July 24, 2026

Understanding Supply Chain Vulnerabilities in Critical Agricultural Inputs

The global agricultural system operates within a delicate balance of interdependencies that can shift dramatically when major suppliers alter their export strategies. Agricultural inputs, particularly nitrogen-based fertilisers, represent one of the most concentrated commodity markets worldwide, where decisions by a handful of producers can cascade through entire food production systems. This concentration creates systemic vulnerabilities that become apparent during periods of geopolitical tension or strategic resource allocation by major exporting nations.

The fertiliser industry exemplifies how modern agriculture has evolved into a globally integrated system where nearly half the world's population depends on agricultural production using three primary nutrients: nitrogen, phosphate, and potassium. When supply chains for these essential inputs experience disruption, the effects ripple through crop yields, food prices, and ultimately food security for billions of people.

When big ASX news breaks, our subscribers know first

Russia Suspends Fertiliser Exports: Strategic Implications for Global Markets

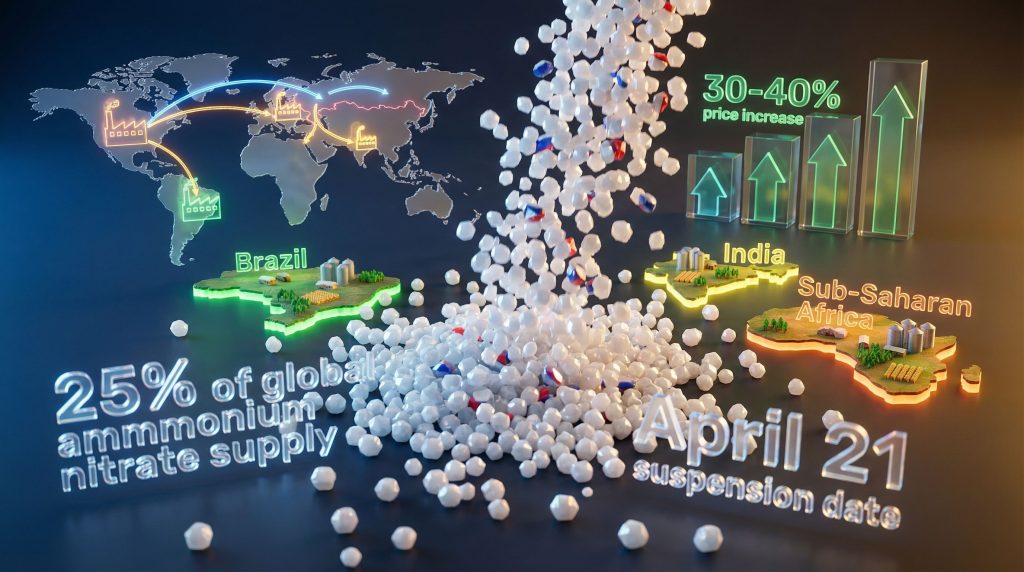

The Russian Federation's decision to Russia suspends fertilizer exports through April 21, 2026, represents a calculated strategic move that prioritises domestic agricultural security over export revenue generation. This suspension affects approximately 25% of global ammonium nitrate supply, creating immediate pressure on international markets already strained by multiple concurrent disruptions.

The Russian Agriculture Ministry implemented this restriction following decisions made by operational headquarters responsible for monitoring nitrogen fertiliser supplies to domestic agricultural producers. According to The Moscow Times, the ministry's framework emphasises that rising export demand necessitates prioritising the domestic market during the critical spring agricultural season to ensure production continuity.

Market Concentration and Strategic Vulnerability

Russia maintains an 18.7% share of global fertiliser exports as of 2023, positioning it as the world's leading fertiliser exporter. This market dominance amplifies the impact of any supply decisions, particularly when combined with similar Russian export restrictions affecting other commodities.

The suspension includes provisions for continuing shipments under existing intergovernmental agreements, creating a two-tier market structure that benefits countries with formal diplomatic arrangements.

Key Statistics:

• Duration: April 21, 2026 temporary suspension period

• Product affected: Ammonium nitrate export licences

• Global impact: 25% of worldwide ammonium nitrate supply

• Exception framework: Intergovernmental agreements remain honoured

• Russia's market position: 18.7% of global fertiliser exports

Geopolitical Disruptions Reshaping Global Fertiliser Trade Networks

Multiple simultaneous supply chain interruptions have fundamentally altered global fertiliser distribution patterns, forcing traders and agricultural producers to rapidly adapt to new realities. The convergence of Russian export suspensions, Chinese restrictions, and maritime transportation constraints creates compound effects that extend far beyond individual disruption sources.

Furthermore, these disruptions occur against a backdrop of existing trade tensions that have already reshaped global commodity flows. The trade war impact on oil markets demonstrates how geopolitical conflicts can create cascading effects across multiple resource sectors.

Transportation Chokepoints and Alternative Routes

The closure of the Strait of Hormuz affects 16 million metric tons of annual fertiliser shipments, representing approximately one-third of global seaborne fertiliser trade. Of this volume, 67% consists of urea, creating particular constraints for nitrogen fertiliser availability worldwide.

This maritime disruption forces traders to seek alternative shipping routes that typically involve longer transit times and higher transportation costs.

Critical Transportation Data:

| Route/Disruption | Annual Volume Affected | Percentage of Global Trade | Primary Fertiliser Type |

|---|---|---|---|

| Strait of Hormuz Closure | 16 million metric tons | 33% seaborne trade | 67% urea |

| Russian Export Suspension | 25% ammonium nitrate | Regional impact | Ammonium nitrate |

| China Export Restrictions | Extended through August 2026 | 30% global production | Urea |

Regional Supply Chain Adaptations

European Union producers face increased pressure to expand capacity utilisation as traditional Russian customers seek alternative suppliers. This demand surge occurs simultaneously with energy cost pressures that constrain European production economics.

North American suppliers experience unprecedented demand from markets previously served by Russian exporters, testing capacity limits and logistics infrastructure. African markets encounter particular challenges due to their combination of limited domestic production capacity and heightened transportation costs resulting from alternative routing requirements.

Latin American agricultural producers actively pursue substitute suppliers ahead of critical planting seasons, creating competitive pressure amongst available exporters.

Economic Drivers Behind Russia's Strategic Fertiliser Policy Evolution

The contrast between Russia's 2022 fertiliser strategy and current export restrictions reveals a fundamental shift in strategic priorities. In 2022, reduced European gas demand created surplus domestic energy resources that Russian producers leveraged to expand ammonia and urea output, consolidating the country's position as the leading global fertiliser exporter.

Strategic Context of Policy Reversal

This earlier expansion strategy capitalised on European gas market disruptions that provided Russian fertiliser producers with competitive advantages through lower input costs. The 2026 suspension represents a reversal of this export-maximisation approach, instead prioritising domestic agricultural input security during peak demand periods.

Strategic Evolution Timeline:

• 2022: Leveraged surplus gas to expand fertiliser production and exports

• 2023: Consolidated position with 18.7% global market share

• 2026: Russia suspends fertilizer exports to prioritise domestic agricultural requirements

Production Economics and Natural Gas Inputs

Fertiliser production, particularly ammonia synthesis, requires substantial natural gas inputs both as feedstock and energy source. The availability and cost of domestic natural gas directly influence production capacity and export potential.

Russia's current policy suggests either increased domestic gas consumption, production capacity constraints, or elevated domestic agricultural demand projections. The ministry's statement emphasising export demand increases indicates that international market conditions could potentially drain domestic supplies below acceptable levels for spring planting requirements.

Identifying Markets with Highest Vulnerability to Supply Disruptions

Import-dependent agricultural economies face asymmetric exposure to fertiliser supply disruptions, with vulnerability levels determined by domestic production capacity, import dependency ratios, and economic resilience to price increases. Nearly half the world's population depends on agricultural production utilising nitrogen, phosphate, and potassium fertilisers, according to UN Food and Agriculture Organisation assessments.

Regional Vulnerability Assessment

Brazil's Agricultural Input Dependencies:

Brazil's soybean and corn production systems rely heavily on imported nitrogen inputs, with domestic fertiliser production insufficient to meet total demand requirements. The country's agricultural expansion model has historically depended on reliable access to international fertiliser markets, particularly for nitrogen supplies traditionally sourced from Russia.

India's Scale and Import Requirements:

India's agricultural sector supports a population exceeding 1.4 billion people while employing approximately 200 million workers directly and indirectly. Despite domestic nitrogen fertiliser production capacity, demand vastly exceeds supply, necessitating substantial imports.

The affordability of imported fertilisers directly impacts smallholder farmer viability and overall agricultural productivity.

Sub-Saharan Africa's Structural Constraints:

The combination of limited domestic production capacity and elevated transportation costs creates compounding constraints for Sub-Saharan African markets. Fertiliser price increases translate directly to reduced agricultural input usage by price-sensitive farmers operating with thin profit margins.

Southeast Asia's Rice Production Systems:

Rice cultivation throughout Southeast Asia depends on reliable nitrogen availability for yield optimisation. These production systems demonstrate limited flexibility to reduce fertiliser inputs without accepting significant yield penalties, creating vulnerability to supply disruptions.

Import Dependency Risk Factors

High-Risk Market Characteristics:

• Limited domestic fertiliser production relative to agricultural demand

• High percentage of agricultural income from export crops requiring intensive fertiliser use

• Smallholder farming systems with limited financial resilience to price increases

• Geographic isolation increasing transportation costs for alternative suppliers

• Limited government capacity to subsidise fertiliser costs during price spikes

Price Dynamics and Market Stress Indicators

Current fertiliser price movements provide quantitative measures of supply chain stress levels across different nutrient categories. Average fertiliser prices have increased by 27% as of March 2026, according to analysis by Global Sovereign Advisory, with nitrogen fertilisers experiencing the most dramatic price escalation at 30-40% above baseline levels.

However, these price pressures interact with broader economic policies. The implementation of US tariff policies has created additional cost burdens on agricultural imports, compounding the fertiliser supply challenges.

Price Impact Analysis by Fertiliser Category

Table: Fertiliser Price Stress Indicators (March 2026)

| Fertiliser Type | Price Increase Range | Primary Disruption Cause | Market Response Pattern |

|---|---|---|---|

| Nitrogen (Urea/Ammonium Nitrate) | 30-40% | Russian suspension + Chinese restrictions | Demand rationing, alternative sourcing |

| Phosphate | 15-25% | Transportation route constraints | Strategic inventory building |

| Potassium | 20-30% | Geopolitical uncertainty effects | Forward contract increases |

| Overall Average | 27% | Multiple simultaneous factors | Market volatility elevation |

Market Response Mechanisms

Agricultural producers respond to fertiliser price increases through multiple adaptation strategies, each carrying distinct economic implications. These responses include application rate reductions (with consequent yield impacts), acceptance of higher input costs, or shifting crop patterns to less fertiliser-intensive alternatives.

The 27% average price increase represents a significant cost shock for agricultural operations worldwide, particularly affecting smallholder farmers in price-sensitive markets. This price elevation approaches levels that can trigger demand destruction in marginal farming operations.

The next major ASX story will hit our subscribers first

Alternative Scenario Analysis for Global Fertiliser Markets

Multiple potential outcomes exist for global fertiliser markets depending on the duration and escalation of current disruptions. Each scenario pathway carries distinct implications for food security, agricultural economics, and trade relationship evolution.

Optimistic Resolution Scenario

Rapid resolution of geopolitical tensions could restore normal trade flows by the third quarter of 2026. This pathway would likely result in price normalisation within 6-12 months, minimal long-term structural changes to market relationships, and return to pre-disruption supply chain patterns.

However, this scenario requires simultaneous resolution of Russian export restrictions, Chinese policy reversals, and maritime transportation constraints.

Extended Disruption Scenario

Prolonged disruptions extending through 2026 planting seasons with gradual stabilisation in 2027 represents a moderate probability outcome. This scenario involves persistent price elevation for 12-18 months, accelerated supply chain diversification efforts, and increased investment in alternative production regions.

Agricultural markets would adapt through efficiency improvements and strategic inventory management. This pathway shares similarities with broader tariff‑induced market shifts affecting global trade patterns.

Structural Transformation Scenario

Permanent alteration of trade relationships due to prolonged geopolitical instability represents the most challenging outcome. This scenario includes structural price increases lasting multiple years, regional food security challenges in vulnerable markets, and fundamental reorganisation of the global fertiliser industry toward regionalised supply chains.

Probability Assessment Framework

Key Variables Determining Scenario Outcomes:

• Duration of Russian export suspension beyond April 2026

• Evolution of Chinese export policy and domestic demand

• Resolution timeline for Strait of Hormuz transportation constraints

• Development of alternative production capacity in non-disrupted regions

• Agricultural sector adaptation speed and efficiency gains

Strategic Market Response and Adaptation Patterns

Industry participants across the fertiliser value chain implement diverse strategies to navigate current uncertainties while positioning for future market stability. These adaptation patterns reflect both short-term crisis management and long-term structural adjustments to supply chain vulnerabilities.

Producer Strategic Responses

Non-disrupted fertiliser producers pursue capacity expansion initiatives to capture market opportunities created by supply constraints. These investments focus on regions with stable energy inputs, reliable transportation access, and supportive regulatory environments.

Long-term supply contracts with strategic buyers provide revenue stability while enabling capacity investment financing. European Union and North American producers face particular opportunities to expand market share, though energy cost constraints and environmental regulations limit rapid capacity additions.

Investment in production technology and efficiency improvements helps optimise existing facility output while reducing input requirements.

Consumer Adaptation Strategies

Agricultural producers implement supplier diversification strategies to reduce dependence on single-source suppliers. This approach involves establishing relationships with multiple fertiliser suppliers across different geographic regions, though often at higher cost structures than previous concentrated purchasing arrangements.

Strategic inventory management becomes critical during periods of supply uncertainty. Forward purchasing and seasonal stockpiling help ensure input availability during critical application periods, though these strategies require additional working capital and storage infrastructure.

Agricultural Technology Adoption:

• Precision agriculture systems optimising fertiliser application rates

• Soil testing programmes identifying specific nutrient requirements

• Variable rate application technology reducing total fertiliser usage

• Organic matter enhancement improving nutrient retention efficiency

Historical Context and Precedent Analysis

The current fertiliser market disruption shares characteristics with previous supply shocks while occurring within a more interconnected and vulnerable global food system. Understanding historical patterns provides insight into potential duration, price trajectories, and market adaptation mechanisms.

In addition, commodity markets have historically demonstrated interconnected behaviour patterns. The current situation bears resemblance to broader energy market volatilities, as evidenced in recent oil price rally analysis examining similar supply-side constraints.

Comparative Historical Analysis

The 2008 global food crisis involved fertiliser price spikes driven primarily by demand surges and speculative trading rather than production constraints. Recovery occurred within 18 months as production capacity expanded and speculative positions unwound.

However, the current situation involves actual supply capacity constraints rather than demand-driven pressure. The 2021-2022 fertiliser disruption resulted from energy cost increases and early geopolitical tensions affecting production economics.

This earlier episode demonstrated the fertiliser market's sensitivity to energy input costs and transportation constraints, with recovery dependent on energy market stabilisation.

Unique Characteristics of 2026 Disruption

The current crisis represents the first instance of simultaneous production constraints, transportation disruptions, and geopolitical tensions affecting multiple major suppliers concurrently. This convergence creates compound effects that exceed the sum of individual disruption sources.

Distinguishing Factors:

• Multiple major exporters implementing supply restrictions simultaneously

• Critical transportation route closures affecting one-third of seaborne trade

• Strategic resource prioritisation by major producers

• Limited spare production capacity available globally

• Agricultural demand seasonality amplifying supply constraints

Market Intelligence and Monitoring Framework

Effective navigation of current market conditions requires systematic monitoring of key indicators that signal potential changes in supply availability, price trajectories, and policy developments. These monitoring frameworks help stakeholders anticipate market movements and adjust strategies accordingly.

Supply-Side Monitoring Indicators

Russian fertiliser production facility operational status provides early signals about potential supply restoration. Government policy announcements regarding domestic agricultural priorities and export licence procedures offer insight into suspension duration and conditions for restoration.

Chinese export policy evolution represents another critical monitoring area, particularly regarding urea export restrictions scheduled to continue through August 2026. According to Bloomberg's coverage, any policy modifications or extensions significantly impact global nitrogen fertiliser availability.

Alternative transportation route capacity and costs provide measures of logistics adaptation progress. Shipping rates for alternative routes compared to standard Hormuz transit indicate the economic feasibility of supply chain diversification.

Demand-Side Indicators

Seasonal planting schedule adherence across major agricultural regions indicates whether farmers maintain normal production patterns despite input cost increases. Delayed or reduced planting signals demand destruction resulting from fertiliser availability constraints.

Crop area allocation decisions by major agricultural producers reflect longer-term adaptation to input cost structures. Shifts toward less fertiliser-intensive crops indicate structural demand changes rather than temporary adjustments.

Critical Monitoring Metrics:

• Weekly fertiliser production rates in major exporting countries

• Export licence issuance and approval volumes

• Alternative shipping route pricing and capacity utilisation

• Agricultural commodity price relationships indicating input cost pressure

• Government subsidy programme announcements and funding levels

Strategic Planning for Agricultural Market Participants

The fertiliser market disruption of 2026 accelerates necessary diversification and resilience-building across global agricultural systems. Strategic planning must account for multiple scenario outcomes while maintaining operational flexibility to adapt as conditions evolve.

Successful navigation of current uncertainties requires understanding that Russia suspends fertilizer exports as part of a broader pattern of resource nationalism affecting global food security. Investment in supply chain diversification, technology adoption, and efficiency improvements provides both short-term adaptation capability and long-term competitive advantages.

The transformation currently underway may ultimately strengthen global agricultural resilience through reduced dependence on concentrated supply sources and improved efficiency in fertiliser utilisation. However, the transition period presents significant challenges requiring coordinated responses from producers, consumers, and policy makers across the international agricultural community.

Disclaimer: This analysis is based on publicly available information and market research as of March 2026. Agricultural commodity markets involve substantial risks, and fertiliser price projections should be considered speculative. Readers should consult with qualified agricultural advisors before making production or investment decisions based on this analysis.

Want to Stay Ahead of Commodity Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of broader market movements during periods of commodity volatility. Explore how major mineral discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, then begin your 14-day free trial today to position yourself advantageously in an evolving resource landscape.