizer supply chains had never been forced to confront at this scale.

The confirmation that several sulphur vessels have exited Hormuz after the peace deal is, on its surface, encouraging news. But the details beneath that headline tell a far more complex story, one involving stranded tonnage, unresolved transit permissions, contested toll regimes, and agricultural markets racing against seasonal planting clocks. Furthermore, supply chain disruptions of this magnitude carry consequences that ripple well beyond the immediate crisis period.

When big ASX news breaks, our subscribers know first

Why Sulphur Is the Fertilizer Industry's Most Overlooked Critical Input

Phosphate fertilizers, which underpin the nutritional yields of staple crops across Asia, Africa, and Latin America, cannot be manufactured without sulphur. The production of phosphoric acid, the intermediate compound used to create diammonium phosphate (DAP) and monoammonium phosphate (MAP), requires sulphuric acid as a processing agent. That sulphuric acid is derived almost entirely from elemental sulphur.

Unlike potash or nitrogen, sulphur is not a primary mined commodity in most producing countries. It is predominantly a byproduct of oil and gas refining and processing, which is precisely why the Arabian Gulf holds such structural dominance over global supply. The region's massive hydrocarbon processing infrastructure at facilities including Ruwais (UAE), Ras Laffan (Qatar), Al Zour (Kuwait), and Ras Al-Khair (Saudi Arabia) continuously generates sulphur as a refining byproduct, creating a concentration of export capacity unmatched anywhere else on Earth.

This creates an asymmetry that most commodity risk models underestimate. Because sulphur is a byproduct rather than a primary product, producers cannot simply scale up or down output in response to price signals. Supply is essentially fixed to hydrocarbon processing volumes, meaning any disruption to export logistics creates immediate and inelastic downstream shortfalls. In addition, fertilizer import reliance in key consuming nations amplifies these vulnerabilities considerably.

"Sulphur is categorically non-discretionary in phosphate fertilizer manufacturing. Every tonne of DAP or MAP that cannot be produced due to sulphur unavailability represents a direct reduction in available crop nutrition, with downstream consequences for food production yields."

From Near-Total Freeze to Partial Thaw: The Crisis in Numbers

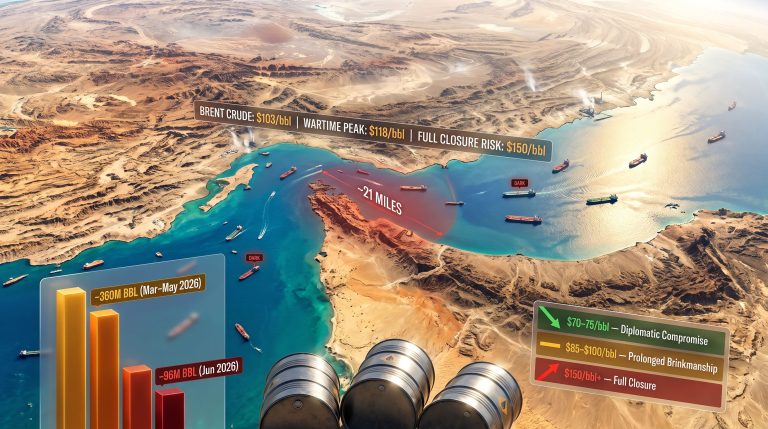

The scale of the supply disruption becomes clear when examining the export data. From conflict onset through mid-June 2026, an estimated 480,000 to 500,000 tonnes of sulphur managed to exit the strait, representing approximately 10% of the region's normal export rate over an equivalent period. The arithmetic is stark: roughly nine out of every ten tonnes of sulphur that would ordinarily have left the Gulf under normal operating conditions simply did not move.

The price consequences were severe and rapid:

| Market Indicator | Pre-Crisis Baseline | Crisis Peak | Post-Deal Signal |

|---|---|---|---|

| Sulphur spot price | ~$200–$250/mt (est.) | ~$710/mt (April 2026) | Declining (June 2026) |

| DAP cfr Pakistan | Below $850/t | Elevated | $925–$950/t (bearish trend) |

| SE Asia amsul cfr | Stable | Elevated | $247.50/t (18 June 2026) |

| Vessels stranded | 0 | 500+ ships | Partial exits underway |

The $710/mt sulphur spot price reached in April 2026 represented a historic high, reflecting a market that had essentially lost access to its dominant supply source. Chinese domestic sulphur prices fell sharply following the June 15 peace deal announcement, functioning as a leading indicator of anticipated supply normalisation, though that normalisation remains far from assured.

Which Sulphur Vessels Have Actually Exited the Strait?

The vessels confirmed as having transited Hormuz since the peace process began fall into two distinct groups, separated by approximately one week.

First Wave: Pre-Deal Transits

| Vessel | DWT | Loading Port | Destination |

|---|---|---|---|

| Nejat | 38,000 | Ras Laffan, Qatar | Bahodopi, Indonesia |

| Abu Al Abyad | 57,000 | Ruwais, UAE | Dar Es Salaam, Tanzania |

| Safeen Al Nasr | 36,600 | Al Zour, Kuwait | Dar Es Salaam, Tanzania |

Second Wave: Post-Deal Transits

According to Reuters, confirmed post-deal vessel movements included the following:

| Vessel | DWT | Loading Port | Destination | ETA |

|---|---|---|---|---|

| Espada X | 88,300 | Ruwais, UAE | Jorf Lasfar, Morocco | 18 July 2026 |

| MV Toro | 55,000 | Ruwais, UAE | Aqaba, Jordan | 28 June 2026 |

| Yan Dang Shan | 63,300 | Ruwais, UAE | Indonesia | TBC |

| Xin Qi Men | 81,600 | Ruwais, UAE | China | TBC |

A critical detail embedded in these movements is frequently overlooked: every confirmed transit to date is understood to represent the fulfilment of pre-existing contractual obligations, not new spot market purchases. This distinction matters enormously. It signals that commercial confidence has not yet been restored to the point where buyers are willing to commit to fresh bookings, as they remain uncertain whether current conditions will hold long enough to guarantee delivery.

Meanwhile, an estimated 500,000 tonnes of sulphur continues to sit loaded aboard vessels still positioned within the strait, the majority committed under earlier contracts and waiting for conditions that permit safe and legally unambiguous transit.

Three Structural Barriers Blocking Full Normalisation

The gap between a political agreement and physical supply chain normalisation is rarely understood by those outside the shipping and commodity trading industries. In the case of Hormuz, at least three distinct operational barriers are preventing anything resembling a rapid return to normal flows.

1. Demining Operations and Physical Safety

Clearing naval mines from a strategically contested waterway is a technically demanding and time-consuming process. Demining operations in the strait are expected to require several weeks to complete. Until maritime safety authorities can certify that the passage is clear, operators of high-value cargo vessels face unacceptable insurance and liability exposure. This constraint also limits inbound traffic into the Gulf, directly suppressing the pace at which fresh DAP and MAP loading operations can resume at Saudi Arabian and UAE export terminals.

2. Transit Permission Ambiguity

On 17 and 18 June 2026, vessel operators who attempted transits were reportedly forced to reverse course when it became apparent that permission status was unresolved. The operational confusion was publicly documented by conflicting statements from the US and Iranian sides. US Central Command indicated no disruption to commercial shipping flows on 20 June, citing 55 merchant vessel transits that day. Iranian authorities, however, maintained that the waterway had been closed to traffic. This kind of jurisdictional ambiguity is precisely the environment in which risk-averse shipowners choose to wait rather than act.

3. The Toll Regime Complication

Iranian state-linked media has reiterated that a traffic toll exercised jointly by Iran and Oman over the strait remains in effect. This introduces a commercial and legal layer of complexity that goes beyond simple physical access. Vessel operators and their charterers face questions about contractual liability, additional costs, and precedent-setting implications of accepting a toll regime that was not part of original freight agreements. US President Trump addressed the toll question on the Truth Social platform, stating there would be no charges during a 60-day negotiating period, though the longer-term position remains unresolved.

"The maintenance of a toll mechanism over one of the world's most critical maritime chokepoints creates a precedent with far-reaching implications for global commodity trade well beyond the current crisis period."

The Geopolitical Conditionality Factor

Layered beneath the operational complexities is an explicit geopolitical condition that Iran has repeatedly articulated: full reopening of the strait is linked to a cessation of Israeli military operations in southern Lebanon. Israeli strikes on Hezbollah positions continued as recently as 19 June 2026, occurring directly after the ceasefire agreement was announced. This conditionality creates a dependency chain that extends well beyond US-Iran diplomacy, involving Israeli strategic decision-making, Lebanese militia posture, and regional security dynamics that no single actor fully controls.

The practical implication is that even a formally signed peace agreement between Washington and Tehran cannot guarantee uninterrupted transit, as demonstrated by the conflicting signals that emerged within days of the deal's announcement. Consequently, geopolitical commodity risks of this nature demand a far more sophisticated risk management response from buyers and producers alike.

The next major ASX story will hit our subscribers first

Pakistan's Agricultural Time Bomb

Of all the countries exposed to the Hormuz sulphur disruption, Pakistan faces arguably the most acute near-term risk. The country's DAP inventories entered June 2026 at approximately 220,000 tonnes, already below the five-year average of 265,000 tonnes for the period.

The demand picture is equally concerning:

- DAP demand in May 2026 reached only 61,000 tonnes, against a five-year average of 94,000 tonnes

- The shortfall reflects demand destruction driven by elevated domestic prices, not genuine reduction in agricultural need

- No DAP imports were recorded in either April or May 2026, as buyers avoided pricing elevated by strait disruption

- Only approximately 64,000 tonnes of DAP was scheduled for June arrival in Pakistan

Running these figures forward through a basic inventory model produces an alarming projection. Using June opening stocks, domestic production estimates, and scheduled June arrivals, Pakistan could enter the October rabi (winter crop) planting season with as little as 61,000 tonnes of DAP in stock. The five-year average for September-end stocks is 335,000 tonnes, implying a potential deficit approaching 274,000 tonnes at the point of highest agricultural demand.

"If Hormuz normalisation is delayed beyond August 2026, Pakistan's farming sector faces a DAP shortage during the October-to-March rabi season that could meaningfully reduce winter crop yields across wheat, oilseed, and pulse cultivation areas."

Pakistan's domestic phosphate producer Fauji reportedly secured its usual phosphoric acid volumes for the second quarter despite tighter Moroccan output linked to sulphur availability constraints, which provided some buffer. However, that buffer is finite, and the country will need to re-enter the import market during the third quarter to avoid a critical agricultural supply gap.

Bearish sentiment in the market has already begun pushing DAP prices down, with the weekly DAP assessment falling to $925–950/t cfr Pakistan in mid-June, reflecting expectations that supply normalisation will eventually materialise even if the timeline remains uncertain.

Indonesia and the Downstream Sulphur Demand Picture

Multiple confirmed sulphur vessels are routing toward Indonesian ports, with Bahodopi emerging as a destination for cargoes originating from Ras Laffan in Qatar. Indonesia's demand for sulphur spans both its nickel processing sector, where sulphuric acid is used in hydrometallurgical refining, and its fertilizer manufacturing base.

State fertilizer producer Pupuk Indonesia closed a tender on 22 June for 100,000 tonnes of ammonium sulphate for August delivery to its subsidiary Pupuk Petrokimia Gresik. Offers were submitted on a formula price basis, with the lowest offer received at approximately $10/t discount to the formula price, though this was not confirmed by the companies involved. Southeast Asian delivered ammonium sulphate prices were assessed at a midpoint of $247.50/t cfr on 18 June 2026, tracking a weakening urea market on a downward trajectory.

Scenario Modelling: Three Possible Hormuz Trajectories

Given the multiple overlapping variables at play, market participants are effectively operating across three broad normalisation scenarios:

| Scenario | Timeline | Sulphur Price Range | DAP Impact | Pakistan Risk |

|---|---|---|---|---|

| A – Rapid Normalisation | 60–90 days | $300–$400/mt | Softening | Manageable |

| B – Gradual Normalisation | 3–6 months | $450–$550/mt | Elevated | High |

| C – Re-Escalation | Indefinite | $700+/mt | Severe spike | Critical |

Scenario A assumes demining completes by August, fresh vessel loadings resume at Gulf export ports, and the backlogged tonnage clears within a single quarter. Under this pathway, sulphur prices retreat materially, Pakistani and Indian buyers secure sufficient Q3 import volumes, and DAP prices soften as upstream cost pressures ease.

Scenario B reflects a more cautious trajectory in which toll disputes, geopolitical conditionality, and incremental transit permission expansion slow full reopening over three to six months. Sulphur prices remain elevated, Pakistan enters October with critically low DAP reserves, and Chinese phosphate producers gain a structural market share advantage as Gulf supply remains partially constrained.

Scenario C involves re-escalation, whether through renewed Israeli-Hezbollah hostilities that trigger Iranian action or a collapse of the US-Iran negotiating framework. Under this pathway, sulphur prices return toward the $700/mt range, alternative supply corridors from Canada, Kazakhstan, and Russia command significant premiums, and the structural case for non-Gulf sulphur sourcing accelerates permanently.

The Long-Term Supply Chain Lesson: Single-Corridor Dependency Is a Systemic Risk

The 2026 Hormuz disruption has forced a reckoning that fertilizer supply chain strategists had long deferred. Routing the vast majority of Middle Eastern sulphur exports through a single 33-kilometre-wide chokepoint is not a logistics strategy — it is a systemic vulnerability. Furthermore, this episode has drawn renewed attention to global industrial demand patterns that create concentrated exposure to single geographies.

The diversification pathways that now command serious attention include:

- Canadian oil sands sulphur, where significant byproduct production capacity exists but export infrastructure toward Asian markets remains underdeveloped

- Central Asian pipeline-associated production from Kazakhstan and Turkmenistan, which can reach South Asian markets via alternative routing but at materially higher logistics cost

- Russian export capacity, which carries its own geopolitical risk profile but represents a volumetrically meaningful alternative source

Beyond supply diversification, the crisis has illuminated the absence of strategic sulphur reserve mechanisms in most importing nations. Countries like Pakistan and India maintain grain buffer stock policies coordinated at the national level, but no equivalent framework exists for sulphur or phosphate fertilizer inputs. The 2026 disruption may catalyse policy development in this area, potentially through multilateral agricultural security frameworks coordinated through bodies such as the FAO or G20 agricultural working groups.

Freight market dynamics have also shifted structurally. War risk insurance premiums for Gulf-loading bulk carriers have risen materially, and shipowners are likely to embed residual geopolitical risk premiums into freight rates for Gulf loadings even after full normalisation, permanently altering the landed cost economics of Middle Eastern sulphur for global buyers. This reality also intersects with broader LNG supply dynamics that are reshaping energy and commodity trade flows across the region.

Frequently Asked Questions

How many sulphur vessels have exited the Strait of Hormuz after the peace deal?

At least seven sulphur-carrying vessels have been confirmed as having transited the strait in the weeks surrounding the June 2026 US-Iran peace agreement, three prior to the deal's announcement and four in the immediate post-deal period. However, the pace of sulphur vessels exit Hormuz after peace deal remains well below what is needed for full market normalisation.

How much sulphur remains stranded in the Strait of Hormuz?

Approximately 500,000 tonnes of sulphur is estimated to remain loaded aboard vessels still positioned within the strait as of late June 2026, the majority committed under pre-existing supply contracts rather than speculative inventory.

Why haven't all sulphur ships exited immediately after the peace deal?

Ongoing demining operations expected to take several weeks, unresolved transit permission protocols, a contested toll regime, and geopolitical conditionality linked to Israeli-Lebanese hostilities are all contributing to a slower-than-anticipated normalisation pace.

Which countries face the greatest agricultural risk from the disruption?

Pakistan faces the most acute near-term risk given its rabi season timing, with India, Indonesia, Morocco, and Brazil also significantly exposed through their reliance on Gulf-sourced sulphur for domestic phosphate fertilizer production and imports.

When could Hormuz sulphur trade fully normalise?

Analysts estimate a range of 60 days to six months from the peace deal signing, contingent on demining completion, sustained geopolitical stability, and resolution of transit toll and permission disputes. None of these factors are currently guaranteed.

This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity price forecasts and scenario projections involve inherent uncertainty and should not be relied upon as the sole basis for commercial or investment decisions. Readers should consult qualified advisors and primary market data sources when making decisions related to fertilizer markets or commodity supply chains. For ongoing sulphur and fertilizer market intelligence, Argus Media publishes regular pricing assessments and market commentary at argusmedia.com.

Want to Stay Ahead of Commodity Supply Shocks Like the Hormuz Sulphur Crisis?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in commodities — including those exposed to the kind of supply chain disruptions reshaping global fertiliser and resource markets. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.