May 21, 2026

Supply Chain Vulnerabilities Expose Critical Market Dependencies

Global commodity markets operate on intricate networks of interdependent supply chains, where concentrated production in specific geographic regions can create systemic vulnerabilities. The aluminium industry exemplifies this phenomenon, with certain regions wielding disproportionate influence over global supply stability despite their relatively modest share of total output. Understanding these concentration risks becomes essential for market participants navigating an increasingly complex geopolitical landscape, particularly as tariffs impact markets and trade tensions escalate.

The mechanics of supply disruption extend beyond simple production capacity arithmetic. When analyzing market impact, the exclusion of dominant producers like China reveals hidden dependencies that standard global production statistics often obscure. Regional clusters of smelting operations, while achieving economies of scale and logistics efficiency, simultaneously create single points of failure that can cascade through international trade networks.

Strategic chokepoints in global shipping lanes compound these vulnerabilities, transforming localised disruptions into far-reaching supply chain crises. The intersection of geopolitical tensions with critical maritime infrastructure demonstrates how quickly established trade patterns can fragment, forcing rapid adaptation across multiple industry sectors and geographic markets.

When big ASX news breaks, our subscribers know first

Critical Infrastructure Dependencies Drive Regional Production Risks

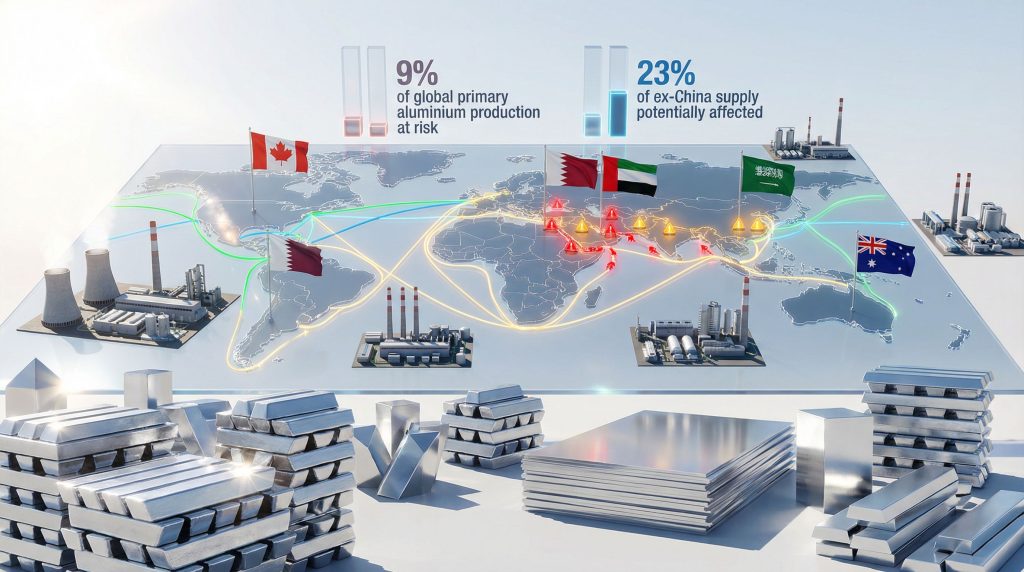

The middle east aluminium supply disruption centers on the vulnerability of the Strait of Hormuz, a maritime corridor through which approximately 4 million tonnes of aluminium materials typically flow annually to regional smelting facilities. This strategic waterway represents more than a shipping route; it functions as a critical artery for raw material flows that sustain Gulf Cooperation Council smelting operations.

Current operational data reveals the immediate impact of these supply chain breakdowns:

- Qatalum facility: Operating at approximately 60 percent capacity

- Aluminium Bahrain (Alba): Three smelting lines offline, representing 19 percent capacity reduction

- Regional production: Gulf smelters collectively produce just under 7 million tonnes annually

- Global significance: Represents 9 percent of worldwide primary aluminium output

The concentration of production capacity within this geographically confined region creates vulnerability that extends well beyond the Middle East itself. When Chinese production is excluded from global calculations, the affected Gulf facilities represent over 20 percent of non-Chinese global supply, fundamentally altering the risk assessment for international markets.

Force majeure considerations now influence operational planning across multiple facilities. Production curtailment strategies have emerged as the primary response mechanism, with individual smelters implementing selective line shutdowns to maintain business continuity while managing raw material supply constraints.

This approach preserves core operational capability while reducing overall output to match available feedstock supplies. The strategic importance of Gulf shipping lanes extends beyond simple tonnage volumes to encompass the specialised infrastructure required for aluminium precursor materials.

Furthermore, bauxite and alumina imports that sustain regional smelting operations depend on port facilities and storage infrastructure specifically designed for these bulk commodities. This creates additional bottlenecks when alternative routing becomes necessary, particularly as critical raw materials supply chains face mounting pressure.

Market Concentration Creates Disproportionate Global Impact

Understanding the true significance of Middle Eastern aluminium production requires analysis beyond absolute tonnage figures. The regional concentration of smelting capacity in the Gulf Cooperation Council countries creates market dynamics that amplify disruption effects across international trade networks.

| Production Metric | Volume/Percentage | Market Context |

|---|---|---|

| Gulf smelter output | 7 million tonnes annually | 9% of global production |

| Non-China market share | Over 20% | Critical supply outside China |

| Affected annual capacity | 1.3 million tonnes at risk | Production slowdowns/stoppages |

| Projected market deficit | 1.9 million tonnes | Global supply shortage estimate |

The dependency relationships become clear when examining customer sourcing patterns. Companies that historically obtained a portion or majority of supply from Middle East smelters now face procurement challenges that extend through the second quarter and second half of 2026.

This timeline suggests that supply chain participants view the disruption as potentially sustained rather than temporary. Raw material import dependencies compound the regional vulnerability, as Gulf smelters rely on specific bauxite and alumina supply chains that flow through the same compromised shipping corridors affecting finished aluminium exports.

This dual dependency creates a feedback loop where both input and output logistics face simultaneous constraint. Export route concentration presents additional risk factors, as the geographic clustering of smelting facilities means that alternative logistics pathways must handle substantially increased volumes when primary routes become unavailable.

Port capacity limitations and specialised handling requirements for aluminium products create additional bottlenecks in supply chain recovery efforts. The regional production model, while efficient under normal operating conditions, demonstrates the inherent trade-offs between cost optimisation and supply security.

Immediate Market Responses Reveal Demand Redistribution Patterns

Supply disruptions trigger immediate behavioural changes across aluminium markets, with demand redistribution patterns emerging as customers scramble to secure alternative sources. The velocity of market response indicates the criticality of affected supply volumes and the limited availability of immediate substitutes.

Order volume increases at alternative suppliers provide direct evidence of demand shifting away from Middle Eastern sources. According to Reuters analysis, Alcoa reports receiving increased customer inquiries related to the second quarter and the second half of the year from companies previously dependent on Gulf smelter output.

This pattern demonstrates proactive risk management as customers attempt to secure supply commitments before availability becomes further constrained. The projected supply shortfall creates mathematical pressure on global markets:

Critical Market Statistics:

- 1.3 million tonnes: Estimated annual production reduction from regional slowdowns

- 1.9 million tonnes: Projected global market deficit

- 20+ percent: Non-Chinese supply exposure to Middle East disruption

- Q2 2026 timeline: Customer inquiry focus for alternative sourcing

Customer procurement behaviour reveals fundamental shifts in decision-making criteria. Supply security considerations now compete directly with traditional cost optimisation in sourcing decisions. Companies that previously balanced price against delivery terms are restructuring procurement frameworks to prioritise availability and supply chain resilience.

Material that would normally flow into the Middle East region is being absorbed by alternative markets, creating secondary effects throughout global trade networks. This redirection places additional demand pressure on non-affected production regions while simultaneously reducing available supply for traditional customers of those alternative sources.

However, the timeline of customer concern extends beyond immediate availability to encompass second half of the year supply security. This forward-looking anxiety suggests market participants anticipate sustained disruption rather than rapid resolution, influencing inventory strategies and long-term contract negotiations across the industry.

Alternative Producers Capitalise on Supply Gap Opportunities

Supply disruptions in one region create corresponding opportunities for producers in unaffected areas, though the capacity to absorb redirected demand varies significantly across alternative sources. The geographical redistribution of aluminium supply reveals both the resilience and constraints within global production networks.

North American producers experience the most immediate benefit from Middle Eastern supply constraints. The material that typically flows into Gulf region smelters now seeks alternative destinations, creating increased demand for North American output. This demand surge tests the ability of regional producers to expand utilisation rates and capture market share previously held by Middle Eastern facilities.

Production capacity utilisation becomes a critical factor in determining which alternative suppliers can benefit most from the supply gap. Facilities operating below maximum capacity possess the flexibility to increase output in response to enhanced demand, while those already at full utilisation face constraints in capturing additional market opportunities.

European smelting operations confront unique challenges in capitalising on Middle Eastern supply disruptions. High energy costs that previously made European production economically disadvantaged may become more acceptable as supply security considerations outweigh cost optimisation in customer procurement decisions.

The economics of restarting idled capacity must be weighed against the expected duration of elevated demand. Canadian and Australian producers benefit from established trade relationships and logistics infrastructure that can accommodate increased export volumes.

Nevertheless, the capacity to rapidly scale production depends on available raw material supplies and existing operational utilisation rates. The competitive dynamics shift as alternative producers compete for suddenly available market share, with long-term customer relationships, production capacity flexibility, and logistics capabilities becoming key differentiators.

Mexican smelter operations represent potential expansion opportunities, though the timeline for capacity increases may exceed the immediate supply shortage period. Investment decisions in facility expansion must consider whether current market disruptions represent temporary opportunities or sustained structural changes in global trade flows.

Asia-Pacific Producers Navigate Complex Market Dynamics

Asia-Pacific producers outside the Middle East face complex market dynamics as regional trade patterns adjust. Chinese producers may increase inventory accumulation as export opportunities expand, while Australian facilities evaluate the balance between domestic market demands and international export opportunities created by Middle Eastern supply constraints.

The regional response patterns indicate how global resources innovation can provide competitive advantages during supply disruptions. Companies with flexible production systems and diversified market access demonstrate superior adaptation capabilities when traditional supply chains fracture.

Industrial Users Implement Emergency Procurement Strategies

End-user industries across multiple sectors face immediate supply chain challenges as middle east aluminium supply disruption filters through the global supply network. The responses reveal both the criticality of aluminium in manufacturing processes and the limited short-term substitution options available to most industrial users.

Automotive manufacturers encounter particular vulnerability due to their just-in-time inventory systems and the essential role of aluminium in modern vehicle production. Supply chain diversification becomes an immediate priority as procurement teams scramble to identify alternative sources for critical components.

The disruption forces automotive OEMs to reevaluate concentrated supplier relationships that previously offered cost advantages. Construction industry impacts manifest through project timeline adjustments and material substitution evaluations. Large infrastructure projects with aluminium-intensive designs face potential delays as material availability becomes uncertain.

Cost escalation management requires balancing immediate procurement at premium prices against project delay expenses. Key industrial adaptations include:

- Supply chain diversification: Expanding supplier bases beyond traditional sources

- Inventory buffer expansion: Increasing strategic stockpiles despite carrying cost implications

- Alternative material evaluation: Assessing substitutes for non-critical applications

- Contract renegotiation: Restructuring long-term agreements to include supply security clauses

- Regional sourcing: Prioritising geographically diverse supplier portfolios

Packaging industry responses focus on can manufacturing supply security, where aluminium represents a critical input with limited substitution options. Beverage companies and packaging manufacturers implement emergency procurement protocols to maintain production continuity while evaluating recycled content optimisation as a supply security measure.

Aerospace and defence contractors face particular challenges due to the specialised aluminium grades required for aircraft manufacturing. The qualification processes for alternative suppliers create additional complexity in supply chain diversification efforts, as new sources must meet stringent quality and traceability requirements.

The electronics industry adapts through component redesign initiatives that reduce aluminium content in non-critical applications while securing premium-priced supply for essential uses. Heat sink manufacturing and electronic housing applications become priorities for available aluminium supplies.

The next major ASX story will hit our subscribers first

Long-Term Structural Changes Reshape Global Trade Architecture

The current supply disruption catalyses structural changes in global aluminium trade patterns that extend far beyond immediate crisis response. Market participants recognise that concentrated production models, while economically efficient, create systemic vulnerabilities that require fundamental reassessment of supply chain architecture.

Geographic diversification emerges as a strategic imperative rather than a risk management option. The revelation that 9 percent of global production can create such significant market disruption when concentrated in a single region drives investment flows toward geographically distributed capacity development.

This shift represents a fundamental change from pure cost optimisation toward resilience-weighted decision making. Investment capital redirection away from geopolitically sensitive regions accelerates as the Middle Eastern supply crisis demonstrates real-world consequences of concentrated exposure.

New capacity development increasingly favours politically stable jurisdictions with diversified energy sources and reliable logistics infrastructure. Strategic stockpiling considerations gain prominence across both government and corporate planning processes. The mathematical reality of 1.9 million tonnes in potential market deficit highlights the importance of buffer inventory systems.

These systems can absorb temporary supply shocks without creating cascading disruptions through industrial supply chains. Alternative transportation route development becomes economically justified by current disruption costs.

| Structural Change Category | Investment Priority | Timeline |

|---|---|---|

| Production diversification | High | 3-5 years |

| Alternative logistics | Medium | 2-3 years |

| Strategic stockpiling | High | 6-12 months |

| Recycling infrastructure | Medium | 2-4 years |

| Technology advancement | Medium | 3-7 years |

Furthermore, overland transportation options, despite higher per-tonne costs, offer supply security benefits that outweigh traditional economic disadvantages. Red Sea alternative corridors and Suez Canal supplementation projects gain investment priority as companies seek route diversification.

Recycling infrastructure expansion accelerates as supply security considerations make secondary aluminium more strategically valuable. The closed-loop potential of aluminium recycling offers independence from primary production vulnerabilities, driving investment in collection, processing, and purification technologies.

Technology Investment and Trade Policy Evolution

Technology investment priorities shift toward production efficiency improvements that can maximise output from geographically secure facilities. Energy efficiency advances become particularly important for justifying production in higher-cost but politically stable regions.

Trade agreement structures evolve to incorporate supply security provisions alongside traditional economic terms. Critical mineral designations and strategic material classifications influence bilateral and multilateral trade negotiations as governments recognise the national security implications of concentrated commodity dependencies.

Risk Management Frameworks Adapt to New Market Realities

Contemporary supply chain disruptions require sophisticated risk management approaches that extend beyond traditional price hedging and inventory optimisation. The middle east aluminium supply disruption demonstrates the inadequacy of conventional risk frameworks when geopolitical events intersect with concentrated production models.

Supply source diversification strategies must balance cost implications against security benefits while maintaining quality standards and delivery reliability. The optimal supplier portfolio increasingly includes geographic, political, and operational diversity metrics alongside traditional price and quality considerations.

Operational flexibility enhancement becomes essential for organisations seeking to maintain continuity during supply disruptions. This includes:

- Production scheduling adaptability: Systems capable of rapid input substitution

- Inventory management optimisation: Dynamic buffer sizing based on supply risk assessment

- Supplier relationship expansion: Maintaining qualified alternative sources even at premium cost

- Contract structure evolution: Force majeure clauses that address geopolitical disruption scenarios

Price hedging mechanisms require recalibration to address supply availability alongside traditional price volatility. Financial instruments that protect against supply shortages, not just price increases, become valuable components of comprehensive risk management portfolios.

Force majeure clause strengthening becomes standard practice in new contract negotiations. The current disruption reveals gaps in traditional contract language that fails to address sustained supply unavailability due to geopolitical events affecting entire production regions.

Strategic partnership formation accelerates as companies recognise the benefits of collaborative supply chain resilience. Joint venture arrangements in geographically stable regions offer shared risk distribution while maintaining individual operational flexibility.

Technology integration enables more sophisticated supply chain monitoring and early warning systems. Real-time tracking of geopolitical developments, shipping route status, and production facility operations allows proactive response to emerging supply chain threats.

Consequently, regional supplier cooperation initiatives develop as alternative producers coordinate capacity expansion and market development efforts. These collaborative approaches help ensure that supply diversification efforts create genuine alternatives rather than simply shifting concentration from one region to another.

Future Market Structure Evolution and Investment Implications

The aluminium industry approaches a structural transformation driven by the recognition that supply chain resilience requires fundamental changes in production geography, logistics networks, and investment priorities. Current disruptions accelerate trends toward decentralised production models that prioritise security alongside economic efficiency.

Market structure changes anticipate regional supply chain configurations that reduce dependence on single-source production clusters. This evolution requires substantial capital allocation toward capacity development in geographically diverse locations, fundamentally altering the industry's investment landscape.

ESG considerations increasingly incorporate geopolitical stability assessments alongside traditional environmental and governance metrics. Investment flows favour jurisdictions with stable political frameworks, diversified energy sources, and reliable legal systems that protect long-term capital commitments.

Renewable energy-powered smelting capacity gains investment priority as sustainability requirements intersect with supply security considerations. Facilities powered by wind, solar, and hydroelectric sources offer both environmental benefits and reduced exposure to fossil fuel supply disruptions.

These facilities can compound aluminium production vulnerabilities, particularly as US‑China trade tensions continue to influence global supply chains. Critical mineral designation policies influence government approaches to strategic material security.

Legislative frameworks increasingly recognise aluminium's role in national economic security, potentially leading to domestic production incentives and strategic reserve programs. Technology advancement acceleration focuses on production efficiency improvements that maximise output from secure facilities.

Advanced smelting technologies, artificial intelligence optimisation, and automated production systems become investment priorities for maintaining competitiveness while operating in higher-cost but stable regions. The recycling sector experiences enhanced strategic importance as secondary aluminium offers supply chain independence from primary production vulnerabilities.

Market Valuation and Investment Strategy Adaptation

Investment in advanced sorting, processing, and purification technologies transforms recycling from waste management into strategic resource security. Trade policy evolution incorporates supply chain resilience considerations into international agreements.

Bilateral and multilateral arrangements increasingly address critical material security alongside traditional economic terms, reflecting recognition of commodity supply chains as national security infrastructure. Moreover, market participants must adapt investment strategies to accommodate the new reality where supply security commands premium valuation.

Companies demonstrating robust supply chain diversification and operational resilience attract investment flows from institutions prioritising long-term stability over short-term cost optimisation. This trend intersects with broader concerns about inflation and debt pressures affecting global economic stability.

According to CNBC analysis, these structural changes represent more than temporary market adjustments. The fundamental shift toward supply security over pure cost efficiency signals a permanent evolution in how global commodity markets operate and evaluate risk.

The middle east aluminium supply disruption serves as a catalyst for this transformation, demonstrating that geographic concentration creates vulnerabilities that extend far beyond the affected regions themselves.

This analysis is based on publicly available market data and industry reports. Investment decisions should consider multiple factors and professional financial advice. Supply chain disruptions involve complex geopolitical and economic variables that may develop differently than current projections suggest.

Looking for Opportunities in Supply Chain Disrupted Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities that emerge during market volatility and supply chain disruptions. Begin your 14-day free trial today to position yourself ahead of the market when global disruptions create new investment possibilities.